Download presentation

Presentation is loading. Please wait.

1

Planning For the Future Financial Literacy Copper Hills High School

2

INSURANCE

3

Health Insurance Provides protection against financial losses resulting form injury, illness, and disability Provides coverage for Medical expenses, emergency and routine Hospital expenditures Surgeries Dental Vision Prescriptions Check you parent’s or guardian’s plan to see how long you can be covered

4

HMO Health Managed Organization Limits the number of doctors, hospitals, and clinics you can use Usually pays a larger portion of the bills

5

Cobra Insurance Allows you to purchase insurance from your former employer for a period of time. You must pay the entire premium amount

6

Future of Health Insurance Congress is currently working on changing health insurance. The new legislation : Requires all employers to provide health insurance Eliminates Pre-Existing Clauses by 2014 Allow individuals to stay on parents’ plan until they turn 26 Requiring states to offer health insurance

7

Life Insurance A contract specifying a sum to be paid to a beneficiary upon the insured’s death Term Life Insurance You are only insured for a period of time. Usually cheaper premiums that are only paid for the period of insured time Whole Life Insurance Pay premiums until death or age 100 Insured until you die

8

Disability Insurance Replaces a portion of one’s income if they become unable to work due to illness or injury Must be purchased through your employer

10

RETIREMENT

11

How long will your money need to last? 65 year old man 41% chance of living to age 85 20% chance of living to age 90 65 year old woman 53% chance of living to age 85 32% chance of living to age 90 Source: Vanguard.com

12

What if there are two of you? If husband and wife are each 65 years old, the probability of one spouse living to age…7099.5% 7597.2% 8090.6% 8575.9% 9050.3% 9522.1% Source: Milevsky and Abaimova, “Applied Risk Management During Retirement,” June 19, 2005, Society of Actuaries RP-2000 table.

13

Government Funded Options

14

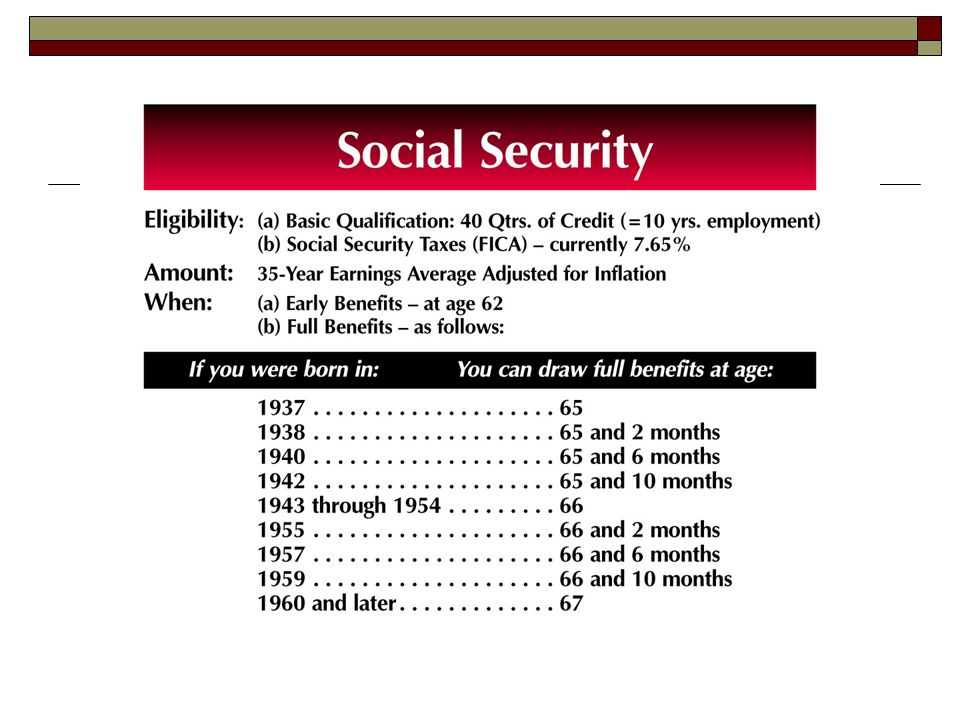

Social Security A government plan where approximately 42% of your average earnings is paid to retired individuals, disabled individuals, or survivors To become eligible, you must pay into the system Benefits are determined by Number of years of service Your average level of earnings An adjustment for inflation

16

Disability Benefits Disability benefits are given to those who experience a physical or mental impairment that is expected to result in Death A job situation where they can not earn more than $500 a month.

17

Survivor Benefits Provided if the breadwinner of the family dies Includes a small lump-sum payment to help with funeral costs. Can include monthly payment if: Spouse is over 60 Spouse is caring for children under 16 Children are under 18 they can get a monthly payment until they turn 18

18

Private Retirement Funding Options Saving Enough to Live on In the Future

20

Employer Funded Pensions Employees receive a promised payout at retirement Noncontributory Plan Employees do no have to pay anything into the plan Contributory Plan Employees help fund part of the plan Must work at a company for a specified number of years to get the benefit Rare to find now

21

Profit Sharing Plans A pension plan in which the company’s contributions vary from year to year depending on the firm’s performance The employee’s salary determines how much they will receive

22

401(k) Plan A tax-deferred retirement plan where both the employer and the employee put in a portion of their salary into an investment account The money is invested in mutual funds Incur a penalty if you access the funds before you retire Money is not taxed until you withdrawal it

Plan A tax-deferred retirement plan where both the employer and the employee put in a portion of their salary into an investment account The money is invested in mutual funds Incur a penalty if you access the funds before you retire Money is not taxed until you withdrawal it")

23

Keogh Plan Self-employment retirement plan Offered through financial institutions Can be contributory or non-contributory

24

Individual Retirement Arrangements (IRAs) A retirement account to which an individual can contribute up to $4000 in 2007, $5000 in 2008 and increased by $500 each year after Usually invested in mutual funds You are penalized if you take money out before age 59 ½ You must start taking money by at 70 ½ Contributions are not taxed Withdrawals are taxed

A retirement account to which an individual can contribute up to $4000 in 2007, $5000 in 2008 and increased by $500 each year after Usually invested in mutual funds You are penalized if you take money out before age 59 ½ You must start taking money by at 70 ½ Contributions are not taxed Withdrawals are taxed")

25

Roth IRA Similar to a traditional IRA Contributions are taxed Withdrawals are tax free as long as you have had the Roth IRA for at least 5 years

26

The Payout Options

27

Single Life Annuity Receive a set monthly payment for your entire life Payments stop when you die

28

Annuity for Life or a “Certain Period of Time” Receive a set monthly payment for a fixed amount of time Even if you die, the payments will still keep coming for that amount of time

29

Joint and Survivor Annuity Receive payment until either you or your spouse dies The payment amount is reduced by as much as 50%

30

Lump Sum Payment Receive all retirement benefits in one single payment If you are not careful, you could run out of money before you die The rule of thumb is not to spend more than 4% of your nest egg per year for your savings to last through retirement.

31

Estate Planning What happens to your wealth after you die

32

Steps to the Process Determine the value of your estate Choose your heirs and decide what they will receive Determine the cash needs of the estate Taxes, Funeral Expenses, Medical Expenses, etc. Create a plan

33

Wills Legal documents describing How you want your property to be transferred Your beneficiaries The executor Guardian for your children

34

Joint Ownership When assets are owned jointly, they’re transferred to the surviving owner(s) without going through probate Probate is the process of validating the will through the court system

without going through probate Probate is the process of validating the will through the court system")

35

Trusts A legal entity in which some of your property is held for the benefit of another person Reduce the amount of estate taxes you will owe Ensure that your wishes are granted

Similar presentations

Plan Annuity Defined-Benefit Plan Defined- Contribution Plan Employer- Sponsored Retirement.>")

Define the characteristics of a tax- favored savings program Explain the key features of the different IRA programs.>")