Download presentation

Presentation is loading. Please wait.

1

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-1 Process Cost Accounting Chapter 20

2

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-2 Learning objectives 1.Process Operation 2.Process Cost Accounting 3.Equivalent Units of Production 4.Process Costing Illustration – GenX Company 5.Hybrid Costing System 6.Process Costing Typical Accounting Entries

3

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-3 Used for production of small, identical, low-cost items. Mass produced in automated continuous production process. Costs cannot be directly traced to each unit of product. Used for production of small, identical, low-cost items. Mass produced in automated continuous production process. Costs cannot be directly traced to each unit of product. 1. Process Manufacturing Operations

4

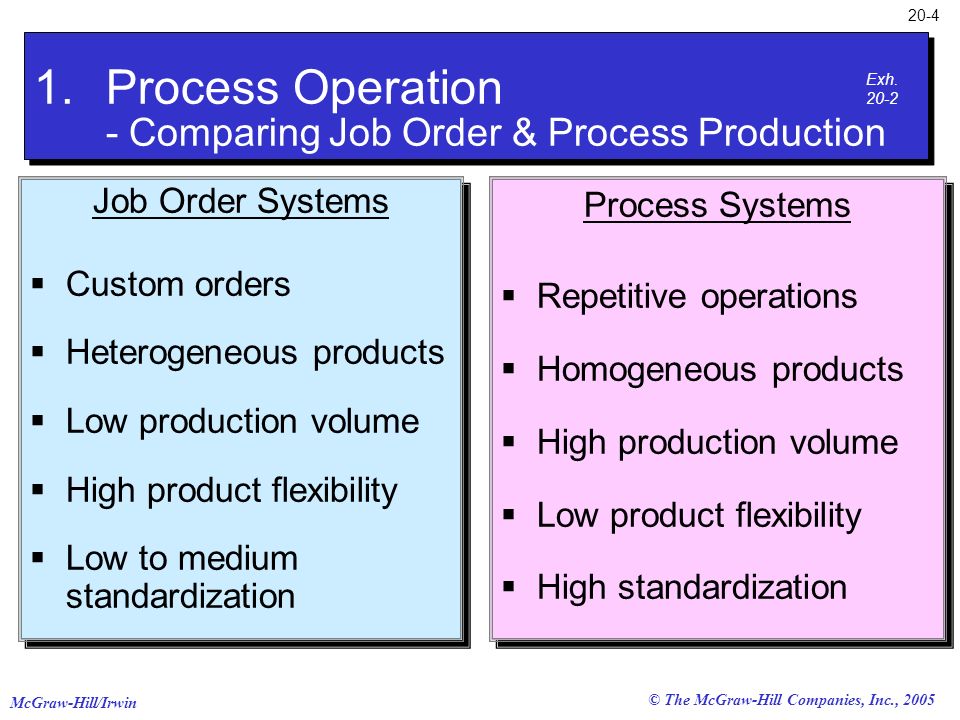

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-4 Job Order Systems Custom orders Heterogeneous products Low production volume High product flexibility Low to medium standardization Job Order Systems Custom orders Heterogeneous products Low production volume High product flexibility Low to medium standardization Process Systems Repetitive operations Homogeneous products High production volume Low product flexibility High standardization Process Systems Repetitive operations Homogeneous products High production volume Low product flexibility High standardization 1.Process Operation - Comparing Job Order & Process Production Exh. 20-2

5

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-5 Direct Materials Finished Goods Cost per unit for each job Direct Labor Factory Overhead Jobs The Goods in Process account consists of individual jobs in a job order system. 2. Process Cost Accounting - Comparing Job Order & Process Production

6

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-6 Direct Materials Finished Goods Direct Labor Factory Overhead Processes The Goods in Process account consists of specific processes in a process cost system. Cost per unit processed 2. Process Cost Accounting - Comparing Job Order & Process Production

7

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-7 Same objective: to determine the cost of products Same inventory accounts: raw materials, work in process, and finished goods Same overhead assignment method: predetermined rate times actual activity 2. Process Cost Accounting - Job and Process Costing Similarities

8

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-8 Costs are accumulated for a period of time by process or department. Unit cost is computed by dividing the accumulated costs by the number of equivalent units produced in the period. 3. Equivalent Units of Production

9

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-9 Equivalent units is a concept expressing a number of partially completed units as a smaller number of fully completed units. Two one-half full pitchers are equivalent to one full pitcher. + = Equivalent Units of Production

10

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-10 For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did PencilCo have for the period? a.10,000 b.11,500 c. 1,500 d. 15,000 For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did PencilCo have for the period? a.10,000 b.11,500 c. 1,500 d. 15,000 Question

11

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-11 For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did PencilCo have for the period? a.10,000 b.11,500 c. 1,500 d. 15,000 For the current period, PencilCo started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did PencilCo have for the period? a.10,000 b.11,500 c. 1,500 d. 15,000 10,000 units + (5,000 units ×.30) = 11,500 equivalent units Question

= 11,500 equivalent units Question.")

12

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-12 Cost per equivalent unit = Product costs for the period Equivalent units for the period Cost Per Equivalent Unit

13

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-13 Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period? a.$1.84 b.$2.40 c.$2.76 d.$2.90 Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period? a.$1.84 b.$2.40 c.$2.76 d.$2.90 Question

14

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-14 Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period? a.$1.84 b.$2.40 c.$2.76 d.$2.90 Now assume that PencilCo incurred $27,600 in production costs. What was PencilCo’s cost per unit for the period? a.$1.84 b.$2.40 c.$2.76 d.$2.90 $27,600 ÷ 11,500 equivalent units = $2.40 per equivalent unit Question

15

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-15 Equivalent units may be different for material and labor and overhead at different stages of a process. At completion of Stage 1 of the process, material is 40% complete, but labor and overhead are only 25% complete. Stage 1 40% of Material 25% of Labor and Overhead Equivalent Units

16

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-16 Stage 2 25% of Labor and Overhead 60% of Material Stage 1 40% of Material 25% of Labor and Overhead + + = = 100% 50% Equivalent Units

17

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-17 Stage 3 50% of Labor and Overhead The process is now complete. Stage 2 25% of Labor and Overhead 60% of Material Stage 1 40% of Material 25% of Labor and Overhead Equivalent Units

18

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-18 GenX makes a product called Profen in two departments, Grinding (G) and Mixing (M). 4. Process Manufacturing Operations - GenX Example

19

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-19 Goods in Process Grinding Labor Materials Indirect Factory Overhead Direct Delivered to Customers Goods in Process Mixing Finished Goods Applied Overhead Process Manufacturing Operations GenX Exh. 20-5

20

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-20 Let’s look at actual units processed and actual costs incurred for GenX. Accounting for GenX

21

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-21 Accounting for GenX Exh. 20-12

22

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-22 Exh. 21-5B Accounting for GenX Exh. 20-12

23

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-23 GenX uses a FIFO cost flow system with the following four steps: Physical flow of units. Computing equivalent units of production. Computing cost per equivalent unit. Cost reconciliation. GenX uses a FIFO cost flow system with the following four steps: Physical flow of units. Computing equivalent units of production. Computing cost per equivalent unit. Cost reconciliation. Accounting for GenX

24

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-24 Physical Flow of Units Exh. 20-13

25

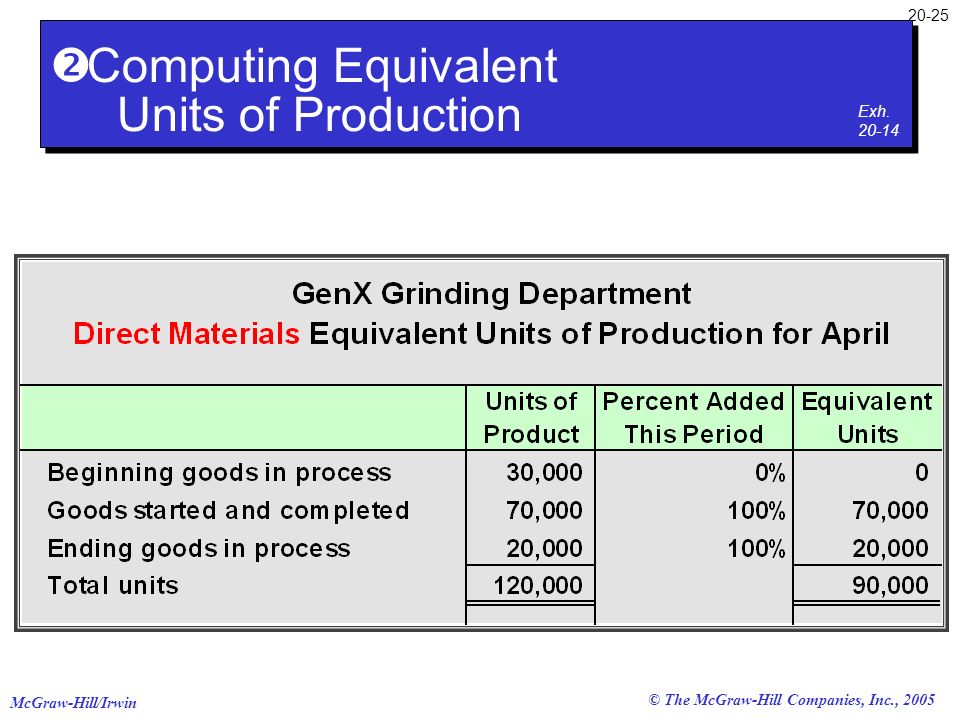

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-25 Computing Equivalent Units of Production Exh. 20-14

26

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-26 } 100,000 100,000 units transferred from grinding to mixing. Computing Equivalent Units of Production Exh. 20-14

27

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-27 Since materials are added at the beginning of the process in Grinding, no additional materials are necessary to complete the beginning inventory. Computing Equivalent Units of Production Exh. 20-14

28

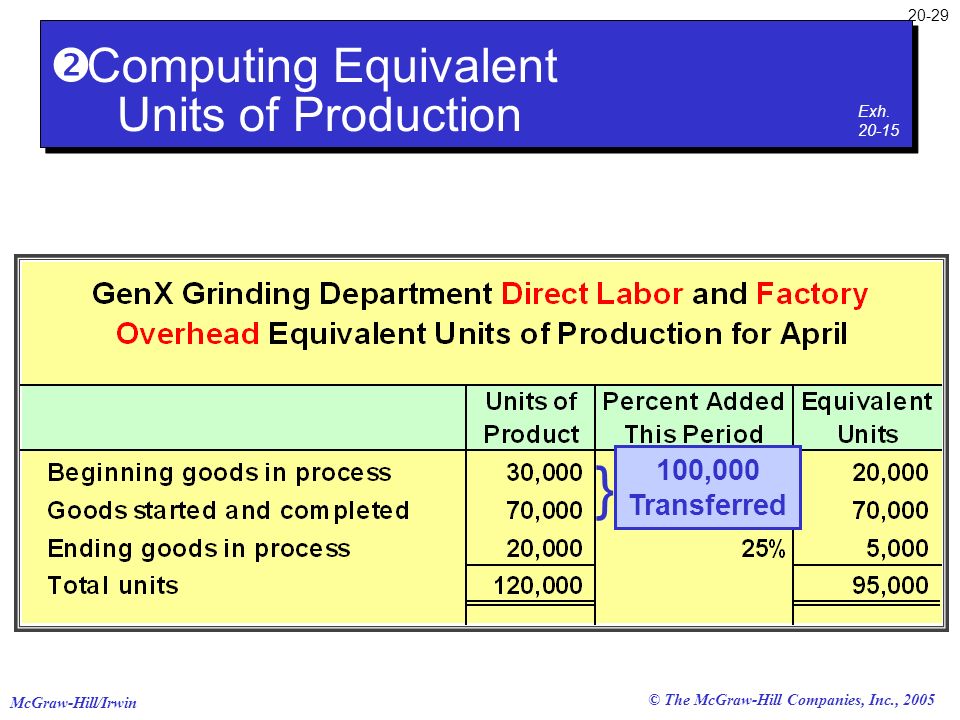

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-28 Computing Equivalent Units of Production Exh. 20-15

29

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-29 } 100,000 Transferred Computing Equivalent Units of Production Exh. 20-15

30

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-30 Since labor and overhead were 33 1 / 3 percent complete in the beginning inventory, 66 2 / 3 percent of the work must be completed in April. Computing Equivalent Units of Production Exh. 20-15

31

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-31 Computing Equivalent Units of Production Exh. 20-16

32

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-32 Computing Equivalent Units of Production Exh. 20-17

33

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-33 In the cost reconciliation, we will account for all costs incurred by assigning unit costs to the: A. 100,000 units transferred from grinding to mixing. B. 20,000 units remaining in ending inventory. In the cost reconciliation, we will account for all costs incurred by assigning unit costs to the: A. 100,000 units transferred from grinding to mixing. B. 20,000 units remaining in ending inventory. Cost Reconciliation

34

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-34 Exh. 20-18

35

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-35 Exh. 20-18

36

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-36 Exh. 20-18

37

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-37 Exh. 20-18

38

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-38 Process Cost Summary Helps managers control their departments. Provides cost information for financial statements. Shows the flow of units and costs through work in process. Helps factory managers evaluate department manager performance.

39

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-39 We will illustrate the process cost summary for the Grinding Department of GenX in three sections: Costs charged to department. Equivalent unit processing costs. Assignment of costs to output of department. We will illustrate the process cost summary for the Grinding Department of GenX in three sections: Costs charged to department. Equivalent unit processing costs. Assignment of costs to output of department. Process Cost Summary

40

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-40 Process Cost Summary Exh. 20-19

41

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-41 Exh. 20-19

42

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-42 Exh. 20-19

43

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-43 Exh. 20-19

44

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-44 Exh. 20-19

45

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-45 Current period unit costs Exh. 20-19

46

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-46 Total costs transferred to Mixing $6,350 + $15,050 = $21,400 Exh. 20-19

47

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-47 Total costs transferred to Mixing $6,350 + $15,050 = $21,400 $21,400 ÷ 100,000 units transferred = $0.214 Exh. 20-19

48

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-48 These unit costs differ because the $0.214 contains costs incurred in March that differed in amount from costs incurred in April. Exh. 20-19

49

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-49 Accounting for GenX Exh. 20-21

50

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-50 Material, labor and overhead are added at the same rate in Mixing. Accounting for GenX Exh. 20-21

51

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-51 GenX Mixing Department Equivalent Units of Production Exh. 20-22

52

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-52 75 percent added to complete the units in beginning inventory. GenX Mixing Department Equivalent Units of Production Exh. 20-22

53

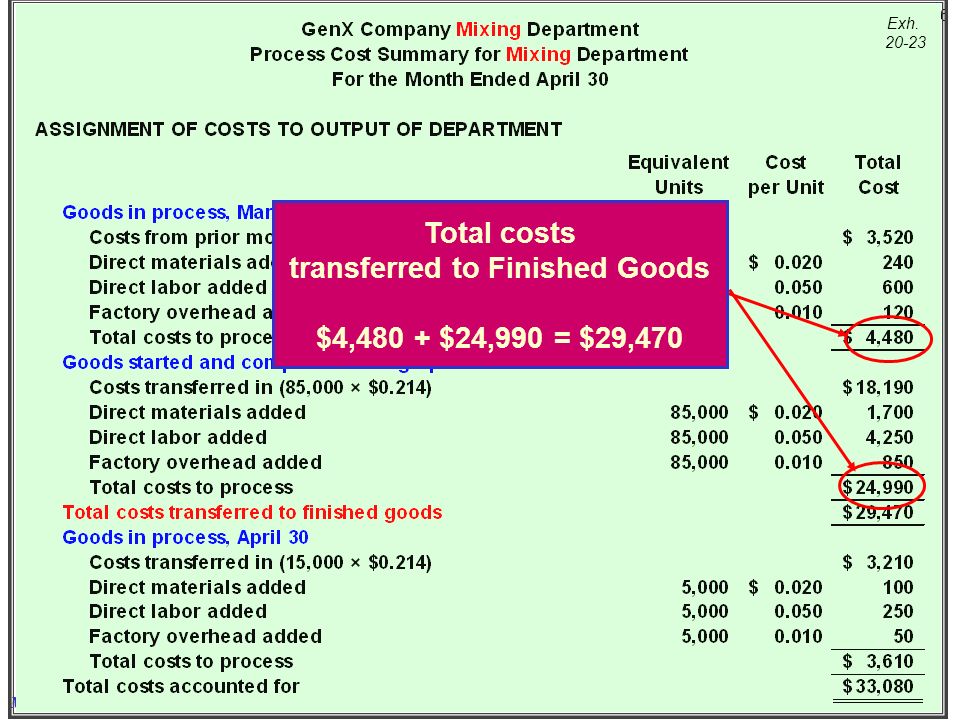

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-53 Process Cost Summary Exh. 20-23

54

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-54 Exh. 20-23

55

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-55 Exh. 20-23

56

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-56 Total costs transferred to Finished Goods $4,480 + $24,990 = $29,470 Exh. 20-23

57

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-57 Total costs transferred to Finished Goods $4,480 + $24,990 = $29,470 Unit cost = $29,470 ÷ 101,000 units transferred = $0.2918 (rounded) Exh. 20-23

58

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-58 Hybrid costing systems contain features of both job order and process operations. Job Order Costing Process Costing Hybrid Costing Material costs are accounted for using a job order system. Conversion costs are accounted for using a process system. 5. Hybrid Costing Systems

59

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-59 Let’s look at the accounting journal entries for a process cost system. We’ll omit the numbers so that we can focus on accounts. 6. Process Costing Typical Accounting Entries

60

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-60 Process Costing Typical Accounting Entries

61

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-61 Process Costing Typical Accounting Entries

62

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-62 Process Costing Typical Accounting Entries

63

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-63 Process Costing Typical Accounting Entries

64

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-64 Process Costing Typical Accounting Entries

65

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-65 Process Costing Typical Accounting Entries

66

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-66 Process Costing Typical Accounting Entries

67

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-67 Process Costing Typical Accounting Entries

68

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-68 Process Costing Typical Accounting Entries

69

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-69 Process Costing Typical Accounting Entries

70

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-70 Process Costing Typical Accounting Entries

71

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 20-71 End of Chapter 20

Similar presentations

>")