Download presentation

Presentation is loading. Please wait.

1

Rajesh Kevin Sanjay Earning Per Share IAS 33

2

History Objectives Scope Requirement for E.P.S Terms Used in E.P.S Disclosure Meaning of E.P.S Benefits of E.P.S Types of E.P.S Overview

3

Company’s earning Common Stock allocation Profitability Earning Per Share

4

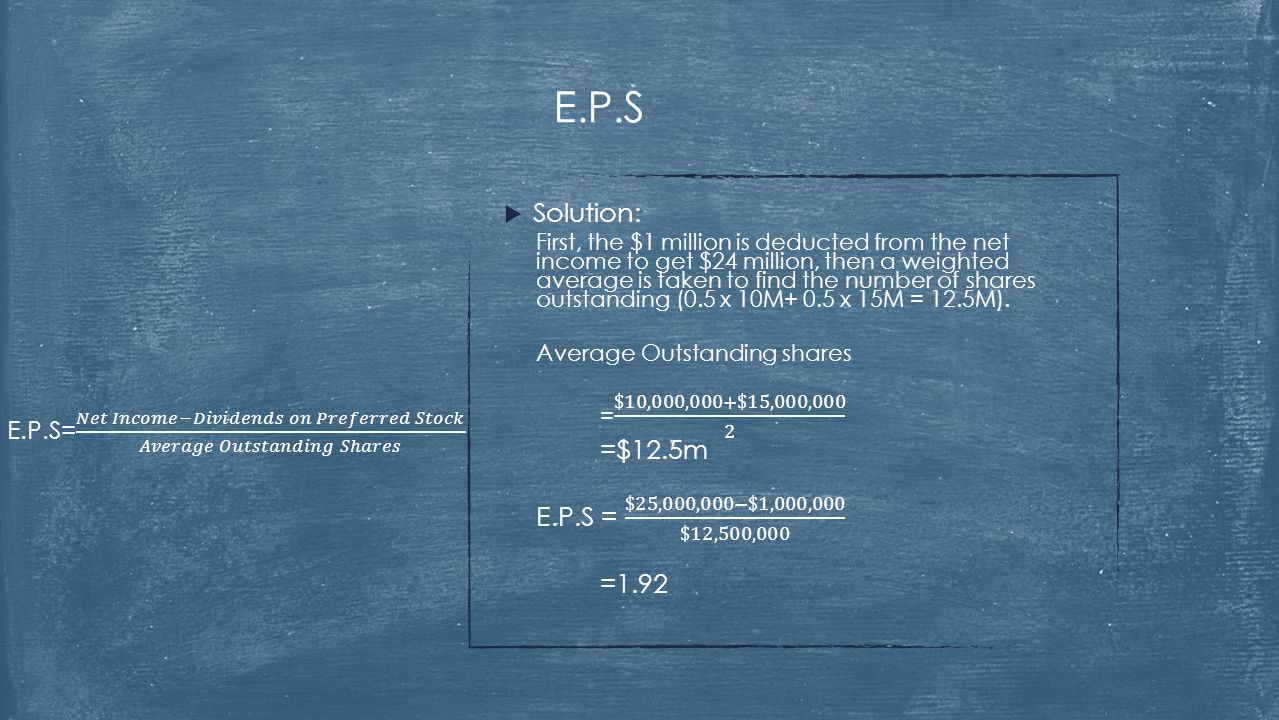

For example, Assume that a company has a net income of $25 million. If the company pays out $1 million in preferred dividends and has 10 million shares for half of the year and 15 million shares for the other half, the EPS would be $1.92). E.P.S

. E.P.S.")

6

Calculation of Income Time Series Earning vs. Dividends Advantages/ Benefits of E.P.S

7

Basic Earning Per Share Diluted Earning Per Share Types of E.P.S

8

January 1996Exposure Draft E33 Earnings Per Share February 1997IAS 33 Earnings Per Share 1 January 1999Effective date of IAS 33 (1997) 18 December 2003 Revised version of IAS 33 issued by the IASB 1 January 2005Effective date of IAS 33 (Revised 2003) 7 August 2008IASB proposes to amend IAS 33. 1 January 2009 Effective date of consequential amendments arising from IAS 1 (2007) History of IAS 33

History of IAS 33.")

9

Prescribe Principles and Presentation of E.P.S Improve Performance Comparison Objective

10

This Standard shall apply to: the separate or individual financial statements of an entity: whose ordinary shares or potential ordinary shares are traded in a public market or, that files, or is in the process of filing, its financial statements with a securities commission or other regulatory organisation for the purpose of issuing ordinary shares in a public market; and Scope

11

The consolidated financial statements of a group with a parent: whose ordinary shares or potential ordinary shares are traded in a public market local and regional markets) or that files, or is in the process of filing, its financial statements with a securities commission or other regulatory organisation for the purpose of issuing ordinary shares in a public market. Scope

12

Profit or loss from continuing operations attributable to the ordinary equity holders of the parent entity, Profit or loss attributable to the ordinary equity holders of the parent entity for the period for each class of ordinary shares that has a different right to share in profit for the period. Requirement to Present E.P.S

13

Antidilution A contingent share agreement Contingently issuable ordinary shares Dilution Options, warrants and their equivalents Terms Used in IAS 33

14

An ordinary share A potential ordinary share Put options on ordinary shares Terms Used Cont’d

15

Disclosure Disclosure in the notes Discontinued operations ReconciliationsAdjusted

16

IAS 34 : Interim Financial Reporting Questions & Discussion

Similar presentations

>")

is an important number. Understand when.>")