Download presentation

Presentation is loading. Please wait.

1

What Is Next for US Economy presented by Rodney Johnson Dent Research Boom & Bust Survive and Prosper

2

Data Source: Bureau of Economic Analysis, 2012 Real Personal Consumption Expenditures 1995-2012 Billions of Chained 2005 Dollars Missing Growth

3

18-22 Single 22-30 Young Married 31-42 Young Family 46-50 Family, College Kids 50+ Empty Nesters 60+ Retired Changes in Spending at each Age & Stage of Life Spending By Age

4

Immigration Adjusted Birth Index Immigration Adjusted Births

5

Spring Summer FallWinter Stocks/ Economy Generation Spending Boom Consumer Prices/ Inflation Simple Four Season Economic Cycle Eighty Years in Modern Times Source: HS Dent

6

Daily Consumer Spending 2008-2012 Data Source: Gallup.com, 2012

7

Not Soup Lines Like This

8

Instead, In the Mail

9

Americans on Disability

10

Tough Road Ahead for Jobs

11

Fall in Real Median Household Income Since 2000 Index 100= 2000 Data Source: U.S. Census Bureau, 2012

12

Drop in Pay for Re-Employed % of Re-Employed That Lost Pay Amount of Pay Reduction Data Source: “Out of Work and Losing Hope: The Misery and Bleak Expectations of American Workers,” Cliff Zukin, Carl Van Horn, Charley Stone. 9/2011

13

Drop in Pay for Re-Employed by Age % of Re-Employed Amount of Pay Reduction Data Source: “Out of Work and Losing Hope: The Misery and Bleak Expectations of American Workers,” Cliff Zukin, Carl Van Horn, Charley Stone. 9/2011

14

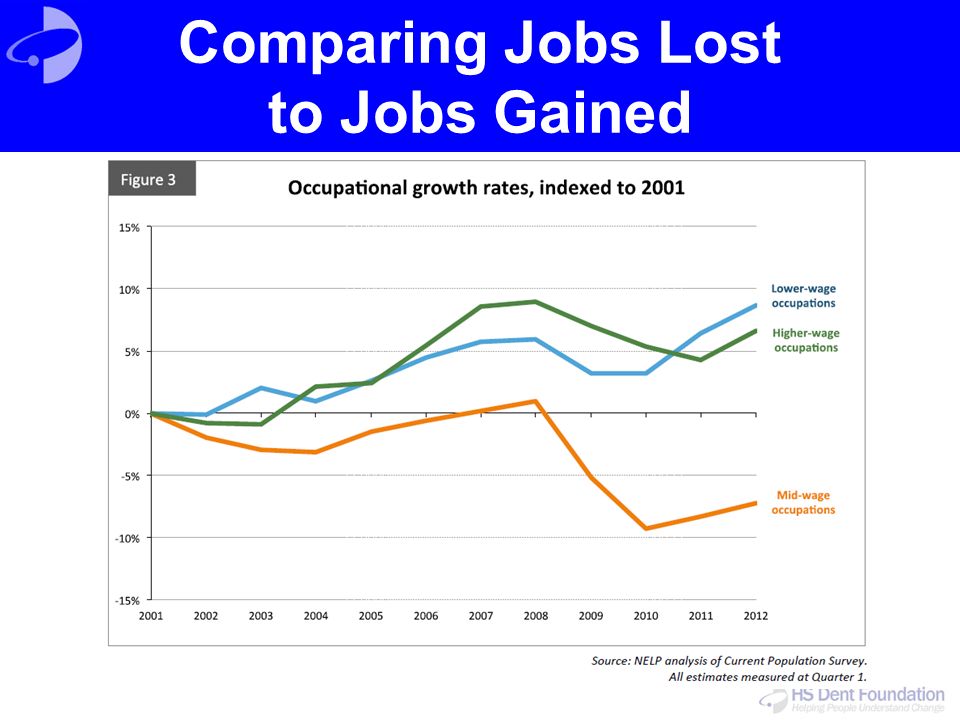

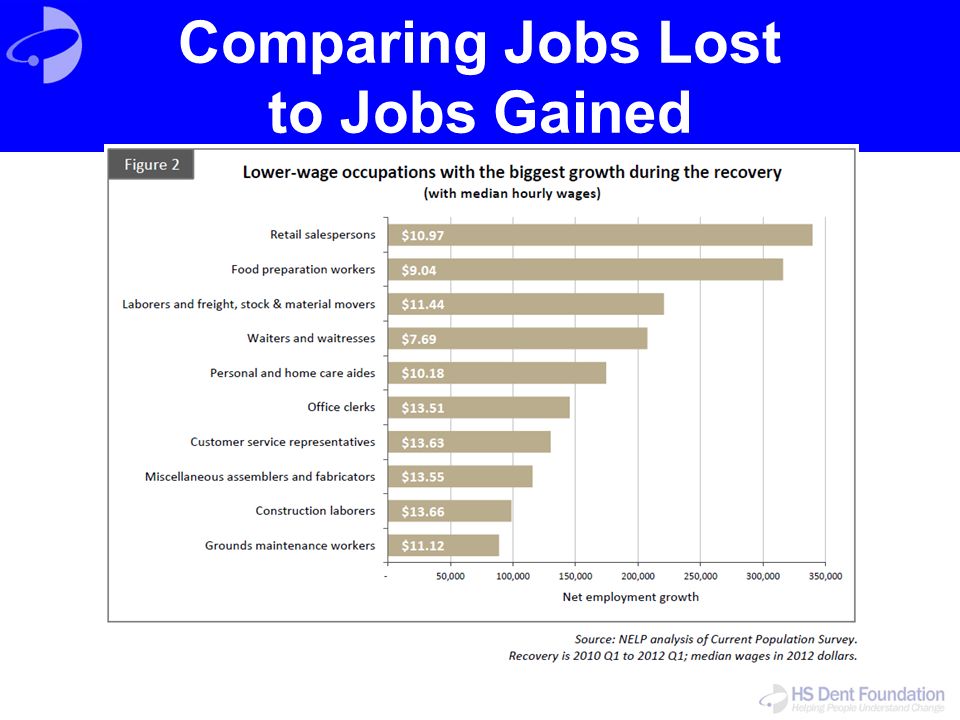

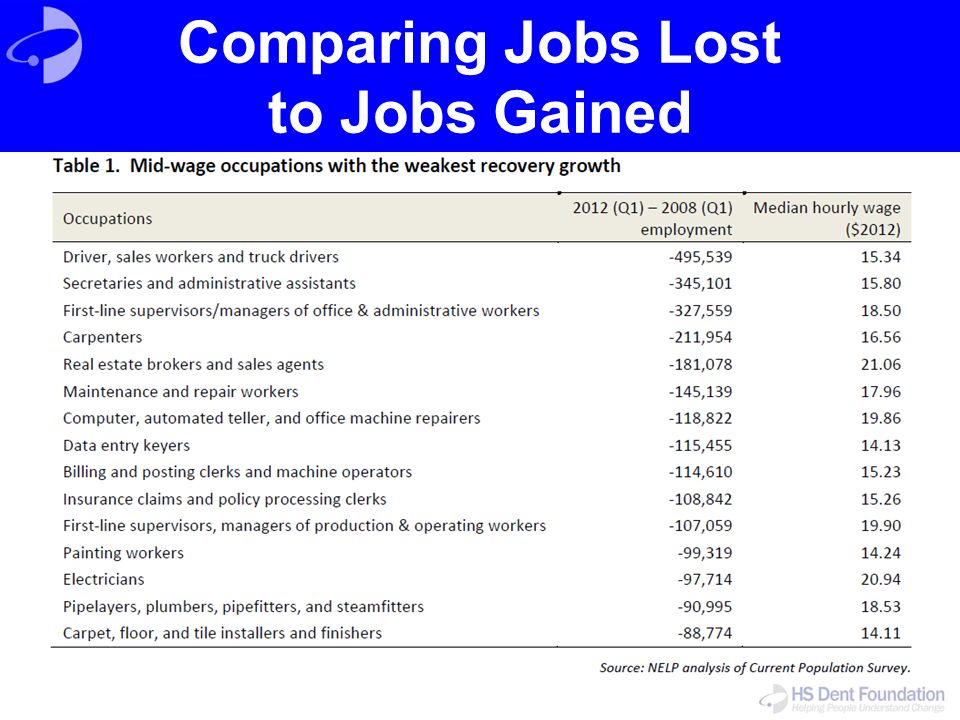

Comparing Jobs Lost to Jobs Gained Use a matrix of three levels of pay to compare jobs lost to those gained (each a third of 2008 employment) - Lower wage - $7.69/hr. to $13.83/hr ($16,049 to $28,863) Median wage - $13.84/hr to $21.13/hr ($28,884 to $44,098) Upper wage - $21.14/hr to $54.55/hr ($44,119 to $113,845)

Median wage - $13.84/hr to $21.13/hr ($28,884 to $44,098) Upper wage - $21.14/hr to $54.55/hr ($44,119 to $113,845).")

15

Comparing Jobs Lost to Jobs Gained Lower-wage occupations were 21 percent of recession losses, but 58 percent of recovery growth. Mid-wage occupations were 60 percent of recession losses, but only 22 percent of recovery growth. Higher-wage occupations were 19 percent of recession job losses, and 20 percent of recovery growth.

16

Comparing Jobs Lost to Jobs Gained

20

` `

21

Home Purchase Applications 1990-2013 Index 100= 1990 Data Source: Bloomberg, 2013

22

New Home Completions 1990-2012 Data Source: St. Louis Federal Reserve, 2013

23

New Home Sales 1963 – September 2012 Data Source: Calculated Risk, US Census Bureau, 2012 Seasonally Adjusted In Thousands

24

U.S. Spending on Construction 1990-2012 Data Source: St. Louis Federal Reserve, 2013 Billions

25

Construction as Percent of GDP 1990-2012 Data Source: St. Louis Federal Reserve, 2013

26

Total Construction Workers 1990-2013 Data Source: St. Louis Federal Reserve, 2013

27

Construction Workers, Share of All Employees, 1990-2013 Data Source: St. Louis Federal Reserve, 2013

28

The Face of the Recovery

29

Share of Job Gains and Losses Since June 2009 Data Source: Bureau of Labor Statistics, 2012 +3.8 Million +781 Thousand -479 Thousand -842 Thousand

30

Percent of Part Time Workers 1968-2012 Data Source: Bureau of Labor Statistics, 2012

31

The Blunt Instruments of Government US Government deficit spending, targeted stimulus Federal Reserve interest rates, bond purchases, printing dollars

32

The Fed Is Here to Help!

33

Federal Reserve Balance Sheet 2000-2013 Data Source: St. Louis Federal Reserve, 2013

34

Outcomes – Desired vs.. Actual Wanted – inflation expectations, increased borrowing and spending, falling unemployment, higher wages, asset inflation (re-inflation) Got – split prices – deflation in services and real estate, inflation in commodities – local vs.. global

Got – split prices – deflation in services and real estate, inflation in commodities – local vs.. global.")

35

Who Gets Helped, Who Gets Hurt? QE favors real assets, hurts dollars, so the question becomes, what is more important to your household, real dollars (dividends, interest, paycheck) or assets such as stocks, metals, commodities? Assets Income

or assets such as stocks, metals, commodities. Assets Income.")

36

Who Gets Helped, Who Gets Hurt? Wealthy households tend to hold assets, poor households tend to rely on income. While higher food/energy costs might annoy rich households, the increase in their assets more than offsets the price difference. Not so for the poor. Affluent households own more hard assets Modest households rely on earned income

37

Percent of After-Tax Income Spent on Food and Energy by Income Source: U.S. Bureau of Labor Statistics, CEX, 2009

38

Inflation since 2000 Through September 2012 Data Source: Bureau of Labor Statistics, HS Dent, 2012 CPI Core CPI Categories

39

Dollars Spent on Essential and Non-Essentials vs.. Inflation (2000- Sept. 2012) on Those Items Data Source: Bureau of Labor Statistics, HS Dent, Bloomberg; 2012 Young Families Peak Spending Retirees

on Those Items Data Source: Bureau of Labor Statistics, HS Dent, Bloomberg; 2012 Young Families Peak Spending Retirees.")

40

Growth of Consumer Credit 2006-2011 Data Source: Federal Reserve Flow of Funds Report, 2012 Index 100= 2006

41

The Term for Where We Are: Financial Repression When interest rates are held artificially low given the rate of inflation, resulting in savers being taxed/punished in order to provide borrowers greater incentives/benefits

42

Normal Yield Curve CPI 2.8% Real Rate of Return

43

Yield Curve Manipulated

44

While US Economy Not Shrinking, Growth Is Anemic at Best

45

U.S. Federal Government Spending vs. Receipts, 1980-2011 Data Source: Bureau of Economic Analysis, 2012 In Billions

46

Distribution of Federal Spending Data Source: Office of Management and Budget, 2012

47

Recent Tax Increases and Spending Cuts Payroll Tax$126 billion Unemployment 12 ACA – personal 24 Bush-era Upper 56 Sequestered Cuts 45 Total$263 billion in Tax Cuts / Spending Reductions at Federal Level

48

State Budget Gaps Source: Center on Budget and Policy Priorities, 2012

49

How States Closed Budget Gaps

50

What A Major Downturn Could Bring Tremendous reduction in private debt outstanding – another $5 trillion at least Commensurate reduction in mortgage debt, freedom of workers to move Continued reduction in home values so that next generation can afford them Wage reduction to make US more competitive with other labor markets

51

What A Major Downturn Could Bring Actually, a lot has already occurred…what an economic downturn HAS BROUGHT… –Debt reduction, lower home values, falling wages What we are missing is falling prices outside of homes, thanks to the Fed and other central banks. We have not given commodity prices the opportunity to reset with other areas of life.

52

What Lies Ahead Anemic US growth, Euro crises, deleveraging, and more Fed action The US as well as other economies is facing a very difficult future, but stocks are near all time highs. Are they worth it? Does it feel like we should be at historic highs, given stubborn unemployment, unbalanced books, falling real wages, and Fed intervention? Be careful, and be cautious. Expect tough times ahead.

53

What About the Next Generation?

54

Falling Pay for College Graduates, 2000-2011 Data Source: U.S. Census Bureau, 2013

55

Borrowers and Balances

56

Young People with Student Debt

57

Share of Borrowers Late

58

Effect of Recession on Household Composition, 1989-2012 Source: US Census Bureau, 2012

Similar presentations

(2011) Aging Baby Boomers Their Impact on the Economy and Financial Services Industry.>")

: The total market value($ value) of all the goods and services produced within.>")