Download presentation

Presentation is loading. Please wait.

1

Some Reflections on ICT and Policy Implications Alfonso Gambardella Bocconi University, Milan Geneve June 2 2006

2

Computer vs Dynamo (Paul David) Rapid technological innovation with slow gains in productivity … Why? In computer like in electricity at the beginning of the XX century Robert Solow: “We see computers everywhere but in the productivity statistics”

3

Both Computer & Dynamo … … were nodal elements of a series of future technological improvements … started during a long productivity slowdown (1890-1913 for the dynamo) … were seen as the start of amazing new trajectories

… were seen as the start of amazing new trajectories")

4

Answer Major technologies put pressures for complementary organizational and institutional changes. This takes time.

5

Dynamo By 1899 only 3% households had electric lightening, and 5% factories had electric motors It took 20 years to reach 50% diffusion In 1990 only 10% of world firms were using computers

6

Diffusion of electricity Pace was largely determined by factory electrification, which had to wait for reduced electricity price depreciation of older plants investment boom (1920s) Most importantly, benefits depended on several complementary factors … re-design and re-organization of factories

Most importantly, benefits depended on several complementary factors … re-design and re-organization of factories")

7

Question, Where are We? Probably after price reduction, depreciation & investment boom But my sense is that we have not yet resolved all the complementarity issues May be more at the level of firms (even though there is more to do) Definitely at the level of markets/uses (large new markets)

Definitely at the level of markets/uses (large new markets).")

8

Bryonjolfsson-Hitt (Computing productivity) Shows empirically that the benefits of firm investments in IT are greater 5-10 years later Consistent with the view that they require complementary investments Data on 527 large US firms, 1987- 1994

Shows empirically that the benefits of firm investments in IT are greater 5-10 years later Consistent with the view that they require complementary investments Data on 527 large US firms,")

9

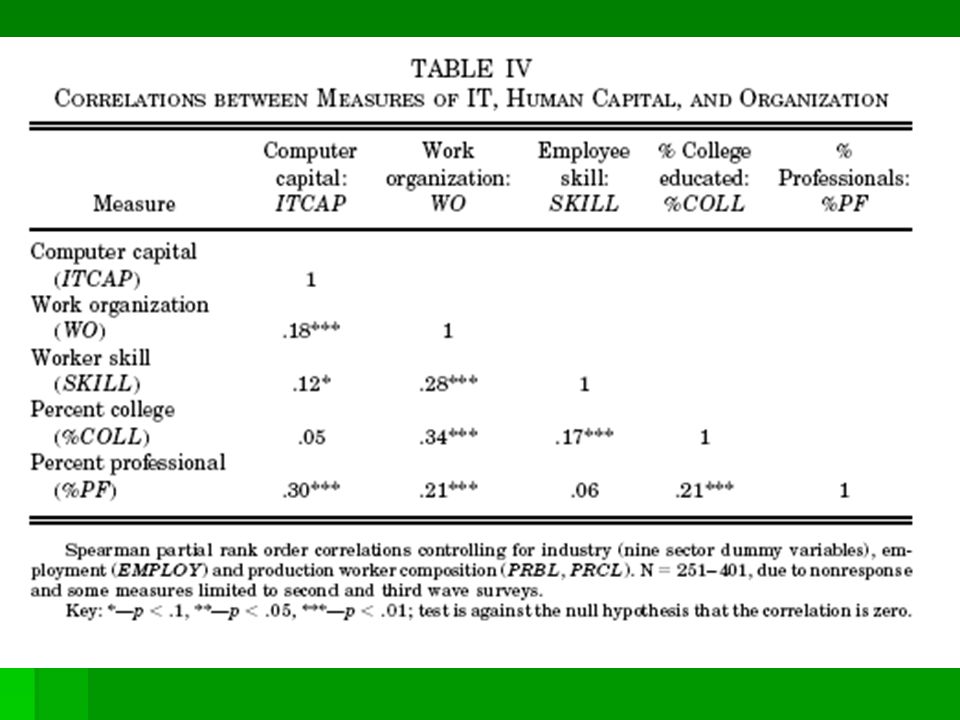

Bresnahan et al, QJE 2001 Tests “complementarity” among: IT investments Worplace organization (WO) Skilled labor Find correlation/complementarity among them Data: Survey of senior managers in 778 Fortune 1000 firms (about 55% mfr, 45% services)

Skilled labor Find correlation/complementarity among them Data: Survey of senior managers in 778 Fortune 1000 firms (about 55% mfr, 45% services)")

11

First policy issue We need to encourage the formation of complementary resources Not just for the leading firms (who do it in any case, and have probably already done it) But for the larger markets (firms, consumers, users)

But for the larger markets (firms, consumers, users)")

12

Let me now move to another related issue The previous question was: where are we with complementary assets in different industries/firms/users? Now we ask a related one: how diffused as ICT really been? Definitely not like automobile, at least in many parts of the world Is ICT going to remain largely an industrial good industry or is it going to become a wider consumer industry?

13

An example, Domotics Technology has not developed much since 1995 Prices are still very high No new services or interesting innovatons Why?

14

An even more important example Bottom of the pyramid Is 4 billion people a big enough market?

15

Can we make it through the computers? Connectivity PCMobile Phone Connectivity an add-onCore function is to connect ExpensiveCheap ComplicatedEasy to use High maintenanceLow maintenance High Power demandCharge once Physical ConnectivityWireless Fixed in space Portable Primarily dataPrimarily voice High bandwidthLow bandwidth From a presentation by Mans Olof Ors, Reuters, at Bocconi University, November 18. 2006

16

Connectivity Internet access grows 2000 2.1% 2004 6.9% Mobile usage explodes 2000 5% 2004 17.8% Mobile subscribers Developed Countries 2000 464m 2004 740m Developing Countries 2000 261m 2004 900m Picture: REUTERS From a presentation by Mans Olof Ors, Reuters, at Bocconi University, November 18. 2006

17

Mobile phones 80% of worlds population lives in areas covered by networks India adds 2 million subscribers per month Total Indian market is 350 million Picture: REUTERS An increase of 10 mobile phones per 100 people in African developing countries would increase GDP growth by 0.6 percent. (LSE 2005) Picture: REUTERS From a presentation by Mans Olof Ors, Reuters, at Bocconi University, November 18. 2006

Picture: REUTERS From a presentation by Mans Olof Ors, Reuters, at Bocconi University, November")

18

Policy? Well, the market seem to grow in any case, it’s companies who should pick this up … creating demand, a Marshall Plan? Needs coordination … in fact coordination is an important policy task here (e.g. standards, promotion) Give out cell phones to Africa?

Give out cell phones to Africa .")

19

Summary & Conclusions With IT we have moved beyond the first steps, but still lack of complementary assets (at firm and societal level, and of course much more in certain parts of the world than others) Policy: Support for creation of complementary assets

Policy: Support for creation of complementary assets")

20

Summary & Conclusions The other big issue/question: The industry is an industrial good but not yet a consumer industry New market expansions can only come through that Cell phones = consumer industry Computers = capital good industry Policy: a classical one, stimulate demand

Similar presentations

United Nations University.>")

Director, CMAI Former Advisor Technology, DOT Government.>")