Download presentation

Presentation is loading. Please wait.

1

Interest Formulas – Equal Payment Series

Engineering Economy

2

Equal Payment Series F P

Using equal payment series you can find present value or future value 1 2 N A A A P N 1 2 N

3

Compound Amount Factor

A(1+i)N-2 A A A A(1+i)N-1 N 1 2 1 2 N This is a geometric series with the first term as A and the constant r = (1+i) The formula for a geometric series = A (1- r^n)/1-r

N-2. A. A. A. A(1+i)N-1. N N. This is a geometric series with the first term as A and the constant r = (1+i) The formula for a geometric series = A (1- r^n)/1-r.")

4

Equal Payment Series Compound Amount Factor (Future Value of an annuity)

N A Example: Given: A = $5,000, N = 5 years, and i = 6% Find: F Solution: F = $5,000(F/A,6%,5) = $28,185.46

= $28,")

5

Finding an Annuity Value

N A = ? Example: Given: F = $5,000, N = 5 years, and i = 7% Find: A Solution: A = $5,000(A/F,7%,5) = $869.50

= $")

6

Example: Handling Time Shifts in a Uniform Series

First deposit occurs at n = 0 i = 6% $5,000 $5, $5, $5,000 $5,000

7

Annuity Due Excel Solution Beginning period =FV(6%,5,5000,0,1)

")

8

Example: College Savings Plan

Sinking Fund Factor The term between the brackets is called the equal-payment-series sinking-fund factor. F N A Example: College Savings Plan Given: F = $100,000, N = 8 years, and i = 7% Find: A Solution: A = $100,000(A/F,7%,8) = $9,746.78

= $9,")

9

Excel Solution Given: Find: A Using the equation:

N = 8 years Find: A Using the equation: Using built in Function: =PMT(i,N,pv,fv,type) =PMT(7%,8,0,100000,0) =$9,746.78

=PMT(7%,8,0,100000,0) =$9,")

10

Capital Recovery Factor

If we need to find A, given P,I, and N Remember that: Replacing F with its value

11

Capital Recovery Factor

This factor is called capital recovery factor P N A = ? Example: Paying Off Education Loan Given: P = $21,061.82, N = 5 years, and i = 6% Find: A Solution: A = $21,061.82(A/P,6%,5) = $5,000

= $5,000.")

12

Example: Deferred Loan Repayment Plan

i = 6% Grace period A A A A A P’ = $21,061.82(F/P, 6%, 1) i = 6% A’ A’ A’ A’ A’

i = 6% A’ A’ A’ A’ A’")

13

Two-Step Procedure Adding the first year interest to the principal then calculating the annuity payment

14

Present Worth of Annuity Series

N A Example:Powerball Lottery Given: A = $7.92M, N = 25 years, and i = 8% Find: P Solution: P = $7.92M(P/A,8%,25) = $84.54M

= $84.54M.")

15

Example: Early Savings Plan – 8% interest

44 Option 1: Early Savings Plan $2,000 ? ? Option 2: Deferred Savings Plan 44 $2,000

16

Option 1 – Early Savings Plan

44 Option 1: Early Savings Plan $2,000 ? Age 31 65

17

Option 2: Deferred Savings Plan

44 Option 2: Deferred Savings Plan $2,000 ?

18

At What Interest Rate These Two Options Would be Equivalent?

20

Using Excel’s Goal Seek Function

21

Result

23

Option 1: Early Savings Plan

$396,644 Option 1: Early Savings Plan 44 $2,000 $317,253 Option 2: Deferred Savings Plan 44 $2,000

24

Interest Formulas (Gradient Series)

")

25

Linear Gradient Series

Gradient-series present –worth factor P

26

Gradient Series as a Composite Series

We view the cash flows as composites of two series a uniform with a payment amount of A1 and a gradient with a constant amount of G

27

Example: $2,000 $1,750 $1,500 $1,250 $1,000 How much do you have to deposit now in a savings account that earns a 12% annual interest, if you want to withdraw the annual series as shown in the figure? P =?

28

Method 1: $2,000 $1,750 $1,500 $1,250 $1,000 $1,000(P/F, 12%, 1) = $892.86 $1,250(P/F, 12%, 2) = $996.49 $1,500(P/F, 12%, 3) = $1,067.67 $1,750(P/F, 12%, 4) = $1,112.16 $2,000(P/F, 12%, 5) = $1,134.85 $5,204.03 P =?

= $ $1,250(P/F, 12%, 2) = $ $1,500(P/F, 12%, 3) = $1, $1,750(P/F, 12%, 4) = $1, $2,000(P/F, 12%, 5) = $1, $5, P =")

29

Method 2:

30

Example: Supper Lottery

$3.44 million Cash Option Annual Payment Option $357,000 G = $7,000 $196,000 $189,000 $175,000

31

Equivalent Present Value of Annual Payment Option at 4.5%

The gradient series is delayed by one period To return the calculations to year zero

32

Geometric Gradient Series

Geometric Gradient is a gradient series that is been determined by a fixed rate expressed as a percentage instead of a fixed dollar amount For example the economic problems related to construction cost which involves cash flows that increase or decrease by a constant percentage

33

Present Worth Factor Geometric-gradient-series present-worth factor

34

Alternate Way of Calculating P

35

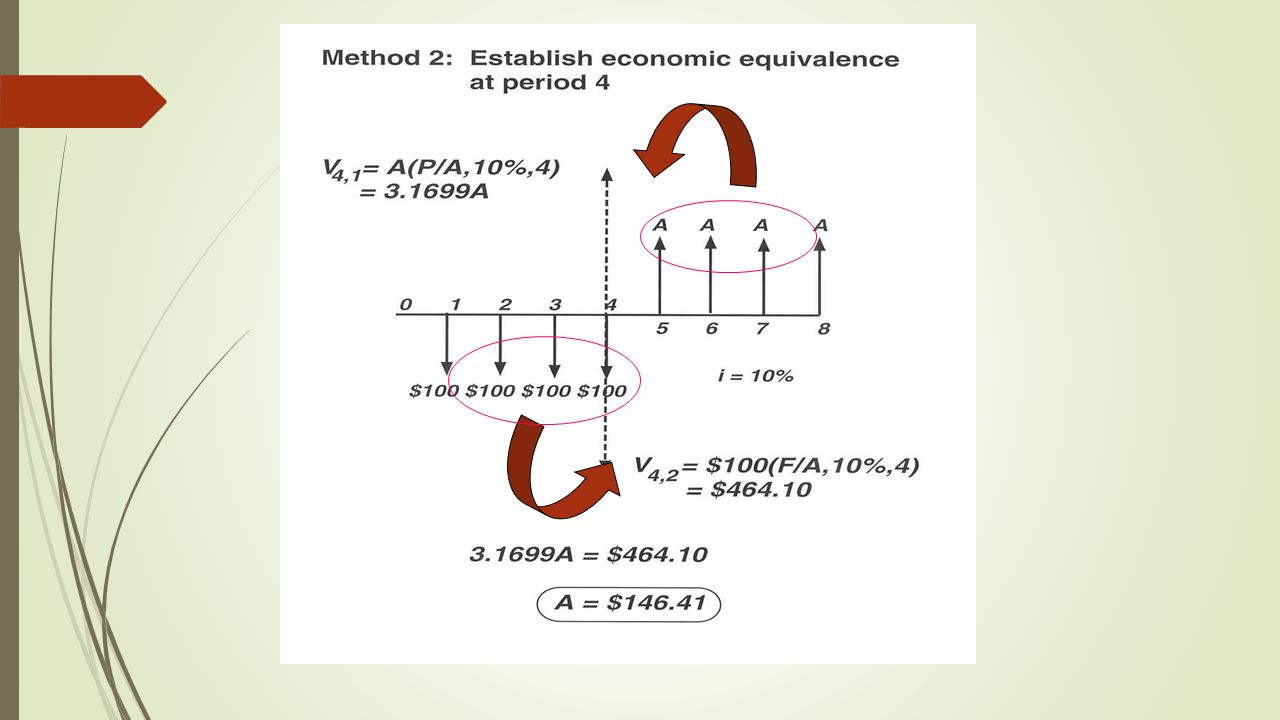

Unconventional Equivalence Calculations

EGN3613 Ch2 Part IV

36

Composite Cash Flows $200 $150 $150 $150 $150 $100 $100 $100 $50

$150 $150 $150 $150 $100 $100 $100 $50

37

Unconventional Equivalence Calculations

Situation: What value of A would make the two cash flow transactions equivalent if i = 10%?

40

Multiple Interest Rates

F = ? Find the balance at the end of year 5. 6% 4% 4% 6% 5% 2 4 5 1 3 $400 $300 $500

41

Solution

42

Cash Flows with Missing Payments

$100 i = 10% Missing payment

43

Solution P = ? i = 10% Add this cash flow to offset the change $100

$100 Pretend that we have the 10th payment i = 10%

44

Approach P = ? $100 $100 i = 10% Equivalent Cash Inflow = Equivalent Cash Outflow

45

Equivalence Relationship

46

Unconventional Regularity in Cash Flow Pattern

$10,000 i = 10% 1 C C C C C C C Payment is made every other year

47

Approach 1: Modify the Original Cash Flows

$10,000 i = 10% 1 A A A A A A A A A A A A A A

48

Relationship Between A and C

$10,000 i = 10% 1 C C C C C C C $10,000 i = 10% 1 A A A A A A A A A A A A A A

49

Solution i = 10% C A A A =$1,357.46

50

Approach 2: Modify the Interest Rate

Idea: Since cash flows occur every other year, let's find out the equivalent compound interest rate that covers the two-year period. How: If interest is compounded 10% annually, the equivalent interest rate for two-year period is 21%. (1+0.10)(1+0.10) = 1.21

(1+0.10) =")

51

Solution $10,000 i = 21% 1 C C C C C C C

Similar presentations

Suppose you wanted to become a millionaire at retirement. If an annual compound interest rate of.>")

2002 Contemporary Engineering Economics 1 Chapter 4 Time Is Money Interest: The Cost of Money Economic Equivalence Development of Interest Formulas.>")

>")

2002 Contemporary Engineering Economics>")

2002 Contemporary Engineering Economics>")