Download presentation

Presentation is loading. Please wait.

1

Financial Leave Accounting George Gomez 03/26/2014

2

FINANCIAL LEAVE ACCOUNTING Overview Background VACLAC Vacation Accrual Vacation Usage Operating Ledger Transferring Funds (PETs) Additional Considerations

Additional Considerations")

3

FINANCIAL LEAVE ACCOUNTING Background Implemented over 30 years ago Relieves the need to monitor vacation reserves within various funding sources Eliminates cumbersome financial transfers to, from or between funds Eliminates financial hardship to departments when employees terminate with large vacation balances

4

FINANCIAL LEAVE ACCOUNTING How does it work? Leave code rate from 1 st lowest Appt. in PPS Utilizes Vacation Pool Concept Departments assessed for vacation monthly Vacation is reimbursed when taken Restricted Funds, Title Codes are not assessed

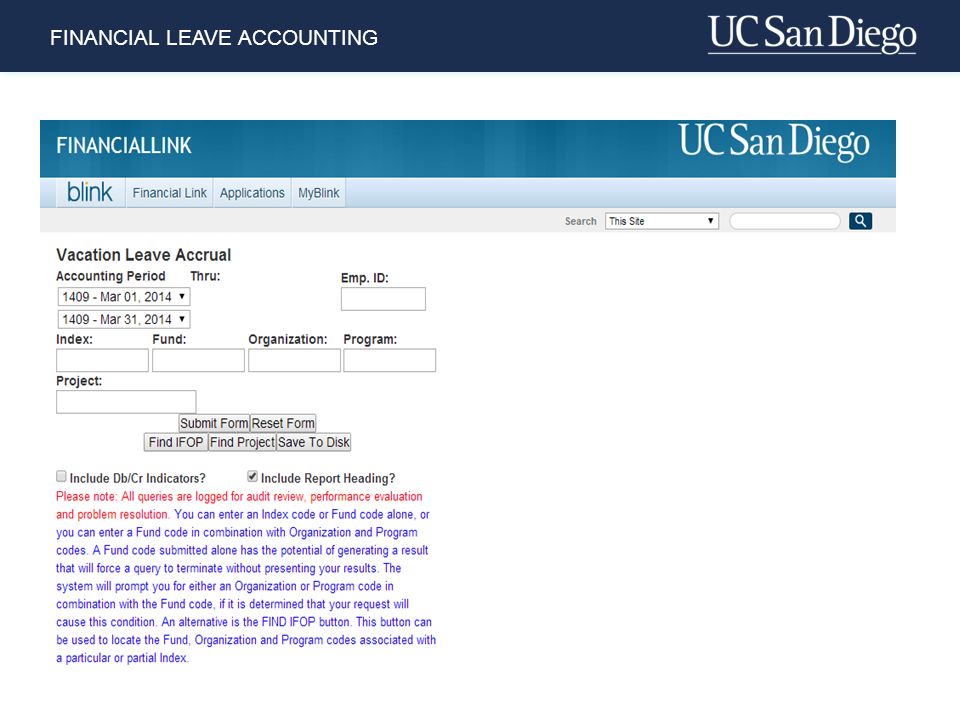

5

FINANCIAL LEAVE ACCOUNTING VACLAC Found in FinancialLink – Reports - Payroll Reports Shows Accruals and Usage Identifies amounts to Ledger

6

FINANCIAL LEAVE ACCOUNTING

8

VACLAC

9

FINANCIAL LEAVE ACCOUNTING Calculating Vacation Accrual Monthly Employees: Divide monthly salary rate by 174 (average monthly hours) and multiply result by hours earned for Accrued Pay Biweekly Employees: Use hourly rate and multiply by hours earned for Accrued Pay Multiply Accrued Pay by Benefits Code rate for Accrued Benefits

and multiply result by hours earned for Accrued Pay Biweekly Employees: Use hourly rate and multiply by hours earned for Accrued Pay Multiply Accrued Pay by Benefits Code rate for Accrued Benefits")

10

FINANCIAL LEAVE ACCOUNTING Accrued Pay = Rate X Hours (Monthly Rate / 174) 6,438.85 / 174 = 37.00 37.00 X 12.92 = 478.04 Benefits = Accrued Pay X Benefits Code BC 04 = 22.89% 478.04 X.2289 = 109.42 Net to Sub 6 Financial Cost = Totals (Pay + Benefits + Used Benefits) Sub Account 1 ~ Net to Sub 6 5,009.16 + 1,091.81 + (-356.19) = 5,744.78 Accrual Only

6, / 174 = X = Benefits = Accrued Pay X Benefits Code BC 04 = 22.89% X.2289 = Net to Sub 6 Financial Cost = Totals (Pay + Benefits + Used Benefits) Sub Account 1 ~ Net to Sub 6 5, , ( ) = 5, Accrual Only")

11

Vacation Liability Account FINANCIAL LEAVE ACCOUNTING LEDGER ACTIVITY SALARY ACCOUNT SUB ACCOUNT 0,1 or 2 Budget Financial Transactions BENEFIT ACCOUNT SUB ACCOUNT 6 (668930) Budget Financial Transactions Salary Amount Reallocated to Sub Account 6 DOC – PAS91XXX LEAVE ACCRUAL 6,100.97 1,091.81 5,009.16 + 6,100.97 (5,009.16 + 1,091.81) Entire Amount (Cost of Salary Accrual and Benefits) Assessed Against Sub Account 6 and Credited to the Vacation Liability Account (Pool). DOC – PAS90XXX – LEAVE ACTIVITY VACATION ACCRUAL

12

FINANCIAL LEAVE ACCOUNTING Calculating Vacation Usage Use actual hours when vacation was taken Monthly Employees: Divide hours used by actual hours in the pay cycle, multiply result by monthly salary rate for Used Pay Biweekly Employees: Multiply hours used by hourly rate for Used Pay Multiply Used Pay by Benefits Code rate for Used Benefits

13

FINANCIAL LEAVE ACCOUNTING Usage Only Usage Pay = Rate X Hours (Hours/Monthly Working Hrs) 16/176 = 0.0909 11,641.39 X 0.0909 = 1,058.20 _________________________ Benefits = Pay X Benefits Code BC 12 = 16.96% 1,058.20 X.1696 = 179.47 _________________________ Net to Salary Sub = Pay Total Sub 1 = 1,895.74

16/176 = , X = 1, _________________________ Benefits = Pay X Benefits Code BC 12 = 16.96% 1, X.1696 = _________________________ Net to Salary Sub = Pay Total Sub 1 = 1,895.74")

14

FINANCIAL LEAVE ACCOUNTING Vacation Liability Account Pay Usage is Credited Back to Department (Benefit Portion Credited to Benefits Sub 6) The Credit or Debit to Sub 6 Depends on the Net Value of Usage Credit and Accrual Debit. DOC – PAS90XXX – LEAVE ACTIVITY LEDGER ACTIVITY SALARY ACCOUNT SUB ACCOUNT 0,1 or 2 (601850, 611850, 621850) Budget Financial Transactions BENEFIT ACCOUNT SUB ACCOUNT 6 (668930) Budget Financial Transactions VACATION USAGE Usage Pay Amount is Credited Back to the Department Salary Sub Account (0,1, or 2) DOC – PAS90XXX LEAVE USAGE - 1,895.74 - 356.19 -1,895.74 -359.19

Budget Financial Transactions BENEFIT ACCOUNT SUB ACCOUNT 6 (668930) Budget Financial Transactions VACATION USAGE Usage Pay Amount is Credited Back to the Department Salary Sub Account (0,1, or 2) DOC – PAS90XXX LEAVE USAGE - 1, ,")

15

LEDGER ACTIVITY SALARY ACCOUNT SUB ACCOUNT 0,1 or 2 Budget Financial Transactions BENEFIT ACCOUNT SUB ACCOUNT 6 (668930) Budget Financial Transactions LEDGER ACTIVITY SALARY ACCOUNT SUB ACCOUNT 0,1 or 2 Budget Financial Transactions BENEFIT ACCOUNT SUB ACCOUNT 6 (668930) Budget Financial Transactions FINANCIAL LEAVE ACCOUNTING 5,009.16 1,091.81 Vacation Liability Account Usage Pay Amount is Credited Back to the Department Salary Sub Account (0,1, or 2) DOC – PAS90XXX LEAVE USAGE Salary Amount Reallocated to Sub Account 6 DOC – PAS91XXX LEAVE ACCRUAL If Accrual Cost is Greater Than Usage Reimbursement, Then Net to Sub 6 is a Debit. If Usage Reimbursement is Greater Than Accrual Cost, Then Net to Sub 6 is a Credit. DOC – PAS90XXX – LEAVE ACTIVITY VACATION ACCRUAL VACATION USAGE 6,100.97 + 6,100.97-1,895.74 -356.19 -1,895.74 -356.19

16

FINANCIAL LEAVE ACCOUNTING Ledger Activity Budget and Financial Transactions Totals for Applicable Sub Sub 0- Academic Sub 1- Staff Sub 2- General Assistance

17

FINANCIAL LEAVE ACCOUNTING From the VACLAC to the Operating Ledger Acct. 668930 Acct. 601850 Acct. 611850 Acct. 621850

18

FINANCIAL LEAVE ACCOUNTING Sub 1 Usage Pay Sub 1 Usage Benefits Sub 0 Accrual Pay Sub 2 Accrual Pay Sub 1 Accrual Pay Sub 0 Accrual Pay Sub 1 Accrual Pay Sub 2 Accrual Pay Sub 1 Usage Pay

19

FINANCIAL LEAVE ACCOUNTING Fund Sources Contract & Grants Budgetary Reallocation General Funds Funding pre-determined based on FTE Usage Reimbursement drawn-off Accrual charges are automatically funded Termination payments cannot be projected, so reimbursements are journalized by Payroll quarterly

20

FINANCIAL LEAVE ACCOUNTING Transferring Funds with PETs Vacation usage can only be moved in timekeeping within a 12 month period.

21

FINANCIAL LEAVE ACCOUNTING Additional Considerations Employee Leave Code in PPS Employee must be below maximum accrual Timekeeping adjustment cannot exceed 12 months Retroactive adjustment Terminal Vacation uses Benefit Code 31

22

FINANCIAL LEAVE ACCOUNTING Vacation Accrual and Usage Accounting Policy http://adminrecords.ucsd.edu/PPM/docs/395-9.pdf

23

FINANCIAL LEAVE ACCOUNTING Questions?

24

FINANCIAL LEAVE ACCOUNTING Thank You George Gomez Payroll 858-534-3245 ggomez@ucsd.edu

Similar presentations

Medical Group.>")

>")