Download presentation

Presentation is loading. Please wait.

2

1 Audit Reports AU-C Sections 700, 705, 706 & 708

3

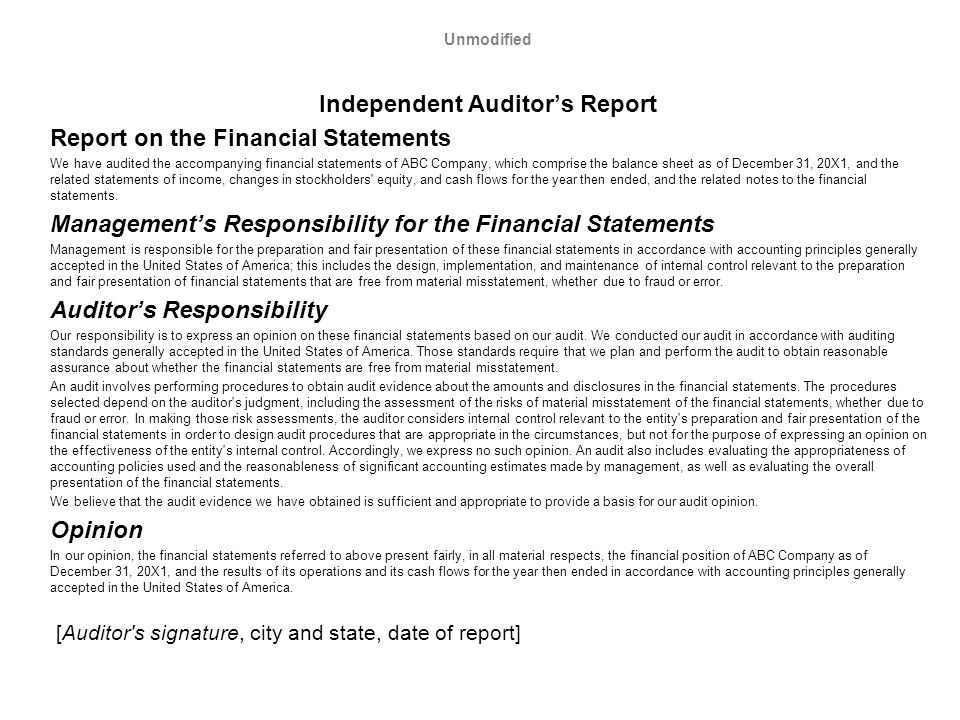

Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.2 Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

4

3 Phases of an Audit p. 67 Phase IPlan & design an audit approach Understand the Entity, Environment, Internal Controls Phase IITests of Controls Substantive Tests of Transactions Phase IIIAnalytical Procedures – substantive Tests of Details of Balances Phase IVComplete the audit Issue Audit Report

5

4 What is the objective of AU-C 700? Steph

6

AU-C 700 Forming an Opinion and Reporting on Financial Statements.10 The objectives of the auditor are to a. form an opinion on the financial statements based on an evaluation of the audit evidence obtained, including evidence obtained about comparative financial statements or comparative financial information, and b. express clearly that opinion on the financial statements through a written report that also describes the basis for that opinion.

7

6 What are the four sections of the independent auditors’ standard unmodified report ? Sam

8

7 sections in the standard report Report on the financial statements Management’s responsibility Auditor’s responsibility Opnion

9

8 Old edition page 45

10

9 Old editions page 48

11

Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.2 Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

12

11 State the first sentence of each of the four sections of the auditor’s report. Aleksandr

13

Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.2 Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

14

13 What audit report do we issue if everything is OK ? the financial statements are fairly presented there are no material misstatements Timothy

15

Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.2 Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

16

15 Everything OK Qualified Opinion or Disclaim an Opinion Std Reports are Unmodified Opinions We may add an Emphasis or Other Material paragraph GAAS problem We did not comply with auditing standards (GAAS) Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP

Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP")

17

16 Ricardo the company refuses to adopt ASC 605-25-25 Accounting Standards Codification 605-25-25 Revenue Recognition for Multiple-Element Arrangements They argue that the amounts are immaterial very immaterial what opinion will you issue

18

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

19

18 What reporting issue does AU-C 708 address? Ian

20

AU-C 708 Consistency of Financial Statements.03 The objectives of the auditor are to a.Evaluate the consistency of the financial statements for the periods presented and b.Communicate appropriately in the auditor’s report when the comparability of financial statements between periods has been materially affected by a change in accounting principle or by adjustments to correct a material misstatement in previously issued financial statements.

21

20 Where in the independent auditor’s report do we address issues regarding consistency (AU-C708) ? Communicate appropriately in the auditor’s report when the comparability of financial statements between periods has been materially affected by a change in accounting principle or by adjustments to correct a material misstatement in previously issued financial statements Romy

22

Emphasis-of-Matter Paragraph Because There Is Inconsistent Application of Accounting Principles Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence that we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in Note X to the financial statements, the entity has elected to change its method of accounting for [describe accounting method change] in [insert year(s) of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor's signature]

of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor s signature].")

23

22 Chen the financial statements are fairly presented BUT the company will probably go bankrupt the statements clearly indicate the company is in very serious financial trouble but…..

24

Emphasis-of-Matter Paragraph Because of going concern Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence that we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter If ABC Company continues to suffer recurring losses from operations and continues to have a net capital deficiency, there may be substantial doubt about its ability to continue as a going concern. [Auditor's signature]

25

24 Fiona the client faces a huge environmental liability (very material) they will probably incur a loss they cannot estimate the amount of the loss Although they have appropriately disclosed this contingent liability in a footnote, you wish to emphasize the matter

they will probably incur a loss they cannot estimate the amount of the loss Although they have appropriately disclosed this contingent liability in a footnote, you wish to emphasize the matter")

26

Emphasis-of-Matter Paragraph Because There Is Uncertainty Relating to a Pending Unusually Important Litigation Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence that we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in Note X to the financial statements, the entity has elected to change its method of accounting for [describe accounting method change] in [insert year(s) of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor's signature]

of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor s signature].")

27

26 Marc the company reports financial instruments using ASU 2013-11 for 2014, the current year ( Accounting Standards Update 2013-11 relates to Unrecognized Tax Benefits when a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryfoward Exists) different accounting principles are used in 2014 relative to 2013 because companies were not required to implement ASU 2013-11 until 2014

different accounting principles are used in 2014 relative to 2013 because companies were not required to implement ASU until 2014")

28

Emphasis-of-Matter Paragraph Because There Is Inconsistent Application of Accounting Principles Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence that we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in Note X to the financial statements, the entity has elected to change its method of accounting for [describe accounting method change] in [insert year(s) of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor's signature]

of financial statements that reflect the accounting method change]. Our opinion is not modified with respect to this matter. [Auditor s signature].")

30

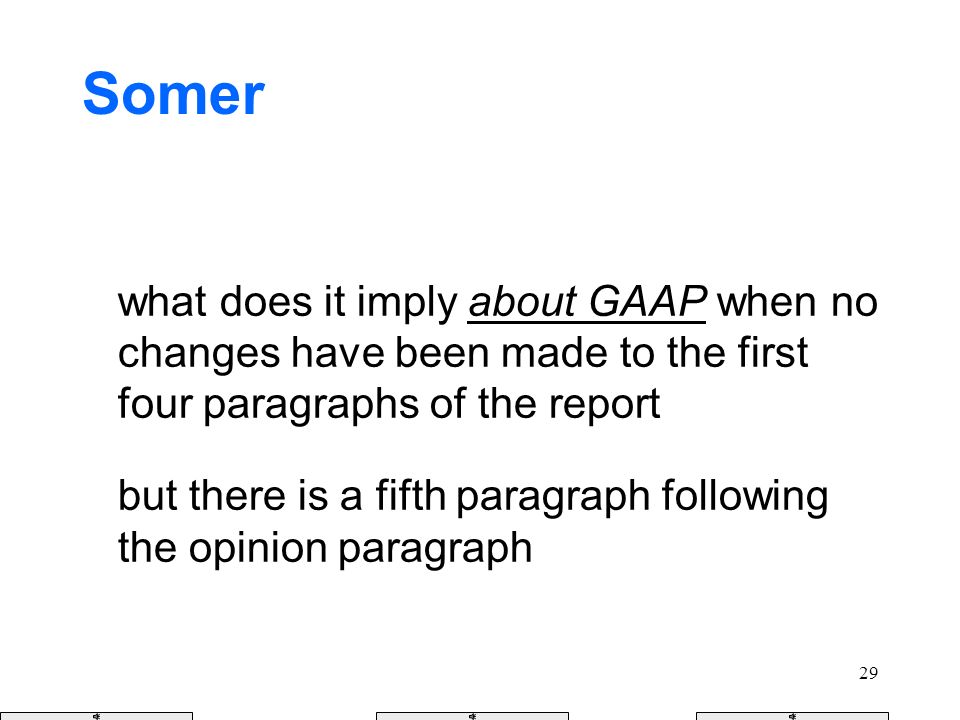

29 Somer what does it imply about GAAP when no changes have been made to the first four paragraphs of the report but there is a fifth paragraph following the opinion paragraph

31

30 unmodifiedAuditingAccounting stdQualDiscQualAdv We audited std modifystd Mgmt’s Resp std Auditor Resp Stdstdstd* modifystd* Basis for Opinion no yes Fairly Present conform w/ GAAP std except forbecause ofexcept forbecause of Emphasis para Other Matters Consistency Emphasis Go Concern Do Not Present Fairly We Not Express an opinion

32

31 Rule 203 departure Justified Departures from GAAP Rule 203: Rules of Conduct in the Code of Professional Conduct

33

32 Everything OK Qualified Opinion or Disclaim an Opinion Std Reports are Unmodified Opinions We may add an Emphasis or Other Material paragraph GAAS problem We did not comply with auditing standards (GAAS) Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP

Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP")

34

33 Departure from GAAP misstatement

35

34 Jonathan S What opinions do we choose from if the opinion paragraph isn’t true \\ there is a GAAP problem

36

35 Qualified Adverse

37

36 Jena the company refuses to adopt ASC 605-25-25 Accounting Standards Codification 605-25-25 Revenue Recognition for Multiple-Element Arrangements They argue that the amounts are immaterial very immaterial what opinion will you issue

38

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

39

38 Ashley the client forgot to depreciate their building they refuse to correct the error although material, you can accurately estimate the effects of this misstatement

40

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

41

Qualified Opinion Due to a Material Misstatement Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheets as of December 31, 20X1 and 20X0, and the related statements of income, changes in stockholders' equity, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion. Basis for Qualified Opinion The Company has stated inventories at cost in the accompanying balance sheets. Accounting principles generally accepted in the United States of America require inventories to be stated at the lower of cost or market. If the Company stated inventories at the lower of cost or market, a write down of $XXX and $XXX would have been required as of December 31, 20X1 and 20X0, respectively. Accordingly, cost of sales would have been increased by $XXX and $XXX, and net income, income taxes, and stockholders' equity would have been reduced by $XXX, $XXX, and $XXX, and $XXX, $XXX, and $XXX, as of and for the years ended December 31, 20X1 and 20X0, respectively. Qualified Opinion In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1 and 20X0, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

42

41 Iris after you tell the client what opinion you are going to issue and they read your explanatory paragraph they will most likely agree to correct the financial statements what opinion will you issue if they correct their financial statements

43

42 Lauren the client does not have the expertise to implement 715-30-25 Defined Benefit Plan Recognition you can’t estimate the amounts it is too complicated but you are sure it is very material

44

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

45

Adverse Opinion Due to a Material Misstatement Independent Auditor’s Report Report on the Consolidated Financial Statements We have audited the accompanying consolidated financial statements of ABC Company and its subsidiaries, which comprise the consolidated balance sheet as of December 31, 20X1, and the related consolidated statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our adverse audit opinion. Basis for Adverse Opinion As described in Note X, the Company has not consolidated the financial statements of subsidiary XYZ Company that it acquired during 20X1 because it has not yet been able to ascertain the fair values of certain of the subsidiary's material assets and liabilities at the acquisition date. This investment is therefore accounted for on a cost basis by the Company. Under accounting principles generally accepted in the United States of America, the subsidiary should have been consolidated because it is controlled by the Company. Had XYZ Company been consolidated, many elements in the accompanying consolidated financial statements would have been materially affected. The effects on the consolidated financial statements of the failure to consolidate have not been determined. Adverse Opinion In our opinion, because of the significance of the matter discussed in the Basis for Adverse Opinion paragraph, the consolidated financial statements referred to above do not present fairly the financial position of ABC Company and its subsidiaries as of December 31, 20X1, or the results of their operations or their cash flows for the year then ended.

46

45 What are the elements of the financial statements? Janet

47

46 Where in the independent auditor’s report do we address inadequate disclosure? When the auditor determines that informative disclosures are not reasonably adequate, the auditor must so state in the auditor’s report Ciara

48

47 Gordon The audit client supplies contractors. It deals primarily with home builders in South Florida. ASC 825-10-50 requires footnote disclosures when credit risk is concentrated in a certain geographic area or among a certain class of customer. The company fails to disclose these credit risks.

49

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

50

Qualified Opinion for Inadequate Disclosure Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheets as of December 31, 20X1 and 20X0, and the related statements of income, changes in stockholders' equity, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion. Basis for Qualified Opinion The Company's financial statements do not disclose [describe the nature of the omitted information that is not practicable to present in the auditor's report]. In our opinion, disclosure of this information is required by accounting principles generally accepted in the United States of America. Qualified Opinion In our opinion, except for the omission of the information described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1 and 20X0, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

51

50 Everything OK Qualified Opinion or Disclaim an Opinion Std Reports are Unmodified Opinions We may add an Emphasis or Other Material paragraph GAAS problem We did not comply with auditing standards (GAAS) Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP

Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP")

52

51 Briefly What does AU-C 315 discuss? What does AU-C 500 discuss? Jonathan P

53

Objectives AU-C 315 Understanding the Entity and Its Environment and Assessing the Risk of Material Misstatement AU-C 330 Performing Audit Procedures in Response to Assessed Risks and Evaluating the audit Evidence Obtained AU-C 500 Audit Evidence

54

53 Failure to comply with GAAS scope limitation

55

54 Katherine Which audit reports do we choose from if there is a scope limitation insufficient evidence there is a GAAS problem

56

55 Qualified Disclaimer

57

56 you are unable to perform all the auditing procedures that you would like …. because you accepted the engagement late you can not observe beginning inventory the client had an outside service organization perform a physical inventory on 1/1/14 the bank that requested the audit is aware of the situation and is comfortable with the situation

58

57 Dillon What opinion do we issue there is a scope limitation

59

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

60

Qualified Opinion Due to the Auditor’s Inability to Obtain Sufficient Appropriate Audit Evidence Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion. Basis for Qualified Opinion ABC Company's investment in XYZ Company, a foreign affiliate acquired during the year and accounted for under the equity method, is carried at $XXX on the balance sheet at December 31, 20X1, and ABC Company's share of XYZ Company's net income of $XXX is included inABCCompany's net income for the year then ended.We were unable to obtain sufficient appropriate audit evidence about the carrying amount of ABC Company's investment in XYZ Company as of December 31, 20X1 and ABC Company's share of XYZ Company's net income for the year then ended because we were denied access to the financial information, management, and the auditors of XYZ Company. Consequently, we were unable to determine whether any adjustments to these amounts were necessary. Qualified Opinion In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature]

61

Qualified Opinion In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Qualified Opinion In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1 and 20X0, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America. Difference between Qualified Opinions

62

61 Julissa you are unable to perform all the auditing procedures that you would like …. because you accepted the engagement late you can not observe beginning inventory …. inventory is very material the client hasn’t taken a physical inventory in years

63

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements.

64

Disclaimer of Opinion Due to the Auditor’s Inability to Obtain Sufficient Appropriate Audit Evidence Independent Auditor’s Report Report on the Financial Statements We were engaged to audit the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on conducting the audit in accordance with auditing standards generally accepted in the United States of America. Because of the matter described in the Basis for Disclaimer of Opinion paragraph, however, we were not able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion. Basis for Disclaimer of Opinion The Company's investment in XYZ Company, a joint venture, is carried at $XXX on the Company's balance sheet, which represents over 90 percent of the Company's net assets as of December 31, 20X1. We were not allowed access to the management and the auditors of XYZ Company. As a result, we were unable to determine whether any adjustments were necessary relating to the Company's proportional share of XYZ Company's assets that it controls jointly, its proportional share of XYZ Company's liabilities for which it is jointly responsible, its proportional share of XYZ Company's income and expenses for the year, and the elements making up the statements of changes in stockholders' equity and cash flows. Disclaimer of Opinion Because of the significance of the matter described in the Basis for Disclaimer of Opinion paragraph, we have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion. Accordingly, we do not express an opinion on these financial statements.

65

64 Independence Ultimate scope limitation

66

65 Not Independent - Disclaimer We are not independent with respect to Miller Motor Co. and the accompanying balance sheet of as of Dec. 31, 2014 and the related statements of income, retained earnings and cash flows were not audited by us. Accordingly, we do not express an opinion or any other form of assurance on these financial statements.

67

66 unmodifiedAuditingAccounting stdQualDiscQualAdv We audited std modifystd Mgmt’s Resp std Auditor Resp Stdstdstd* modifystd* Basis for Opinion n/a yes Fairly Present conform w/ GAAP std except forbecause ofexcept forbecause of Emphasis para Other Matters Consistency Emphasis Go Concern Do Not Present Fairly We Do Not Express an opinion

68

67

69

68

70

69 What is the objective of AU-C 700? Christina

71

AU-C 700 Forming an Opinion and Reporting on Financial Statements.10 The objectives of the auditor are to a. form an opinion on the financial statements based on an evaluation of the audit evidence obtained, including evidence obtained about comparative financial statements or comparative financial information, and b. express clearly that opinion on the financial statements through a written report that also describes the basis for that opinion.

72

71 Where in the independent auditor’s report do we “express an opinion” Julia

73

72 Where does the independent auditor’s report describe the nature of the auditor’s work? Alyssa

74

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

75

74 Everything OK Qualified Opinion or Disclaim an Opinion Std Reports are Unmodified Opinions We may add an Emphasis or Other Material paragraph GAAS problem We did not comply with auditing standards (GAAS) Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP

Unmodified Opinion Qualified Opinion or Adverse Opinion GAAP problem NOT fairly presented f/s do not conform to GAAP")

76

75 unmodifiedAuditingAccounting stdQualDiscQualAdv We audited std modifystd Mgmt’s Resp std Auditor Resp Stdstdstd* modifystd* Basis for Opinion n/a yes Fairly Present conform w/ GAAP std except forbecause ofexcept forbecause of Emphasis para Other Matters Consistency Emphasis Go Concern Do Not Present Fairly We Do Not Express an opinion

81

Unmodified Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature, city and state, date of report]

82

Qualified Opinion Due to a Material Misstatement Independent Auditor’s Report Report on the Financial Statements We have audited the accompanying financial statements of ABC Company, which comprise the balance sheets as of December 31, 20X1 and 20X0, and the related statements of income, changes in stockholders' equity, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion. Basis for Qualified Opinion The Company has stated inventories at cost in the accompanying balance sheets. Accounting principles generally accepted in the United States of America require inventories to be stated at the lower of cost or market. If the Company stated inventories at the lower of cost or market, a write down of $XXX and $XXX would have been required as of December 31, 20X1 and 20X0, respectively. Accordingly, cost of sales would have been increased by $XXX and $XXX, and net income, income taxes, and stockholders' equity would have been reduced by $XXX, $XXX, and $XXX, and $XXX, $XXX, and $XXX, as of and for the years ended December 31, 20X1 and 20X0, respectively. Qualified Opinion In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X1 and 20X0, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America. [Auditor's signature]

83