Download presentation

Presentation is loading. Please wait.

1

Global Trends in Telecom Restructuring Dr Tim Kelly, ITU Monday Session 1 CTO Senior management seminar: Telecoms restructuring and business change Malta, 17-21 May, 1999 The views expressed in this paper are those of the author and do not necessarily reflect the opinions of the ITU or its membership. Dr Kelly can be contacted at Tim.Kelly@itu.int.

2

Agenda The state of the Telecoms sector worldwide The Public Switched Telephone Network Mobile Communications The Internet Market liberalisation / privatisation * Separation of regulatory and operational functions The telecoms development gap: The changing international telecoms environment The erosion of the accounting rate system Key policy issues * This will be the subject of separate presentations.

3

Telephone main lines worldwide (M) Source: ITU World Telecommunication Indicators Database. 96 129 175 245 327 407 520 744 792 970 694 6065707580859095969700 0% 1% 2% 3% 4% 5% 6% 7% Annual average growth (right scale) F o r e c a s t

F o r e c a s t.")

4

Annual growth in telephone network Emerging economies, 1990-95 8% 9% 10% 27% AfricaArab States Latin America Asia- Pacific Source: ITU Asia-Pacific Telecommunication Indicators, 1997: New Telecom Operators.

5

Top 20 PTOs by revenue, 1997 Source: ITU PTO Database.

6

Cellular subscribers worldwide (M) Source: ITU World Telecommunication Indicators Database. Annual average growth (right scale) 11 16 23 34 55 91 144 214 285 420 1990199119921993199419951996199719982000 0% 10% 20% 30% 40% 50% 60% 70% F o r e c a s t

% 10% 20% 30% 40% 50% 60% 70% F o r e c a s t.")

7

Cellphones, like fixed-lines, are closely related to wealth Saudi Arabia Gabon Russia Israel Finland Switzerland Belgium Bolivia Azerbaijan Lebanon Estonia Cambodia Tunisia Cameroon R 2 = 0.8422 0.01 0.10 1.00 10.00 100.00 $100$1'000$10'000$100'000 GDP per capita, US$, 1996 Cellular subscribers per 100 inhabitants, 1997 Countries above the line have a higher than expected mobile cellular penetration considering their level of income. Countries below the line have a higher than expected mobile cellular penetration considering their level of income. Source: ITU World Telecommunication Indicators Database.

8

Top 20 mobile companies, 1997 Source: ITU PTO Database.

9

Internet hosts (million) and growth rates, 1990-1998 Source: ITU Challenges to the Network: Internet for development, 1999. Network Wizards. 0.4 0.7 1.3 2.3 4.7 9.4 29.7 43.5 16.1 0 10 20 30 40 50 909192939495969798 87% 52% 6% Telephone lines Cellular subscribers Internet hosts

10

Canada & US 64.1% Europe, 24.3% LAC* 1.2% Africa 0.5% Developing Asia-Pacific 2.9% Other 4.6% Australia, Japan & New Zealand 7.0% Distribution of Internet hosts, January 1998 Source: ITU Challenges to the Network: Internet for development, 1999.

11

Top 20 Internet Service Providers, 1998 Rank Internet / Online Service provider (Country) Owner WebsiteSubscribers (latest, 000s) 1 AOL (USA) *AOL www.aol.com 17100 Jun-98 2 Nifty-Serve (Japan) Fujitsu, others www.nifty.ne.jp 2'630 Aug-98 3 Biglobe (Japan)NEC, others www.biglobe.ne.jp 2'560 Mar-98 4 T-Online (Germany)Deutsche Telekom www.t-online.de 2'300 Jun-98 5 MSN (USA)Microsoft home.microsoft.com 2'000 Jun-98 6 Chollian (Korea (Rep.))Dacom http://www.chollian.net/ 1'170 Dec-97 7 WorldNet (USA)AT&T www.att.net 1'095 Jun-98 8 EarthLink Sprint (USA)Sprint, others www.earthlink.com 710 Jun-98 9 Prodigy (USA)Prodigy www.prodigy.com 638 Jun-98 10 Infovia (Spain)Telefonica www.tsai.es 535 Dec-97 11 Netcom (USA)ICG www.netcom.com 512 Jun-98 12 HiNet (Taiwan-China)Chungwa Telecom www.hinet.net 507 Jun-98 13 MindSpring (USA)MindSpring www.mindspring.net 393 Jun-98 14 SBC Internet ServicesSBC www.public.swbell.net www.public.pacbell.net 330 Jun-98 15 Tele2 (Sweden)Tele2 www.tele2.se 317 Jun-98 16 GTE Internetworking (USA)GTE www.gte.net 311 Jun-98 17 CWIX (USA)Cable&Wireless www.cwix.com 310 Jun-98 18 Wanadoo (France)France Telecom www.wanadoo.fr 266 Jun-98 19 Netvigator (Hongkong SAR)Hongkong Telecom www.netvigator.com 235 Mar-98 20 Telia Internet (Sweden)Telia www.telia.se 232 Dec-97 TOTAL, top 20 34151 Source: ITU Challenges to the Network: Internet for development, 1999.

Owner WebsiteSubscribers (latest, 000s) 1 AOL (USA) *AOL Jun-98 2 Nifty-Serve (Japan) Fujitsu, others Aug-98 3 Biglobe (Japan)NEC, others Mar-98 4 T-Online (Germany)Deutsche Telekom Jun-98 5 MSN (USA)Microsoft home.microsoft.com Jun-98 6 Chollian (Korea (Rep.))Dacom Dec-97 7 WorldNet (USA)AT&T Jun-98 8 EarthLink Sprint (USA)Sprint, others Jun-98 9 Prodigy (USA)Prodigy Jun Infovia (Spain)Telefonica Dec Netcom (USA)ICG Jun HiNet (Taiwan-China)Chungwa Telecom Jun MindSpring (USA)MindSpring Jun SBC Internet ServicesSBC Jun Tele2 (Sweden)Tele Jun GTE Internetworking (USA)GTE Jun CWIX (USA)Cable&Wireless Jun Wanadoo (France)France Telecom Jun Netvigator (Hongkong SAR)Hongkong Telecom Mar Telia Internet (Sweden)Telia Dec-97 TOTAL, top Source: ITU Challenges to the Network: Internet for development, 1999.")

12

Market liberalisation and corporatisation/privatisation of incumbents Process and impact of liberalisation: worldwide trends (Tuesday, Session 1) Process and impact of commercialisation/privatisation: worldwide trends (Tuesday, Session 2) Towards the future: what next for telecoms businesses? (Wednesday, Session 1)

.")

13

Separation of regulatory and operational functions Of 188 ITU Member States: 156 have separated posts & telecoms (32 have not) 147 have separated regulatory and operational functions (41 have not) 132 have a regulator which is independent of the operators in terms of finance and decision- making (in 56, it is not) 83 have fully or partially privatised the incumbent operator (105 have not) 38 have liberalised basic telecom services (150 have not)

147 have separated regulatory and operational functions (41 have not) 132 have a regulator which is independent of the operators in terms of finance and decision- making (in 56, it is not) 83 have fully or partially privatised the incumbent operator (105 have not) 38 have liberalised basic telecom services (150 have not)")

14

Drafting of new telecom laws Source: ITU Telecom Regulatory Database.

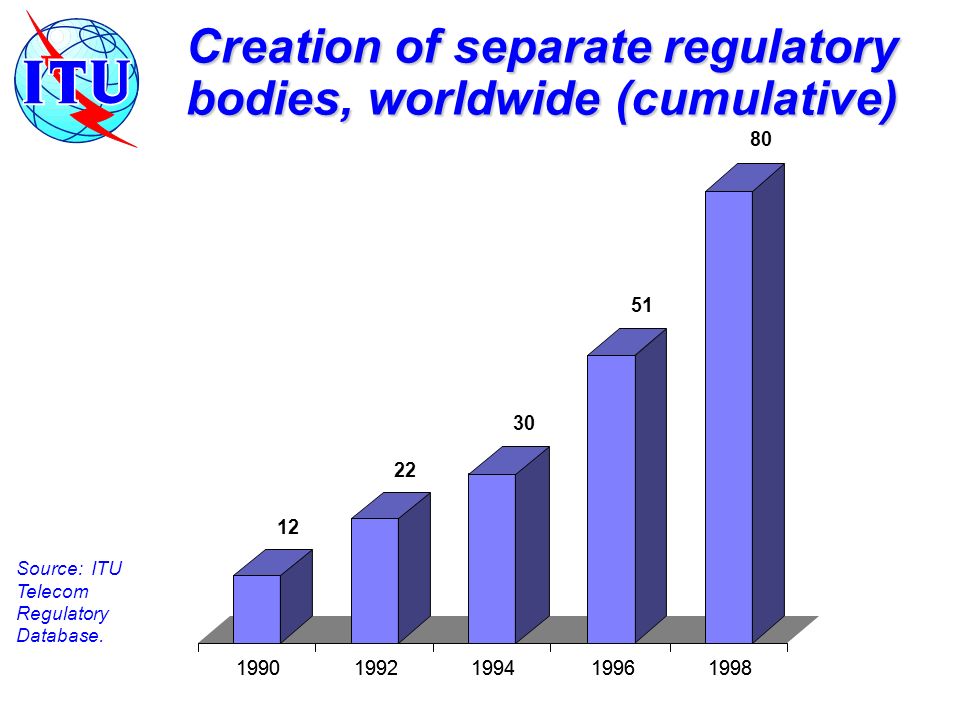

15

Creation of separate regulatory bodies, worldwide (cumulative) Source: ITU Telecom Regulatory Database. 19901992199419961998 12 22 30 51 80 19901992199419961998

16

Separate regulatory bodies, worldwide, 1998 Source: ITU Telecom Regulatory Database.

17

The development gap: Impact of the changing international telecoms environment Telecommunications development gap Narrowing between developed and middle-income developing countries Widening between middle-income developing countries and the Least Developed Countries (LDCs) New development gap emerging for advanced telecom services (Internet, broadband, multimedia) Uneven pace of market liberalisation For instance, there are more telephone companies in the UK than the whole of Africa Erosion of accounting rate system Traditional support for network roll-out

New development gap emerging for advanced telecom services (Internet, broadband, multimedia) Uneven pace of market liberalisation For instance, there are more telephone companies in the UK than the whole of Africa Erosion of accounting rate system Traditional support for network roll-out")

18

Source: ITU World Telecommunication Indicators Database. The future is here, its just not evenly distributed William Gibson Teledensity 1996 27.8 to68.3 (46) 8.6 to27.8 (45) 1.4 to8.6 (47) 0 to1.4 (48)

8.6 to27.8 (45) 1.4 to8.6 (47) 0 to1.4 (48).")

19

0% 20% 40% 60% 80% 100% Internet hosts Telephone lines TV setsPopulation High income Upper middle Lower middle Low income 1.4 billion792 m21.8 m5.8 billion Percentage of installed base, 1997 Source: ITU World Telecommunication Indicators Database.

20

Collection charge revenue, 30% Net settlements, 37% Domestic revenues, 33% Sri Lanka Developing countries typically depend on international services & settlements Source: ITU/CTO/InfoDev Country Case Studies.

21

User tariff Settlement rate Cost (low estimate) Developing countries also have relatively high cost structures (US cents per minute) 0 50 100 150 200 250 300 350 IndiaMauritaniaSri Lanka UgandaColombiaThe Bahamas SenegalSamoa Source: ITU/CTO/InfoDev Country Case Studies.

Developing countries also have relatively high cost structures (US cents per minute) IndiaMauritaniaSri Lanka UgandaColombiaThe Bahamas SenegalSamoa Source: ITU/CTO/InfoDev Country Case Studies.")

22

Settlement rates are now declining rapidly... Source: ITU-T Study Group 3 (COM 3-53). 1998 estimate is a minimum projection based on D.140 Annex D. 0.81 0.67 0.50 0.85 0.87 0.92 0.95 0.98 1.00 1.02 1.04 1.06 0 0.2 0.4 0.6 0.8 1 1.2 198719881989199019911992199319941995199619971998 Settlement rate, in SDR per minute Pre-1992 (D.140) Change = -2% p.a. 1992-1996 Change = -4% p.a. 1996-98 Change = -21% p.a. Global average

Change = -2% p.a Change = -4% p.a Change = -21% p.a. Global average.")

23

Two alternative scenarios: Source: ITU Focus Group Report, FCC. ITU Focus Group targets, by teledensity (T), to be achieved by 2001 (2004) FCC Benchmarks, by income group

, to be achieved by 2001 (2004) FCC Benchmarks, by income group.")

24

Key policy issues to be tackled Interconnection How to manage the transition to a multi-player environment? Internet Who really sets the rules? Who really gets benefits? International settlements How to transition to a cost-oriented system while providing a soft-landing for developing countries? International infrastructures How to ensure equal access at competitive rates? Investment How to increase investment, esp in LDCs?

Similar presentations

, International Telecommunication Union (ITU) Market Forecasting.>")