Download presentation

Presentation is loading. Please wait.

1

Credit Cards

2

What are the benefits? No need to carry large sums of cash Helps credit rating Have access to a written record of all purchases Rewards programs (points, cash back, frequent flyer, etc)

.")

3

Impulse Buying What is impulse buying? When a consumer purchases something to which they suddenly were attracted to and had no intention of buying previously. What is one purchase you have made on impulse? Why does having a credit card increase impulse buying?

4

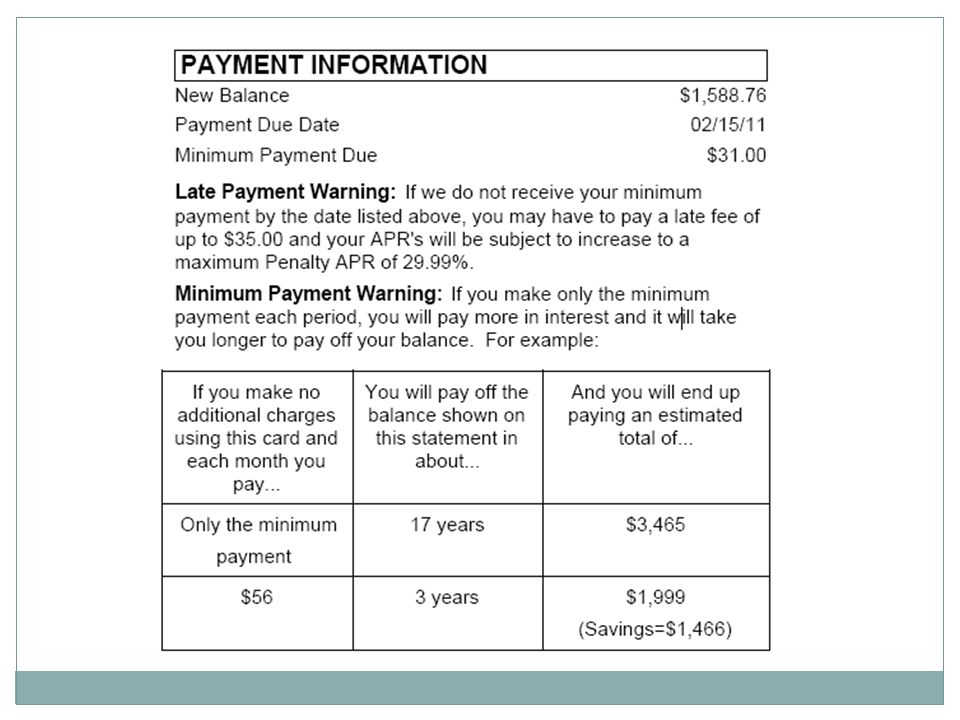

Revolving Charge Account Most common type of card Entire bill does not have to be paid in full each month. Rather, there is a minimum monthly payment, and a finance charge for all balances carried over. To avoid a finance charge, pay your bill in full each month

6

Your rights: Truth in Lending Act (1968) Protects you if your card is lost or stolen You may be partially responsible for purchases made prior to you reporting the card stolen May have to pay $50 Not responsible for any purchases made after the card is reported stolen

Protects you if your card is lost or stolen You may be partially responsible for purchases made prior to you reporting the card stolen May have to pay $50 Not responsible for any purchases made after the card is reported stolen")

7

Credit Card terms & Conditions

8

APR Annual Percentage Rate Rate at which your balance is charged to be carried over each month To find monthly finance charge, need monthly percentage rate Divide by 12

9

APR You sign up for a credit card with a 21.6% APR. What is your monthly interest rate? → 21.6% ÷ 12 = 1.8%

10

Average Daily Balance The average of the amounts you owed each day in the billing period. Changes due to purchases and payments made Most common method used in computing finance charges Gets credit card companies the most $$$

11

Finding Average Daily Balance Add the balances for every day in the billing cycle Divide by the number of days This will result in the average amount owed on each day

12

Example: Rebecca did not pay last month’s credit card bill in full. Below is a list of Rebecca’s daily balances for her last billing cycle. For seven days, she owed $456.11 For three days she owed $1,177.60 For six days she owed $990.08 For nine days, she owed $2,115.15 For five days, she owed $2,309.13

13

Example Find the sum of the daily balances: 7 (456.11) = 3,192.77 3 (1,177.60) = 3,532.80 6 (990.08) = 5,940.48 9 (2,115.15) = 19,036.35 5 (2,309.13) = 11,545.65 Total = $43,248.05

= 3, (1,177.60) = 3, (990.08) = 5, (2,115.15) = 19, (2,309.13) = 11, Total = $43,248.05")

14

Example Divide the total balance by the number of days in the billing cycle: # of days: 7 + 3 + 6 + 9 + 5 = 30 A.D.B. = $43,248.05 ÷ 30 = $1,441.60

15

One more example: Naoko has these daily balances on his credit card bill. 2 days at $99.78 15 days at $315.64 11 days at $515.64 2 days at $580.32 Find Naoko’s average daily balance

16

Example Find the sum of the daily balances: 2 (99.78) = 199.56 15 (315.64) = 4,734.60 11 (515.64) = 5,672.04 2 (580.32) = 1,160.64 Total = $11,766.84

= (315.64) = 4, (515.64) = 5, (580.32) = 1, Total = $11,766.84")

17

Example Divide the total balance by the number of days in the billing cycle: # of days: 2 + 15 + 11 + 2 = 30 A.D.B. = $11,766.84 ÷ 30 = $392.22

18

Classwork: Page 197, 2 – 9 (skip 7)

")

Similar presentations