Download presentation

Presentation is loading. Please wait.

1

Chapter 7: Demand and Supply

2

A. Demand

3

Think about a time you went shopping: Did you see something in the store and thought “who would ever buy that?!” Have you ever bought something that was unique? What was it?

4

Remember: Demand includes only those people who are willing and able to buy something Consumers have influence over the price of an item through demand Sellers decide how much to sell….this is called supply The market represents the interaction between buyers and sellers Local National International combination

5

Examples: Local: National: International: Combination:

6

Remember: Voluntary exchange includes the free choices that buyers and sellers make Buyers and sellers agree on a price Economists analyze the actions of buyers and sellers in the market place to show how supply and demand affect prices Law of demand: explains how people react to changes in price As price goes up, quantity demanded goes down As price goes down, quantity demanded goes up

7

Remember: Quantity demanded refers to the amount of a good or service that a consumer is willing and able to purchase at a specific price There is an inverse relationship between price and quantity demanded: as one goes up the other goes down

8

Why would people adjust the amount of goods or services they are willing to buy?

9

Remember: There are 3 reasons that people will adjust the amount they are willing to buy: Income effect: as a person’s income decreases, he or she will purchase less Substitution effect: people may substitute one item for another to save money Diminishing marginal utility: Utility is ability of a good or service to satisfy a need or want. As you buy more of a product, you get more satisfaction or marginal utility. This lessens with each additional product bought. The price of the product must be lowered to get you to buy.

10

B. The Demand Curve and Elasticity of Demand

11

List: Make a list of items you would buy more or less of if the price changed: Make a list of items that you would still buy the same amount of even if the price changed significantly:

12

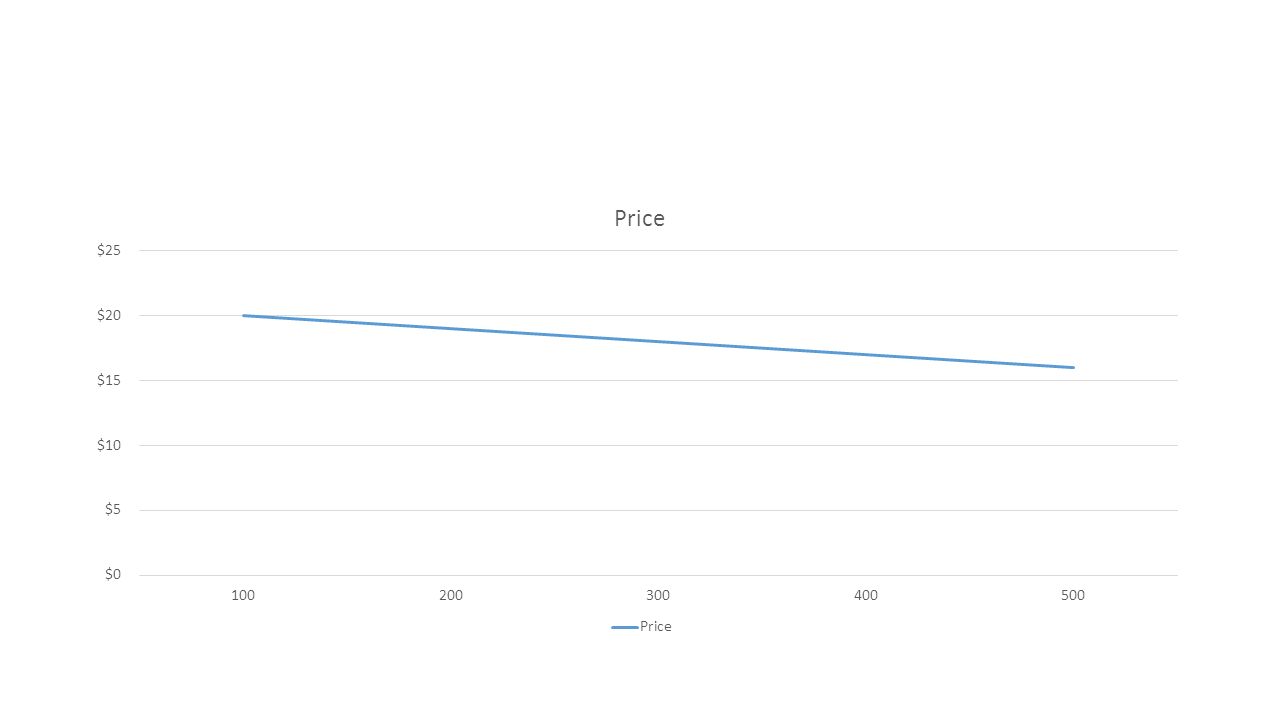

Graph a demand curve: Demand Schedule Price of dvdQuantity demanded (in millions) $20100 $19200 $18300 $17400 $16500

$20100 $19200 $18300 $17400 $16500")

13

Bottom or horizontal axis to show the quantity demanded The side or vertical axis to show price/item When plotted we end up with a demand curve

15

Remember: Quantity demanded is a specific point on the demand curve that shows how much is demanded at a specific price A change in quantity demanded is caused by a change in price and is shown by a movement to a different point along the demand curve A change in demand itself is shown by shifting the entire demand curve A shift to the left indicates a decrease in demand A shift to the right indicates an increase in demand

16

What causes changes in demand? Population Income Taste or preference (when trends change) Substitutes (a cheaper substitute will cause the demand curve for a product to shift to the left) Complementary products: peanut butter and jelly (a decrease in the price of one, will cause an increase in demand for the complementary product and the demand curve shifts right)

Substitutes (a cheaper substitute will cause the demand curve for a product to shift to the left) Complementary products: peanut butter and jelly (a decrease in the price of one, will cause an increase in demand for the complementary product and the demand curve shifts right).")

17

Price elasticity of demand Elasticity measures consumer’s responsiveness to an increase or decrease in price Price elasticity of demand measures the amount that demand varies according to the change in price Elastic demand is the increase or decrease in a consumer’s willingness to buy a product as the price increases or decreases Inelastic demand means that there is little change in a consumer’s willingness to buy a product if the price changes (see chart pg 184)

")

18

Remember: There are 3 factors that determine the price elasticity of demand for a particular product: Existence of a substitute Income available to spend Amount of time consumers are given to adjust to a new price

19

c. The Law of Supply and the Supply Curve

20

Think about a time you cooked a meal: How many of those meals could you make in 2 hours? What might the answer depend on? How could you increase your production?

21

Remember: The law of supply states that the price and quantity supplied are directly related As price for a good goes up, so does the supply As the price for a good goes down, so does the supply

22

Supply Schedule Price per movieQuantity supplied in millions $10100 $15200 $20300 $25400 $30500

23

Supply curve

24

Quantity supplied vs. supply The supply curve shows that the quantity supplied will change when the price changes (change in quantity supplied) A change in supply at every price along the curve will cause the curve to shift right or left, this is called a change in supply Increase in supply causes curve to shift right Decrease in supply causes curve to shift left

A change in supply at every price along the curve will cause the curve to shift right or left, this is called a change in supply Increase in supply causes curve to shift right Decrease in supply causes curve to shift left.")

25

There are 4 major determinants of supply price of inputs Number of firms in an industry Taxes technology

26

Law of diminishing returns As more units of a factor of production are added, at some point the rate of increased production will diminish….the producer will not see as much profit

27

Putting Supply and Demand Together

28

Note to teacher: pass out graph! Identify the supply curve Identify the demand curve Identify the equilibrium price

29

Remember: Supply and demand work together to set price A change in supply or demand(or both) will affect the equilibrium price Prices serve as signals: A shortage occurs when, at a current price, more of a product is demanded than is supplied…prices rise…demand decreases A surplus happens when suppliers produce more than consumers want at a given price…inventories build up and prices fall

will affect the equilibrium price Prices serve as signals: A shortage occurs when, at a current price, more of a product is demanded than is supplied…prices rise…demand decreases A surplus happens when suppliers produce more than consumers want at a given price…inventories build up and prices fall")

30

Sometimes the government has to intervene Price ceiling: maximum price that can be charged Rationing: limiting distribution of items that are in short supply Black market: illegal market in which high prices are charged Price floor: minimum price that can be charged

Similar presentations