Download presentation

Presentation is loading. Please wait.

1

2013 Legislative Agenda Orange County Board of County Commissioners October 16, 2012

2

Legislative Team Mission: Identify proposals that impact the county’s provision of services to citizens; Inform decision makers of positive/negative consequences of proposed legislation; Advocate fair, reasonable and balanced resolution of current and future challenges. 2013 Legislative Agenda

3

Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested 2013 Legislative Agenda

4

Presentation Outline: Legislative Overview State Budget Assessment Suggested Priorities Other Agenda Items Discussion Action Requested

5

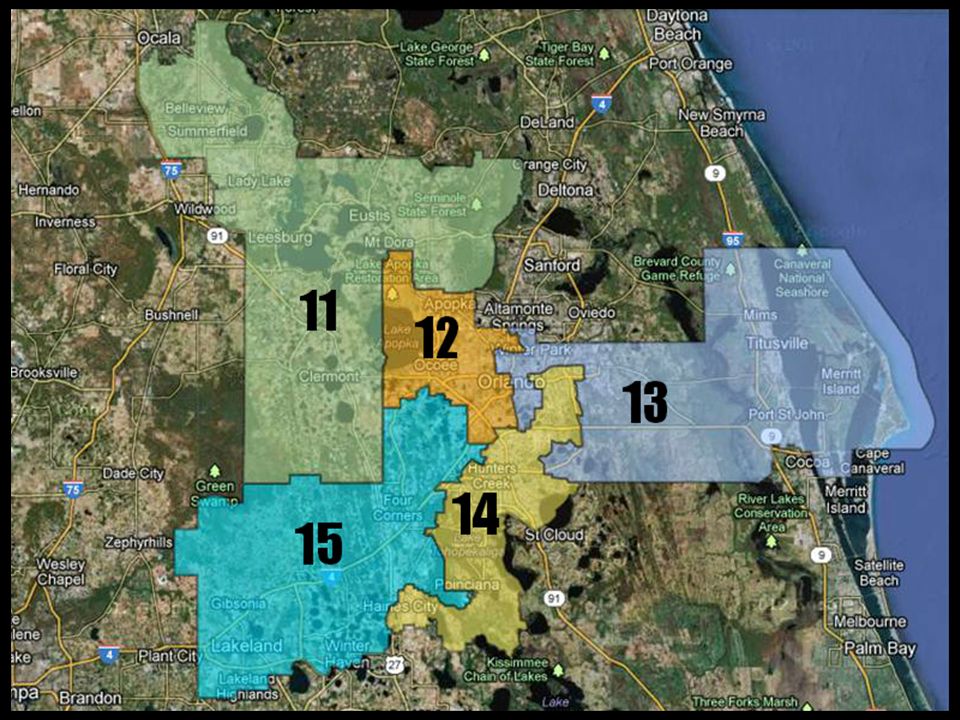

2013 Legislative Agenda Orange County Delegation Impacts of redistricting, following 2010 census: Delegation of 14, versus 16 5 Senators [ +1 ] 9 Representatives [ -3 ]

![2013 Legislative Agenda Orange County Delegation Impacts of redistricting, following 2010 census: Delegation of 14, versus 16 5 Senators [ +1 ] 9 Representatives [ -3 ]](http://images.slideplayer.com/24/6992904/slides/slide_5.jpg "2013 Legislative Agenda Orange County Delegation Impacts of redistricting, following 2010 census: Delegation of 14, versus 16 5 Senators [ +1 ] 9 Representatives [ -3 ]")

6

2013 Legislative Agenda Florida Senate President Don Gaetz District 1, Okaloosa County

8

2013 Legislative Agenda Florida House Speaker Will Weatherford District 38, Pasco County

10

Timeline 2013 Legislative Agenda Committee Week February Dec. 13 Central FL Delegation March 5 Session Begins May 3 Session Concludes Orange County Day FAC Day March 27* Reorganization November 20 Dec. / Jan. Orange County Delegation

11

2013 Legislative Agenda Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested

12

Florida’s Financial Future Dr. James A. Zingale

13

A History of Recessions Since the Great Depression…

14

*Current Recovery: 3 years, 4 months

15

Key Economic Variables: All Down Global/Nat’l Economic Conditions Population Growth Employment Growth FL Economy GDP & Personal Income Growth Tourism Credit Market (+ or -) Inventory of Unsold Homes and Commercial Space New Construction Simplified Flow of Major Drivers Financial Assets Services/Goods Need

Inventory of Unsold Homes and Commercial Space New Construction Simplified Flow of Major Drivers Financial Assets Services/Goods Need")

16

Florida’s Financial Future The economy is slowly recovering: Growth rates are gradually returning to more typical levels, but drags are more persistent than past events. It will take a few more years to climb completely out of the hole.

17

Florida’s Financial Future National Economy While most areas of commercial and consumer credit are strengthening – residential credit remains sluggish and difficult to access. So far, the recovery has been roughly half as strong as the average gain of 9.8 percent over the same period during the past seven recoveries.

18

Florida’s Financial Future State Economy A turnaround in Florida housing will be led by: Low home prices that begin to attract buyers and clear inventory Sustainable demand caused by continued population growth and household formation Florida’s unique demographics and aging of the baby-boom generation (2011!)

")

19

Florida’s Financial Future Forecast Risks Supercommittee failure triggers automatic spending cuts in 2013. ‘Automatic sequester’ ensures $1.2 trillion in spending reductions – falling equally on defense and non-defense spending – with roughly 10% cut in defense and 9% cut in non-defense. FY 2010: 8,101 Florida businesses received nearly $18.5 billion in federal contracts; vast majority defense related

20

Florida’s Financial Future Forecast Risks Sovereign debt crisis in the Eurozone has led to banking instability – with spillover effects on the global credit market. Latest Indications: Eurozone as a whole contracted 0.2% in second quarter of calendar year Greece, Italy, Spain, Finland displayed sharpest contractions Strong risk for another deep recession

21

Florida’s Financial Future Eurozone conditions have already created negative impacts on the United States economy. Currently, tighter credit conditions exist, especially for businesses with foreign interests. Reduced exports and corporate earnings already exist. Greater Miami area is experiencing a significant reduction in exports to Spain; Florida exports to Spain fell nearly 30% last year.

22

Florida: Net Migration History

23

Florida U.S. Labor Statistics Recessionary Periods and Unemployment Rates

24

Primary Funding Sources GENERAL REVENUE TRUST FUNDS Recurring and non- recurring revenues State tax revenues available to governor and legislature for any use Revenues that programs compete for, allocated between programs by governor and legislature Monies that are earmarked by law for specific purposes Governor and legislature have little discretion allocating among programs, unless law is changed

25

Program Area By Fund Source

26

General Revenue Recurring History Revenues%Appropriations%Expenditure% FY 99-00 Actual18,867.6 18,704.83.917,711.9-1.3 FY 00-01 Actual19,059.51.020,049.67.218,906.06.7 FY 01-02 Actual19,083.90.120,281.21.218,605.7-1.6 FY 02-03 Actual19,346.11.420,005.0-1.420,023.37.6 FY 03-04 Actual21,527.511.321,132.75.621,017.45.0 FY 04-05 Actual24,400.113.322,577.46.822,213.35.7 FY 05-06 Actual26,562.98.924,820.79.923,700.46.7 FY 06-07 Actual25,480.2-4.126,644.67.325,408.27.5 FY 07-08 Actual24,159.4-5.227,490.23.225,737.01.0 FY 08-09 Actual20,958.4-13.224,973.9-9.222,887.7-11.1 FY 09-10 Actual21,488.22.520,310.6-18.720,310.6-11.3 FY 10-11 Actual22,217.63.422,618.011.422,356.810.1 FY 11-12 Est.23,496.05.822,799.30.8 FY 12-13 Est.24,150.02.824,559.57.7 FY 13-14 Est.25,563.85.9 General Revenue Recurring History

27

FLORIDA COUNTIESORANGE COUNTY Taxable ValueChange% ChangeTaxable ValueChange% Change 2001802,204.4 55,904.8 2002882,238.280,033.810.058,534.42,629.64.7 2003981,794.399,556.111.362,389.53,855.16.6 20041,105,948.8124,154.512.667,095.34,705.87.5 20051,309,754.2203,805.418.475,253.28,157.912.2 20061,635,033.6325,279.524.891,811.816,558.622 20071,805,873.1170,839.510.4107,296.315,484.516.9 20081,701,867.8(104,005.3)-5.8107,014.9(281.4)-0.3 20091,499,312.2(202,555.6)-11.995,585.2(11,429.7)-10.7 20101,333,444.8(165,867.4)-11.183,586.8(11,998.4)-12.6 20111,284,383.1(49,061.7)-3.781,290.4(2,296.4)-2.7 20121,274,057.6(10,325.5)-0.881,436.2145.80.2 20131,278,154.24,096.60.382,251.5815.31.0 County Taxable Values Amounts in $ Millions

,014.9(281.4) ,499,312.2(202,555.6) ,585.2(11,429.7) ,333,444.8(165,867.4) ,586.8(11,998.4) ,284,383.1(49,061.7)-3.781,290.4(2,296.4) ,274,057.6(10,325.5)-0.881, ,278,154.24, , County Taxable Values Amounts in $ Millions")

28

Financial Outlook Overview Adjusted for August REC FY 11-12 Recurring GRNon - Rec GRTotal GR Reserves 493.6 750.0 696.8303.31,000.11,243.6 FY 12-13 Recurring GRNon - Rec GRTotal GR Reserves 708.1 444.0 (409.1)1,953.91,544.81,152.1 FY 13-14 Recurring GRNon - Rec GRTotal GR Reserves 922.6 519.2 Revenue Est. 25,563.81,953.927,517.71,441.8 Recurring Appr. (24,559.5)- Annualizations (63.6)- Critical Needs (484.6)(321.8)(806.4) **Excess Funds** 456.11,632.12,088.2 1.9% High Priority Needs (696.6)(320.3)(1,016.9) ADJUSTED FOR AUGUSTREC (240.5)1,311.81,071.3 Financial Outlook Overview

- Annualizations (63.6)- Critical Needs (484.6)(321.8)(806.4) **Excess Funds** ,632.12, % High Priority Needs (696.6)(320.3)(1,016.9) ADJUSTED FOR AUGUSTREC (240.5)1,311.81,071.3 Financial Outlook Overview.")

29

Florida’s Financial Future Dr. James A. Zingale

30

2013 Legislative Agenda Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested

31

Draft Priorities: Online Hotel Room / DOT COM Eliminate the TDT and sales tax ‘exemption’ that exists between wholesale and final price Medicaid Billing deadlines should follow the process to reconcile errors; revenue share policy 2013 Legislative Agenda

32

Business Tax Maintain funding option, along with flexibility in use Pre-Trial Release Maintain county’s pre-trail services program for eligible inmates Regional Transportation Authority Support regional coordination, while ensuring revenues are not diverted 2013 Legislative Agenda

33

Home Rule: Pill Mill Regulation Maintain local government flexibility, no state preemption Fertilizer Regulation Maintain local government flexibility, no state preemption 2013 Legislative Agenda

34

Support Oppose: SUPPORT: Department of Juvenile Justice equity for pre-adjudication and post- adjudication costs SUPPORT: Transportation projects critical to Orange County SUPPORT: Main Street Fairness initiatives 2013 Legislative Agenda

35

OPPOSE: Repealing the Mark Wandall Safety Act (i.e. Red Light Camera Enforcement) OPPOSE: Expansion and/or new authority for casino and internet gambling 2013 Legislative Agenda

OPPOSE: Expansion and/or new authority for casino and internet gambling 2013 Legislative Agenda.")

36

Monitor: Amendment 10 Implementation* Animal Services Communications Service Tax Environmental Resource Permitting Florida Retirement System Funding Opportunities Septic Tank Inspection Water Policy 2013 Legislative Agenda

37

Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested

38

Other Agenda Items: Cost Shifts & Unfunded Mandates Oppose attempts to balance state budget at local tax payers’ expense Regulatory Streamlining Support sensible streamlining legislation 2013 Legislative Agenda

39

Community Partners: When not adverse to Orange County interests, support legislative priorities of community partners such as: Florida Association of Counties University of Central Florida, Valencia College MetroPlan Orlando LYNX Metro Orlando EDC Orange County Health Department 2013 Legislative Agenda

40

Commissioner Issues: Commissioner Moore Russell Concealed weapons in parks and government buildings 2013 Legislative Agenda

41

Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested

42

2013 Legislative Agenda Presentation Outline: Legislative Overview State Budget Assessment Draft Priorities Other Agenda Items Discussion Action Requested

43

Action Requested: Approval of Legislative Priorities for the 2013 Legislative Session 2013 Legislative Agenda

44

Orange County Board of County Commissioners October 16, 2012

Similar presentations

CHIEF ECONOMIST COLORADO LEGISLATIVE COUNCIL FEBRUARY 24, 2011 303-866-4778>")