Download presentation

Presentation is loading. Please wait.

1

Stress-testing the capital input measures in the EUKLEMS database Nicholas OULTON LSE, UCL and NIESR and Ana RINCON-AZNAR NIESR March 2007 Paper to be presented at the meeting of the EUKLEMS Consortium, Brussels, March16-17, 2007 This research was made possible by financial support under the 6th Framework Programme of the European Commission to the EU KLEMS Project on Productivity in the European Union. The views expressed are our own.

2

Outline Aim of the study: Stress-testing capital input measures in the EUKLEMS database Estimating the average real rate of return: methodology and results Conclusions Further work

3

The spirit of the new SNA Capital stocks, capital services and capital consumption should all be estimated in an intellectually consistent way. All underlying data should be consistent (see OECD manuals). Gross operating surplus is the return to capital = the sum of the returns to each asset

. Gross operating surplus is the return to capital = the sum of the returns to each asset.")

4

Stress testing The user cost has three elements: Depreciation Capital gain/loss Rate of return The average rate of return is implicit in the other estimates Is the implied rate of return plausible?

5

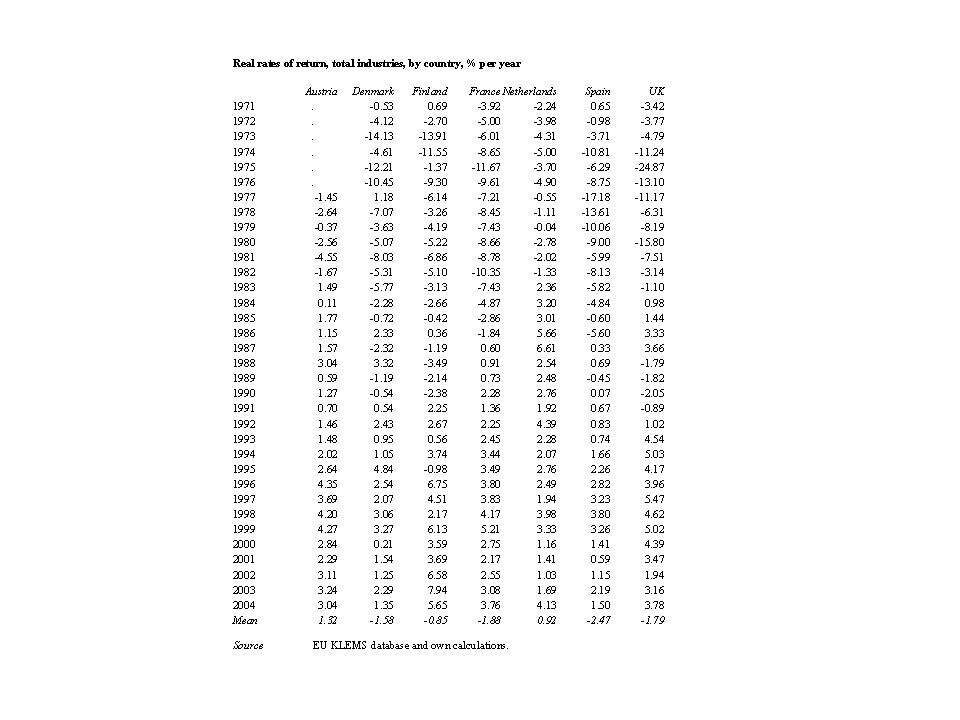

A plausible picture: the UK, 1970-2000 Source: Bank of England Industry Dataset

6

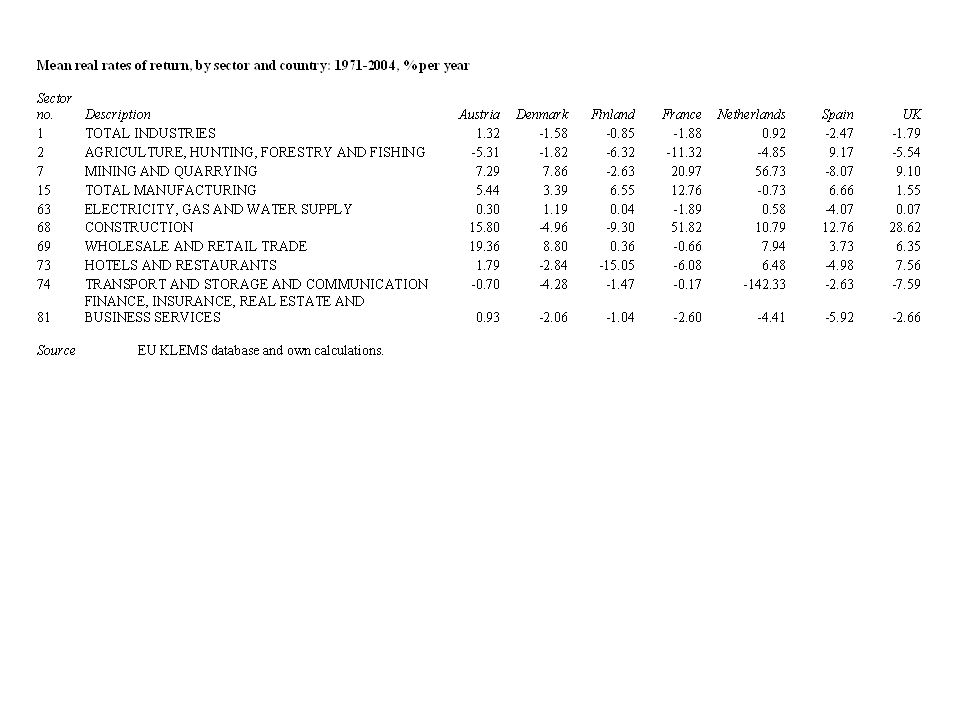

Estimating the rate of return (1) Mean nominal rate of return in a sector/industry:

Mean nominal rate of return in a sector/industry:")

7

Estimating the rate of return (2) Mean real rate of return:

Mean real rate of return:")

8

Reasons why the estimates may be wrong 1.Asset stocks: allocation of investment across industries may be wrong 2.Tax factors are needed for calculating depreciation and capital gains, but are not (yet) available in EU KLEMS 3.Some assets that generate profits may be missing, eg inventories, land, R&D, intangibles

available in EU KLEMS 3.Some assets that generate profits may be missing, eg inventories, land, R&D, intangibles")

12

Is there a pattern? (1) Dummy variable model Dependent variable: real rate of return Independent variables: dummies for countries, sectors, and years Drop extreme observations (r 50): N was 7859, now 5744 (2115 obs. dropped)

Dummy variable model Dependent variable: real rate of return Independent variables: dummies for countries, sectors, and years Drop extreme observations (r 50): N was 7859, now 5744 (2115 obs. dropped).")

13

Is there a pattern? (2) Results of dummy variable model (after dropping extreme obs.) Country dummies (Austria omitted) Coef.|t-ratio| Denmark -2.42 5.2 Finland-3.176.8 France2.084.4 Netherlands-0.952.0 Spain-0.120.3 UK-1.623.5 N5744 R2R2 0.38

Results of dummy variable model (after dropping extreme obs.) Country dummies (Austria omitted) Coef.|t-ratio| Denmark Finland France Netherlands Spain UK N5744 R2R")

14

Is there a pattern? (3)

")

15

Is there a pattern? (4) Year dummies (1971 omitted) Coefficient |t-ratio| 1972-2.12-2.0 1973-6.52-6.2 1974-7.84-7.5 1975-10.09-9.6 1976-9.15-8.7 1977-6.09-6.0 1978-5.69-5.6 1979-4.68-4.6 1980-7.18-7.1 1981-7.21-7.1 1982-5.44-5.4 1983-2.35-2.3 1984-0.55-0.6 19851.151.1

Year dummies (1971 omitted) Coefficient |t-ratio|")

16

Conclusions The differences between countries and across sectors in estimated real rates of return are larger than can be explained by differences in economic fundamentals Tentative explanations: 1.The allocation of investment across industries may be at fault 2.The initial capital stocks may be too high

17

Further work… Extend analysis to rest of EU-25 countries Second part of stress-testing: calculate sensitivity of capital input estimates to method employed –Using estimates of rates of return, calculate contribution of capital to growth by ex-post, ex-ante and hybrid methods

Similar presentations

>")