Download presentation

Presentation is loading. Please wait.

1

David Stark Columbia University Moscow 28 October 2012 Peripheral Vision in Financial Markets

2

My research collaborators: Daniel Beunza London School of Economics Supported by the National Science Foundation and a fellowship from The Netherlands Institute for Advanced Study. Matteo Prato University of Lugano

3

The origins of the new economic sociology Parsons Pact

4

The origins of the new economic sociology Parsons Pact You, the economists, get value; we, the sociologists, get values. You study the economy; we will study the social relations in which economies are embedded.

5

Two dominant schools in economic sociology: Economies are embedded in cultural values (and cognitive frames). Economies are embedded in social relations. In both approaches, calculative practices are left unexamined.

6

STS enters Economic Sociology Michel Callon (France) Donald MacKenzie (Great Britain) Karin Knorr-Cetina (Germany) And their students Fabian Muniesa Vincent Lepinay Yuval Milo Alex Preda

Donald MacKenzie (Great Britain) Karin Knorr-Cetina (Germany) And their students Fabian Muniesa Vincent Lepinay Yuval Milo Alex Preda")

7

Network analysis in economic sociology views economies as embedded in social relations. In our view: Calculation is not embedded in social relations. Calculation is itself social. Calculation is socio-technically distributed. What counts? Bring tools into accounts about what counts.

9

This is a pipe organ in largest hall of Moscow House of Music. Posted by Irina at 20:5520:55 Labels: instuments, theatreinstumentstheatre A declarative

10

I apologize. A performative

11

Performativity (following MacKenzie): Financial models are not representations. They are interventions that format, shape, perform markets. Their use brings new economic objects (markets) into being.

into being..")

15

This is the way that people get from point A to point B.

17

Performativity (in my defintion): A model is performative when its use increases its predictive capabilities.

: A model is performative when its use increases its predictive capabilities.")

18

From Perfomativity to Reflexivity

19

Institutionalism in economic sociology focuses on routines, scripts, taken-for- granteds, and unreflective action. In my view: the performativity view ignores skilled performance. Why should we deny to actors the reflexivity that we prize and praise in our own profession?

20

Key, in thinking about distributed cognition and distributed reflexivity: A new form of sociality disembedded yet entangled; anonymous yet collective; screen-mediated yet differentiated; impersonal yet emphatically social.

21

Research with Daniel Beunza

22

How do traders deal with the fallibility of their models?

23

This is a pipe organ.

26

The arbitrage traders we studied do the same.

27

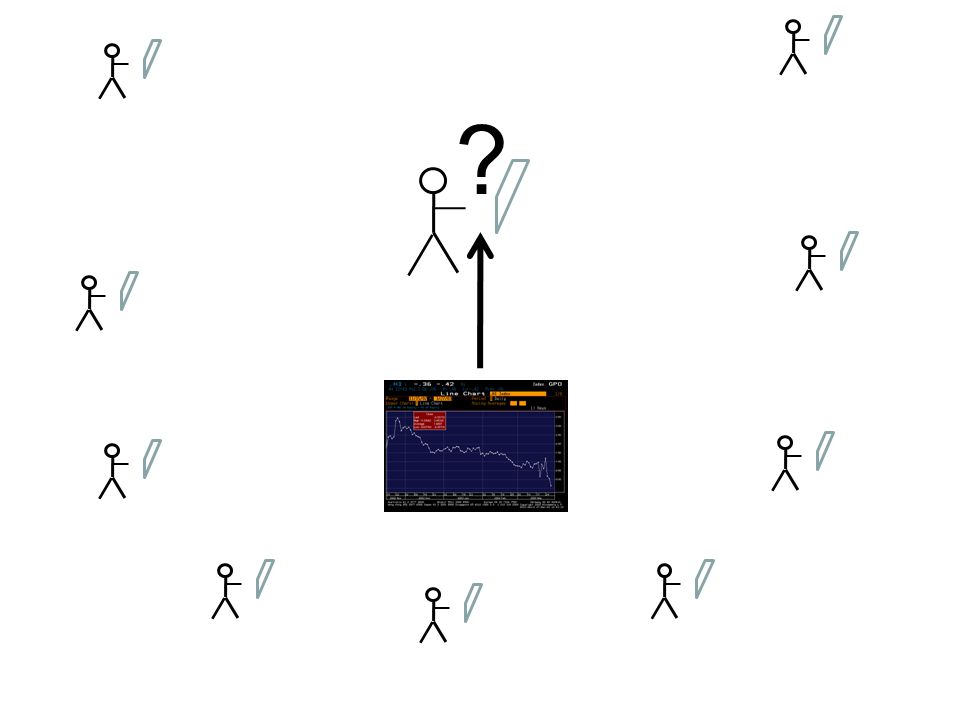

The trading room is populated with devices for doubt. Traders do not simply use models and devices that perform the market. They also create and use devices for reflexivity. This reflexivity is not exterior to (or above) the structures of socially distributed calculation but is an integral part of it.

the structures of socially distributed calculation but is an integral part of it..")

28

Arbitrage is a (reflexively) skilled performance. And this reflexivity is not of the individual but is social and material.

29

Cognitive challenges of using models in arbitrage

30

Calculation in merger arbitrage involves the dissonance between two sets of probability estimates: 1) probability estimates derived at the desk using proprietary models, databases, and instrumentation. 2) implied probablity – the aggregate probability estimates of the traders rivals

implied probablity – the aggregate probability estimates of the traders rivals.")

32

a given trading desk makes probability estimates based on models, proprietary databases, and instrumentation

33

V= (1- )P NS + P S

P NS + P S")

35

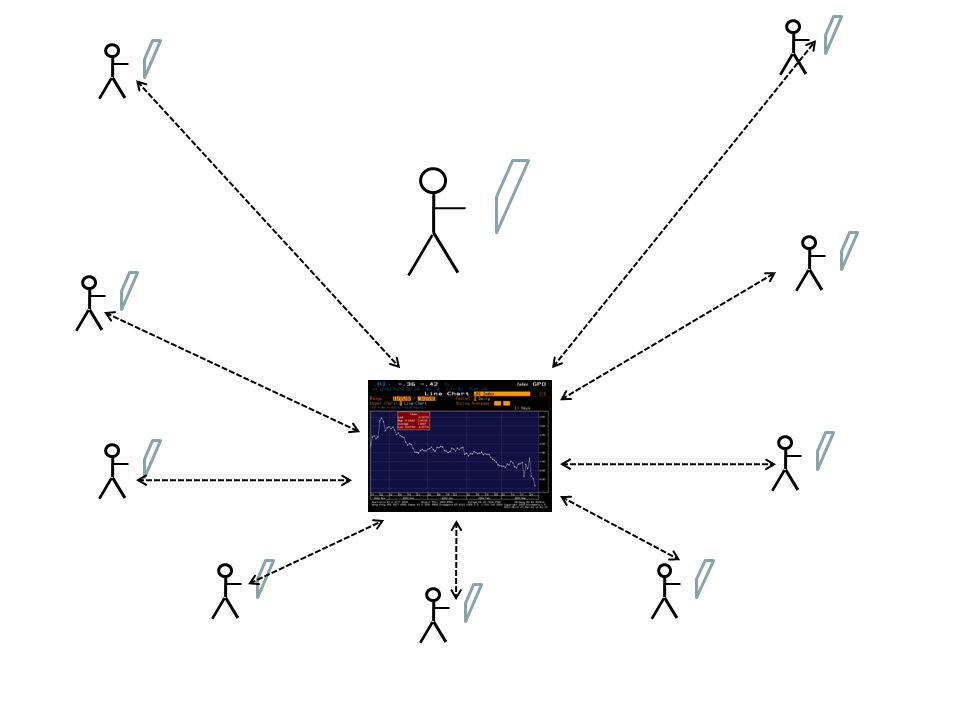

The traders models and instrumentation are powerful scopes for viewing the markets.

36

But scopes that reveal can also conceal. If you take your model for granted, you can lose your shirt.

37

To avoid cognitive lock-in, the traders turn to socio- technical networks outside the trading room.

38

relation between the trader and his rivals

40

Seeing the screens of ones rivals is not possible.

44

The spread plot

45

The spread plot is a representation of an economic object that does not have a price and is otherwise not observable, co-produced by the positioning of actors who use it to confront their interpretations and re-evaluate their positions.

46

time $ Target Acquirer Decoding the spread plot Backing out implied probability

47

The spread plot instantiates the diversity of dispersed anonymous actors.

50

dissonance

51

Reflexive modeling Dissonance disrupts. It prompts reflexivity.

53

?

54

re-search

55

Reflexive modeling Differs from herding Here, dissonance prompts re-search

56

Reflexivity is not self-awareness or conceptual transcendence. So as not to be captive of an epistemic trap, traders use devices for dissonance.

57

Models have given rise to a new mode of sociability: disembedded yet entangled, anonymous yet collective, impersonal yet nevertheless social.

58

WARNING

59

In cases lacking diversity, devices for dissonance become devices for overconfidence. Resonance blocks reflexivity and can lead to collective calamity.

60

The strength of reflexive modeling is based on the fact that it leverages the cognitive independence among dispersed and anonymous actors.

61

But this same process suggests the possibilities of cognitive interdependence among the rival traders in the professional arbitrage community.

62

Reflexive modeling is born of the effort to avoid cognitive lock-in. But absent dissonance, through this cognitive interdependence, it leads to a collective cognitive lock-in that can yield disaster.

63

Just as reflexive modeling can typically be a source of correction, so this same cognitive interdependence among traders can, in rare but dramatic instances, lead to the amplification of error.

64

From cognition as categorical to cognition as perspectival Research with Matteo Prato

65

Dominant view reduces cognition to categories Compare the object to the categorical ideal; penalize if a categorical mismatch (Zuckerman 1999, 2004).

.")

66

Valuation always takes place in a calculative space. The most primitive aspect of a calculative space is the other objects in the field of attention. Distributed cognition in two-mode networks

67

Location and allocation Focus – locate an object by allocating attention. Make associations across these objects and situations and not simply comparisions to the categorical ideal.

68

Interobjectivity Exploit the network ties that are created when multiple agents allocate their attention across multiple objects. Study socially peripheral vision.

69

Valuation is perspectival With apologies to Pierro della Francesca

70

Valuation is perspectival

72

How we assess an object or interpret a situation is shaped against the background of the other objects or situations across which we allocate our attention.

73

Viewpoints, views, peripheral visions The two-mode (agents-objects) structure of an attention network is a calculative space. My views about a given focal asset are shaped by your views and viewpoints about other assets. In fact, what is in your peripheral vision can effect my focus.

74

Data Securities analysts -Stock coverage of US publicly listed firms -Earnings per share estimates I/B/E/S for 1994-2006 Approx. 8,000 analysts, 15,000 firms, and several million analyst-firm observations.

75

Viewpoints matter. If how an actor interprets a given situation depends on the portfolio of situations that are in her field of view, then we expect that: Hypothesis 1: Greater change in the portfolio of background situations will result in greater change in assesment of the focal issue.

76

Viewpoints matter. If how an actor interprets a given situation depends on the portfolio of situations that are in her field of view, then we further expect that: Hypothesis 2: The more similar their portfolios of background situations the more similar will be two actors assessments of the focal issue even when they have not seen each others estimates.

77

Peripheral Vision. Because actors are influenced by views in their peripheral vision, we expect that Hypothesis 3 The more (less) two actors have encountered each others views on other situations, the more their interpretations of a given situation will converge (diverge).

two actors have encountered each others views on other situations, the more their interpretations of a given situation will converge (diverge)..")

78

Peripheral Vision. Because actors are influenced by views in their peripheral vision, we further expect that Hypothesis 4 This convergence (divergence) will be greater the more they have been exposed to interpretations of same (different, i.e., non-shared) third actors.

will be greater the more they have been exposed to interpretations of same (different, i.e., non-shared) third actors..")

79

Hypothesis 1 individual, 2 moments in time Hypothesis 2 dyad, same moment in time Hypothesis 3 dyad, over time Hypothesis 4 open or closed triad, over time

Similar presentations

Awareness.>")

Course : Security Analysis and Portfolio Management Unit I: Introduction to Security Analysis Lesson No. 1.3–>")