Download presentation

Presentation is loading. Please wait.

1

REINSURANCE: small, limited underwriting products VS large, fully underwritten products

3

www.finmark.org.za

4

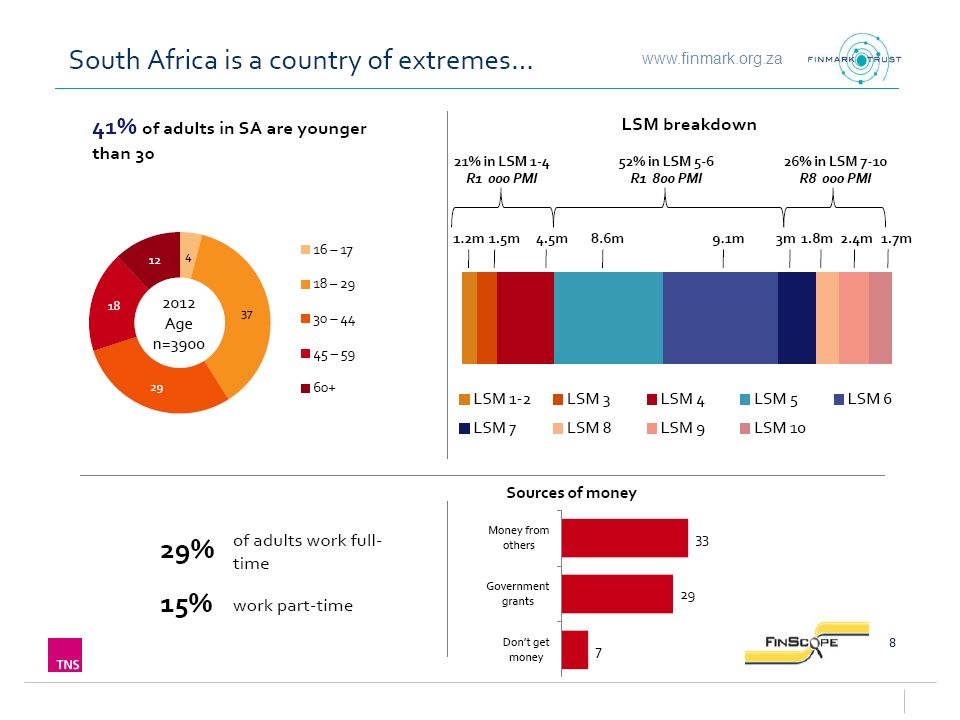

Insurance take up across LSM groups

5

Transforming financially www.finmark.org.za

6

Transforming financially www.finmark.org.za

7

THE SOUTH AFRICAN SPECTRUM CUSTOMERS PRODUCT TYPES BENEFITS AND PREMIUMS FEATURES RISK MANAGEMENT HIV TESTING UNDERWRITING LIMITED UNDERWRITING FULL UNDERWRITTEN

8

Different Risks: The moment you go into different markets you assume different risks…

9

Fully Underwritten vs Limited Underwriting Customers “Millennials” “Boomers and Gen X”

11

Fully vs Limited Underwriting: Product types Death Critical Illness Functional impairment Disability -lumpsum Disability – Income Credit Life Funeral Cover Accidental Cover Cancer Cover Hospital Cash

12

Benefits and Premiums Fully U/WLimited U/W Rating FactorSocio Economic (LSM) - Income, education Gender, Smoking loadings Make use of Data Analytics to determine optimal rate variations Premium Patterns Range of patterns -Level -fixed increases -age rated Single Premium Pattern, with automatic changes DesignHigh maximum cover levels - Disability capped at 100% replacement ratio Low Maximum cover levels T&C’sDetermined after underwriting, depending on the information disclosed Standard exclusions - pre-existing conditions - Accidental death only etc Underwriting result Accept, decline, loaded, deferred, additional medical requirements, exclude Accept or decline

- Income, education Gender, Smoking loadings Make use of Data Analytics to determine optimal rate variations Premium Patterns Range of patterns -Level -fixed increases -age rated Single Premium Pattern, with automatic changes DesignHigh maximum cover levels - Disability capped at 100% replacement ratio Low Maximum cover levels T&C’sDetermined after underwriting, depending on the information disclosed Standard exclusions - pre-existing conditions - Accidental death only etc Underwriting result Accept, decline, loaded, deferred, additional medical requirements, exclude Accept or decline")

13

Product Features Fully U/WLimited U/W ConvenienceCompliance ProcessComplete at end of Call UnderwritingMedical and HIV tests requiredSpecific Medical only; HIV test after application only AcceptanceCover granted after completion of U/W Cover cancelled for dishonesty in application CostHigh – Commission; Medical testsLow – large volumes StructureMultiple variations. riders and claim definitions Single, “vanilla” format only Distribution channel Questions answers by agent/broker Call Center / on-line / mobile application ExclusionsFew, reflecting U/W resultsMany standard policy exclusions Margins5-8%Excess of 20% ScaleLimited to agent or broker network Very, especially on-line or mobile platforms

14

Risk Management Options Fully U/WLimited U/W Reinsurance: Surplus treatyReinsurance: Quota Share or stop-loss agreements Important to really understand the risk – ask for lots of information Avoid asking unnecessary questions – Smart underwriting / Analytics Meeting the claim condition, proof of loss of income Exclusions of Pre-existing conditions and limited risks covered Financial Underwriting to limit exposurePhased in Waiting periods on risks covered and sum assured Claims Assessor trainingLimited sums assured size and have clear claim definitions Broker and agent analysisPattern recognition for fraud Automated systems needed to red flag risky policies and claims

15

HIV testing requirements HIV testing type Laboratory (4th Gen Combination test), or Spot/Rapid test (finger prick or saliva) Accuracy and retest of results, speed of result, costs If HIV+ Limited U/W products allow post acceptance testing Only allow accidental death or reduced Sum Assured Managed care products allow cover to be retained Need to monitor CD4 count: Remove natural death cause cover if below required level

, or Spot/Rapid test (finger prick or saliva) Accuracy and retest of results, speed of result, costs If HIV+ Limited U/W products allow post acceptance testing Only allow accidental death or reduced Sum Assured Managed care products allow cover to be retained Need to monitor CD4 count: Remove natural death cause cover if below required level")

16

Underwriting Efficiency Limited underwriting Mostly a few underwriting questions (medical focus) Use automated rules and decision trees Make certain the appropriate questions are asked Make use of an expert underwriting system Make best use of limited time Fully underwritten Questions on various risk areas, medical exam and bloods Most still use manual (human) underwriting process Slower, less consistent but free text not an issue & don’t miss any information Starting to use Expert U/W System – some input from UWs still required

Use automated rules and decision trees Make certain the appropriate questions are asked Make use of an expert underwriting system Make best use of limited time Fully underwritten Questions on various risk areas, medical exam and bloods Most still use manual (human) underwriting process Slower, less consistent but free text not an issue & don’t miss any information Starting to use Expert U/W System – some input from UWs still required")

17

Rent a body – get a death certificate Rent an Identity document – cross check IDs Rent a doctor – find pattern of doctor/hospital name Hospital Bed & Breakfast – require stays of >3 days Stolen medical records - ??? Source: SAICB How to Fraudulently claim….

18

The future of limited underwriting Millennials want simple products Don’t care about reading the contract Price, convenience and accessibility key factors Must be low cost and easy to complete the transaction Determine risk via smart underwriting Only give cover for specified risks – exclusions and waiting periods key – But do they understand when they can claims or NOT Control risk by looking for patterns Analyse data to identify systematic causes of fraud

19

Visit genre.com for more info. Adriaan Rowan

Similar presentations

End time: ____ Please set phones to silent ring and answer outside of the room.>")

© AmericoFor agent use only. Not for public use.Policy Series 281/282/283/284.>")