Download presentation

Presentation is loading. Please wait.

1

LABOUR COSTING

2

Introduction Labour cost is one of the important elements of production. Wage, salaries and other incentives of employee remuneration constitute a very large component of operating costs. Remuneration of employees is a vital factor not only affecting the cost of production but also industrial relation relations of the organisation.

3

Introduction No organization can expect to attract and attain qualified and motivated employees unless it pays them fair remuneration. Employee remuneration therefore influences vitally the growth and profitability of the company. For employees, remuneration is more than a means of satisfying their physical needs. Wages and salaries have significant influence on distribution of income, consumption, savings, employment and prices. Thus. employee remuneration is a very significant issue from the viewpoint of employers, employees and the nation as whole.

4

Objectives of an Ideal Wage System

An ideal wage system is required to achieve the following objectives: The wage system should establish a fair and equitable remuneration. A sound wage system helps to attract qualified and efficient worker by ensuring an adequate payment. It assists to improve the motivation and moral of employees which in turn lead to higher productivity. It enables effective control of labour cost. An Ideal wage system helps to improve union-management relations. It should reduce grievances arising out of wage inequities. It should facilitate job sequences and lines of promotion wherever applicable. An ideal system seeks to project the image of a progressive employer and to comply with legal requirements relating to wages and salaries.

5

Principles of an Ideal Wage System

The following principles should be adopted for an ideal wage system: Differences in pay should be based on differences in job requirements. Follow the principle of equal pay for equal work. The scheme should be based on work study, and the work contents of various jobs should be stabilized. Recognize individual differences in ability and contributions. The scheme should not be very costly in operation. The scheme should be flexible. The scheme should encourage productivity. The scheme should not undermine co-operation amongst the workers. The scheme should be sufficient to ensure for the worker and his family reasonable standard of living.

6

Method of Remuneration

There are two basic methods of wage payment: (1) Time Wage System and (2) Piece Wage System. Under time wage system. wages are paid on the basis of time spent on the job irrespective of the amount of work done. This is known as Time Rate or Day Wage System. The unit of time may be a day, a week, a fortnight or a month. Under piece wage system, remuneration is based on the amount of work done or output of a worker. This is known as "Piece Rate System" or "Payment by Result." Thus. a workman is paid in direct proportion to his output. A variety of bonus and premium plans have been designed to overcome the drawbacks of two basic methods of wage payments. A system of incentive plans also takes into consideration the primary principles of these two basic plans known as Incentive or Bonus or Premium Plan.

Time Wage System and (2) Piece Wage System. Under time wage system. wages are paid on the basis of time spent on the job irrespective of the amount of work done. This is known as Time Rate or Day Wage System. The unit of time may be a day, a week, a fortnight or a month. Under piece wage system, remuneration is based on the amount of work done or output of a worker. This is known as Piece Rate System or Payment by Result. Thus. a workman is paid in direct proportion to his output. A variety of bonus and premium plans have been designed to overcome the drawbacks of two basic methods of wage payments. A system of incentive plans also takes into consideration the primary principles of these two basic plans known as Incentive or Bonus or Premium Plan.")

7

Method of Remuneration

The following are the important methods of remuneration which may be grouped into : Time Rate Systems Piece Rate Systems Bonus System (or) Incentives Schemes. Indirect Monetary Incentives. These may be further classified as under:

Incentives Schemes. Indirect Monetary Incentives. These may be further classified as under:")

8

Method of Remuneration

Time Rate Systems: At Ordinary Levels At High Wage Levels Guaranteed Time Rates. Piece Rate Systems: Straight Piece Rate Piece Rates with Guaranteed Time Rate Differential Piece Rates: Taylor's Differential Piece Rate System Merrick Differential Piece Rate System Gantt Task and Bonus Plan.

9

Bonus System or Incentive Schemes:

Halsey Premium Plan Halsey-Weir Premium Plan Rowan Plan Barth Variable Sharing Plan Emerson Efficiency Plan Bedaux Point Premium System Accelerating Premium Plan Group or Collective Bonus Plans. Indirect Monetary Incentives: Non-Monetary Incentives:

10

Comparison between Time Rate and Piece Rate System

11

Time Wage System Time Rate at Ordinary Levels: This is also termed as "Day Wage System" or "Flat Rate System." Under this system, wages are paid to the workers on the basis of time spent on the job irrespective of the quantity of work produced by the workers. Payment can be made at a rate per day or a week, a fortnight or a month. The formula for calculation of payment of time rate of ordinary levels is as follows:

12

Remuneration or Earnings = Hours Worked X Rate Per Hour

Time wage system is suitable under the following conditions: Where the units of output are difficult to measure, e.g., watchman. Where the quality of work is more important, e.g., artistic furniture, fine jewellery, carving etc. Where machinery and materials used are very sophisticated and expensive. Where supervision is effective and close supervision is possible. Where the workers are new and learning the job. Where the work is of a highly varied nature and standard of performance cannot be established.

13

Advantages of Time wage system

It is simple and easy to calculate. Earning of workers are regular and fixed. Time rate system is accepted by trade unions. Quality of the work is not affected. This method also avoids inefficient handling of materials and tools.

14

Disadvantages No distinction between efficient and inefficient worker is made and hence they get the same remuneration. Cost of supervision are high due to strict supervision used for high productivity of labour. Labour cost is difficult to control due to more payment may be made for the lesser amount of work. No incentive is given to efficient workers. It will depress the efficient workers. There is no specific standards for evaluating the merit of different employees for promotions.

15

Time Rate at High Levels: Under this system, efficient workers are paid higher wages in order to increase production. The main object of this method designed to remove the drawbacks of time rate at ordinary levels. This system is simple and easily understandable. When higher rate of wages are paid, it does not only reduce labour turnover but also increases production and efficiency. Guaranteed Time Rates: Under this method, the wage rate is calculated by considering changes in cost of living index. Accordingly, the wage rate is varied for each worker according to the change in cost of living index. This system is suitable during the period of raising prices.

16

Piece Rate System This is also known as "Piece Wage System" or "Payment By Result." Under this system, wages of a worker are calculated on the basis of amount of work done or output of a worker. Accordingly, a worker is paid in direct proportion to his output.

17

Advantages It facilitates direct relation between efforts and reward.

This system encourages the efficient workers to increase production. Under this system efficient workers are recognized and rewarded. It helps to reduce the cost of supervision and idle time. Tenders or quotations can be prepared confidently and accurately.

18

Disadvantages Where a concern is producing large quantities, it is difficult to fix a piece rate. In order to maximize their earnings, workers working with high speed may affect their health. The quality of output cannot be maintained. This system is not encouraging to the inefficient workers. Temporary delays or difficulties may affect the earnings of the workers.

19

Piece Rate System is Suitable Where

Quality and workmanship are not important. Work can be measured accurately. Quantity of output directly depends upon the efforts of the worker. Production of standardized goods in a factory. Job is of a repetitive nature.

20

Piece Rate Payment Methods

There are three important methods of paying labour remuneration falling under this type Straight Piece Rate Piece Rates with Guaranteed Time Rates and Differential Piece Rates.

21

Straight Piece Rate Under this system, workers are paid according to the number of units produced at a given rate per unit. Thus, total earnings of each worker is calculated on the basis of his output irrespective of the time taken by him. The following formula is used for measuring piece work earning: Straight Piece Work Earnings = Units Produced x Rate Per Hour

22

Piece Rates with Guaranteed Time Rates:

Under this method, the worker earning from piece work less than the guaranteed minimum wage, will get the fixed amount of guaranteed time rate. A guaranteed rate would be paid per hour rate or day rate or week rate.

23

Differential Piece Rates:

This system is designed to provide for variation of piece rates at different levels of output. Accordingly increase in wages is proportionate to increase in output. Under this system, efficient workers get ample reward and at the same time inefficient workers are motivated to earn more. The following are the three important types of differential piece rates : Taylor's Differential Piece Rates System. Merrick's Differential Piece Rates System. Gantt Task Bonus Plan.

24

Taylor's Differential Piece Rates System

FW. Taylor, who is the father of scientific management introduced this plan. Under this system, two piece rates are applicable on the basis of standard of performance established. Accordingly one is high rate and the other one is lower rate. Thus high piece rate is applicable for standard and above the standard performance. Lower piece rate for those workers with below the standard performance.

25

Illustration: 1 Calculate the earnings of workers A and B under Straight Piece Rate System and Taylor's Differential Piece Rate System from the following particulars: Standard time allowed 50 units per hour. Normal time rate per hour Rs.100. Differentials to be applied. 80% of Piece rate below standard. 120% of Piece rate at or above standard. In a day of 8 hours A produced 300 units and B produced 450 units.

26

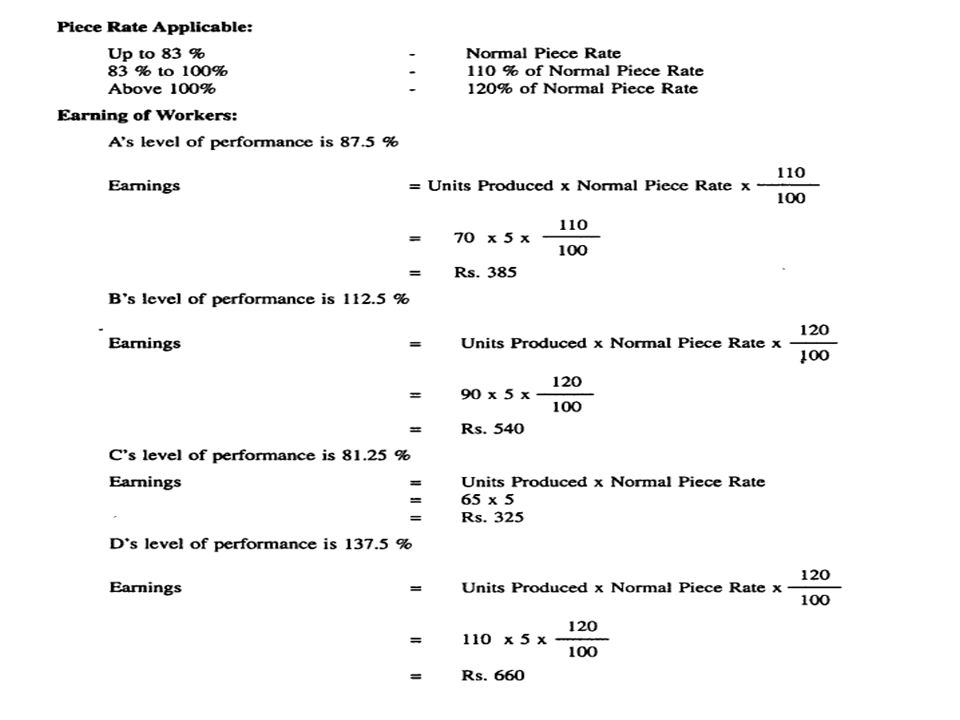

Merrick Differential Piece Rate System

This is also termed as Multiple Piece Rate system. This plan is 'designed to overcome the drawback of Taylor's Differential Piece Rate System. Under this method, three piece rates are applied with different levels of performance. Accordingly

28

Illustration: 2 From the following particulars calculate the total earning of the three workers under Merrick Differential Piece Rate System. Normal rate per hour Rs. 5 per unit Standard production per hour 10 units In an 8 hours a day: A produced 70 units. B produced 90 units. C produced 65 units. D produced 110 units

29

Solution:

31

Gantt's Task Bonus Plan This system is designed by Henry L. Gantt.

Under this system, standard time for every task is fixed through time and motion study. The main feature of this system is a good combination of time rate, differential piece rate and bonus. In this system day wages are guaranteed to all workers. Wages under this system are calculated as follows :

32

GANTT’S TASK BONUS PLAN

33

Illustration: 3 From the following particulars, calculate total earnings of each worker under Gantt's Task Bonus Scheme: Standard production per week per worker is 2000 units, piece work rate Rs. 0.5 per unit Actual production during the month : A-10OO units B units C units

34

Solution: Standard production per month = 2000 units Piece work rate = Rs per unit . '. Guaranteed Time Rate = 2000 X 0.5O = Rs 1000

35

Solution :EARNINGS: A (50% Below standard) B (100% efficiency)

C (125% efficiency above standard) Rs 1,000 (Guaranteed Monthly wages) 2000 units x Rs per unit + Bonus of 20% Rs % of Rs. 1000 Rs = Rs. 1200 2500 units x Re Bonus of 20% Rs % of Rs. 1250 Rs.1500

Rs 1,000 (Guaranteed Monthly wages) 2000 units x Rs per unit + Bonus of 20% Rs % of Rs Rs = Rs units x Re Bonus of 20% Rs % of Rs Rs")

36

Bonus or Incentives Schemes

Incentive schemes of wage payment are also known as Premium Bonus Plans. introduced in order to increase production with ensuring proper industrial climate. Wage incentive plans may be of two types : Individual Incentive Plans and Group Incentive Plans. Under individual incentive plans, remuneration can be measured on the performance of the individual worker. In the case of the group incentive scheme earnings can be measured on the basis of the productivity of the group of workers or entire work force of the organization. Various types of incentive schemes are combinations of time and piece rate systems. The following are the important individual incentive plans discussed below:

37

Halsey Premium Plan This Plan was developed by F. A. Halsey. This system also termed as Split Bonus Plan or Fifty-Fifty Plan. Under this plan, standard time is fixed for each job or operation on the basis of past performance. If a worker completes his job within or more than the standard time then the worker is paid a guaranteed time wage. If a worker completes his job within or less than the standard time, then he gets a bonus of 50% of the time saved plus normal earnings. Under this method, the total earnings is calculated as follows:

38

Formula

39

Illustration: 4 Calculate the total earnings of the worker under Halsey Premium Plans: Standard Time 12 hours Hourly Rate Rs. 3 Time Taken 8 hours

40

Merits & Demerits of Halsey Premium Plan

It is simple to understand. Total earnings of each worker can be easy to calculate. Both employer and employee get equal benefit of time saved. This system not only benefits efficient worker but also provides average worker to get guaranteed minimum wages. This system is based on time saved and it can reduce the labour cost. Demerits Lack of co-operation among the employees. Under this system establishment of standard is very difficult. Earnings are reduced at high level of efficiency.

41

The Halsey-Weir Scheme:

Under this system, the worker gets the bonus of 30% of the time saved instead of 50% of time saved under Halsey Plan. Except for this, Halsey Plan and Halsey-Weir Systems are similar in all other respects. Illustration: 5 From the following particulars calculate total earnings of a worker under Halsey-Weir Plan : Standard Time = 10 Hours Time Taken = 8 Hours Hourly Rate = Shs. 2 per hour

42

Rowan Plan: This plan was introduced by James Rowan of England. It was similar to the Halsey Plan in many respects except that it differs in calculation of bonus. Under this system, bonus is determined as the proportion of the time taken which the time saved bears to the standard time allowed. Under this system the following formula is applied to calculation of bonus:

43

Formula

44

Illustration 6 From the following information, calculate total earnings of a worker under Rowan System : Standard Time = 10 hours Time Taken = 8 hours Rate per hour = Rs.3

45

Exercise The finishing shop of a company employs 60 direct workers. Each worker is paid Rs. 400 as wages per week of 40 hours. When necessary, overtime is worked upto a maximum of 15 hours per week per worker at time rate plus one-half as premium. The current output on an average is 6 units per man hour which may be regarded a standard output. If bonus scheme is introduced, it is expected that the output will increase to 8 units per man hour. The workers will, if necessary, continue to work overtime up to the specified limit although no premium on incentives will be paid. The company is considering introduction of either Halsey Scheme or Rowan Scheme of wage incentive system. The budgeted weekly output is units. The selling price is Rs. 11 per unit and the direct material cost is Rs. 8 per unit. The variable overheads amount to Rs per direct labour hour and the fixed overhead is Rs per week. Prepare a statement to show the effect on the company's weekly profit of the proposal to introduce (a) Halsey Scheme, and (b) Rowan Scheme.

Halsey Scheme, and (b) Rowan Scheme.")

46

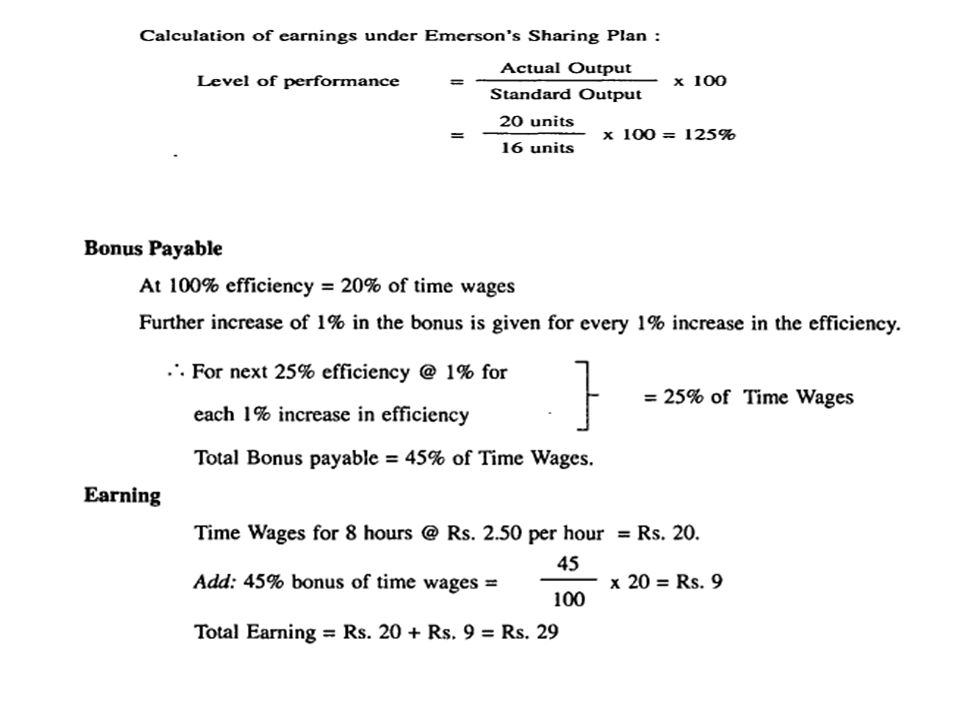

Emerson's Efficiency Sharing Plan

Under this plan, earning of a worker is by combining guaranteed day wages with a differential piece rate. Accordingly the level of efficiency is determined on the basis of establishment of standard task for a unit of time. If the level of worker's efficiency reaches 67% the bonus is paid to him at a normal rate. The rate of bonus increases in a given rate as the output increases from 67% to 100% efficiency. Above 100% efficiency, the bonus increases to 20% of the wage earned plus additional bonus of 1 % is added for each increase of 1 % in efficiency.

47

Illustration 7 From the following particulars calculate total earnings of a worker under Emerson's Efficiency Sharing Plan : Standard output per day of 8 hours is 16 units Actual output of a worker for 8 hours is 20 units Rate per hour is Rs. 2.50 Solution ??

49

Barth Variable Sharing Plan

This scheme introduced to attract newly recruited and skilled employees who are motivated to learn work. It provides sufficient incentives to inefficient workers who are motivated to increase productivity. Earning under this method is calculated by applying the following formula:

50

Bedaux Point Premium System:

This plan was introduced by Charles E.Bedaux in Under this plan, standard time fixed for each operation or job is expressed in terms of Bedaux point or'S.' For example, a standard time of 360 B means the operation or job should be completed within 360 minutes. The main advantage of this plan is that it can be applied to any kind of a job. Under this system, a worker is paid at the time for actual hours worked, and 75% of the wages for the time saved are paid as bonus to the worker and 25% to the foremen, supervisors etc. The following is the formula for calculation of total wages of a worker: Total earnings = S x R + 75% of R (S - T)

")

51

Illustration: 8 From the following particulars, calculate total earnings of a worker under Bedaux Point Premium System: Standard Time = 360 B Time Taken = 240 B Rate per hour = Re. 1

52

Solution:

53

Accelerating Premium Bonus Plan:

Under this plan, bonus is determined on the basis of time saved unlike a fixed percentage under Halsey Plan and as a decreasing percentage under Rowan Plan. The bonus is paid to workers at an increased rate according to more and more time saved. This provides increasing incentives to efficient workers.

54

Group or Collective Bonus Plan

The incentive schemes explained so far are applicable to individual performance depending directly on production. However. it is not the individual worker who produce the goods or services (operation) alone but group of several other workers are required to jointly perform a single operation. It is, therefore, essential that a group incentive scheme be introduced. Bonus is calculated for a group incentive scheme. The bonus is calculated for a group of workers and the total amount is distributed among the group of workers on anyone of the following basis : Equally by all the workers of the group. Pro rata on the time rate basis. Pre determined percentage basis. Specified proportion basis.

alone but group of several other workers are required to jointly perform a single operation. It is, therefore, essential that a group incentive scheme be introduced. Bonus is calculated for a group incentive scheme. The bonus is calculated for a group of workers and the total amount is distributed among the group of workers on anyone of the following basis : Equally by all the workers of the group. Pro rata on the time rate basis. Pre determined percentage basis. Specified proportion basis.")

55

Types of Group Incentive Plans

Budgeted Expenses Bonus Plan: Under this method, bonus is determined on the basis of savings in actual expenditure compared with total budgeted expenditure. Priest Man Bonus Plan: Under this plan, standard performance is fixed by the management and committee of workers. The group of workers get bonus when actual performance exceeds the standard performance irrespective of individual's efficiency or inefficiency.

56

Towne's Gain-sharing Plan: Under this plan, bonus is calculated on the basis of savings in labour cost. The group of workers get bonus when actual costs is less than the standard costs, one-half of the savings is distributed among workers including foremen in proportion with the wages earned. Scanlon Plan: Scanlon Plan is designed with the chief aim of reducing the cost of operations in order to increase the production efficiency. This plan is generally applicable in industries where the operation cost is high. Under this scheme, bonus is determined on the basis of standard costs or wastages and percentage of the reduction in operation cost.

57

Indirect Monetary Incentives

Incentive schemes are regarded beneficial to both employers and workers. In this regard, under indirect monetary incentives by giving them a share of profit and introducing co-partnership schemes or as they have become partners in the business in order to make a very profitable enterprise.

58

Non-Monetary Incentive Schemes:

Under this system, employees are provided better facilities, instead of additional monetary payments. Some of the examples of non-monetary incentives are free education for children, rent free accommodation, medical facilities, canteen facilities, welfare facilities, and entertainment facilities etc.

59

MEASUREMENT OF LABOUR EFFICIENCY AND PRODUCTIVITY

In order to introduce a good remuneration system, it is necessary to know the contents of the job or operation that an employee is expected to perform. A detailed analysis of each job and operation will reveal its characteristics and scope for improvement, and lead to establish methods for measurement of efforts involved and productivity to be achieved. In big organisations, industrial engineer or time study engineer undertakes various work studies, while personnel department prepares job evaluation and merit rating for this purpose.

60

Work Study Work study consists of method time and motion study in relation to the performance of a job or operation. Time study involves the technique of establishing an allowed time standard to perform a given task, based upon measurement of the work content of the prescribed method, with due allowance for fatigue and for personal and avoidable delay

61

Time study is concerned with the determination of standard time required by a worker of average ability, under normal condition to perform a task. Motion study technique, developed by F.B.Gilbraith, is defined by Benjamin W. Niebel as “the study of the body motion used in performing an operation, with the thought of improving the operation by eliminating unnecessary motion and simplifying necessary motions and then establishing the most favourable motion sequence for maximum efficiency”. Time and motion study is incomplete without method study, which is concerned with determining the proper method of performing a job. All the three i.e. time, motion and method study are parts of the total work study which helps management in effective use of human efforts.

62

The steps in time and motion study are the following:

Identify the work. Observe the workers performing the job. Record all the relevant parts of performing job by present method. Note down wasteful movements and restructure proposed method giving due allowance for fatigue, interference, etc. Critically examine the proposed method, and develop the most practical, acceptable and effective method. Install that method as standard practice.

63

The time and motion study serves the following purposes:

Standardising jobs, operations, etc. by providing the best method of operating within the time allowed. Standardisation of equipments, methods, materials and working conditions. Fixation of wage-rates including piece rates and incentive schemes. Assessing manpower requirements correctly. Cost control through proper planning.

64

Job Evaluation Job evaluation is a process of analysis and assessment of each job determining its worth in relation to all other jobs within an organisation in order to provide a basis for wages and salary structure. It helps determination of correct grade of labour for each job or operation, and establishes the rationale for differentials in wages and salaries between different groups of employees. The objectives of job evaluation is to evolve a systematic job, wages and salary structure according to characteristic features of each job.

65

Reading Assignment Methods of job evaluation can be classified into four groups as given below: Ranking method Grading method Point rating method Factor comparison method.

66

IDLE TIME AND OVERTIME Idle time refers to that portion of hours paid which are not utilised for productive purposes. This is reflected in the time card as the hours not booked in job or work order, and during which time the worker remains idle. Idle time can be classified under normal and abnormal idle time. Normal idle time represents inevitable loss of labour hours arising out of the following situations: Time lost between factory gate and place of work, tea break, lunch break, etc. Time lost in setting the machine, tools, change-over from one job to another, fatigue, etc. Time lost in power-failure, machine breakdown, waiting for material, etc.

67

Idle time Out of the above causes, some are inherent in the process and controllable to a great extent. While time lost due to external causes such as general power-failure are uncontrollable in the hands of the management. Thus, it is possible to identify normal idle time, and any loss of time beyond the normal allowed hours shall be called abnormal idle time, such as: Excessive machine-breakdown. Excessive internal power failure. Excessive waiting time for material, instructions, etc. Too much time to rectify defectives. Strike, lockout, fire, floods, etc.

68

Idle time can be controlled by adopting the following measures :–

Preparation and analysis of labour utilisation report with breakdown of idle time. Minimising machine breakdown by adopting preventive maintenance. Proper material and production planning, and follow-up system. Timely purchase of materials and components.

69

Accounting of Idle Time

Normal idle time of all workers should be collected under standing order number and charged to factory overheads. However, some of the normal idle time of direct workers, which are associated with the job or work order, such as, time taken for machine setting, change-over or tool setting, can be added to the product cost as direct wages by inflating the hourly rate of wages. Abnormal idle time cost shall be collected as per standing order numbers or accounts code numbers and shall be charged to costing profit and loss account. Under no circumstances, abnormal idle time can be charged to product-cost.

70

Overtime The control of overtime is very important, because of its tendency to increase and to become a normal practice for earning extra money. It has harmful effect on the health and morale of the workers, besides unfavourable effect on productivity. It may also lead to high absenteeism. The overtime hours should, therefore, be controlled rigorously. Except for unavoidable reasons, overtime work should not be allowed. Sanctioned overtime work should be supervised properly to ensure full utilisation of time. Daily or weekly overtime report should be reviewed by higher management. Overtime is normally paid at a rate higher than normal wages. Usually, it is one and half or double the normal wage-rate. The extra amount over the normal wage-rate is called overtime premium. Normal wages form part of direct labour cost. The charging of overtime premium needs consideration of the circumstances under which overtime was undertaken, and accordingly, the standing order number will be debited.

71

Accounting of Overtime Premium

If overtime is paid to complete a job at the request of the customer, overtime premium is charged to the job order concerned. If overtime is undertaken in order to cope up with increased production, overtime premium is treated as factory overheads. Alternative method is to distribute the overhead premium over all the jobs undertaken during normal as well as overtime hours at an average rate If overtime is paid for any capital order, such as, fabrication of a machine to be used internally, the overtime premium shall be charged to capital work order account. If overtime is worked to recover production loss due to abnormal conditions such as, strike, lock out, flood, etc., the premium should be charged to costing profit and loss account.

72

Overtime work should be controlled in the following ways —

No overtime work shall be allowed without prior authorisation. If overtime is unavoidable, then it should be planned in advance, and actual overtime hours should be compared against plan. Overtime hours with normal working hours should be reported daily. A monthly overtime report showing overtime hours, and cost compared to the previous month as well as plan should be submitted to higher authority. Cost of overtime work vis-a-vis recruitment of additional worker should be reviewed periodically

Similar presentations

Companies Partnership Companies Joint Stock Companies Co-operative Societies/Organizations Public.>")