Download presentation

Presentation is loading. Please wait.

1

Briefing on Local Support for Council Tax David Magor OBE IRRV (Hons) Chief Executive Institute of Revenues, Rating and Valuation

Chief Executive Institute of Revenues, Rating and Valuation")

2

Introduction

3

Council tax rebate reforms risk repeat of poll tax disaster, says IFS

4

Context DEFICIT REDUCTION Government’s top priority. Taxpayers were paying almost £120 million a day (£43 billion a year) in debt interest - more than council tax, stamp duty and inheritance tax combined last year WELFARE REFORM Reforming the welfare system - to make it fairer, more affordable and better able to tackle poverty, worklessness and welfare dependency LOCALISATION Coalition principles of increasing freedom and sharing responsibility by localising power and funding. De-ringfencing of funding, abolition of top-down targets and inspection regime

in debt interest - more than council tax, stamp duty and inheritance tax combined last year WELFARE REFORM Reforming the welfare system - to make it fairer, more affordable and better able to tackle poverty, worklessness and welfare dependency LOCALISATION Coalition principles of increasing freedom and sharing responsibility by localising power and funding. De-ringfencing of funding, abolition of top-down targets and inspection regime.")

5

Background Spending Review 2010 Localise support for council tax and reduce the subsidy by 10% from 2013 -14 Abolition of council tax benefit provision in the Welfare Reform Act Part of wider policy giving councils increased financial autonomy Enabling power for the new scheme to be contained in a finance bill now before the current parliamentary session

6

Why localise support for council tax the CLG view Give local authorities (LAs) a greater stake in the economic future of their area Give LAs the opportunity to reform the system of support for working age claimants Reinforce local control over council tax Give LAs a degree of control on the impact of the 10% reduction Give LAs a financial stake in the local support for council tax (LSCT)

a greater stake in the economic future of their area Give LAs the opportunity to reform the system of support for working age claimants Reinforce local control over council tax Give LAs a degree of control on the impact of the 10% reduction Give LAs a financial stake in the local support for council tax (LSCT)")

7

Overview Broad parameters of LSCT Reduce subsidy by 10% Existing subsidy to be replaced by a new grant Create a local scheme Statutory provision of a default scheme Protection for eligible pensioners and locally determined vulnerable people Scheme should support incentives to work LAs encouraged to collaborate to reduce costs LAs to consider how system can be simplified for working age claimants LAs will seek to integrate arrangements for providing support within council tax system Local mechanisms to manage financial pressures

8

Localism and Council Tax Support

9

Council Tax and Localism The Localism Act 2011 More scrutiny on levy Just how far does the proposed power of competence go? Referendum on levels of council tax above stated thresholds Neighbourhoods, Community Councils and Parishes – a new power base? How does all this impact on local support for council tax?

10

A Recent Report

11

Paragraph 32

12

The LSCT Documents

13

The Initial Consultation

14

Consultation Response

15

Local Government Finance Bill

16

Impact Assessment

17

Statement of Intent

18

Equality Impact Assessment

19

Funding Arrangements

20

Vulnerable People

21

Taking Work Incentives into Account

22

Governance of LSCT

23

The Reference Group Challenge Risks and opportunities Identify interactions Consideration of specific policy issues through the use of networks Act as a sounding board Membership

24

The Delivery Group Timetable Model Schemes Data sharing LA Software Forecasting Finance Issues Membership

25

Establishing a Local Scheme

26

Establishing a local scheme (1) Analysis of existing caseload Impact analysis Developing a scheme Factors to be covered by schemes Consultation Adoption of the scheme Revisions to schemes Default schemes

Analysis of existing caseload Impact analysis Developing a scheme Factors to be covered by schemes Consultation Adoption of the scheme Revisions to schemes Default schemes")

27

Establishing a local scheme (2) Likely to be a minimum of central criteria. Information from the Universal Credit (UC) system to be available to local authorities for use in the administration LSCT The rules relative to changes of circumstance should be identical for both schemes any change in entitlement to UC should automatically trigger a recalculation of LSCT

system to be available to local authorities for use in the administration LSCT The rules relative to changes of circumstance should be identical for both schemes any change in entitlement to UC should automatically trigger a recalculation of LSCT.")

28

Developing the Local Scheme

29

The Link with Universal Credit Universal Credit will provide a new single system of means-tested support for working-age people who are in-work or out-of-work. Support for housing costs, children and childcare costs will be integrated in the new benefit. It will also provide additions for disabled people and carers Under Universal Credit, couples living in the same household will make a joint claim for the benefit payment. Ordinarily the benefit will be given in a single monthly payment to a household. It will be for the family to decide who receives the benefit No entitlement if capital of claimant or couple exceeds £16,000 Transitional protection which will ensure that there are no cash losers at the point of change as a direct result of the migration to Universal Credit, where circumstances remain the same

30

Personal Independence Payment Universal Credit The Changes Child Benefit, Carer’s Allowance (will remain) Income related JSA Income related ESA Income Support (including SMI) Working Tax Credits Child Tax Credits Housing Benefit Disability Living allowance Current system New system Contributory JSA and ESA (DWP still considering how these will work) Council Tax and Rate Support ( schemes being considered) … will include support for housing and children Pension credit

Income related JSA Income related ESA Income Support (including SMI) Working Tax Credits Child Tax Credits Housing Benefit Disability Living allowance Current system New system Contributory JSA and ESA (DWP still considering how these will work) Council Tax and Rate Support ( schemes being considered) … will include support for housing and children Pension credit")

31

The Universal Credit Award The standard allowance The child responsibility element The housing cost element The limited capability for work element The limited capability for work element and the work related activity element The carer element Childcare costs element

32

Treatment of Income Calculation of monthly income Earned income Unearned income Income disregards Deprivation of income and income foregone Income treated as yield from capital Personal injury Compensation

33

Treatment of Capital The capital limit, this appears to be £16,000 with similar derived income rules The calculation of capital Jointly held capital Valuation of capital Deprivation of capital Capital treated as income Capital of a company Disregarded capital

34

Treatment of Housing Costs When an award is to include a housing cost element The payment condition (Category A,B,C, or D payments) The occupation condition The liability condition The calculation of the amount Restrictions on the amount of the housing costs element

The occupation condition The liability condition The calculation of the amount Restrictions on the amount of the housing costs element")

35

Universal Credit - Key stages in the UC calculation process Localised Council Tax Support and Universal Credit calculation data

36

OBJECTIVES Show the stages of the Universal Credit calculation Highlight which figures may be available for transmission to Local Authorities for the purposes of LCTS assessment Explain which elements are still subject to design and/or Policy activity

37

CONTEXT DWP currently transmits data to LAs for Housing and Council Tax Benefit LAs require Universal Credit data to be transferred for LCTS purposes The UC calculation process is markedly different from existing legacy benefits We are working with DCLG, Devolved Administrations and LAs to clarify requirements for LCTS This presentation is intended to facilitate further discussion

38

SUMMARY – THE KEY STAGES IN THE UC ASSESSMENT PROCESS STAGE 3 – CALCULATE UC ENTITLEMENT (APPLY ANY SANCTIONS, ADD ANY HARDSHIP PAYMENTS) STAGE 2 – CALCULATE THE ADJUSTED UC AWARD (DEDUCT EARNINGS, CAPITAL, INCOME, BENEFIT CAP) then STAGE 0 – IDENTIFY WHO IS IN THE BENEFIT UNIT (ADULTS, DEPENDENT CHILDREN AND NON-DEPENDANTS) STAGE 1 – CALCULATE THE UC MAXIMUM AMOUNT (TOTAL ALLOWED FOR LIVING AND HOUSING COSTS) then STAGE 4 – CALCULATE THE UC PAYMENT (ADD ANY ADVANCES, APPLY ANY DEDUCTIONS) then

STAGE 2 – CALCULATE THE ADJUSTED UC AWARD (DEDUCT EARNINGS, CAPITAL, INCOME, BENEFIT CAP) then STAGE 0 – IDENTIFY WHO IS IN THE BENEFIT UNIT (ADULTS, DEPENDENT CHILDREN AND NON-DEPENDANTS) STAGE 1 – CALCULATE THE UC MAXIMUM AMOUNT (TOTAL ALLOWED FOR LIVING AND HOUSING COSTS) then STAGE 4 – CALCULATE THE UC PAYMENT (ADD ANY ADVANCES, APPLY ANY DEDUCTIONS) then")

39

STAGE 0 – IDENTIFY THE BENEFIT UNIT One or two ‘eligible (and connected ) adult claimants, and relevant child dependents = The UC Benefit Unit Identify ( for Housing Element purposes only ) any non-dependants

adult claimants, and relevant child dependents = The UC Benefit Unit Identify ( for Housing Element purposes only ) any non-dependants")

40

STAGE 1 – CALCULATE THE BENEFIT UNIT’S ‘MAXIMUM AMOUNT’ BY ADDING UP RELEVANT AMOUNTS COVERING…… Childcare Element Carer Element Housing Element LCW Limited capability for Work Related Activity, or Work Element Carer Child Element/Disabled Child Additions Standard Allowance Adults Children Housing Childcare Tick indicates available for LCTS

41

STAGE 2 (a) – CALCULATE THE UC ‘ADJUSTED AWARD’ Any earnings (subject to any disregards and taper) Other applicable income minus UC MAXIMUM AMOUNT Tariff income from applicable capital minus And then...... Tick indicates available for LCTS

42

STAGE 2 (b) – ‘CALCULATE THE UC ‘ADJUSTED AWARD’ BY APPLYING FURTHER CRITERIA Any increases necessary (where Cap does/will not apply) to take account of Transitional Protection minus ADJUSTED AWARD stage 2(a) Any reductions necessary to take account of the Benefit Cap plus UC ADJUSTED AWARD equals Tick indicates available for LCTS

– ‘CALCULATE THE UC ‘ADJUSTED AWARD’ BY APPLYING FURTHER CRITERIA Any increases necessary (where Cap does/will not apply) to take account of Transitional Protection minus ADJUSTED AWARD stage 2(a) Any reductions necessary to take account of the Benefit Cap plus UC ADJUSTED AWARD equals Tick indicates available for LCTS")

43

STAGE 3 –CALCULATE THE ‘UC ENTITLEMENT’ minus UC ADJUSTED AWARD Any conditionality sanctions (plus any hardship payment amounts) equals UC ENTITLEMENT Tick indicates available for LCTS

equals UC ENTITLEMENT Tick indicates available for LCTS")

44

STAGE 4 – ESTABLISH ANY DEDUCTIONS TO BE MADE TO UC ENTITLEMENT TO WORK OUT THE ‘UC PAYMENT’ Any short-term or budgeting advance UC ENTITLEMENT plus The UC Payment equals and Any agreed deductions e.g. child support, third party rent payments) minus Tick indicates available for LCTS

minus Tick indicates available for LCTS.")

45

What will not be available The actual amount included in the net payment for housing costs (although the amount included in the “maximum award” is available) Net earnings for each member of the Benefit Unit – a total for the household can be provided

Net earnings for each member of the Benefit Unit – a total for the household can be provided")

46

Elements not yet finalised Treatment of non-dependants How any potential payments to third parties could be shown

47

Using existing Parameters Building on existing approaches The existing structure Personal allowances Premiums Non-dependant deductions Resources Disregards Second adult rebate Taper Excess benefit Forecasting Formulating the scheme

48

Constraints System Funding Limitation and referendums Protecting vulnerable groups Setting aside a sum for extraordinary events Political dimension Timetable Adverse consultation Collection issues

49

Administering Local Schemes Initial transition The application Calculation and award Notification Excess LSCT Appeals To the local authority To another body Arrangements for individuals subject to immigration control or are not habitually resident in the UK

50

An Approach to Modelling

51

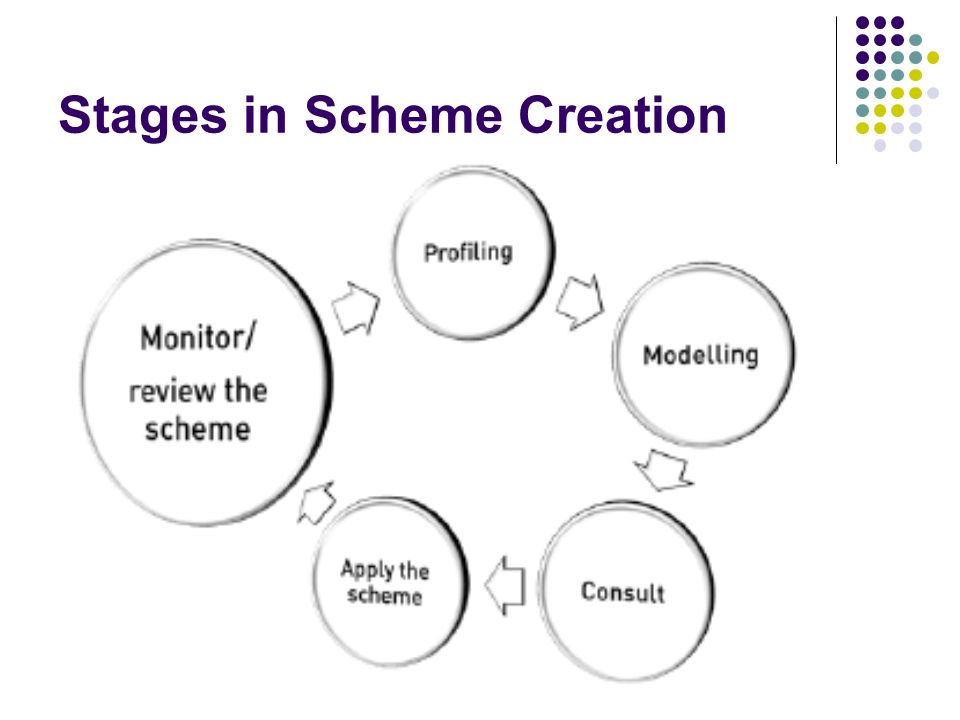

Stages in Scheme Creation

53

Profiling

54

Available Data Sets SHBE Benefits system data Council tax system Electoral register Other internal data sets

55

Profiling requirements Understanding current demographics Identify older people Identify vulnerable groups Identify claimant groups Identify the financials Identify potential saving areas

56

Stages in Scheme Creation

57

Model Structure

58

Approaches to modelling Cap Minimum and maximum benefit Claimant type and/or status Percentage Needs and/or resources Family Flat rate Council Tax band

59

Forecasting One to five year forecasts “ What if ” reporting Impact Population movement Forecasting across several data sources

60

Stages in Scheme Creation

62

Monitor and review Budgetary control Shortfall or surplus Scheme impact Need for additional data sets Standard, comparative and regular reporting Preparing for year two !

63

Vulnerable People

64

Key Local Authority Duties The public sector Equality Duty Equality Act 2010 Duty to mitigate the effects of child poverty Child Poverty Act 2010 Duty to people with disabilities Disabled persons (Services, Consultation and Representation) Act 1986 The Armed Forces covenant Duty to prevent homelessness Housing Act 1996

Act 1986 The Armed Forces covenant Duty to prevent homelessness Housing Act 1996")

65

The Public Sector Equality Duty The duty Relevant protected characteristics Requirements of the Equality Duty Welfare needs of disabled people Equality information and engagement

66

Duty to mitigate the effects of child poverty Co-operate Understand needs Develop and deliver a strategy Equality information and engagement

67

The Armed Forces Covenant Redress disadvantages Recognise sacrifices The obligation of the Whole nation State Treatment of War Pensions and the Armed Forces Compensation Scheme

68

Duty to Prevent Homelessness Families with children No blame People at risk Vulnerable The Equality Duty

69

Equality Impact Assessment Fit for purpose Data and circumstance driven Cannot be subordinated, “going through the motions” Published as part of the consultation process Adverse outcome? Potential for Judicial Review

70

Work Incentives

71

What are the key aims? 1) Reduce worklessness, reward work and personal responsibility as a result of the single withdrawal rate under Universal Credit, 1.2 million households will see a reduction in their marginal deduction rate (MDR) virtually no household will have a MDR above 80 percent, compared to 500,000 households with a MDR above 80 per cent in the current system a single taper rate and a simple system of earnings disregards so people in work to see clearly how much support they can get while making sure that people considering a job will understand the advantages of work clear conditionality rules that strike a balance between dependency and support What is a MDR? MDR measures the incentive for someone to increase their hours of work as the earnings of a household increase, means-tested benefits and tax credits start to be withdrawn in addition, above a certain level of earnings, the increase in their wages will also be partially offset by income tax and national insurance contributions MDR is calculated as the proportion of a small increase in earnings which is lost in lower Benefits/Tax credits and/or higher income tax and national insurance payments

Reduce worklessness, reward work and personal responsibility as a result of the single withdrawal rate under Universal Credit, 1.2 million households will see a reduction in their marginal deduction rate (MDR) virtually no household will have a MDR above 80 percent, compared to 500,000 households with a MDR above 80 per cent in the current system a single taper rate and a simple system of earnings disregards so people in work to see clearly how much support they can get while making sure that people considering a job will understand the advantages of work clear conditionality rules that strike a balance between dependency and support What is a MDR. MDR measures the incentive for someone to increase their hours of work as the earnings of a household increase, means-tested benefits and tax credits start to be withdrawn in addition, above a certain level of earnings, the increase in their wages will also be partially offset by income tax and national insurance contributions MDR is calculated as the proportion of a small increase in earnings which is lost in lower Benefits/Tax credits and/or higher income tax and national insurance payments.")

72

Options on work incentives Run on Disregards Non-dependant deductions Progressive manipulation Progressive taper Cash award Non cash facilities These all have a cost

73

Treatment of income (other than earnings) UCPB9 Key policy proposals As the White Paper ‘Universal Credit: Welfare that works’ set out, Universal Credit claimants who enter work will not see any reduction in their Universal Credit award so long as their earnings are below the appropriate earnings disregard. A small group of income types will be treated identically to earnings. These are Statutory Sick Pay and Statutory Maternity/Paternity/Adoption Pay.

74

Treatment of income (other than earnings) UCPB9 Income received due to additional costs or expenses the claimant has will be fully disregarded. There is also a group of income types which it would be inappropriate to take into account due to the disproportionate administrative burden of doing so. Obvious examples would be the value of payments in kind or charitable payments. Such income will be fully disregarded. The current approach of fully disregarding payments of child maintenance received by a claimant who is a parent with care, in order to encourage such parents to apply for child maintenance, will continue under Universal Credit.

75

Earnings disregards and tapers UCPB14 Minimum levels of disregards The recently published Impact Assessment for Universal Credit assumes the following proposed minimum annual levels for the earnings disregards: for a single person without children: £700 for a couple: £1920 plus £520 for the first child and £260 for the second and third children; for a lone parent: £2,260 plus £520 for the first child and £260 for the second and third children; and for single disabled people or a couple where at least one person is disabled: £2,080. Only one earnings disregard, whichever is highest, will be available in each household. The exact amount of these minimum earnings disregards has not yet been set and will be set closer to implementation of Universal Credit.

76

Earnings disregards and tapers UCPB14 Maximum levels of disregard With the minimum floor levels, the exact amount of these higher disregards has not been set yet. The latest Universal Credit Impact Assessment assumed disregards in the order of: for a single person without children: £700 couple: £3,000 plus £4,250 per household for a child (regardless of the number of children); lone parent: £9,000 (regardless of the number of children); and disabled people: £7,000 per household if a recipient or either partner in a couple is disabled. Only one earnings disregard - whichever is highest - will be available in each household.

; lone parent: £9,000 (regardless of the number of children); and disabled people: £7,000 per household if a recipient or either partner in a couple is disabled. Only one earnings disregard - whichever is highest - will be available in each household..")

77

Earnings disregards and tapers UCPB14 How will the reduction for housing support work? There will be maximum and minimum disregards within Universal Credit. The maximum earnings disregard will only apply where there are no additions for housing costs included in the Universal Credit gross award. If the claimant is receiving some support for housing costs, the value of this support reduces the maximum level of their earnings disregard by, on current assumptions, 1½ times the amount of the housing element. A household receiving some support for housing costs will be entitled to an earnings disregard equal to the value of the larger of their reduced earnings disregard and the minimum disregard.

78

Earnings disregards and tapers UCPB14 Earnings Taper A taper is the rate at which benefit is reduced to take account of earnings. A simplified single taper is at the heart of the design of Universal Credit. Currently there are different taper rates operating throughout the benefit and Tax Credit system. The interaction between these tapers can mean that people have very little incentive to work more hours or to aspire towards a pay rise as they see only a few pence more in their pockets as a result. Final decisions on the actual taper rate in Universal Credit will be taken closer to its introduction in 2013. However, the White Paper suggested that the taper or withdrawal rate would be around 65 per cent. In simple terms, that would mean that 35 pence in every pound earned would be kept.

79

The Default Scheme

80

The Features of the Default Scheme Will follow the existing CTB scheme NOT a substitute for a local scheme Will not make the provision for the 10% cut If you fail to make your scheme by the 31 st January you will have to apply it You cannot deviate from it Would result in serious financial difficulties for both the Billing Authority and Major Precepting Authorities

81

How Would You Manage It? Could be seen as the benefit practitioners dream! Existing procedures could continue You would need to meet the overall legislative objectives Subject to the up rating? Tax base problems? Tax levels could trigger difficult outcomes Collection Fund issues

82

Local Schemes

83

Brent LBC

84

Chiltern DC

85

Harrow LBC

86

Consultation

87

The First Four Stages The first consultation should be with the major precepting authorities to gauge the general reaction to local funding of all or part of the reduction in grant. These should be County wide meetings involving all the billing authorities and be at both officer and member level, all meetings need to be properly convened with appropriate minutes. The second consultation should be with all billing authorities in the County to gauge the support or otherwise for a common scheme and resource pooling. The third consultation should take the form of a briefing with all Third Sector bodies particularly those who represent client groups likely to be affected by the reductions in benefit. The fourth consultation should be with the local precepting authorities warning them of the implications of the scheme for their tax base and the potential for triggering a referendum under the Localism Act. At this stage the billing authorities should finalise the proposed scheme and carry out a detailed impact analysis. The authority should also be able to show it has properly considered incentives to return to work. The scheme should also be costed.

88

The Final Five Stages The fifth consultation should be with the major precepting authorities for the third time to gauge the general reaction to proposed local scheme and the financial implications. The sixth consultation should be with all billing authorities in the County to give them a further opportunity to share schemes. The seventh consultation should take the form of a second briefing with all Third Sector bodies particularly those who represent client groups are to be affected by the reductions in benefit. The eighth stage in the consultation should be seeking the direct views of your claimants both working age and pension aged. The final consultation should be with the local precepting authorities after giving them the likely local financial impact and the potential need for local referendums.

89

Data Sharing

90

Data sharing to process claims within local schemes Provision in the Welfare Reform Act Will be subject to a protocol between CLG and DWP Establishing data sharing Link with UC

91

Fraud and Error

92

Fraud What structure? SFIS? Enabling power in Bill Specific powers or general powers? Developing local services High level business case for SFIS Risk based verification

93

Practical Issues Staffing and structure Relationship with SFIS Exercise of new powers Legal process Information sharing Cost Wider fraud issues NRPF Other areas of activity

94

Delivery

95

Aspects of Delivery (1) The legally authenticated version of the local scheme Fit for purpose Resilient to challenge Avoid practitioners short cuts Publicity Literature Application process

The legally authenticated version of the local scheme Fit for purpose Resilient to challenge Avoid practitioners short cuts Publicity Literature Application process")

96

Aspects of Delivery (2) Notification Excess local scheme awards Accounting A liability determination First level appeals Learning curve for the Billing Authority role in the Valuation Tribunal This is not a minor issue!

Notification Excess local scheme awards Accounting A liability determination First level appeals Learning curve for the Billing Authority role in the Valuation Tribunal This is not a minor issue!")

97

The Appeal Process

98

The Process Notification Extent of detail Detailed statements Appeal to the local authority Decision Appeal to another place The Valuation Tribunal Service Enabling power already in place

99

Appealing to the VTS Read the Annual Review ! Process Need for regulation? Practice Statements Procedure Statements Sufficient expertise? Customer friendly? Is there a capacity issue?

100

The Hearing Amendment in the Bill Provision for cases to be heard before a Judge Evidence of scheme to be formally given? These are liability appeals Will there be a crossover with UC appeals? The big question “what is the potential volume”

101

Funding

102

The Overall Funding Mechanism The government’s consultation on localising support for council tax introduced the proposal to transfer the funding of council tax support from demand-led AME (Annually Managed Expenditure) to DEL (Departmental Expenditure Limits) The Government is proposing to pay grant to billing and major precepting authorities to bring down council tax requirement rather than allocate it to the Collection Fund This will mean the tax base will have to take account of the local scheme in a similar manner to discounts This issue could create problems for Local Precepting Authorities (parish councils and town councils) because if the tax base is reduced and they do not receive grant then parish band D council tax will go up This could be a particular issue if referendums are extended to some parish councils.

to DEL (Departmental Expenditure Limits) The Government is proposing to pay grant to billing and major precepting authorities to bring down council tax requirement rather than allocate it to the Collection Fund This will mean the tax base will have to take account of the local scheme in a similar manner to discounts This issue could create problems for Local Precepting Authorities (parish councils and town councils) because if the tax base is reduced and they do not receive grant then parish band D council tax will go up This could be a particular issue if referendums are extended to some parish councils.")

103

Calculating the Council Tax under the new rules

104

Benefit cost funding The authorities that will receive grant Billing Authorities Major Precepting Authorities The position on parishes Powers to pay grant Funded through the Central Share of non domestic rates Methodology for distributing grant Frequency of grant allocation Grant allocation in future Spending Review periods Limits on spending Maximising the tax base Managing pressures through the collection fund

105

Administration Costs Administrative cost Implementation costs (£80k to billing authorities and £27 to major precepting authorities already paid) On going costs Link to existing subsidy arrangements New Burdens Assessment

On going costs Link to existing subsidy arrangements New Burdens Assessment")

106

Business Rates Retention Local Share and Central Share Was going to be 70/30 or even 80/20 The decision 50% Local Share and 50 % Central Share Why the change? Could it be because the LSCT Grant is one of the nominated matters to be funded from the Central Share Doesn’t apply to Scotland, N Ireland and Wales What about growth in England? So where is the £3.82bn?

107

Grant allocation The DCLG has invited a separate technical consultation on the specific factors and indicators which should determine the level of grant allocated to a particular authority. Issues to be considered in the consultation includes: The basis for allocation (what factors are taken into account in distributing grant) The frequency of allocation (how frequently grant is adjusted – annually or less annually).

The frequency of allocation (how frequently grant is adjusted – annually or less annually)..")

108

Grant allocation The relevant factors for the basis of allocation could include: The relative size of eligible claimant groups Previous expenditure Other indicators – unemployment levels etc Council tax costs

109

Grant allocation The issues that will need to be considered are: What are the advantages – and disadvantages of using previous expenditure to determine shares of funding? Is there a case for using previous expenditure initially? What other factors could be taken into account as well or instead? How should Government balance the need to reflect costs with the importance of incentivising local authorities to manage down demand/ensure there is accountability over council tax levels?

110

Grant allocation Consideration will need to be given to the frequency of allocation. There are two broad options: Reflecting as closely as possible levels of take-up or demand, by adjusting as frequently as is practicable. This would achieve a better match between needs and grant across all authorities and would tend to reduce the financial risks to authorities Leaving the grant allocation unchanged for several years. This would provide local authorities with greater certainty about their allocation in future years and help with financial planning; it would also enable a local authority to gain if liabilities under its scheme were to fall during that period.

111

Local precepting authorities Option one - pass no money on Disregard the parish share entirely in distributing the total grant between billing and precepting authorities Pass the parish share to billing authorities – but with no obligation to pass it on to parishes Implications Does not require additional legal powers Administratively simple for billing authorities – more complex for central government if parish share has to be identified Could lead to big leap in Band D for some parishes – may mean that some get caught by any referendums principles

112

Local precepting authorities Option two - pass money on Pay grant directly to parishes Implications Requires additional legal powers Highly administratively complex for central government Minimises impact on Band D Unclear how this could operate under retained business rates

113

Local precepting authorities Option three - pass money on Pay grant to billing authorities with a requirement to pass the grant on to parishes Paying grant to billing authority, with requirement to pass on through council tax system Implications Requires additional legal powers Degree of complexity for both central and local government – integrating within the council tax system could make less administratively onerous Minimise impact on parish Band D Unclear how this could operate under retained business rates

114

Legislative Process

115

Legislative progress The Local Government Finance Bill The need for subordinate legislation Draft regulations where needed Statements of intent Legislative timetable

116

Progress on the Bill The Bill has passed through 1 st and 2 nd Reading as well as the Committee stage in the House of Commons. The next stage is the House of Commons Report Stage followed by the Third Reading on the 28 th May, before Moved to the House of Lords on the 12 th June with the Committee stage started on the 26 th June Royal Assent in July?

117

Pension Age Regulations Commitment to protect pensioners Definition in relation to age Mixed age couples – DWP approach Treatment of war pensioners Uprating for pension aged claimants

118

Transitional Regulations A claim under CTB on or before 31 st March 2013 A claim under CTB on or after the 1 st April 2013 A change of circumstance declaration for CTB A change of circumstances for UC

119

Collection Fund Regulations Possible amendment to the Local Authorities (Funds) (England) Regulations 1992 Precepts The proposal to vary the payment schedule Views being sort from the two groups The potential for an alternative proposal The impact of the in-year financial pressure on Major Precepting Authorities

(England) Regulations 1992 Precepts The proposal to vary the payment schedule Views being sort from the two groups The potential for an alternative proposal The impact of the in-year financial pressure on Major Precepting Authorities")

120

Council Tax Base Regulations Amendment to existing regulations rather than new ones Calculation of the impact of LSCT on the council tax base The council tax base for baseline purposes likely to remain gross of LSCT Timeline

121

Timetable

122

The Timetable Spring 2012 Primary legislation in passage through Parliament. Government preparing and consulting on draft secondary legislation. Initial thoughts on local scheme Discussions between billing authorities and major preceptors Political direction Technical consultation on grant distribution

123

The Timetable Summer 2012 Primary legislation passed. Secondary legislation prepared Develop operational project plan Billing authorities designing local schemes Scoping IT changes Consultation with Major Precepting Authorities Modelling proposed scheme Public consultation

124

The Timetable Autumn / Winter 2012 Secondary legislation passed (early Autumn) Prepare risk assessment Grant allocations published Establishing local schemes – final consultation with major precepting authorities and public, revisions to schemes. Technical changes to systems begin Setting budgets. Adopt local scheme

125

The Timetable Winter/Spring 2012/13 Finalise system changes Prepare tax base Set council tax and formally adopt scheme Publicise scheme Agree monitoring arrangements Billing

126

Policy into Practice

127

Operating the scheme in a small shire district Under the new scheme the amount provided to support Council Tax benefit will be reduced by 10% amounting to £695K Annual Council Tax benefits £6,954 Less: 10% reduction as proposed£ 695 Less: Protection for pension age groups (50%)£3,477 Balance to be used for working age£2,782 This means that the assistance with Council tax for working age claimants will be reduced by around 18% which means that in future working age claimants will be entitled to around 80% of the their current entitlement.

£3,477 Balance to be used for working age£2,782 This means that the assistance with Council tax for working age claimants will be reduced by around 18% which means that in future working age claimants will be entitled to around 80% of the their current entitlement.")

128

The caseload 6,800 caseload Working age 3,830 ISA/JSA etc Earners Non earners Second adult Elderly 3,000

129

Operating the scheme in a large unitary council Under the new scheme the amount provided to support Council Tax benefit will be reduced by 10% amounting to £6.3m Annual Council Tax benefits £63.0m Less: 10% reduction as proposed£ 6.3m Less: Protection for pension age groups £30.9m Balance to be used for working age£25.8m This means that the assistance with Council tax for working age claimants will be reduced by around 19% which means that in future working age claimants will be entitled to around 80% of the their current entitlement.

130

The caseload 63,257 total caseload Working age 32,115 ISA/JSA etc Earners Non earners Second adult Elderly 31,142

131

What are the realistic options for Billing Authorities? Maximise the tax base and utilise the discount changes Adjust the tax base provision Fund from the Non Domestic Rate growth Own resources? Fund the 10% locally from own resources either partially or fully The Billing Authority proportion The Precepting Authority’s proportion Continue with existing scheme with work incentives less up to 10% cost and protecting vulnerable groups, achieved by either/or A straight cut of the appropriate percentage for all non protected claimants – the “equal pain” approach A flexible approach to minimum benefit or a cap A regressive taper A modified existing scheme protecting vulnerable groups and reducing cost

132

The Council Tax Base

133

Council Tax Dwellings

134

Discounts

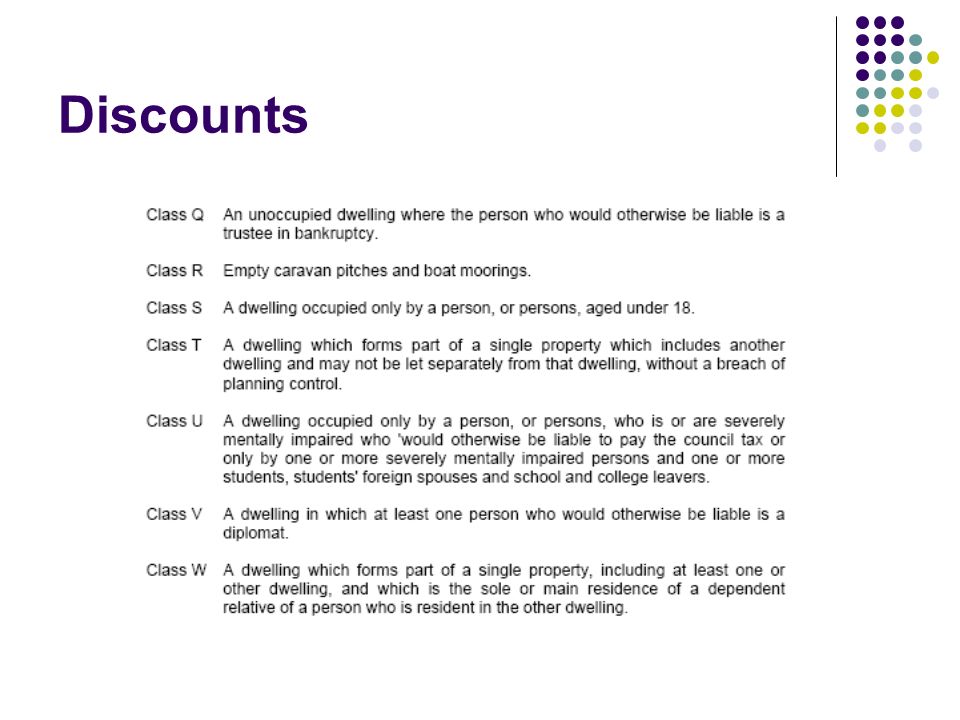

138

Ipswich

139

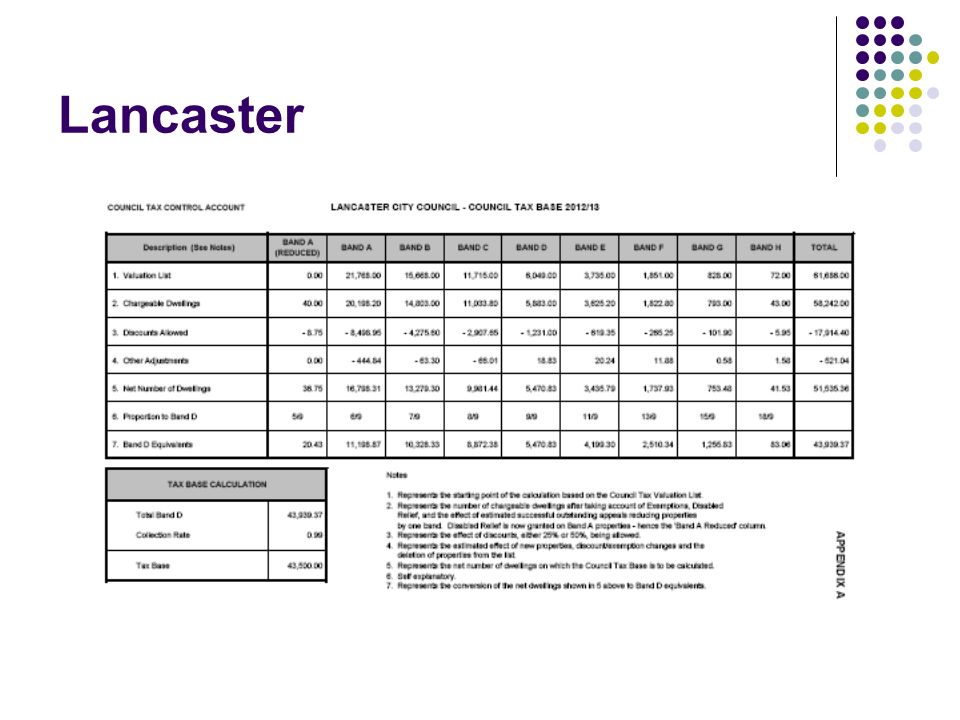

Lancaster

141

Lancaster Non Parished Areas

142

Arnholme Parish

143

Managing Risk

144

Risk sharing Sharing risk through the collection fund Deficit or surplus in the collection fund Shared the following year? Should major precepting authorities be able to influence scheme design? Varying precepts in year To reflect collection rates A new power

145

The risks of localisation If the current financial crises continues, benefit costs will continue to rise. Collection performance could suffer significantly with the 10% reduction which will fall largely on working age claimants. The impact of the reduction in housing costs as a result of housing benefit changes and the cap will have a cumulative affect on the ability to meet council tax and other domestic bills CTB is currently based on actual as opposed to estimated eligibility. Therefore an increase in the number of claimants will automatically lead to an increase in CTB costs This will expose councils to increased expenditure. Any cap on expenditure needs to protect local authorities from the burden of increased caseloads.

146

Managing the risk of fraud and error The consultation document suggests that it is for local authorities to administer support for council tax in as fair and efficient a way as is possible whilst minimising errors and the risk of fraud. The Department for Work and Pensions will be launching the new Single Fraud Investigation Service (SFIS) in April 2013. Local authority administration of fraud and error in LSCT should continue, whilst working in partnership with SFIS where the need arises. In the long term LAs will have to make their own arrangements The risk of fraud and error should be minimised by effective data sharing across all areas of the public sector. The Government have yet to realise the potential savings of comprehensive public sector data sharing coupled with effective partnerships with the private sector.

in April Local authority administration of fraud and error in LSCT should continue, whilst working in partnership with SFIS where the need arises. In the long term LAs will have to make their own arrangements The risk of fraud and error should be minimised by effective data sharing across all areas of the public sector. The Government have yet to realise the potential savings of comprehensive public sector data sharing coupled with effective partnerships with the private sector..")

147

Managing the financial risk Billing authorities should be able to share the risk of any scheme across the tiers of administration and with Precepting Bodies Strict budgetary control is necessary to manage the financial risk Managing the Collection Fund and regular reporting will be critical There is however a need for more discussion on how risk is managed across the tiers of local authorities and between central and local government.

148

Collection Issues

149

And finally, collection issues April 2013 and beyond Collecting residue debt identical to the reduction in LSCT Collecting small balances from those in receipt of LSCT Do you apply for a liability order? If so which remedy do you use? If the debt remains unpaid how will you prove culpable neglect and/or wilful refusal?

150

And Finally, What is the IRRV doing? Membership of the Reference Board and the Delivery Group Partnership with “Destin” on a modelling tool Partnership with “Coactiva” on a Risk Based Verification tool Partnership with “Entitled to” on a UC/LSCT calculator Delivering a “Resource Centre” for LSCT Developing a Mutual model for residue fraud teams and a social enterprise for UC/LSCT/Benefit advice

Similar presentations

Chief Executive Institute of Revenues, Rating and Valuation.>")

Chief Executive Institute of Revenues, Rating and Valuation.>")

Chief Executive Institute of Revenues, Rating and Valuation.>")