Download presentation

Presentation is loading. Please wait.

1

Production

2

Objectives To understand the concept of the short- run, diminishing returns and costs in the short run

3

The Short- run a period of time where at least one factor of production is assumed to be in fixed supply i.e. it cannot be changed Normally assumed that capital and physical land is fixed and that production can be altered through changing labour or input of raw materials

4

The Production Function

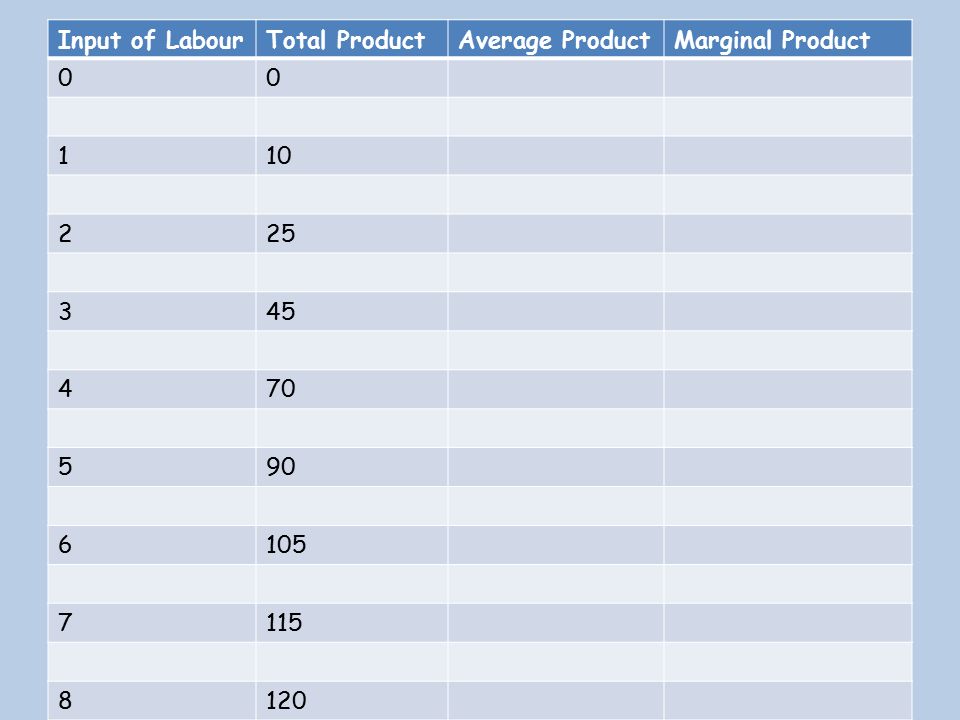

A mathematical expression which relates the quantity of factor inputs to the quantity of outputs that result. Three measures of production / productivity Total product = total output Average product = the total output divided by the number of units of the variable factor of production employed (e.g. output per worker or output per unit of capital employed) Marginal product = the change in total product when an additional unit of the variable factor of production is employed. For example marginal product would measure the change in output that comes from increasing the employment of labour by one person, or by adding one more machine to the production process in the short run

Marginal product = the change in total product when an additional unit of the variable factor of production is employed. For example marginal product would measure the change in output that comes from increasing the employment of labour by one person, or by adding one more machine to the production process in the short run.")

5

The Law of Diminishing Returns: A Simple Demonstration

Terry D. McCraney, Vincennes University I use a simple example to explain the law of diminishing returns to students--sweeping the classroom floor. I usually start by stating the law as simply as possible. Then I tell the class that we have the job of sweeping the floor. All students agree that they are interchangeable when it comes to sweeping. They can all sweep and all can sweep equally well. I ask them how to measure our efficiency, if all sweep equally well. The general response is that we can measure efficiency in terms of time. Then I explain that we have four brooms and I will choose people to serve as sweepers. I choose the first sweeper and tell him it will take 60 minutes to do the job. The use of 60 minutes is for easy division. If you must, you can remind the students that the job was never done before so we have no idea how long it will take to complete the job. A second student is chosen and I ask how long it will take with two sweepers. The response is thirty minutes. Questions may be asked to explain the thirty minute time. After a third sweeper is added the time falls to twenty minutes. A fourth sweeper brings the time to fifteen minutes. Then I add a fifth sweeper and ask for the time. Twelve minutes will be given as the logical answer. Now I explain that twelve minutes is incorrect, and that it will take twenty-four minutes. I ask the students to explain why it took longer with five sweepers than with four. Most of the class will quickly point out that we only have four brooms. Then I restate the law of diminishing returns stressing that sweepers are inputs, brooms are the fixed factors, and the amount of time reflects marginal returns

6

Example- Law of diminishing returns

A firm has 4 machines (fixed factors) and increases it’s output by using more operators to work the machines Production figures per week are in the following table…

and increases it’s output by using more operators to work the machines. Production figures per week are in the following table…")

7

Input of Labour Total Product Average Product Marginal Product 1 10 2 25 3 45 4 70 5 90 6 105 7 115 8 120

8

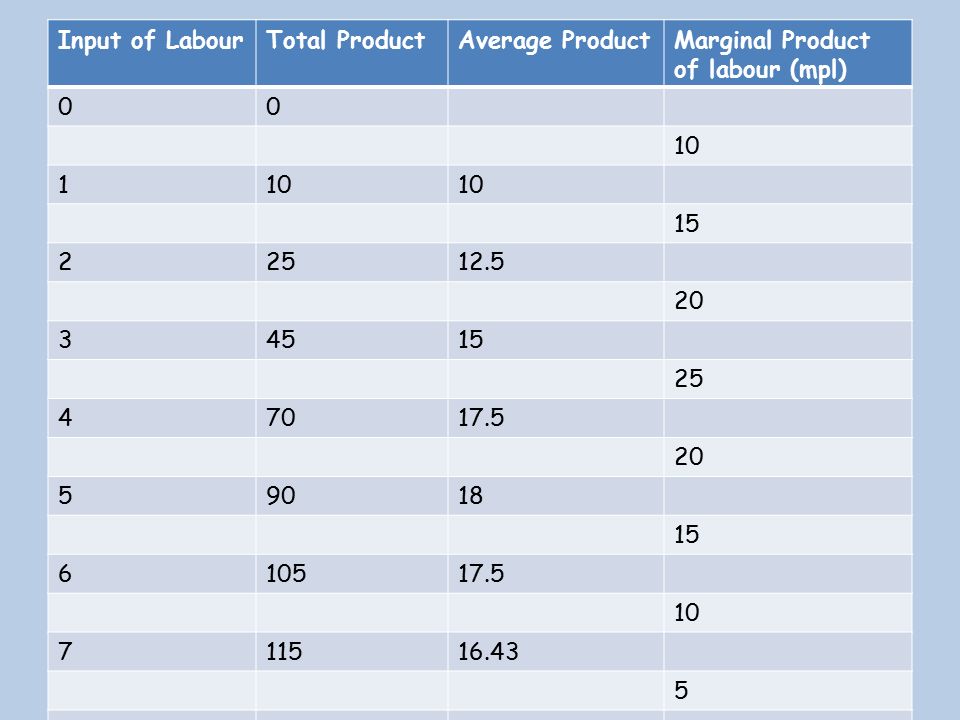

Input of Labour Total Product Average Product Marginal Product of labour (mpl) 10 1 15 2 25 12.5 20 3 45 4 70 17.5 5 90 18 6 105 7 115 16.43 8 120

9

The Law of Diminishing Returns

In the short run, the law of diminishing returns states that As more units of a variable input (i.e. labour or raw materials) is added to fixed amounts of land and capital, the change in total output will at first rise and then fall In example Diminishing returns to labour occurs when the mpl starts to fall. This means that total output will still be rising – but increasing at a decreasing rate as more workers are employed. Eventually a decline in marginal product leads to a fall in average product As a result, the marginal productivity of each worker tends to fall – this is known as the principle of diminishing returns.

is added to fixed amounts of land and capital, the change in total output will at first rise and then fall. In example. Diminishing returns to labour occurs when the mpl starts to fall. This means that total output will still be rising – but increasing at a decreasing rate as more workers are employed. Eventually a decline in marginal product leads to a fall in average product. As a result, the marginal productivity of each worker tends to fall – this is known as the principle of diminishing returns.")

10

Handout

11

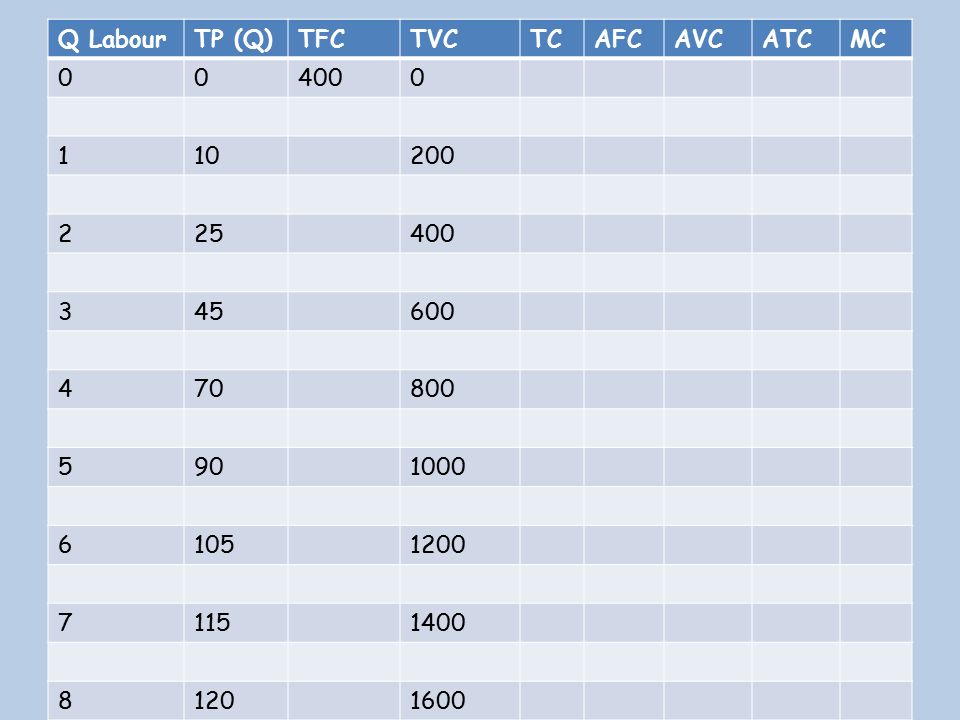

Short- run costs Fixed costs- do not vary with output

Variable Costs- vary directly with output Total cost= fixed costs + variable costs Average Cost= Total costs/ output Marginal Cost= addition to total cost when one extra unit of output is produced

12

Q Labour TP (Q) TFC TVC TC AFC AVC ATC MC 400 1 10 200 2 25 3 45 600 4 70 800 5 90 1000 6 105 1200 7 115 1400 8 120 1600

13

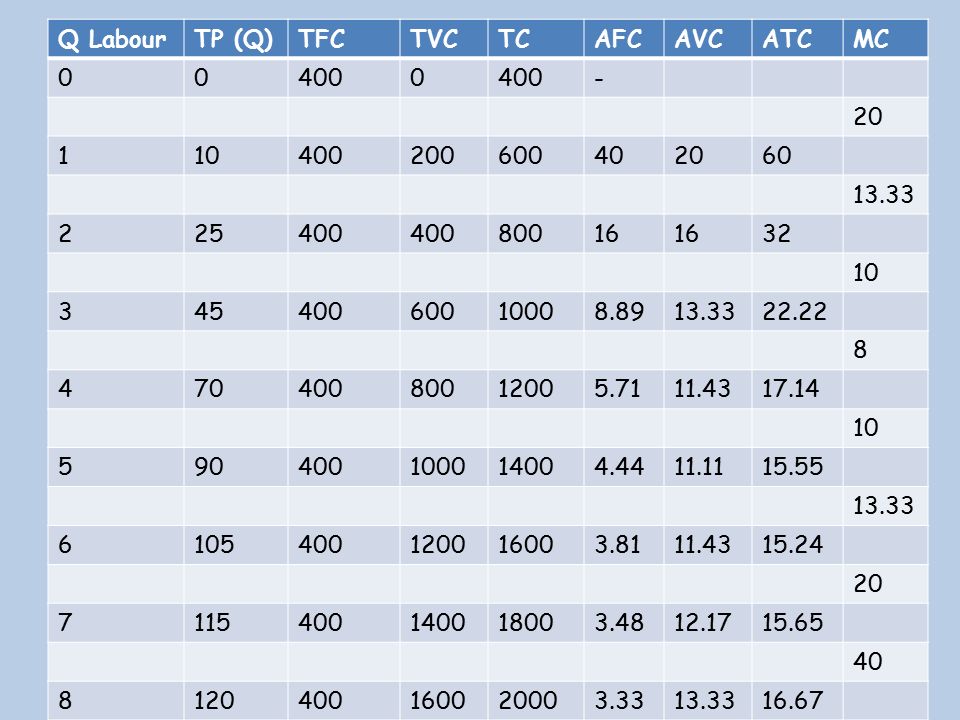

Q Labour TP (Q) TFC TVC TC AFC AVC ATC MC 400 - 20 1 10 200 600 40 60 13.33 2 25 800 16 32 3 45 1000 8.89 22.22 8 4 70 1200 5.71 11.43 17.14 5 90 1400 4.44 11.11 15.55 6 105 1600 3.81 15.24 7 115 1800 3.48 12.17 15.65 120 2000 3.33 16.67

14

On graph Paper Plot the TC, TFC and TVC

15

Average Costs Costs per unit of output

Plot the AFC, AVC and ATC on a separate graph Why are the AC curves shaped as they are? Average Fixed Costs- Because TFC is constant AFC always falls as output increases Average Variable Costs- Tends to fall as output rises (due to increasing returns to the variable factor as more are employed and more specialised methods are adopted) and then starts to rise again as output continues to increase, this is due to the concept of diminishing returns Average cost (AC) (or average total cost (ATC)) = AFC + AVC and is therefore ‘U’ shaped because of the reasons above Now plot the MC curve on this graph

and then starts to rise again as output continues to increase, this is due to the concept of diminishing returns. Average cost (AC) (or average total cost (ATC)) = AFC + AVC and is therefore ‘U’ shaped because of the reasons above. Now plot the MC curve on this graph.")

16

Marginal Costs MC tends to fall as output increases, and then starts to rise again as output continues to increase. Explained by the concept of diminishing returns.

17

Relationship between AC, AVC and MC curve

The MC curve cuts the AVC and AC curve at their lowest points AFC falls as output increases and, since it is the difference between AC and AVC, the vertical gap between AC and AVC gets smaller as output grows.

18

Illustrated…

19

AC Output MC AVC Optimum Output MC= ATC

20

The MC and AC of Late Arrivals at Small Parties

Frederick S. Weaver, Hampshire College How can the marginal cost curve start rising before the average cost curve does? Why does the marginal cost curve always intersect the average cost curve as its minimum point? These are simply arithmetic relationships, but they do confuse students and are sufficiently important to the theory of the firm that they warrant some special attention. An example that works for me is to ask students to imagine a small gathering of, say, ten people, and the average height of those at the party is 5'7". But some people are still arriving, and a latecomer who is 5'2" tall arrives at the party. What does this marginal guest do to the average height of those at the party (i.e., what direction does it change)? Another person, who is 5'3" arrives, and the average height of the roomful of revelers is pulled down a bit more. Yet another character drifts in, and her height is 5'6". The average height again declines (to 5'7"), as it has consistently even though the successive marginal changes have been getting larger. So as long as the increments are below the average, the average declines. Anyway, back to the party: when a person who is 5'7" joins the party, the average is unchanged, and when someone 5'8" tall finally manages to get there, the average height rises. So when a person of average height joints the festivities, the average does not change, but when someone above average height appears on the scene, the average height rises. Ergo, the marginal curve intersects the average curve at the average curve's minimum point. Only directions of change rather than the particular numbers matter, but from experience, it pays to have a clear numerical example worked out before class. Initial confusion may facilitate understanding of some analytical issues, but this is not one of them!

Another person, who is 5 3 arrives, and the average height of the roomful of revelers is pulled down a bit more. Yet another character drifts in, and her height is The average height again declines (to 5 7 ), as it has consistently even though the successive marginal changes have been getting larger. So as long as the increments are below the average, the average declines. Anyway, back to the party: when a person who is 5 7 joins the party, the average is unchanged, and when someone 5 8 tall finally manages to get there, the average height rises. So when a person of average height joints the festivities, the average does not change, but when someone above average height appears on the scene, the average height rises. Ergo, the marginal curve intersects the average curve at the average curve s minimum point. Only directions of change rather than the particular numbers matter, but from experience, it pays to have a clear numerical example worked out before class. Initial confusion may facilitate understanding of some analytical issues, but this is not one of them!")

Similar presentations

Think about how production might occur and change as different amounts of.>")