Download presentation

Presentation is loading. Please wait.

1

Lecture 24 Practice Questions

2

Lecture Overview Contribution Margin Method MCQs Test

CVP Relationships in Graphic Form CVP Graph Target Profit Analysis The CVP Equation The Contribution Margin Approach The Margin of Safety

3

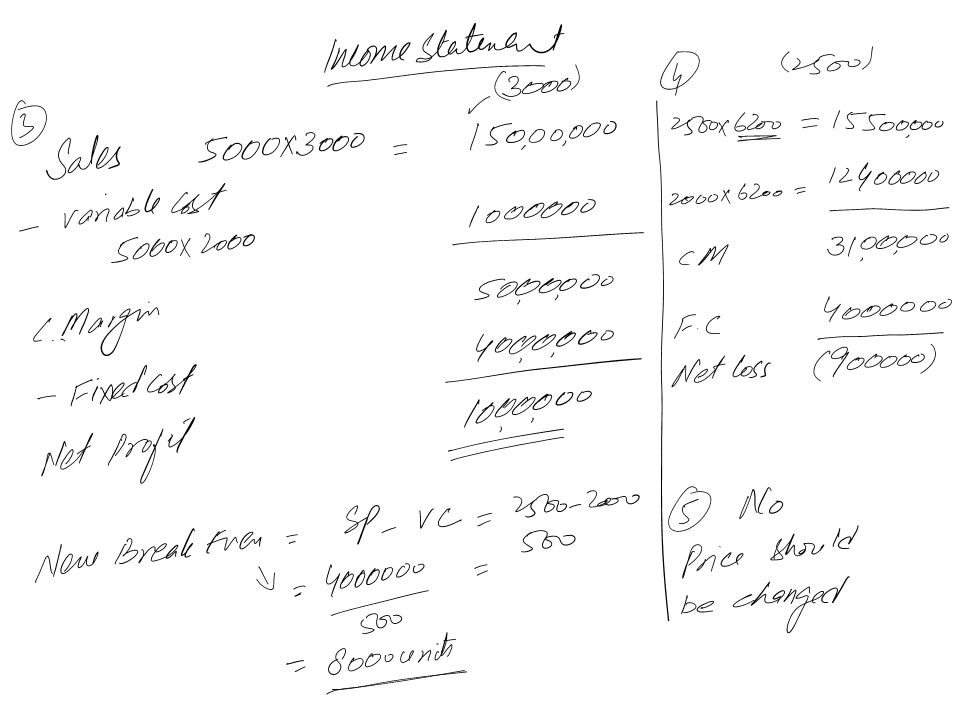

Company Oliver located in Karachi manufactures computer casing

Company Oliver located in Karachi manufactures computer casing. The firm`s fixed costs are Rs per month while prices are Rs and Variable Cost Rs each. Company sold 5000 components during the previous year. Requirements Compute the break-even point in units. What will the new break-even point be if fixed costs increase by 10 percent? What was the company`s net income for the prior year? The sales manager believes that a reduction in the sales price to Rs 2500 will result in orders for 1200 more components each year. What will be break-even point be if price is changed? Should the price change discuss in requirement (4) be made?

be made")

6

The Concept of Sales Mix

Sales mix is the relative proportions in which a company’s products are sold. Different products have different selling prices, cost structures, and contribution margins. Let’s assume Wind sells bikes and carts and see how we deal with break-even analysis.

7

Multi-product break-even analysis

Wind Bicycle Co. provides the following information: $265,000 $550,00 = 48.2% (rounded)

")

8

Multi-product break-even analysis

Rounding error

9

Assumptions of CVP Analysis

Selling price is constant throughout the entire relevant range. Costs are linear throughout the entire relevant range. In multi-product companies, the sales mix is constant. In manufacturing companies, inventories do not change (units produced = units sold).

.")

10

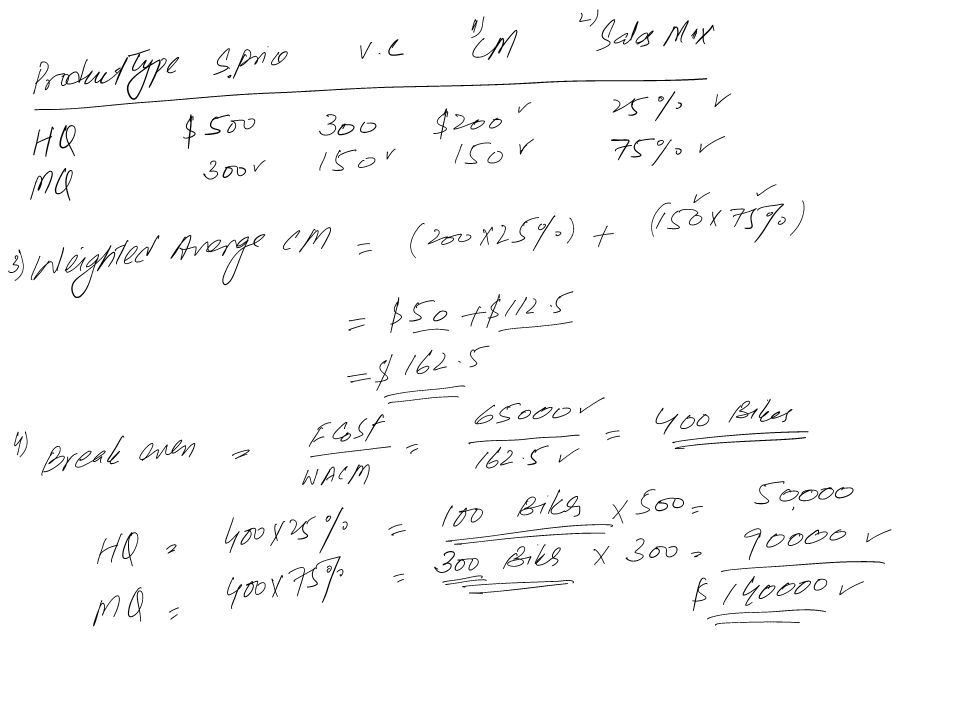

Tim`s Bicycle shop sells speed race bicycles

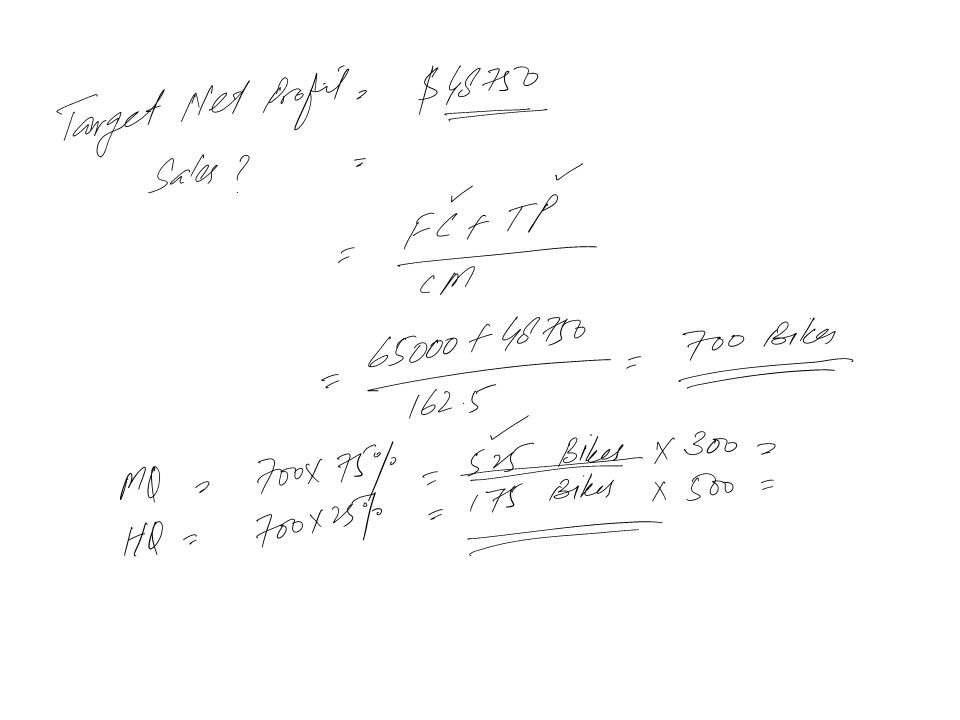

Tim`s Bicycle shop sells speed race bicycles. For purposes of a cost volume profit analysis, the shop owner has divided sales into two categories as follows: Product Type Sales Price Invoice Cost Sales Commissions High Quality $500 $275 $25 Medium Quality 300 135 15 Three quarters of the shop`s sales are medium-quality bikes. The shop`s annual fixed expenses are $ (in the following requirements, ignore income tax) Required Compute the unit contribution margin for each product type. What is the shop`s sales mix? Compute the weighted-average unit contribution margin, assuming a constant sales mix What is the shop`s break-even sales volume in dollars? Assume a constant sales mix. How many bicycles of each type must be sold to earn a target net income of $48,750? Assume a constant sales mix.

Required. Compute the unit contribution margin for each product type. What is the shop`s sales mix Compute the weighted-average unit contribution margin, assuming a constant sales mix. What is the shop`s break-even sales volume in dollars Assume a constant sales mix. How many bicycles of each type must be sold to earn a target net income of $48,750 Assume a constant sales mix.")

14

Compute the unit contribution margin for each product type.

Tim`s Bicycle shop sells speed race bicycles. For purposes of a cost volume profit analysis, the shop owner has divided sales into three categories as follows: Product Type Sales Price Invoice Cost Sales Commissions High Quality $500 $275 $25 Medium Quality 300 135 15 Low Quality 150 75 25 Two quarters of the shop`s sales are low-quality bikes and one quarter each to the high quality and medium quality. The shop`s annual fixed expenses are $ (In the following requirements, ignore income tax) Required Compute the unit contribution margin for each product type. What is the shop`s sales mix? Compute the weighted-average unit contribution margin, assuming a constant sales mix What is the shop`s break-even sales volume in dollars? Assume a constant sales mix. How many bicycles of each type must be sold to earn a target net income of $50625? Assume a constant sales mix.

Required. Compute the unit contribution margin for each product type. What is the shop`s sales mix Compute the weighted-average unit contribution margin, assuming a constant sales mix. What is the shop`s break-even sales volume in dollars Assume a constant sales mix. How many bicycles of each type must be sold to earn a target net income of $50625 Assume a constant sales mix.")

17

Lecture Overview The Concept of Sales Mix

Multi-product break-even analysis Assumptions of CVP Analysis

18

End of Lecture 24

Similar presentations

Bab 4. © The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill Dasar Analisis Cost-Volume-Profit (CVP) Contribution.>")

CURL SURFBOARDS>")

Analysis.>")

Analysis Contribution margin (CM) is the difference between sales revenue and variable expenses. Next Page Click.>")

Analysis.>")