Download presentation

Presentation is loading. Please wait.

1

8-1 CHAPTER 9 Stocks and Their Valuation Features of common stock Stock valuations Constant dividend growth model The behavior of dividends and their PV The model Applying the model when g>r, g=0 and g<0 Future stock price Dividend yield and capital gain Non-constant growth model Preferred stock

2

8-2 Facts about common stock Represents ownership Ownership implies control Stockholders elect directors Directors elect management Receives cash flow in the form of dividend Management’s goal: Maximize the stock price

3

8-3 Dividend growth model Value of a stock is the present value of the future dividends expected to be generated by the stock.

4

8-4 Constant growth stock A stock whose dividends are expected to grow forever at a constant rate, g. D 1 = D 0 (1+g) 1 D 2 = D 0 (1+g) 2 D t = D 0 (1+g) t

1 D 2 = D 0 (1+g) 2 D t = D 0 (1+g) t.")

5

8-5 Constant growth stock If g is constant, the dividend growth formula converges to:

6

8-6 What happens if g > r s ? If g > r s, the constant growth formula leads to a negative stock price, which does not make sense. The constant growth model can only be used if: r s > g g is expected to be constant forever

7

8-7 If r RF = 7%, r M = 12%, and β = 1.2, what is the required rate of return on the firm’s stock? Use the SML to calculate the required rate of return (k s ): r s = r RF + (r M – r RF )β = 7% + (12% - 7%)1.2 = 13% D 0 = $2 and g is a constant 6%,

: r s = r RF + (r M – r RF )β = 7% + (12% - 7%)1.2 = 13% D 0 = $2 and g is a constant 6%,.")

8

8-8 What is the stock’s market value? Using the constant growth model:

9

8-9 What would the expected price today be, if g = -5%?, if g=0? When g=-5% D1=1.9, P=1.9/(13%+5%)=10.56 When g=0, The dividend stream would be a perpetuity. 2.00 0123 r s = 13%...

=10.56 When g=0, The dividend stream would be a perpetuity r s = 13%....")

10

8-10 Computing other variables Computing Ks Computing D Computing g

11

8-11 What is the expected market price of the stock, one year from now? D 1 will have been paid out already. So, P 1 is the present value (as of year 1) of D 2, D 3, D 4, etc.

of D 2, D 3, D 4, etc..")

12

8-12 Future stock price What is the expected market price of the stock P 2, two years from now? What is the expected market price of the stock P n, n years from now?

13

8-13 The growth rate of stock price What is the % change of stock price from P 0 to P 1 and from P 1 to P 2 What is the % change of stock price from P n to P n+1 What is the expected market price of the stock P 2, two years from now? P 2 =P 1 *(1+g)= P 0 *(1+g) 2

= P 0 *(1+g) 2.")

14

8-14 Dividend Yield and Capital Gain P 0 =D 1 /(r-g) k=(D 1 /P 0 )+g Total return=dividend yield + Capital gain g is capital gain for constant growth stock

k=(D 1 /P 0 )+g Total return=dividend yield + Capital gain g is capital gain for constant growth stock")

15

8-15 What is the expected dividend yield, capital gains yield, and total return during the first year? Dividend yield = D 1 / P 0 = $2.12 / $30.29 = 7.0% Capital gains yield = (P 1 – P 0 ) / P 0 = ($32.10 - $30.29) / $30.29 = 6.0% Total return (r s ) = Dividend Yield + Capital Gains Yield = 7.0% + 6.0% = 13.0%

/ P 0 = ($ $30.29) / $30.29 = 6.0% Total return (r s ) = Dividend Yield + Capital Gains Yield = 7.0% + 6.0% = 13.0%.")

16

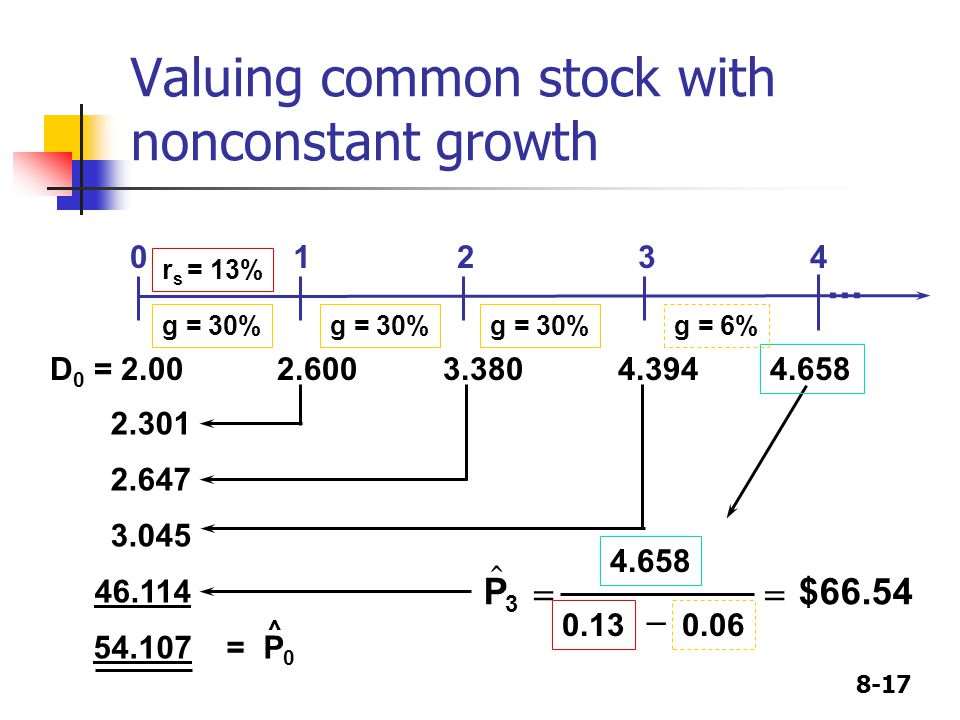

8-16 Supernormal growth: What if g = 30% for 3 years before achieving long-run growth of 6%? Can no longer use just the constant growth model to find stock value. However, the growth does become constant after 3 years.

17

8-17 Valuing common stock with nonconstant growth r s = 13% g = 30% g = 6% P 0.06 $66.54 3 4.658 0.13 2.301 2.647 3.045 46.114 54.107 = P 0 ^ 01234 D 0 = 2.00 2.600 3.380 4.394... 4.658

18

8-18 Nonconstant growth: What if g = 0% for 3 years before long- run growth of 6%? r s = 13% g = 0% g = 6% 0.06 $30.29P 3 2.12 0.13 1.77 1.57 1.39 20.99 25.72 = P 0 ^ 01234 D 0 = 2.00 2.00 2.00 2.00... 2.12

19

8-19 Preferred stock Hybrid security Like bonds, preferred stockholders receive a fixed dividend that must be paid before dividends are paid to common stockholders. However, companies can omit preferred dividend payments without fear of pushing the firm into bankruptcy.

20

8-20 A preferred stock has an annual dividend of $5, what should the preferred stock price be if discount rate is 10%? V p = D / r p $50= $5 / 10%

Similar presentations

>")