Download presentation

Presentation is loading. Please wait.

1

The CAP: origins, institutions and financing Economics of Food Markets Lecture 7 Alan Matthews

2

Objectives The complex structure of EU agriculture The decision-making processes in the CAP How the CAP price support mechanisms work Characteristics of individual common market organisations The budgetary framework for CAP expenditure The ‘green money’ mechanism A critical assessment of the consequences of the CAP

3

Reading Ackrill, R. 2000 The Common Agricultural Policy Tracy, M., 1997 Agricultural Policy in the European Union and other Market Economies Fennell, 1997, The Common Agricultural Policy: continuity and change Shucksmith, M., Thompson, K and Roberts, D., 2005, CAP and the Regions: the territorial impact of the CAP Grant, W. 1997, The Common Agricultural Policy Ingersent, Rayner and Hine, 1998, The Reform of the Common Agricultural Policy. Commission DG Agriculture and Food website

4

Source: European Commission, The CAP Explained Differing agricultural structures

5

EmploymentGross domestic product 195019731999195019731999 EU-15::4.5::1.8 Belgium123.92.48.84.21.2 Denmark229.43.320.09.02.0 Germany237.32.912.33.50.9 Greece54:17.033.5:7.1 Spain49:7.435.0:4.1 France3211.94.3:6.52.4 Ireland4025.18.631.319.02.9 Italy3916.35.429.59.92.6 Netherlands196.63.212.95.82.4 Austria32:6.216.4:1.2 Portugal47:12.726.8:3.3 Finland::6.4::0.9 Sweden18:3.07.0n.a.0.7 UK52.91.26.03.00.9

6

Number of farms Average farm size Per cent of farms > 50 ha Per cent of farms < 10 ha 199719871997 ‘000ha % EU-15 6,989.1:18.48.668.6 Belgium 67.217.320.610.044.2 Denmark 63.232.542.627.819.5 Germany 534.417.632.114.145.6 Greece 821.45.34.30.490.0 Spain 1,208.316.021.28.269.0 France 679.830.741.729.735.3 Ireland 147.822.729.414.119.8 Italy 2,315.27.76.41.887.4 Netherlands 107.917.218.67.146.4 Austria 210.1:16.34.046.4 Portugal 416.78.39.22.387.5 Finland 91.4:23.78.824.2 Sweden 89.6:34.720.229.8 UK 233.268.969.333.726.8

7

Brief history of CAP origins Article 33 (ex 39) set out objectives, but left open means to achieve these objectives Note all original member states already had protectionist agricultural policies, so EC was not starting with a clean slate Key decisions on market mechanisms taken in January 1962, though common prices not achieved until 1968 Principles established Market unity Community preference Financial solidarity (Producer co-responsibility)

set out objectives, but left open means to achieve these objectives Note all original member states already had protectionist agricultural policies, so EC was not starting with a clean slate Key decisions on market mechanisms taken in January 1962, though common prices not achieved until 1968 Principles established Market unity Community preference Financial solidarity (Producer co-responsibility)")

8

CAP objectives and instruments CAP objectives set out in Article 33 (ex 39) –to increase agricultural productivity –to ensure a fair standard of living for the agricultural community –to stabilise markets –to ensure the availability of supplies –to ensure that supplies reach consumers at reasonable prices –Note no mention of environment, food safety or rural development Two broad policy instruments –Price policy implemented through market organisation measures and funded by the Guarantee Section of EAGGF (FEOGA) –Socio-structural measures funded by the Guidance Section of FEOGA –Original expenditure ratio of 2:1 envisaged, in practice turned out to be nearer 95:5.

–to increase agricultural productivity –to ensure a fair standard of living for the agricultural community –to stabilise markets –to ensure the availability of supplies –to ensure that supplies reach consumers at reasonable prices –Note no mention of environment, food safety or rural development Two broad policy instruments –Price policy implemented through market organisation measures and funded by the Guarantee Section of EAGGF (FEOGA) –Socio-structural measures funded by the Guidance Section of FEOGA –Original expenditure ratio of 2:1 envisaged, in practice turned out to be nearer 95:5.")

9

Agricultural decision-making in the EU Distribution of powers between EU institutions: –originally Commission proposes, Council disposes, Parliament advises, and Court rules Greater EP powers of co-decision –but only consultative powers on CAP expenditure, will change with Reform Treaty Role of member states and lobby groups –Formalised through management and advisory committees Majority voting and the Luxembourg compromise –Consensus decision-making encouraged by willingness of some member states to form a blocking minority when ‘vital interests’ of another are at stake. Of doubtful current relevance Annual price review –Based on formula approach in the past, now of much less significance because Commission’s powers to manage markets increased under the Financial Perspective.

10

Price policy mechanisms Cereals taken as the prototypical regime but each commodity regime has its own characteristics Three support pillars of import levies, intervention buying and export subsidies. Additional support through consumer subsidies, aids to private storage, withdrawals, deficiency payments Objective has been to provide price stability as well as price support, hence variable nature of trade instruments Mechanisms are in theory neutral as between farmers and consumers although price levels in practice set very high Support provided at wholesale, not farm, level. Assumes competition in commodity markets to reflect support back to farmers.

11

Pre-GATT Uruguay Round CAP mechanisms variable levy export subsidy world price threshold price intervention price target price ImportInternalExport

12

The green money (agri-monetary) system CAP prices fixed in ecus (euros), require conversion rates to national currencies Conversion rates used administered (green) exchange rates Devaluation should raise domestic prices, revaluation should lower domestic prices Governments manipulated green rates to prevent these market effects from occurring, thus causing market prices within the EU to diverge Differences compensated for by border taxes and subsidies (MCAs monetary compensatory amounts)

system CAP prices fixed in ecus (euros), require conversion rates to national currencies Conversion rates used administered (green) exchange rates Devaluation should raise domestic prices, revaluation should lower domestic prices Governments manipulated green rates to prevent these market effects from occurring, thus causing market prices within the EU to diverge Differences compensated for by border taxes and subsidies (MCAs monetary compensatory amounts)")

13

The green money (agri-monetary) system Introduction of ‘switchover system’ in 1984 at German insistence to prevent a cut in German nominal support prices meant a hidden upward push to support prices in that decade across the EU (extra 21% by 1992) Consequences of green money system and MCAs –While intended to prevent trade distortions, created additional distortions due to limited coverage, inadequate compensation and possibilities of fraud Changes consequent to single market 1 January 1993 –Abolition of MCAs and the switchover system –Compensatory aid to farmers if prices cut by currency revaluation –Now relevant only to countries outside euro zone

system Introduction of ‘switchover system’ in 1984 at German insistence to prevent a cut in German nominal support prices meant a hidden upward push to support prices in that decade across the EU (extra 21% by 1992) Consequences of green money system and MCAs –While intended to prevent trade distortions, created additional distortions due to limited coverage, inadequate compensation and possibilities of fraud Changes consequent to single market 1 January 1993 –Abolition of MCAs and the switchover system –Compensatory aid to farmers if prices cut by currency revaluation –Now relevant only to countries outside euro zone")

14

Budget impact of the CAP The role of the EU’s ‘own resources’ – currently customs duties, VAT-based contribution and the GNP resource Overall EU budget very small, but share of CAP spending very high Transfers between member states arising from common financing of the CAP inequitable and a source of controversy Attempts to control budget expenditure have been a significant driver of CAP reform

15

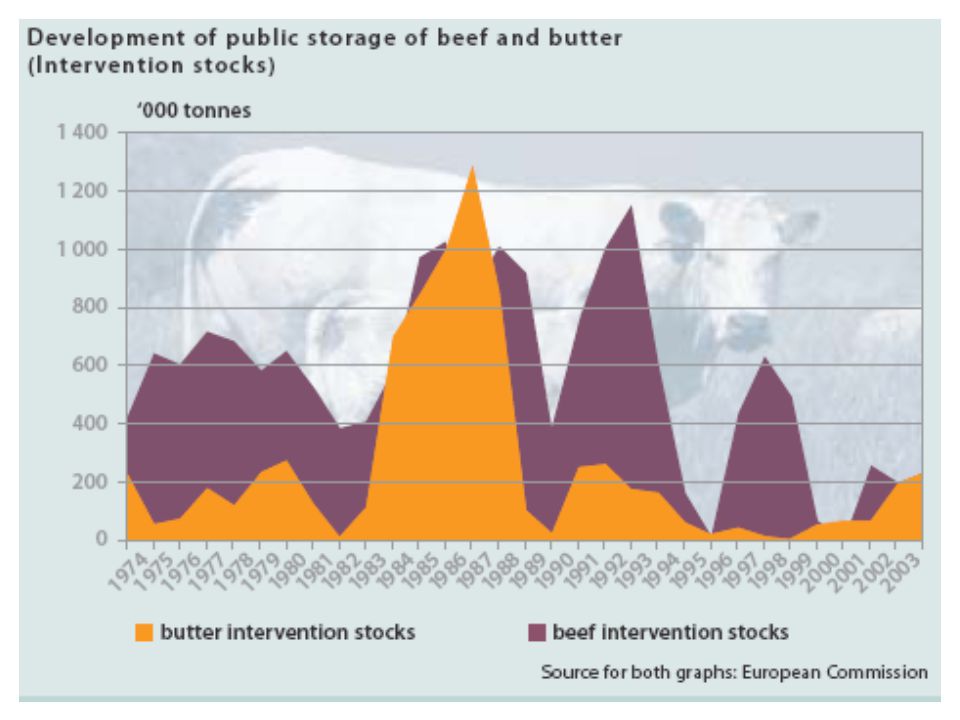

Consequences of EU price support policies Growth in self-sufficiency due to supply outrunning demand Unforeseen reliance on intervention mechanisms, although currently much reduced Uneven levels of protection across commodities, particularly for cereals/oilseeds and cereal substitutes Regional disparities in support – the North/South divide within the EU Introduction of milk quotas 1984 (until then, sugar was only CMO using quotas)

")

18

Problems of agricultural price policy at beginning of the 1990s an uncommon market –a single agricultural market was created, but... –green currencies kept prices different and... –veterinary and plant health rules kept the market fragmented growing overproduction and intervention overload... … leading to growing budget costs the inefficiency of CAP price policy –large transactions costs incurred to transfer income support the inequity of CAP price policy –larger farmers benefit at the expense of low income consumers, and more advantaged regions attract higher levels of support environmental costs of the CAP price policy –higher prices encouraged intensification and greater input use

Similar presentations

After a long time of food shortages suffered by Europe throughout WWII. Established in 1957 with the Rome Treaty upon.>")