Download presentation

Presentation is loading. Please wait.

1

Derivative-Based Risk Management Crude Oil Deliverable Oil King Management Team: Xiao Meng Sayam Ibrahim Tanya Patwa

2

The Situation We are an oil drilling company called Oil King operating in Texas. We will have a delivery of 100,000 barrels (100 futures contracts) of WTI crude oil to a cruise line company deliverable on January 1 2008. We have not locked in a price yet. (We are Long)

of WTI crude oil to a cruise line company deliverable on January We have not locked in a price yet. (We are Long).")

3

Market Outlook As of December 7 th the January futures contracts are at $88.28.There have been talks of OPEC increasing the supply of crude oil, which would cause the price of the January contract to sell off. However, if OPEC decides not to increase world supply of oil, the price may increase. The odds of each situation occurring are equal. As a result, we expect the volatility of crude oil to remain at historical levels and we have a neutral view in regards to price direction.

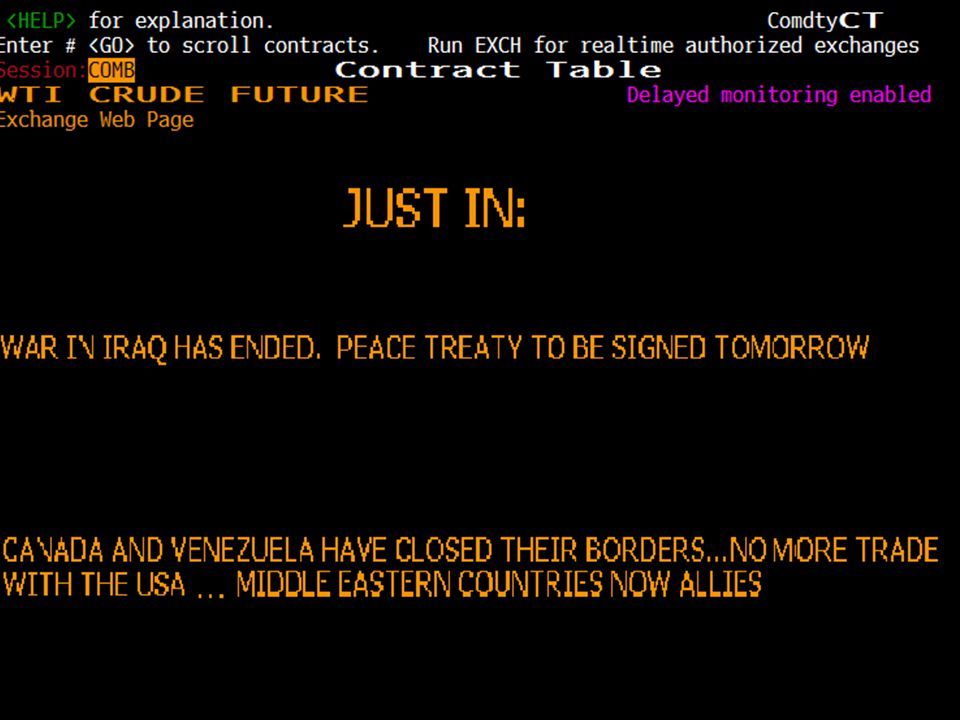

5

Update!!! Given the recent news that has just been released, it is difficult to predict the direction of crude oil futures prices. However, due to the fact that these headlines will have major impacts on crude prices, our view is now that volatility will be extremely high without a directional bias.

6

Our Purpose We want to hedge our long crude oil position based on our view that volatility between today and the contract maturity date will be greater than the implied volatility, with a direction neutral view. After a thorough analysis done by our quantitative analyst, Dr. Bodurtha, he came to the conclusion that the volatility (judgmental) will be 50%, which is greater than the implied volatility of 37.79%. This implies a likely range of $71.14 – $109.55 for 25 days.

will be 50%, which is greater than the implied volatility of 37.79%. This implies a likely range of $71.14 – $ for 25 days..")

7

Volatility Going Up

8

F8 (Jan08) Futures Most Liquid

Futures Most Liquid")

9

Futures Market Situation Underlying - SS = Crude oil - CLJanMar Current date 12/07/2007 Settle (Close) Price88.2887.94 Actual Maturity date1/1/20083/1/2008 SymbolCLF8CLH8 Units of underlying each contract represent: 1,000 Barrels (42,000 gallons)

Price Actual Maturity date1/1/20083/1/2008 SymbolCLF8CLH8 Units of underlying each contract represent: 1,000 Barrels (42,000 gallons)")

10

Risk Management We seek to manage the risk of Light Sweet crude oil (CL) Total exposure value: 100,000 barrels = $8.828 million. Percentage loss limit decided upon for our exposure based on our risk tolerance: 5%, which is equivalent to a dollar value of $441,400.

11

Critical probability level We want only a 5% chance of losing more than $441,400. For the CL underlying January 1 maturity date and 25 (remaining) day futures contract: = $88.28 with R = 4.8 and RP = 0% (*next slide) Our 5% loss limit critical price level is calculated relative to a measure of the consensus market expectation: Expected Futures Price = $88.28

day futures contract: = $88.28 with R = 4.8 and RP = 0% (*next slide) Our 5% loss limit critical price level is calculated relative to a measure of the consensus market expectation: Expected Futures Price = $")

12

Risk Premium Calculation VolmonthlyAnnualσ(WTI) / σ(S&P) S&P6.57246522.767691.208070336 WTI7.9427.50497 Correlation S&P-WTI -0.08261 Beta-0.0998 Market Return 5.00% Risk Free Rate 4.17% Crude Oil Risk Premium -0.000828319 Our risk premium calculation is a small negative number (-0.000828319), which we attribute to recent market trends in which commodity prices have been increasing while equity markets have been selling off. Consequently, we will use 0% as our risk premium.

13

Critical Prices for One Year Annualized standard deviation estimate (risk metrics): 26.154% For a long exposure, the lower critical price level equals = 88.28*e -.26154* 1.65 = $57.34 For a short exposure, the upper critical price level equals = 88.28*e.26154 * 1.65 = $135.92 Likely range for one year: $57.34 – $135.92

: % For a long exposure, the lower critical price level equals = 88.28*e * 1.65 = $57.34 For a short exposure, the upper critical price level equals = 88.28*e * 1.65 = $ Likely range for one year: $57.34 – $135.92")

14

Critical Prices for 25 days Annualized standard deviation estimate (risk metrics): 26.154% For a long exposure, the lower critical price level equals = 88.28*e -.26154 * 1.65 = $78.79 For a short exposure, the upper critical price level equals = 88.28*e.26154 * 1.65 = $98.92 Likely range for 25 days: $78.79 - $98.92

: % For a long exposure, the lower critical price level equals = 88.28*e * 1.65 = $78.79 For a short exposure, the upper critical price level equals = 88.28*e * 1.65 = $98.92 Likely range for 25 days: $ $98.92")

15

Hedging with Futures From the calculation above, there is a 5 % chance that the underlying price will be at or below $78.79 in 25 days. The associated loss relative to selling the underlying at the current futures price of $88.28 equals the "loss at the lower critical price level" = -10.75% Long exposure that may be retained: = -5%/-10.75% = 46.51% Roughly, we must decrease our exposure by one minus the amount of loss that may be retained: 1 - (.4651) =.5349 For the underlying position of $8.828 million, we must sell 53.49% or $4,722,097 How many futures contracts equal our underlying exposure? = 100 How many futures must we sell to meet our risk targets? 54

=.5349 For the underlying position of $8.828 million, we must sell 53.49% or $4,722,097 How many futures contracts equal our underlying exposure. = 100 How many futures must we sell to meet our risk targets. 54.")

16

Value @ Risk

17

Initial Position

18

Hedge with Futures

19

Hedging with Options Direction view: neutral Volatility view: volatile CallsPuts In-at-out of moneyStrike PricePrice QuoteStrike PricePrice Quote More OTM920.48850.54 OTM901871.13 ATM88.51.688.51.82 ITM872.41902.72 More ITM853.82924.2

20

Views and Positions Vol upVol stableVol down Up * (synthetic call) Not Likely Not Likely Stable X long straddle (even more volatile: long strangle) * (butterfly spread) Not Likely Down * (synthetic put) Not Likely

Not Likely Not Likely Stable X long straddle (even more volatile: long strangle) * (butterfly spread) Not Likely Down * (synthetic put) Not Likely")

21

Recommended Strategy: Synthetic Long Straddle Purpose: Trade Volatility, Insurance

22

More Aggressive Long Straddle Purpose: Trade Volatility, Insurance

23

Alternative Way to Create Long Straddle cost is the same Purpose: Trade Volatility, Insurance

24

More Aggressive Long Straddle (alternative strategy) Purpose: Trade Volatility, Insurance

Purpose: Trade Volatility, Insurance")

25

Even more volatility: Long Strangle Purpose: Trade Volatility, Insurance

26

More Aggressive Long Strangle Purpose: Trade Volatility, Insurance

27

Volatility Neutral: Butterfly Spread Purpose: Trade Volatility, Insurance, Income

28

More Aggressive Butterfly Spread Purpose: Trade Volatility, Insurance, Income

29

Price up: Synthetic Long Call Purpose: Trade, Insurance

30

Breakeven Analysis for Call

31

Price Down: Synthetic Long Put Purpose: Trade, Insurance

32

Breakeven Analysis for Put

33

Recommendation Given that our view is long volatility and price direction neutral, our options are long straddle and long strangle. More specifically, we have the choice of levering our volatility position with options while still meeting our 5% risk limit. We have decided that as an oil drilling company, our purpose is to hedge our exposure with as little risk as possible. While we have set our risk limits to 5%, given the nature of our business, it is not in our best interest to approach our risk limits to speculate with a levered position, the more aggressive straddle and strangle. After evaluating the different alternatives available to us, we believe that the best strategy given our risk tolerance, nature of business, and purpose is to put on a synthetic long straddle trade (3.62%). Although, it would be cheaper to implement a strangle (2.41%), given the fact that only 25 days remain to maturity, a long straddle position seems to be the more sensible approach. This is because the options are at the money and thus delta is 50, while the delta of the strangle is less than 50 because it involves out of the money options, implying a lower likelihood of ending in the money in before expiration.

. Although, it would be cheaper to implement a strangle (2.41%), given the fact that only 25 days remain to maturity, a long straddle position seems to be the more sensible approach. This is because the options are at the money and thus delta is 50, while the delta of the strangle is less than 50 because it involves out of the money options, implying a lower likelihood of ending in the money in before expiration..")

Similar presentations

Hee Joo Kim Joyce Chung Michael Chen Orlando Ardila May 8, 2012.>")

would prefer to hedge their.>")