Download presentation

Presentation is loading. Please wait.

1

Commodity Market Outlook WBFI Annual Meeting T. Randall Fortenbery Professor School of Economic Sciences Washington State University

4

Price Relationships Sunflower and Safflower prices are highly correlated with soybean prices when looking at national average prices on an annual basis. Proso Millet prices are highly correlated with corn prices. This suggests that we can look at current futures prices for soybeans and corn, and unless we believe they are somehow “biased” we can infer what the market is currently saying about sunflower, safflower, and millet prices in the coming year.

5

Sunflower Prices If we look at sunflower prices over the last 11 years or so, Changes in the annual values from year to year have about a 95 percent correlation with soybean price changes. In other words, soybean price changes explain about 95 percent of the variation in sunflower prices.

6

Actual vs. Predicted Sunflower Prices

10

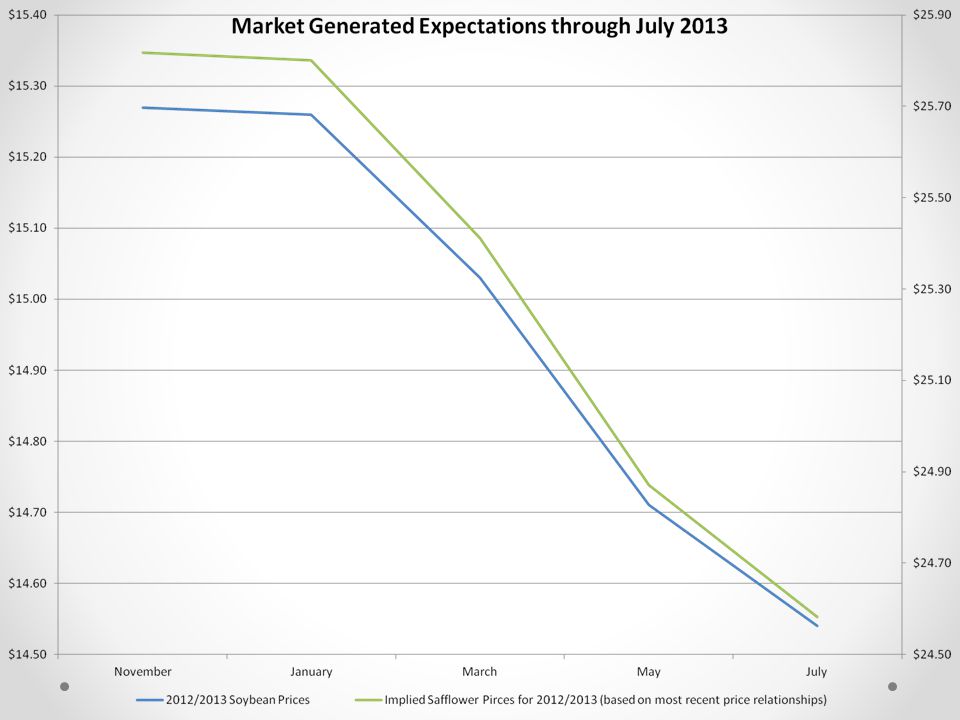

Safflower Prices If we look at safflower prices over the last 11 years or so, Changes in the annual values from year to year have about a 91 percent correlation with soybean price changes. In other words, soybean price changes explain about 91 percent of the variation in sunflower prices.

11

Actual vs. Predicted Safflower Prices

13

Sunflower vs. Safflower Prices

14

Actual vs. Predicted Safflower Prices

20

Proso Millet Prices Comparing millet prices to corn over the last over the last 11 years or so, about 74 percent of the millet price can be explained by corn prices. While this is not as strong as the oilseed price relationships, it still, provides some useful information in thinking about prices this coming season.

25

Important Addition SOMETHING ABOUT WHEAT

26

26 Longer Term Outlook Value of the U.S. dollar Global Economic Activity Additional crop land

27

Total Agricultural Exports (bil $)

")

33

33 Why the Importance of the U.S. Dollar o Prices of traded commodities are often denominated in dollars. o Commodities have historically been inversely related to the value of the dollar – as the dollar falls, commodity prices tend to rise. o Falling dollar boosts purchasing power of foreign buyers of dollar-denominated commodities, thereby increasing demand and putting upward pressure on prices. o U.S. dollar has been trending down since 2002. o Most economists expect U.S. dollar to ease over the longer term, particularly relative to emerging market currencies. o If true, this will put continued upward pressure on a wide range of commodity prices as the dollar declines – INCLUDING THOSE FOR WHICH WE ARE NOT A MAJOR PRODUCER!

35

Agricultural Commodity Prices Expected To Remain High for Next 10 Years … Source: 2011 USDA Baseline projection

36

36 The Global Economic Growth o Global economy emerging from worst recession in decades. Developing countries performed better and growing faster than developed countries. This should continue through 2020. o Global recessions historically result in lower commodity prices – Not this time because of strength in emerging markets. o Consumer incomes are rising and middle class households are expanding rapidly, especially in large emerging markets like China and India. o Logarithmic growth in middle class expected through 2020 – up 104% in developing countries by 2020 vs just 9% for developed countries. o Risk Factor – Sustainable Chinese Growth

37

33 Potential Availability of Uncultivated Land 123 million ha 201 million ha 3 million ha 51 million ha 15 million ha Sub-Saharan Africa 47% M. East & N. Africa 97% E. Europe & C. Asia 86% East & South Asia 22% Latin America & Car. 76% Data Source: World Bank Share of Land With Travel Time to Market < 6 Hours STOLEN FROM Michael J. Dwyer Director of Global Policy Analysis Office of Global Analysis, Foreign Agricultural Service/USDA

38

38 Foreign households w/real PPP incomes greater than $20,000 a year (in millions of households) “Middle Class” Outside the U.S. Expected to Double By 2020 – To 1 Billion Households Worldwide food consumption will be impacted Developing countries Developed countries (ex US) Middle class in developing countries projected to increase 104% by 2020 vs. just 9% in developed countries in 2009 Source: Global Insight’s Global Consumer Markets data as analyzed by OGA ALSO STOLEN

Middle class in developing countries projected to increase 104% by 2020 vs. just 9% in developed countries in 2009 Source: Global Insight’s Global Consumer Markets data as analyzed by OGA ALSO STOLEN.")

39

OUTLOOK SUMMARY We have likely entered a sustained period of higher average prices, coupled with increased volatility. Sources of volatility vary, but international relationships continue to increase in importance relative to overall commodity price discovery. While the short term outlook for U.S. crops is for slightly weaker prices, this is not a long-run expectation. If commodities continue to be priced in U.S. dollars in international markets, then continued deterioration in the dollars value will contribute to higher commodity prices. Think carefully about new ways to contract with business partners.

40

THANK YOU

Similar presentations