Download presentation

Presentation is loading. Please wait.

1

Economic Concepts Related to Appraisals

2

Time Value of Money The basic idea is that a dollar today is worth more than a dollar tomorrow Why? – Consumption – Risk (uncertainty) – Investment – Inflation – Other?

– Investment – Inflation – Other .")

3

Present Value Present value (PV) is the value today of a sum of money to be received in the future This can be the value of an amount at one time period in the future or it can be the value of a stream of payments into the future The PV is determined by discounting, the future value is ‘discounted’ to the present The interest rate used is sometimes referred to as the discount rate

is the value today of a sum of money to be received in the future This can be the value of an amount at one time period in the future or it can be the value of a stream of payments into the future The PV is determined by discounting, the future value is ‘discounted’ to the present The interest rate used is sometimes referred to as the discount rate")

4

Present Value, cont. Lump sum PV = Future value/ (1 + i) n = FV*1/(1+i) n where: – i = the interest or discount rate – n = the time period PV of $8,000 in 10 years at a 4% discount rate – PV = $8000* 1 / (1 +.04) 10 = $8000 *.6756 = $5,405

n = FV*1/(1+i) n where: – i = the interest or discount rate – n = the time period PV of $8,000 in 10 years at a 4% discount rate – PV = $8000* 1 / (1 +.04) 10 = $8000 *.6756 = $5,405.")

5

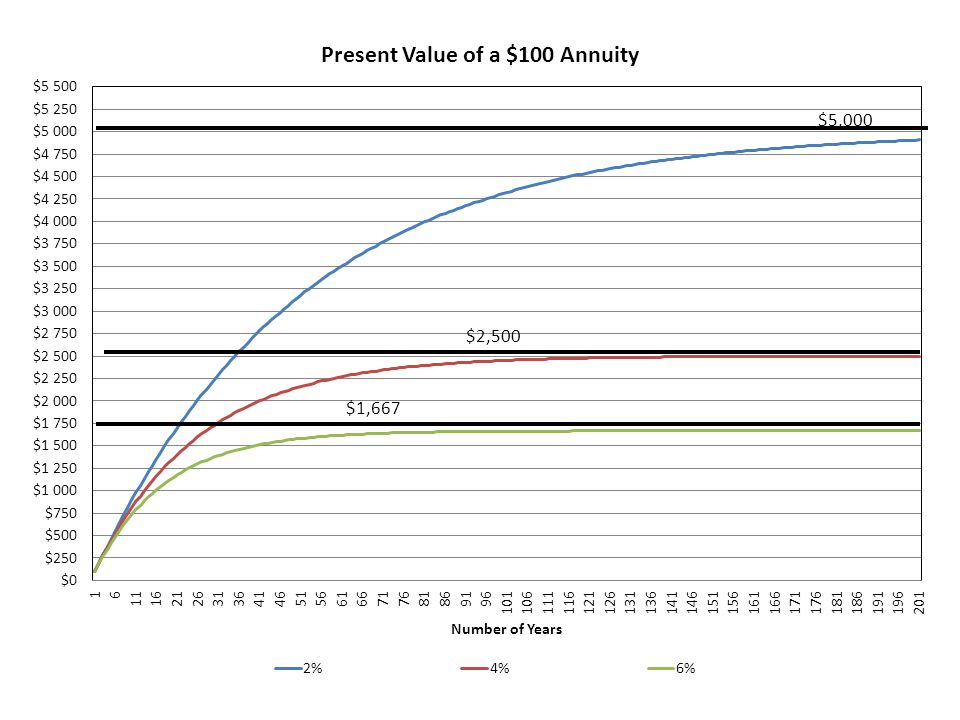

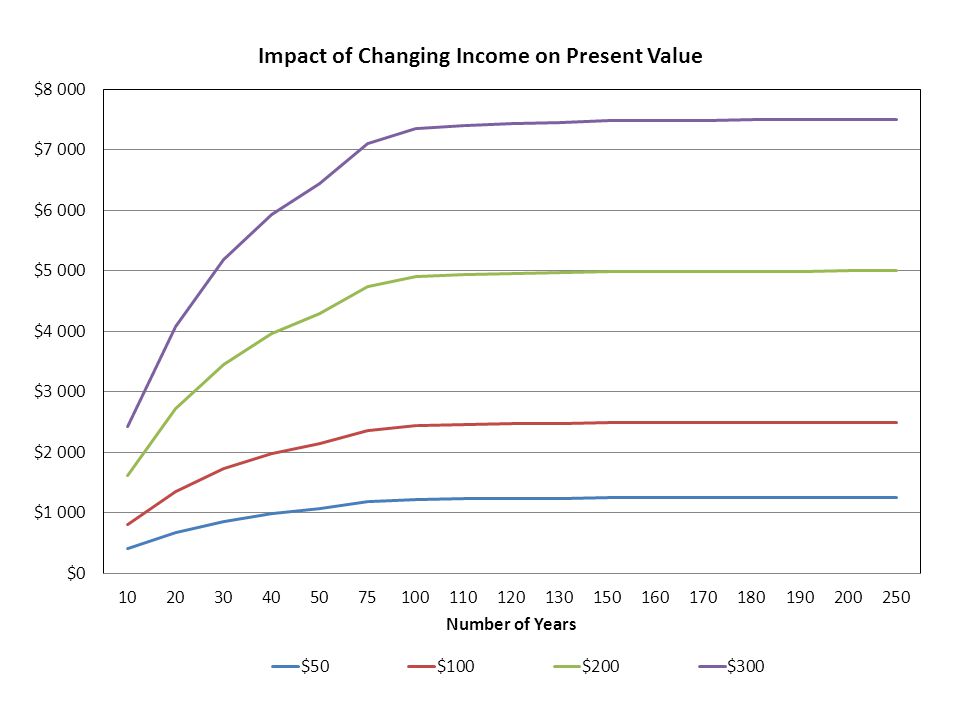

Present Value, cont. PV of an annuity or series of payments over time is: – PV = Payment * (1-(1 + i) -n / i ) Tables have been developed to use for either the present value factor for a lump sum or a series of payments. Excel is very useful If we assume an infinite number of years and equal payments the PV formula reduces to: – PV = Pmt/i

-n / i ) Tables have been developed to use for either the present value factor for a lump sum or a series of payments. Excel is very useful If we assume an infinite number of years and equal payments the PV formula reduces to: – PV = Pmt/i.")

8

Example 1 What is the present value of an annuity of $150 for: – 25 years at 4% $150 * 15.62208 = $2,343 – 25 years at 2% $150 * 19.52346 = $2,929 – 22 years at 6% $150 * 12.04158 = $1,806

9

Example 2 What is the present value of $150 at 6% in perpetuity? – $150/.06 = $2,500 What is the payment used if the present value is $5,064 and the interest rate is 4% – $5,064 = X/.04 = $5,064 *.04 = X X = $203

10

Example 3 You want to know what will have the lowest cost to control erosion, building a dam or changing tillage practices and using cover crops. The discount rate is 4% – Dam costs $5,000 to build, $5 a year to maintain and in 25 years there will need to be major repairs for $1,000. Expected life is 75 years – Cover crop will be $135 a year.

11

Present value Example 3 Dam$5,000 Maintenance $5 * (1-(1+i) -n )/I = 5*23.68041 $ 118 Rebuild $1,000 * 1 / (1+i) n = 1000*.3751 $ 375 $5,493 Cover Crop $135 * 23.68041 =$3,197

-n )/I = 5* $ 118 Rebuild $1,000 * 1 / (1+i) n = 1000*.3751 $ 375 $5,493 Cover Crop $135 * =$3,197")

12

Example 4 What is the value of an orchard if the initial cost of the trees is $1,000 and there is a $60 expense in year 2, $30 expenses in years 3, 4, and 5 and then there is income of $125 for the next 50 years? Use a 6% discount rate. Expenses $1,000 – $60 *.8900 = $53 – $30 *.8396 + 30*.7921 + 30*.7473 = – 25 + 24 + 22 = $71 PV of expenses $1000 + $53 + $71 = $1,124

13

Example 4 Cont Income – PV $125 for 50 years at 6% – $125 * 15.76186 = $1,970 PV of orchard $1,970 - $1,124 - $527 = $319

14

Future Value The future value is the amount of money to be received at some point in the future or it is the amount a present value will grow to when invested at a given interest rate. The present value is discounted but the future value is compounded. Compounding and discounting are the opposite of each other

15

Future Value, cont. FV = PV * (1 + i) n where the variables are the same as before FV of an annuity; – FV = PMT * ((1 + i) n – 1) / i Rule of 72; if you divide 72 by the interest rate you get the approximate time it takes an investment to double

n where the variables are the same as before FV of an annuity; – FV = PMT * ((1 + i) n – 1) / i Rule of 72; if you divide 72 by the interest rate you get the approximate time it takes an investment to double.")

16

Time $ PV $ FV ? PMT FV $ Time $$$$ ? Future Value

17

FV $ Time PV ? $ PMT $$$$ ? $ Time PRESENT VALUE PV

18

Example 1 Land is worth $1,500 today. You expect that it will increase in value by 3% a year. What will be the value of the land in 15 years? $1,500 * 1.5580 = $2,337

19

Example 2 Assume we had a farm that sold for $500, 000 seven years ago. What would we have to sell it for today to earn 6% on the investment? FV of $500,000 today earning 6% for 7 years – $500,000 * 1.5036 = $751,800

20

Example 3 You think you’ll need $30,000 for your child to go to college in 8 years. You deposit $4000 a year into an 5% savings account. How much will you have when they start school? $4,000 * 9.5491 = $38,196 How much should you have saved to just have $30,000? – $30,000 / 9.5491 = $3,142

21

Investment Analysis Investment analysis or capital budgeting is used to determine profitability and/or compare alternatives Investment analysis requires knowing: Initial costs Actual total expenditure not just down payment or list price

22

Investment Analysis, cont. Need to know continued Net cash flow for each time period over the life of the investment Only cash revenues and expenses; DO NOT include depreciation or any financing charges Terminal value (salvage value); For land estimate of the market value when investment is terminated or if assumed to be held indefinitely the terminal value can be ignored

; For land estimate of the market value when investment is terminated or if assumed to be held indefinitely the terminal value can be ignored.")

23

Investment Analysis, cont. 4. Discount rate Opportunity cost of capital, cost of borrowing, weighted average, Risk premium especially when comparing alternatives with different risks Other adjustments to remember when considering a discount rate include; tax differences and inflation Increasing discount rate lowers value of investment

24

Net Present Value Preferred method of evaluation – Also called discounted cash flow method NPV is the sum of the present values for each year’s net cash flow minus the initial cost of the investment NPV = P 1 /(1+i) + P 2 /(1+i) 2 + … + P n /(1+i) n – C Calculations in Excel or from Present Value factor tables

+ P 2 /(1+i) 2 + … + P n /(1+i) n – C Calculations in Excel or from Present Value factor tables")

25

Net Present Value, cont NPV > 0 accept NPV < 0 reject NPV = 0 indifferent NPV > 0 means rate of return higher than the discount rate; C could be higher and investor could still receive the discount rate Discount rate is critical

26

Internal Rate of Return Internal rate of return (IRR) is another technique used to compare investments IRR is the discount rate that makes the NPV just equal 0 0 = (.)-C C = (.) so that the IRR is the i to make C = 0 IRR > cost of capital is profitable, some people only invest if IRR is greater than a certain level Hard to calculate; doesn’t account for size; assumes same rate possible every period

is another technique used to compare investments IRR is the discount rate that makes the NPV just equal 0 0 = (.)-C C = (.) so that the IRR is the i to make C = 0 IRR > cost of capital is profitable, some people only invest if IRR is greater than a certain level Hard to calculate; doesn’t account for size; assumes same rate possible every period")

27

Financial Feasibility IRR and NPV don’t consider the financing except through the discount rate It is important to think about financing when considering an investment Financing can affect the cash flows, especially in the early years; some cases with negative cash flows may not even be possible Something can be profitable but not feasible because of the cash flow associated with financing

28

Example 1 Which would you prefer, an investment A that returns $3,000 a year for 5 years or investment B that returns – Year 1$1,000 – Year 2$2,000 – Year 3$3,000 – Year 4$4,000 – Year 5$6,000 Both Cost $10,000 and use a 6% discount rate

29

Example 1 cont Investment A – $3,000 *.9434=$2,830 – $3,000 *.8900=$2,670 – $3,000 *.8396=$2,519 – $3,000 *.7921=$2,376 – $3,000 *.7473=$2,242 – Total $12,637 – Less cost $10,000 NET PRESENT VALUE $ 2,637

30

Investment B – $1,000 *.9434= $943 – $2,000*.8900= $1,780 – $3,000*.8396= $2,519 – $4,000*.7921= $3,168 – $6,000*.7473= $4,484 – Total $12,894 – Less costs $10,000 – NPV $ 2,894

31

Investment ANPV$2,637 Investment BNPV $2,894 Both earn more than 6% Could afford to pay more for either investment What if there had been a terminal or salvage value

32

Other thoughts Discount rate; – Inflation adjustments Adjust if some costs and/or revenues will move differently over time; Otherwise NPV will be the same Inflation premium should be ADDED to the real discount rate to obtain the adjusted rate – Risk adjustments Adjust for risk if there is a difference in the perceived risks of the investment Risk premium so you add to the real discount rate because you need a higher rate of return

33

Other Economic Considerations with Land There is an intrinsic value to land; people just want to own it especially a particular parcel of land There is a social value to land; land is the basis for many societies and for the wealth of a society; How we treat the land says who we are Why people own land is not always as an investment; legacy; security, retirement Don’t own land to make money but own land to own it

Similar presentations