Download presentation

Presentation is loading. Please wait.

1

Trends in R&D Investments Global ICT Companies 2007 to 2011 Alain Stekke DG INFSO Economic and Statistical Unit Georg Kelm DG INFSO Nanoelectronics Unit

3

R&D Data 2010 Digital Competitiveness Report –Eurostat BERD + Predict Report (IPTS) + EU KLEMS 2011 Digital Agenda Scoreboard –No new Eurostat and EU KLEMS data => R&D expenses as reported by companies in their quarterly and annual reports

+ EU KLEMS 2011 Digital Agenda Scoreboard –No new Eurostat and EU KLEMS data => R&D expenses as reported by companies in their quarterly and annual reports")

4

Firm level analysis "Nations do not trade; it is firms that trade. This simple truth makes it clear that understanding the firm-level facts is essential to good policy making in Europe." The happy few: the internationalisation of European firms. New facts based on firm-level evidence, Thierry Mayer and Gianmarco I.P. Ottaviano, "Geography matters for R&D" given the strong link between R&D and growth driven by ‘knowledge spillovers’ between firms located close to each other Why geography matters for R&D, John Van Reenen The European Union’s business research and development deficit relative to the United States can be almost entirely accounted for by the EU having fewer young leading innovators" Europe's missing yollies, Reinhilde Veugelers and Michele Cincera

6

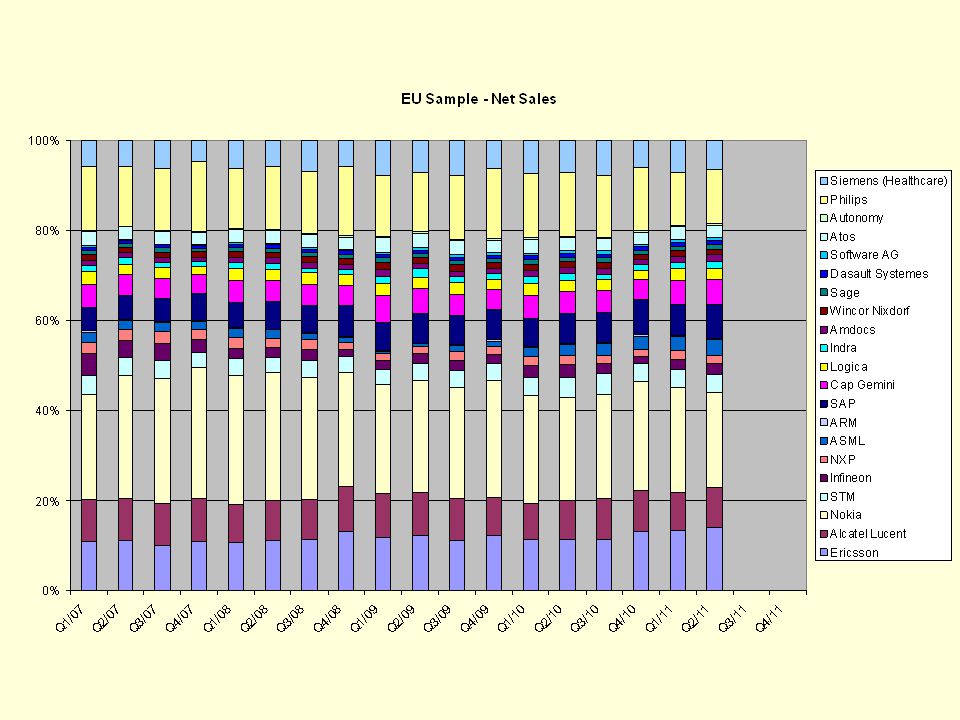

€28bn €27bn

7

Impact of the economic crises Post Lehman Brother bankruptcy recession

8

Q4/2008 & Q1/2009 Panic

13

R&D is pro-cyclical

19

2007 – 2011 is about innovation Global Internet platforms / Social networks / Smartphones / Tablets / Cloud computing / LTE and Fiber –Demand for 24/7 internet connectivity –Mobility –Software “Renaissance” (apps) –More e-content (publishing) Industry shake up semiconductors, telecom equipment & devices, software and publishing industry, telecom operators etc. Policy digital agenda Net neutrality, broadband deployment, cloud computing regulation, privacy,

20

2007 – 2011 is about innovation Innovations of a magnitude (probably) never experienced before Truly disruptive –Big winners (and losers) –Bankruptcies/ Exits / Entries / Acquisitions –Goodwill and intangible asset impairments –Wave of patent litigation & gold rush for patents Very different from an economic downturn –Where you go down and up together

never experienced before Truly disruptive –Big winners (and losers) –Bankruptcies/ Exits / Entries / Acquisitions –Goodwill and intangible asset impairments –Wave of patent litigation & gold rush for patents Very different from an economic downturn –Where you go down and up together")

21

US versus EU US –Extending the ICT universe Devices + content + platform –Re-integrating software and hardware Oracle/Sun, HP/EDS, Dell/Perot EU –Technological leadership –Silicon driven –Extending outside rather inside ICT

22

The European Semiconductor Industry – Application Driven Largest market shares in application fields as: Automotive, Industrial, Security, Communication, Medical Silicon Technologies used to fabricate such devices: - From 0,32µm down to 40 nm CMOS, both bulk CMOS and FD SOI - From 0,16 µm Smart power to IGBT high power devices - From 77 GHz BiCMOS RF to - CMOS cameras (65 nm CMOS) and to MEMS based sensors Both large IC makers as STM, Infineon, NXP and GlobalFoundries as well as smaller European foundries as X-fab, L-foundry or Elmos are competitive in the market place with high volume production or specialised products for niche markets respectively. Value chain: It is important to note that the critical elements of the supply chain are still present in Europe; special strenghts in Lithography, Metrology and Materials.

23

European S/C Component Suppliers in Global Context A EU IC suppliers are competitive !!! Courtesy STM

24

Leading edge NanoE and PowerE Technology for your Car Courtesy STM Advanced nanoE components down to 40 nm CMOS processors

25

Source: IC-Insights, 01/2008 Reduction of cost / transistor by factor of 1 million over past 40 years

26

The other side of “ Moore ’ s Law ” after IHS iSuppli 2011 16/14 nm12/11 nm ?????? ? TSMC Globalfoundries STMicroelectronics Intel Samsung 22/20 nm

27

Outlook The global technology race does not stop. There is visibility for another decade of ever smaller features (3nm!), larger Si wafers (450 mm), both boosting functionality & performance and keeping cost per function low. In the long run Europe cannot afford to be out of this race as the system know-how is more and more integrated in the chip

, larger Si wafers (450 mm), both boosting functionality & performance and keeping cost per function low. In the long run Europe cannot afford to be out of this race as the system know-how is more and more integrated in the chip.")

28

Outlook The global technology race does not stop. There is visibility for another decade of ever smaller features (3nm!), larger Si wafers (450 mm), both boosting functionality & performance and keeping cost per function low. In the long run Europe cannot afford to be out of this race as the system know-how is more and more integrated in the chip

, larger Si wafers (450 mm), both boosting functionality & performance and keeping cost per function low. In the long run Europe cannot afford to be out of this race as the system know-how is more and more integrated in the chip.")

Similar presentations