Download presentation

Presentation is loading. Please wait.

1

Borrowing, Lending, and Investing

Chapter 3 Borrowing, Lending, and Investing

2

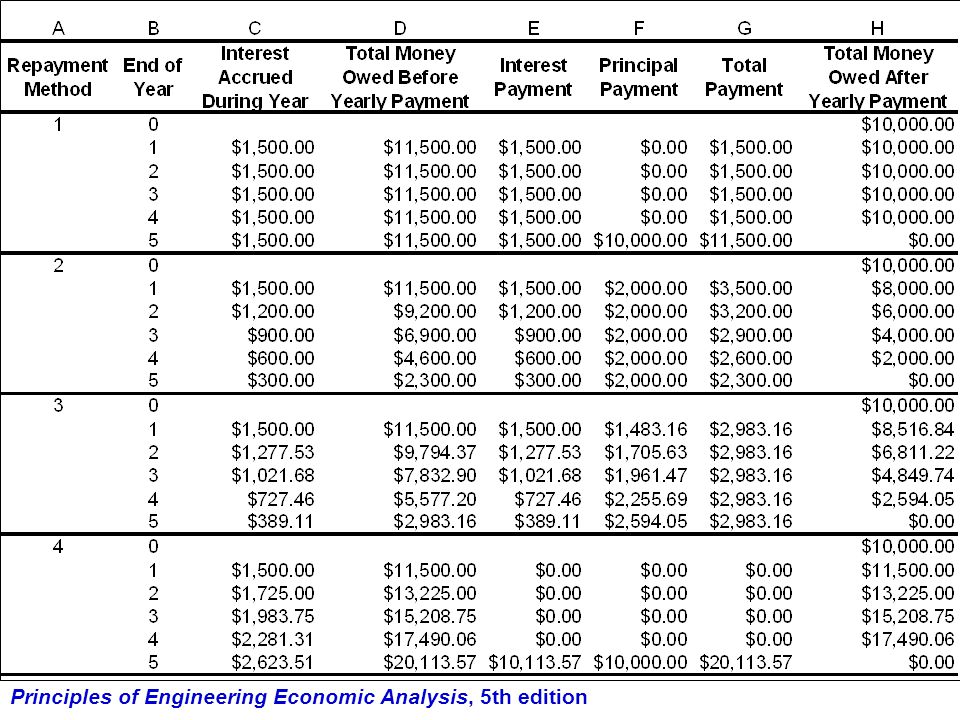

Four Loan Repayment Methods

Pay interest each period, but make no principal payment until the end of the loan period Make equal end-of-period principal payments and pay interest each period on the unpaid balance at the beginning of the period Make equal end-of-period payments over the loan period Make no payment until the end of the loan period

3

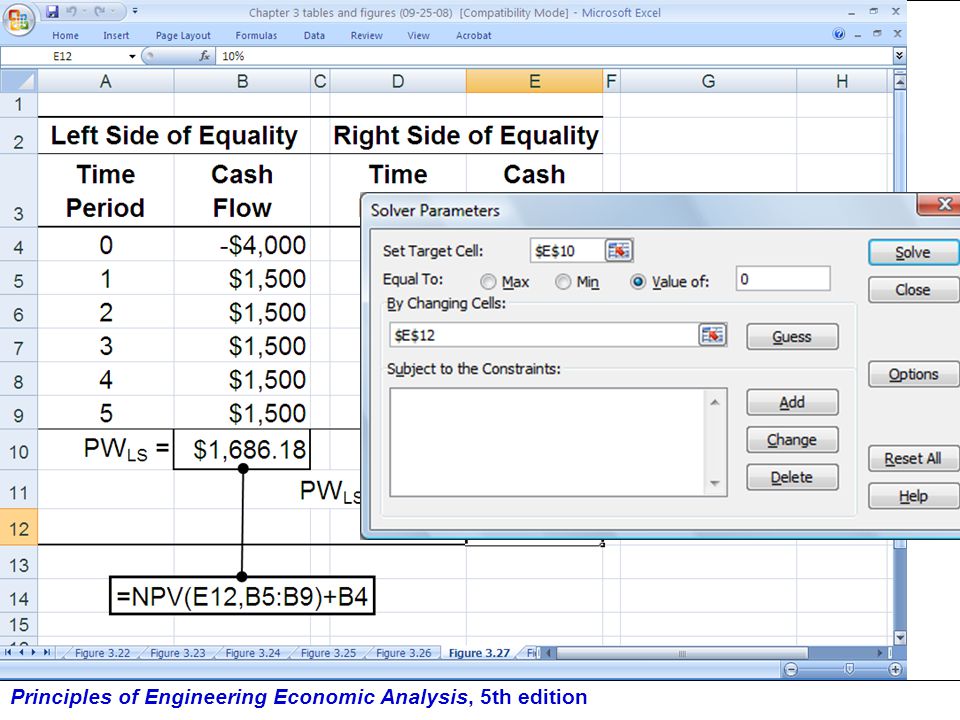

Example 3.1 An owner of a small business borrows $10,000 at 15% annual compound interest. The loan is to be repaid over a 5-year period using one of the 4 repayment methods. Method 1: pay $1,500 interest each year and pay off the principal of $10,000 at the end of 5 years Method 2: make five $2,000 principal payments, plus the interest on the unpaid balance, i.e., payments of $3,500, $3,200, $2,900, $2,600, and $2,300 Method 3: make five annual payments of $10,000(A|P 15%,5) = $2,983.16 Method 4: after 5 years make a single payment of $10,000(F|P 15%,5) = $20,113.57

= $2, Method 4: after 5 years make a single payment of. $10,000(F|P 15%,5) = $20,")

4

CFDs for the Four Repayment Methods

6

Example 3.2 If the borrower’s TVOM is equal to 15%, then the business owner would be indifferent regarding the loan repayment plan. However, suppose the lender’s interest rate is 10%. Which repayment method would the borrower prefer? PW(loan payments): PW1(15%) = $10,000-$10,000(0.10)(P|A 15%,5)-$10,000(P|F 15%,5) PW1(15%) = $ PW2(15%) = $10,000-$3000(P|A 15%,5)+$200(P|G 15%,5) PW2(15%) = $ PW3(15%) = $10,000(A|P 10%,5)(P|A 15%,5) PW3(15%) = $ PW4(15%) = $10,000(F|P 10%,5)(P|F 15%,5) PW4(15%) = $ Method 4 has the greatest present worth of loan payments. Therefore, it would be preferred. Notice: PW > $0 for all methods

: PW1(15%) = $10,000-$10,000(0.10)(P|A 15%,5)-$10,000(P|F 15%,5) PW1(15%) = $ PW2(15%) = $10,000-$3000(P|A 15%,5)+$200(P|G 15%,5) PW2(15%) = $ PW3(15%) = $10,000(A|P 10%,5)(P|A 15%,5) PW3(15%) = $ PW4(15%) = $10,000(F|P 10%,5)(P|F 15%,5) PW4(15%) = $ Method 4 has the greatest present worth of loan payments. Therefore, it would be preferred. Notice: PW > $0 for all methods.")

7

Example 3.2 (Continued) Now, suppose the lender’s interest rate is equal to 20%. Which plan would the borrower prefer? PW(loan payments): PW1(15%) = $10,000-$10,000(0.20)(P|A 15%,5)-$10,000(P|F 15%,5) PW1(15%) = -$ PW2(15%) = $10,000-$4000(P|A 15%,5)+$400(P|G 15%,5) PW2(15%) = -$ PW3(15%) = $10,000(A|P 20%,5)(P|A 15%,5) PW3(15%) = -$ PW4(15%) = $10,000(F|P 20%,5)(P|F 15%,5) PW4(15%) = -$ Method 2 has the greatest present worth (albeit negative) of loan payments. Therefore, it would be preferred. What can we conclude from this example? Notice: PW < $0 for all methods

: PW1(15%) = $10,000-$10,000(0.20)(P|A 15%,5)-$10,000(P|F 15%,5) PW1(15%) = -$ PW2(15%) = $10,000-$4000(P|A 15%,5)+$400(P|G 15%,5) PW2(15%) = -$ PW3(15%) = $10,000(A|P 20%,5)(P|A 15%,5) PW3(15%) = -$ PW4(15%) = $10,000(F|P 20%,5)(P|F 15%,5) PW4(15%) = -$ Method 2 has the greatest present worth (albeit negative) of loan payments. Therefore, it would be preferred. What can we conclude from this example Notice: PW < $0 for all methods.")

8

Borrower’s Present Worth of Loan Payments

9

Borrower’s TVOM = 15%

10

Borrower’s Preferred Payment Method

Method 2 preferred if borrower’s TVOM < lender’s interest rate Method 4 preferred if borrower’s TVOM > lender’s interest rate

11

Real Estate Investments

In the current environment (post-subprime lending debacle),real estate investments are not as “attractive” as they once were. But, people still need housing. Let’s understand better the pluses and minuses of real estate investment.

,real estate investments are not as attractive as they once were. But, people still need housing. Let’s understand better the pluses and minuses of real estate investment.")

12

“Why Should I Purchase a House? Why not Rent?”

your house payments allow you to accumulate equity (ownership) in the property—rent does not; the interest you pay in purchasing a house can be deducted from your taxable income—rent cannot; and if the value of the house increases over time, you are the beneficiary of that increase—renters do not share in the benefits of an increase in the value of the property.

in the property—rent does not; the interest you pay in purchasing a house can be deducted from your taxable income—rent cannot; and. if the value of the house increases over time, you are the beneficiary of that increase—renters do not share in the benefits of an increase in the value of the property.")

13

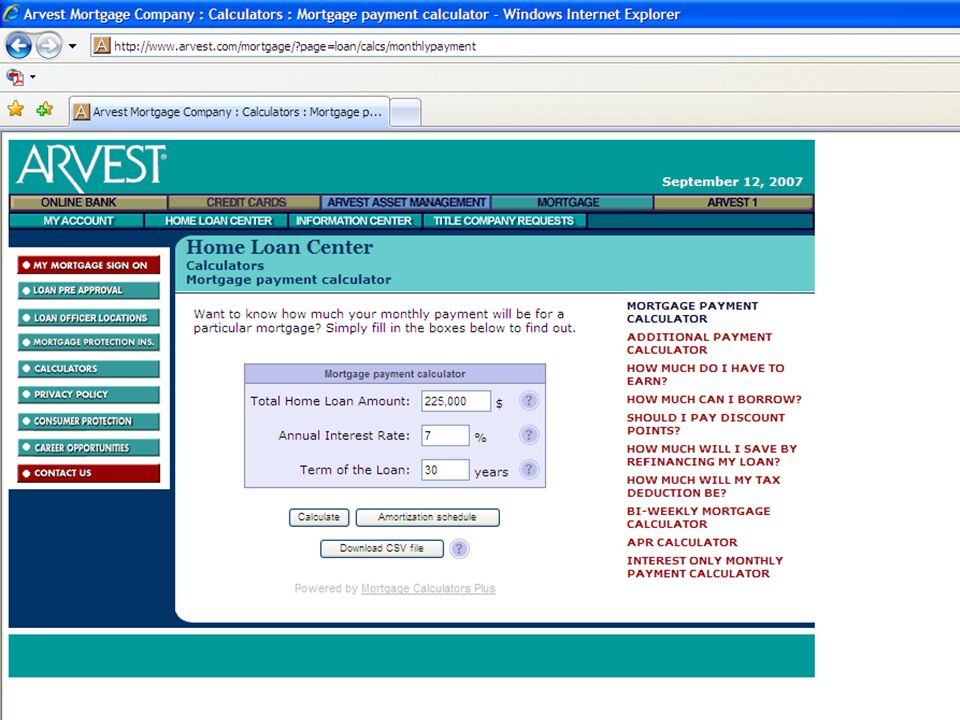

A Wide Variety of Mortgage Options Exist

Personnel at a Bank of America branch office provided detailed rates for the following 14 mortgage alternatives: 30-year conventional fixed rate loan; 15-year conventional fixed rate loan; 30-year Federal Housing Authority (FHA) mortgage; 15-year FHA mortgage; 30-year Veterans Authority (VA) mortgage; 15-year VA mortgage; 30-year ARM, adjustable every 6 months; 25-year ARM, adjustable every 6 months; 30-year ARM, adjustable every 12 months; 3/1 30-year ARM, adjustable every 12 months; a 5/1 30-year ARM, adjustable every 12 months; 7/1 30-year ARM, adjustable every 12 months; 30-year balloon loan; and 40-year balloon loan.

mortgage; 15-year FHA mortgage; 30-year Veterans Authority (VA) mortgage; 15-year VA mortgage; 30-year ARM, adjustable every 6 months; 25-year ARM, adjustable every 6 months; 30-year ARM, adjustable every 12 months; 3/1 30-year ARM, adjustable every 12 months; a 5/1 30-year ARM, adjustable every 12 months; 7/1 30-year ARM, adjustable every 12 months; 30-year balloon loan; and. 40-year balloon loan.")

14

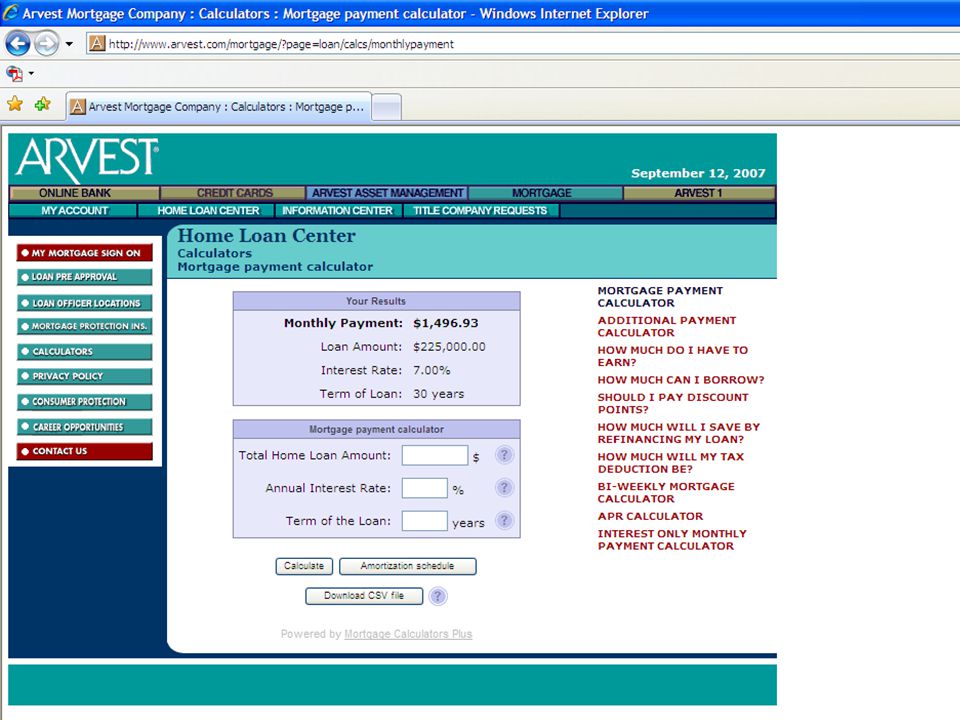

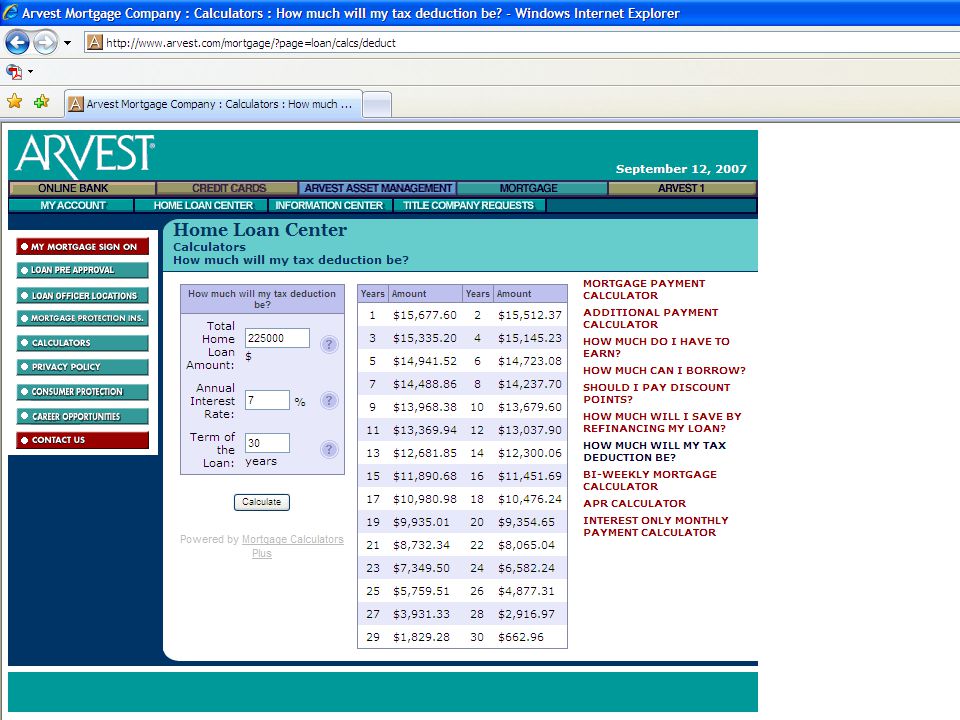

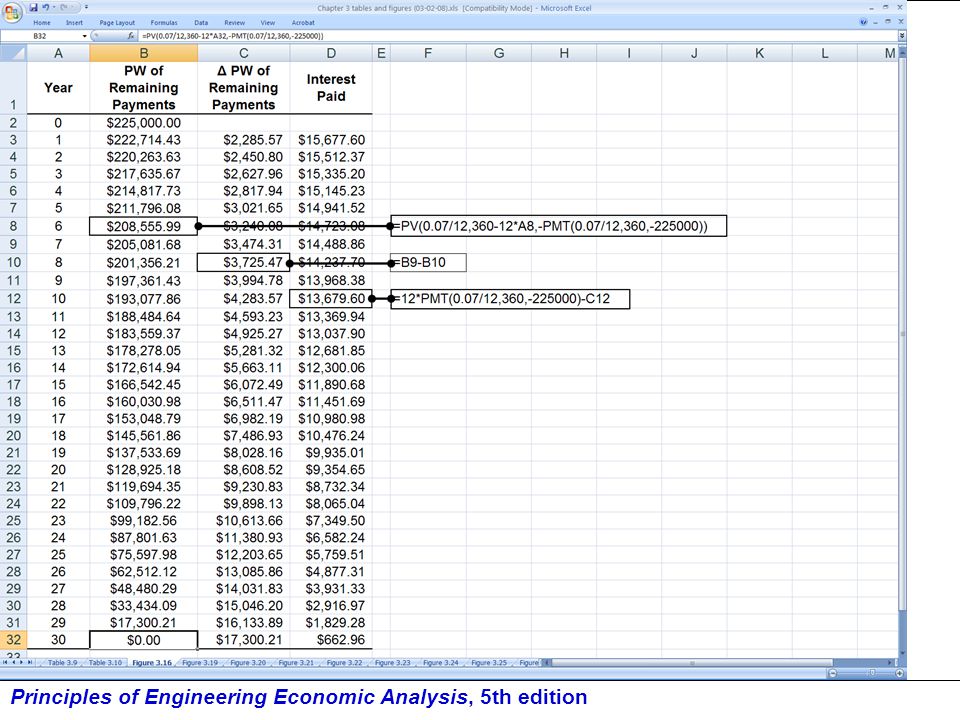

Example 3.3 Adriana agreed to pay $250,000 for a house. She made a $25,000 down payment and financed the balance using a 30-year, 7% per annum compounded monthly conventional loan. How much were her monthly payments? If she sold the house for $300,000 after 5 years, how much equity did she have in the house? A = $225,000(A|P 7/12%,360) =PMT(0.07/12,360, ) = $ P =PV(0.07/12,300,-PMT(0.07/12,360, )) = $211,796.08 Equity = $300, $211,796.08 = $88,203.92 ($13, is from loan payments) Remember this number

=PMT(0.07/12,360, ) = $ P =PV(0.07/12,300,-PMT(0.07/12,360, )) = $211, Equity = $300, $211, = $88, ($13, is from loan payments) Remember this number.")

18

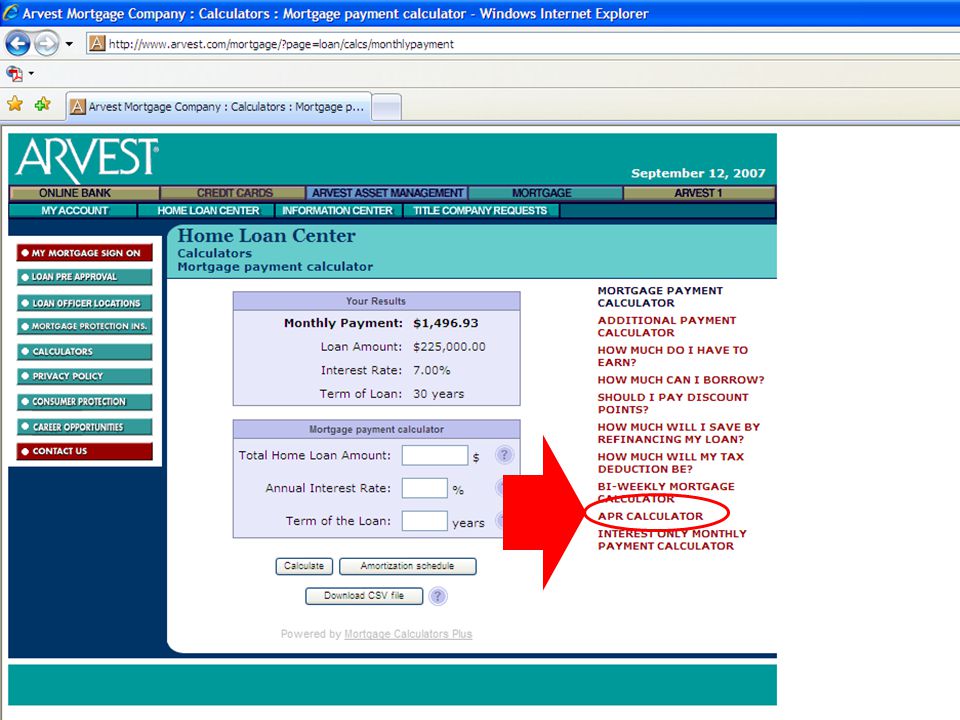

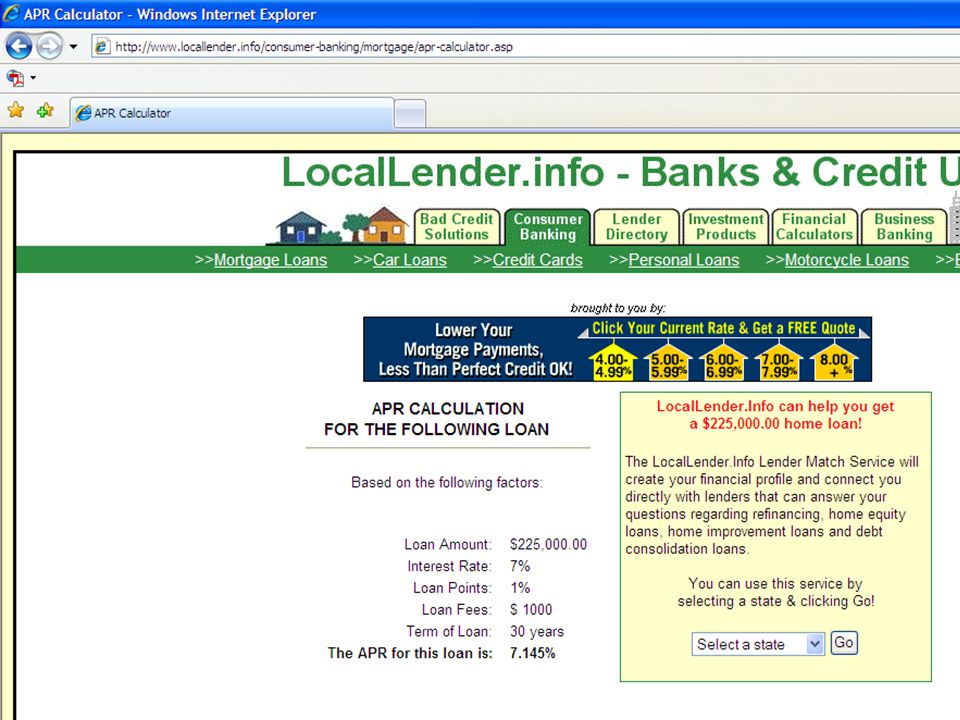

What Is the APR? “A document called the Truth in Lending Disclosure Statement will show you the ‘Annual Percentage Rate’ (‘APR’) and other payment information for the loan you have applied for. The APR takes into account not only the interest rate, but also the points, mortgage broker fees and certain other fees that you have to pay. Ask for the APR before you apply to help you shop for the loan that is best for you. Also ask if your loan will have a charge or fee for paying all or part of the loan before payment is due (‘prepayment penalty’). You may be able to negotiate the terms of the prepayment penalty.”2 2Buying Your Home: Settlement Costs & Helpful Information, U.S. Department of Housing and Urban Development, Office of Housing—Federal Housing Commission, Item 1583 (9706), to order call:

and other payment information for the loan you have applied for. The APR takes into account not only the interest rate, but also the points, mortgage broker fees and certain other fees that you have to pay. Ask for the APR before you apply to help you shop for the loan that is best for you. Also ask if your loan will have a charge or fee for paying all or part of the loan before payment is due (‘prepayment penalty’). You may be able to negotiate the terms of the prepayment penalty. 2. 2Buying Your Home: Settlement Costs & Helpful Information, U.S. Department of Housing and Urban Development, Office of Housing—Federal Housing Commission, Item 1583 (9706), to order call:")

19

Calculating APR Values

Notation n = number of monthly payments to be made i = monthly interest rate P = amount borrowed co = closing costs, other than “points” p1 = points applied to the amount borrowed p2 = points applied to “other” closing costs C = closing costs, including points and “other” closing costs = p1 P + (1 + p2)co Asub = payment, excluding closing costs =PMT(i%,n,-P) (3.1) Aadd = payment, including closing costs =PMT(i%,n,-(P+C)) (3.2)

co. Asub = payment, excluding closing costs. =PMT(i%,n,-P) (3.1) Aadd = payment, including closing costs. =PMT(i%,n,-(P+C)) (3.2)")

20

APR Formulas APRsub = annual percentage rate with the subtractive approach APRadd = annual percentage rate with the additive approach APRsub =RATE(n,-Asub,P-C)* (3.3) APRadd =RATE(n,-Aadd,P)* (3.4)

*12 (3.3) APRadd =RATE(n,-Aadd,P)*12 (3.4)")

21

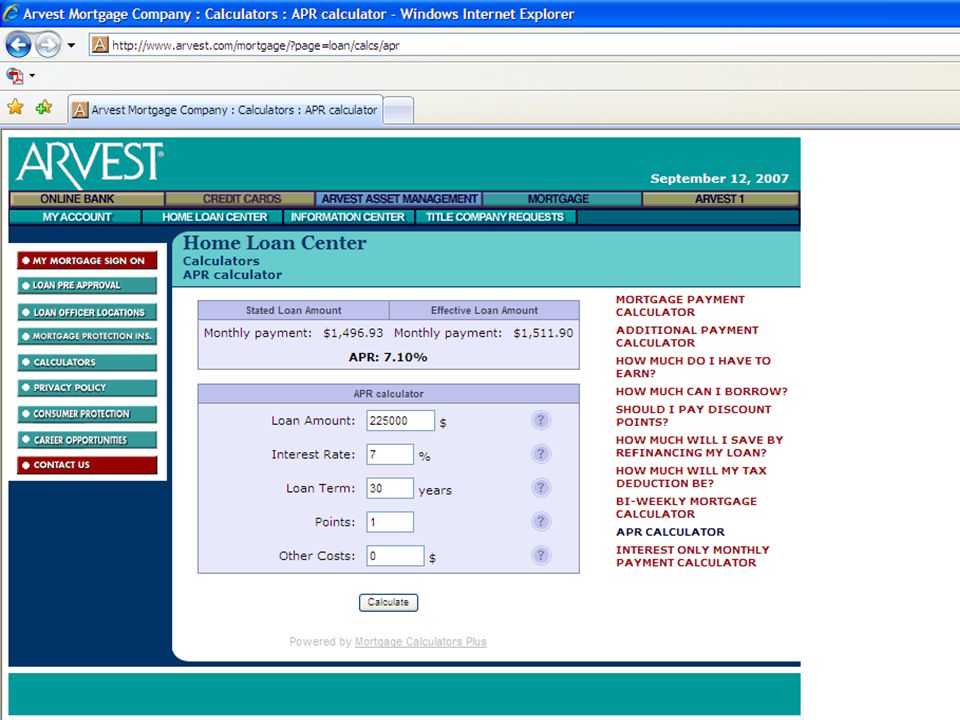

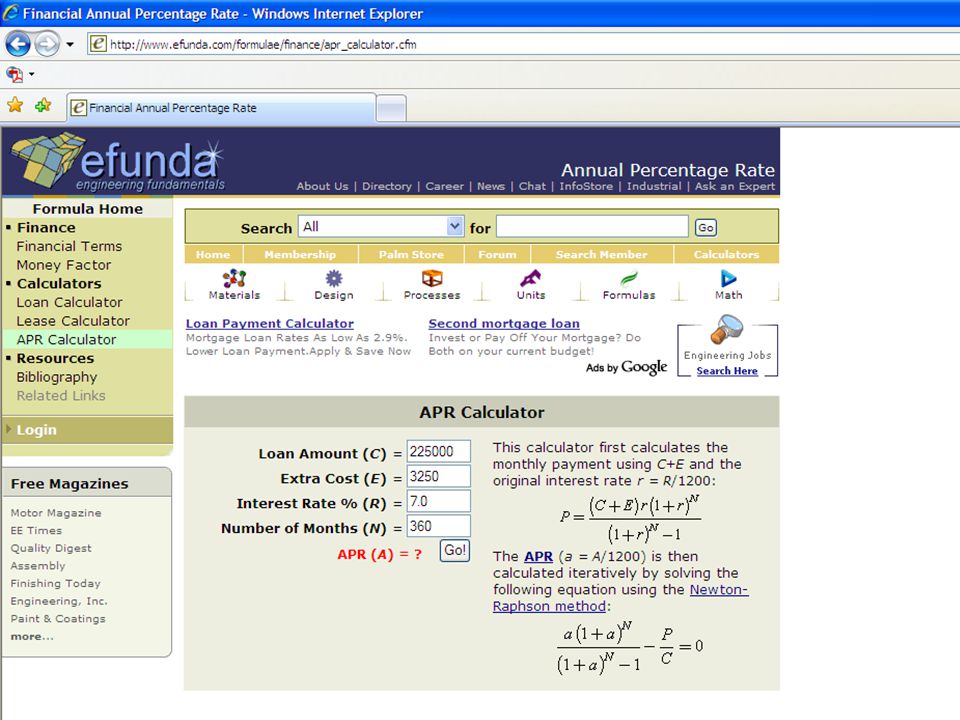

Example 3.4 Suppose Adriana has to pay 1 point to the lender at closing. If she finances the closing costs, what will be her monthly payment, her APR, and her ieff? A = $225,000(1.01)(A|P 7/12%,360) =PMT(0.07/12,360, *1.01) = $ C = 0.01($225,000) = $2250 P – C = $225,000 - $2250 = $222,750 A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,222750)*12 = 7.10% ieff =(1+RATE(360, ,225000))^12–1 = 7.33%1 or ieff =(1+RATE(360, ,222250))^12–1 = 7.36%2 1closing costs are financed 2closing costs are paid at closing, instead of financed

(A|P 7/12%,360) =PMT(0.07/12,360, *1.01) = $ C = 0.01($225,000) = $2250. P – C = $225,000 - $2250 = $222,750. A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,222750)*12 = 7.10% ieff =(1+RATE(360, ,225000))^12–1 = 7.33%1 or. ieff =(1+RATE(360, ,222250))^12–1 = 7.36%2. 1closing costs are financed. 2closing costs are paid at closing, instead of financed.")

23

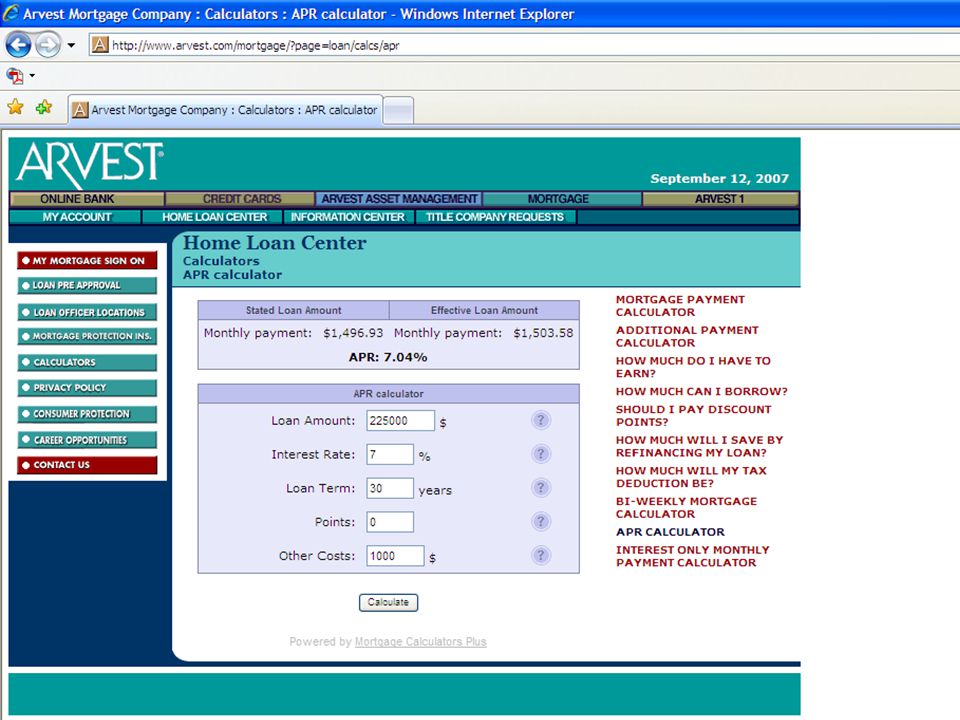

Example 3.5 Now, suppose Adriana has to pay $1000 in closing costs, but no points. If she finances the closing costs, what will be her monthly payment, her APR, and her ieff? A = $226,000(A|P 7/12%,360) =PMT(0.07/12,360, ) = $ C = $1000 P – C = $225,000 - $1000 = $224,000 A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,224000)*12 = 7.04% ieff =(1+RATE(360, ,225000))^12–1 = %1 or ieff =(1+RATE(360, ,224000))^12–1 = %2 1closing costs are financed 2closing costs are paid at closing, instead of financed

=PMT(0.07/12,360, ) = $ C = $1000. P – C = $225,000 - $1000 = $224,000. A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,224000)*12 = 7.04% ieff =(1+RATE(360, ,225000))^12–1 = %1 or. ieff =(1+RATE(360, ,224000))^12–1 = %2. 1closing costs are financed. 2closing costs are paid at closing, instead of financed.")

25

Example 3.6 Next, suppose Adriana has to pay $1000 plus 1 point in closing costs. If, for APR purposes, the 1 pt. does not apply to the other closing costs, what will be her monthly payment, her APR, and her ieff? A = [$225,000(1.01) + $1000](A|P 7/12%,360) =PMT(0.07/12,360, ) = $ C = 0.01($225,000) + $1000 = $3250 P – C = $225,000 - $3250 = $221,750 A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,221750)*12 = % ieff =(1+RATE(360, ,225000))^12–1 = %1 or ieff =(1+RATE(360, ,221750))^12–1 = %2 1closing costs are financed 2closing costs are paid at closing, instead of financed

+ $1000](A|P 7/12%,360) =PMT(0.07/12,360, ) = $ C = 0.01($225,000) + $1000 = $3250. P – C = $225,000 - $3250 = $221,750. A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,221750)*12 = % ieff =(1+RATE(360, ,225000))^12–1 = %1 or ieff =(1+RATE(360, ,221750))^12–1 = %2. 1closing costs are financed. 2closing costs are paid at closing, instead of financed.")

26

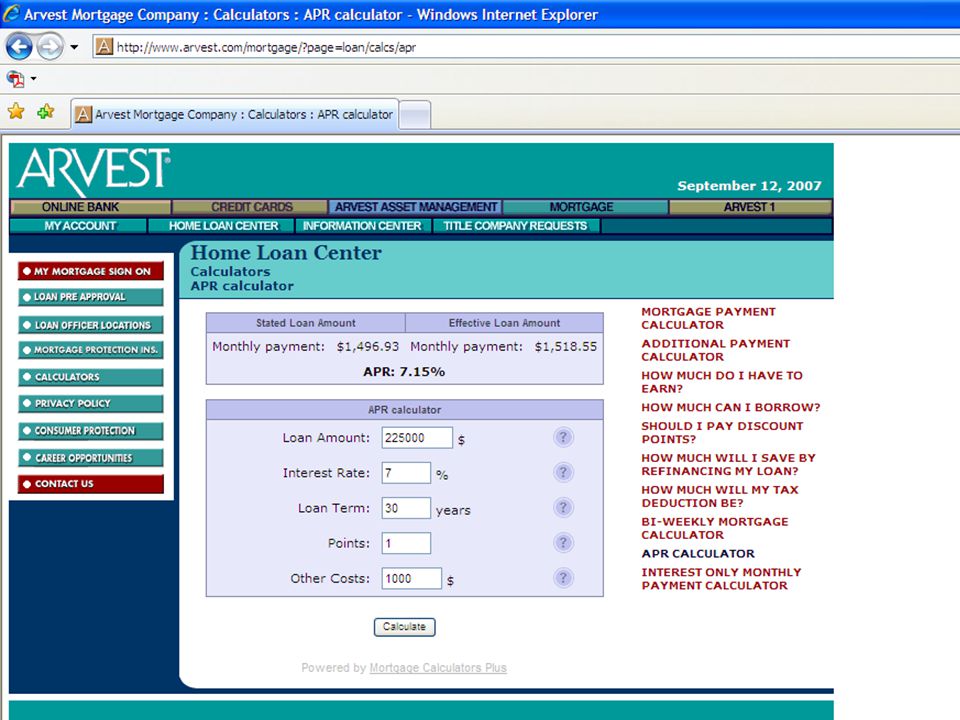

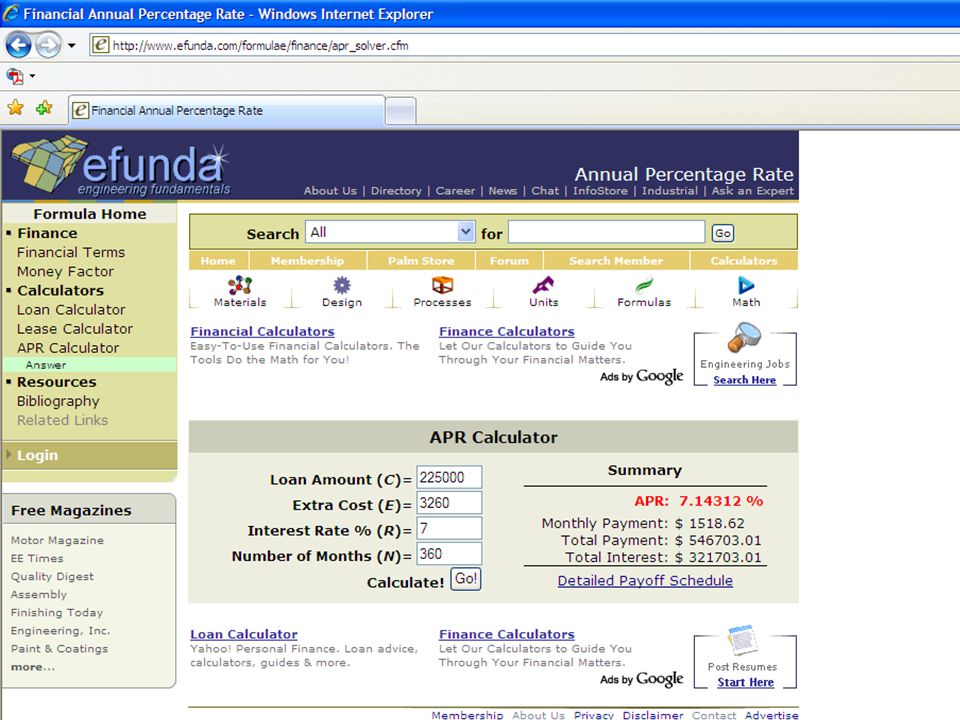

Example 3.6 (continued) Now, suppose the 1 point applies to the other closing costs of $1000. What will be Adriana’s monthly payment, her APR, and her ieff? A = 1.01($225,000 + $1000)(A|P 7/12%,360) =PMT(0.07/12,360, ) = $ C = 0.01($225,000) ($1000) = $3260 P – C = $225,000 - $3260 = $221,740 A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,221740)*12 = %* ieff =(1+RATE(360, ,225000))^12–1 = %1 or ieff =(1+RATE(360, ,221740))^12–1 = %2 *rounds off to 7.15%; perhaps the Arvest APR calculator assumes p1 = p2 = 1% 1closing costs are financed 2closing costs are paid at closing, instead of financed

(A|P 7/12%,360) =PMT(0.07/12,360, ) = $ C = 0.01($225,000) ($1000) = $3260. P – C = $225,000 - $3260 = $221,740. A =PMT(0.07/12,360, ) = $ APRsub =RATE(360, ,221740)*12 = %* ieff =(1+RATE(360, ,225000))^12–1 = %1. or ieff =(1+RATE(360, ,221740))^12–1 = %2. *rounds off to 7.15%; perhaps the Arvest APR calculator assumes p1 = p2 = 1% 1closing costs are financed. 2closing costs are paid at closing, instead of financed.")

30

Example 3.6 (Continued) Now, consider the additive approach. Consider the case of 1 pt. and no other closing costs. The APR will be P = $225,000 C = 0.01($225,000) = $2250 P + C = $225,000 + $2250 = $227,250 APRadd =RATE(360,-PMT(0.07/12,360, ),225000)*12 = % Next, consider the case of 1 pt. and $1000 of other closing costs, with the 1 pt counting only against the amount borrowed C = 0.01($225,000) + $1000 = $3250 P + C = $225,000 + $3250 = $228,250 APRadd =RATE(360,-PMT(0.07/12,360,28250),225000)*12 = %

= $2250. P + C = $225,000 + $2250 = $227,250. APRadd =RATE(360,-PMT(0.07/12,360, ),225000)*12. = % Next, consider the case of 1 pt. and $1000 of other closing costs, with the 1 pt counting only against the amount borrowed. C = 0.01($225,000) + $1000 = $3250. P + C = $225,000 + $3250 = $228,250. APRadd =RATE(360,-PMT(0.07/12,360,28250),225000)*12. = %")

33

Example 3.6 (Continued) We now consider the additive approach with 1 pt, $1000 in other closing costs, and the 1 pt counting against the $1000 closing cost. C = 0.01($225,000) ($1000) = $3260 P + C = $225,000 + $3260 = $228,260 APRadd =RATE(360,-PMT(0.07/12,360, ),225000)*12 = %

($1000) = $3260. P + C = $225,000 + $3260 = $228,260. APRadd =RATE(360,-PMT(0.07/12,360, ),225000)*12. = %")

35

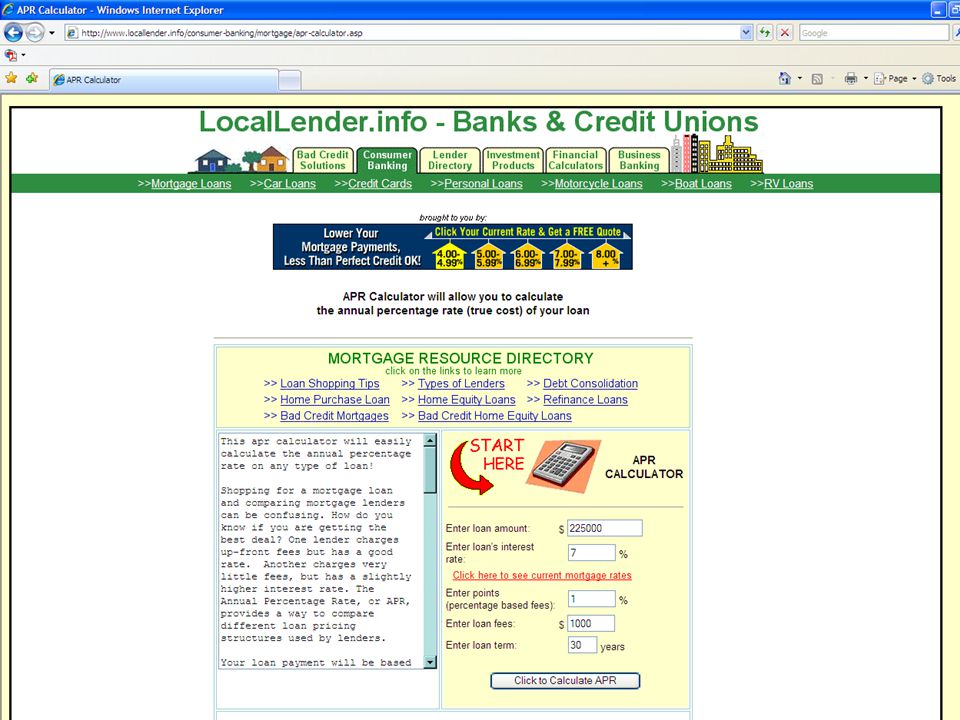

Example 3.7 Finally, suppose Adriana has to pay points plus other administrative costs. The APR is 7.095%. Excluding closing costs, her monthly payment is $6.65 per $1000 borrowed. How much were her “other administrative costs”? BASE =PV( /12,360,-6.65)*225000/1000 = $222,757.40 Therefore, administrative costs plus “points” equals the difference in $225, and $222,757.40, or $ Since “points” on a $225, loan equals $353.25, the administrative costs total $

*225000/1000. = $222, Therefore, administrative costs plus points equals the difference in $225, and $222,757.40, or $ Since points on a $225, loan equals $353.25, the administrative costs total $")

36

Example 3.8 A couple is purchasing a $400,000 house with a $50,000 down payment Their mortgage options are: 1) 30-yr. 7% fixed rate, with points plus $1000 closing costs; 2) 30-yr ARM, 6.5%, with maximum increase of 100 basis points per year and no more than 500 basis points over the 7-year period; plus points and $850 other closing costs; and 3) 30-year balloon loan, with 6.1% annual nominal interest, points, and $7500 other closing costs Which should they choose if their nominal annual TVOM is 10% and they plan to sell the house in 5 years?

30-yr. 7% fixed rate, with points plus $1000 closing costs; 2) 30-yr ARM, 6.5%, with maximum increase of 100 basis points per year and no more than 500 basis points over the 7-year period; plus points and $850 other closing costs; and. 3) 30-year balloon loan, with 6.1% annual nominal interest, points, and $7500 other closing costs. Which should they choose if their nominal annual TVOM is 10% and they plan to sell the house in 5 years")

37

Solution to Example 3.8 Step 1: calculate the monthly payments for each scenario 1) 30-yr. 7% conventional loan: A = [$350,000( ) + $1000](A|P 7/12%,360) =PMT(.07/12,360,350000* ) = $ 2) 30-yr ARM, 6.5%: 1st year payment A = [$350,000(1.0128) + $850](A|P 6.5/12%,360) =PMT(.065/12,360, * ) = $ 3) 30-year balloon loan A = (0.06/12)[$350,000( ) + $7500] = $

+ $1000](A|P 7/12%,360) =PMT(.07/12,360,350000* ) = $ ) 30-yr ARM, 6.5%: 1st year payment. A = [$350,000(1.0128) + $850](A|P 6.5/12%,360) =PMT(.065/12,360, * ) = $ ) 30-year balloon loan. A = (0.06/12)[$350,000( ) + $7500] = $")

38

Solution to Example 3.8 Step 2: calculate the present worth for each over 5 years 1) 30-yr. 7% conventional loan: PW = -$ (P|A 10/12%,60) - $ (P|A 7/12%,300)(P|F 10/12%,60) =PV(.10/12,60, ) +PV(.10/12,60,,-PV(.07/12,300, )) = -$311,208.86 2) 30-year ARM loan: (optimistic case) PW = -$ (P|A 10/12%,60) - $ (P|A 6.5/12%,300)(P|F 10/12%,60) =PV(.10/12,60, ) +PV(.10/12,60,,-PV(.065/12,300, )) = -$307,873.20

- $ (P|A 7/12%,300)(P|F 10/12%,60) =PV(.10/12,60, ) +PV(.10/12,60,,-PV(.07/12,300, )) = -$311, ) 30-year ARM loan: (optimistic case) PW = -$ (P|A 10/12%,60) - $ (P|A 6.5/12%,300)(P|F 10/12%,60) =PV(.10/12,60, ) +PV(.10/12,60,,-PV(.065/12,300, )) = -$307,")

39

Solution to Example 3.8 Step 2: calculate the present worth for each over 5 years 2) 30-year 7/1 ARM loan: (pessimistic case) Note: the nominal annual interest rate does not increase to 11.5%, because the couple sells the house after 5 years. At the time the house is sold, all future payments are based on a 10.5% nominal annual interest rate.

40

Solution to Example 3.8 Step 2: calculate the present worth for each over 5 years 3) 30-year balloon loan PW = -$ (P|A 10/12%,60) - [$350,000( ) + $7500](P|F 10/12%,60)] =PV(.10/12,60,(.061/12)*(35000* )) +PV(.10/12,60,,350000* ) = -$308,012.92 Based on the analysis, the couple chose the balloon loan.

- [$350,000( ) + $7500](P|F 10/12%,60)] =PV(.10/12,60,(.061/12)*(35000* )) +PV(.10/12,60,,350000* ) = -$308, Based on the analysis, the couple chose the balloon loan.")

41

PW of Two Mortgage Alternatives with a Planning Horizon of M Months

42

Why did we ignore the selling price for the house after 5 years?

Solution to Example 3.8 Why did we ignore the selling price for the house after 5 years?

43

Why did we ignore the selling price for the house after 5 years?

Solution to Example 3.8 Why did we ignore the selling price for the house after 5 years? Principle #7 Consider only differences in cash flows among investment alternatives

44

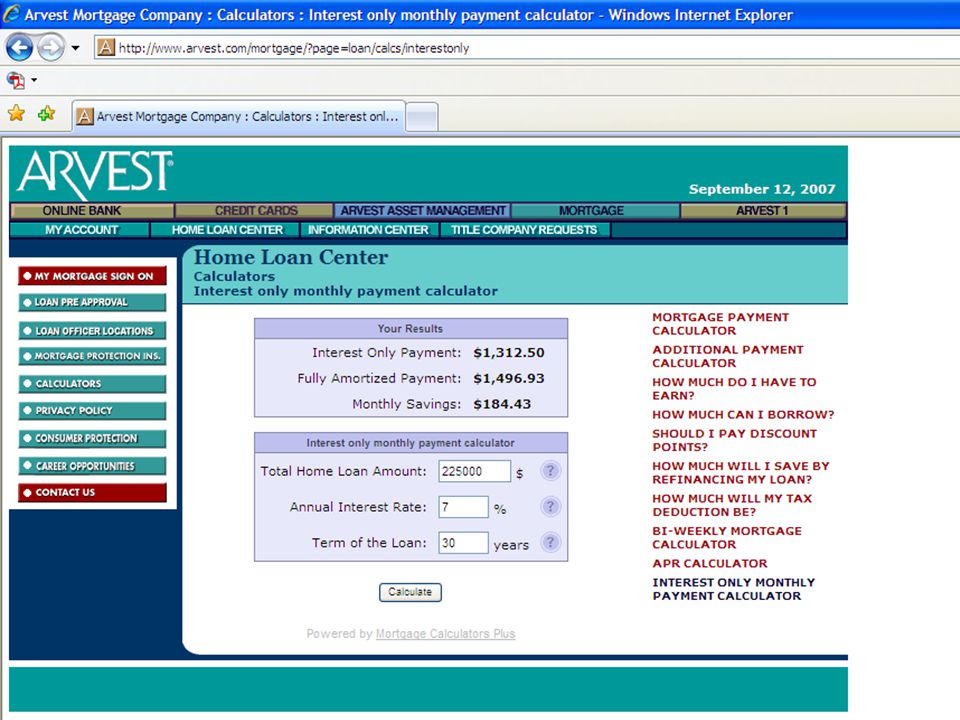

Example 3.9 If Adriana had chosen a 7% balloon loan, her monthly payments (without closing costs) would be A = $225,000(0.07)/12 = $ The same result is provided using Arvest’s loan calculator. However, balloon loans can have sizeable closing costs, as Table 3.5 illustrates.

/12. = $ The same result is provided using Arvest’s loan calculator. However, balloon loans can have sizeable closing costs, as Table 3.5 illustrates.")

47

Principal Amount & Interest Amount in Loan Payment

Because businesses can deduct from taxable income the interest paid on a loan and individuals can deduct from taxable income the interest paid on a mortgage on a primary residence, it is useful to know how much of a payment is interest. The balance of the payment is a reduction in the unpaid balance (or principal) on the loan.

on the loan.")

48

Principal Amount & Interest Amount in Loan Payment

Consider loan repayment plan 3—equal sized payments, with the first payment made one period after receipt of the loan. Let It = interest amount in payment t Pt = payment against principal (equity payment) in payment t Princ = principal amount borrowed A = payment size = P(A|P i%,n) i = interest rate for the loan n = number of equal payments then It = A[1- (P|F i%,n-t+1)] (3.9) Pt = A(P|F i%,n-t+1) (3.11)

in. payment t. Princ = principal amount borrowed. A = payment size = P(A|P i%,n) i = interest rate for the loan. n = number of equal payments. then. It = A[1- (P|F i%,n-t+1)] (3.9) Pt = A(P|F i%,n-t+1) (3.11)")

49

Deriving Equation 3.11 Let PWt-1 be the unpaid balance on the loan immediately after making the (t-1)st payment and PWt be the unpaid balance on the loan immediately after making the tth payment. The difference in the two is the amount of the tth payment that was a principal payment. Hence, Pt = PWt-1 - PWt or Pt = A(P|A i%,n-t+1) – A(P|A i%,n-t) or Pt = A[(P|A i%,n-t+1) – (P|A i%,n-t)]. Which reduces to Pt = A(P|F i%,n-t+1) (3.11)

st payment and PWt be the unpaid balance on the loan immediately after making the tth payment. The difference in the two is the amount of the tth payment that was a principal payment. Hence, Pt = PWt-1 - PWt or. Pt = A(P|A i%,n-t+1) – A(P|A i%,n-t) or. Pt = A[(P|A i%,n-t+1) – (P|A i%,n-t)]. Which reduces to Pt = A(P|F i%,n-t+1) (3.11)")

50

10/10/10 Loan Payment Example

If you borrow $10,000 at 10% compound annual interest and repay it with 10 equal annual payments, what amount of each payment will be interest? principal?

51

10/10/10 Loan Payment Example

If you borrow $10,000 at 10% compound annual interest and repay it with 10 equal annual payments, what amount of each payment will be interest? principal? P = $10,000, i = 10%, n = 10 A = $10,000(A|P 10%,10) = $1,627.50 It = A[1 – (P|F i%,n-t+1)] t It 1 $1627[ ] 6 $1627[ ] 2 $1627[ ] 7 $1627[ ] 3 $1627[ ] 8 $1627[ ] 4 $1627[ ] 9 $1627[ ] 5 $1627[ ] 10 $1627[ ]

= $1, It = A[1 – (P|F i%,n-t+1)] t. It. 1. $1627[ ] 6. $1627[ ] 2. $1627[ ] 7. $1627[ ] 3. $1627[ ] 8. $1627[ ] 4. $1627[ ] 9. $1627[ ] 5. $1627[ ] 10. $1627[ ]")

52

10/10/10 Loan Payment Example

If you borrow $10,000 at 10% compound annual interest and repay it with 10 equal annual payments, what amount of each payment will be interest? principal? P = $10,000, i = 10%, n = 10 A = $10,000(A|P 10%,10) = $1,627.50 t It Pt 1 $ $627.47 6 $616.95 $ 2 $937.28 $690.22 7 $515.90 $ 3 $868.25 $759.25 8 $404.74 $ 4 $792.33 $835.17 9 $282.45 $ 5 $708.83 $918.67 10 $147.96 $ I1 should equal $1,000. Round-off error in tables causes 3¢ error

= $1, t. It. Pt. 1. $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ I1 should equal $1,000. Round-off error in tables causes 3¢ error.")

53

10/10/10 Loan Payment (Excel)

If you borrow $10,000 and repay it with 10 equal annual payments, what amount of each payment will be interest? Using Excel’s IPMT financial function: =IPMT(rate,per,nper,pv,[fv],[type])

")

54

10/10/10 Loan Payment (Excel)

If you borrow $10,000 and repay it with 10 equal annual payments, what amount of each payment will be principal? Using Excel’s PPMT financial function: =PPMT(rate,per,nper,pv,[fv],[type])

")

55

Using an Alternative Approach

56

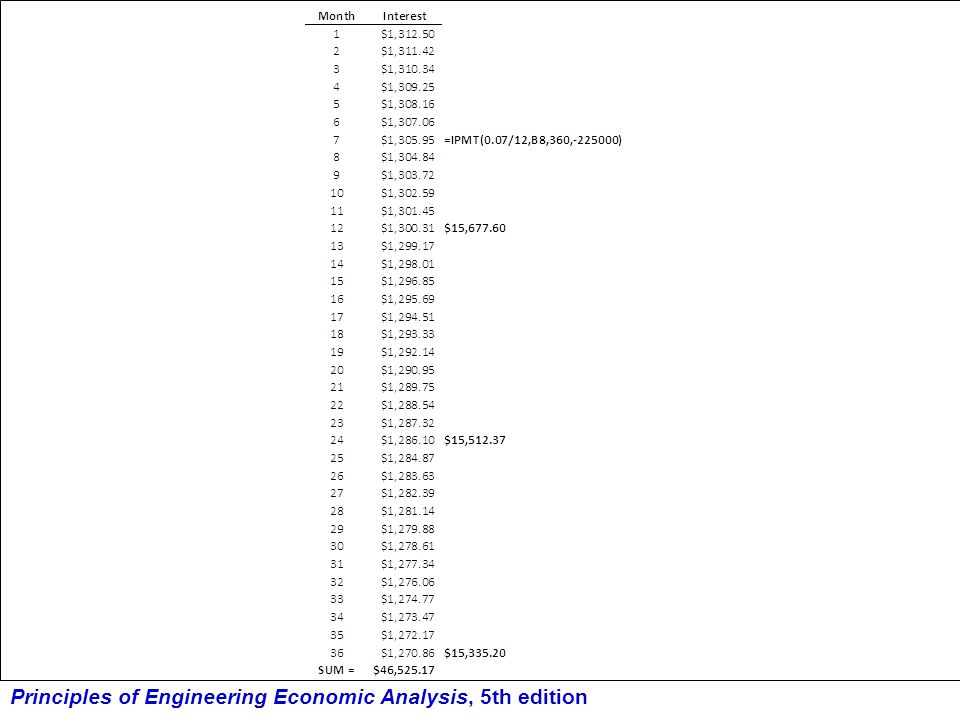

Example 3.14 Over a 3-year period, how much interest will Ms. Lopez pay on the $225,000 7% nominal annual interest rate, with monthly payments?

59

Example 3.14 (continued) Over a 3-year period, how much interest will Ms. Lopez pay on the $225,000 7% nominal annual interest rate, with monthly payments? Hence, Ms. Lopez will pay $15, $15, $15, = $46, in interest. She will pay 36*PMT(0.07/12,360, ) or $53, over a 3-year period. Therefore, she will pay $53, $46, = $7, toward principal.

or $53, over a 3-year period. Therefore, she will pay $53, $46, = $7, toward principal.")

61

Deferred Payment Loans

Let Princ = loan principal IR = interest rate on the loan UB = unpaid balance at the beginning of the interest period AO = cumulative amount owed just before making a payment Int = interest earned during the period = UB*IR UIB = unpaid accumulated interest immediately before making a loan payment UIA = unpaid accumulated interest immediately after making a loan payment Pmt = size of deferred loan payment IPmt = interest amount in payment PPmt = principal amount in payment = Pmt – IPmt IPmt = Min(UIB,Pmt)

")

62

10/10/10 Loan with Deferred Loan Payments

You borrow $10,000 at 10% annual compound interest and repay it with 10 equal annual payments. You make the first payment 4 years after receiving the $10,000. What amount of each payment will be principal? interest?

63

Excel Solution Interest Payment = Min(Unpaid Interest Before Payment, Loan Payment)

")

64

An Alternative Approach

When making loan payments, no reduction of the principal occurs until all accumulated interest has been paid. With deferred payments, the amount of interest owed might be such that no reduction in principal occurs until after several payments have been made. To determine the amount of interest and principal in a deferred payment, the following steps can be taken:

65

Determine the size of the deferred payment Ad = P(F|P i%,k)(A|P i%,n), where k is the deferment period, n is the number of payments, and P is the amount borrowed. Determine, Nd, the integer portion of the number of payments of size Ad required to pay off P, the amount borrowed. (IPMT and PPMT in the last Nd payments can be computed using Equations 3.9 and 3.11.) Determine PW(Nd), the present worth of Nd payments of size Ad. P - PW(Nd) is the amount of principal in payment n - Nd. (PPMT = $0 in payments 1, … , n - Nd -1.)

Determine PW(Nd), the present worth of Nd payments of size Ad. P - PW(Nd) is the amount of principal in payment n - Nd. (PPMT = $0 in payments 1, … , n - Nd -1.)")

66

10/10/10 Loan with Deferred Loan Payments

You borrow $10,000 at 10% annual compound interest and repay it with 10 equal annual payments. You make the first payment 4 years after receiving the $10,000. What amount of each payment will be principal? Interest? Ad = $10,000(F|P 10%,3)(A|P 10%,10) = $2,166.14 Nd =ROUNDDOWN(NPER(10%, ,10000),0) = 6 or (A|P 10%,n) = $2,166.14/$10,000 = n = and Nd = 6 For the last 6 payments, Eqs. 3.9 and 3.11 can be used to determine IPMT and PPMT. For payments 1, 2, and 3, IPMT = Ad = $2, and PPMT = $0. PW(Nd) = $2,166.14(P|A 10%,6) = $9,434.11 $10,000 - $9, = $ = PPMT4

(A|P 10%,10) = $2, Nd =ROUNDDOWN(NPER(10%, ,10000),0) = 6 or (A|P 10%,n) = $2,166.14/$10,000 = n = and Nd = 6. For the last 6 payments, Eqs. 3.9 and 3.11 can be used to determine IPMT and PPMT. For payments 1, 2, and 3, IPMT = Ad = $2, and PPMT = $0. PW(Nd) = $2,166.14(P|A 10%,6) = $9, $10,000 - $9, = $ = PPMT4.")

67

PPMT1 = PPMT2 = PPMT3 = $0 PPMT4 = $565

PPMT1 = PPMT2 = PPMT3 = $0 PPMT4 = $ PPMT5 =PPMT(10%,5,10,FV(10%,3,,10000)) = $1, PPMT6 =PPMT(10%,6,10,FV(10%,3,,10000)) = $1, PPMT7 =PPMT(10%,7,10,FV(10%,3,,10000)) = $1, PPMT8 =PPMT(10%,8,10,FV(10%,3,,10000)) = $1, PPMT9 =PPMT(10%,9,10,FV(10%,3,,10000)) = $1, PPMT10 =PPMT(10%,10,10,FV(10%,3,,10000)) = $1, IPMTt = Ad - PPMTt

) = $1, PPMT6 =PPMT(10%,6,10,FV(10%,3,,10000)) = $1, PPMT7 =PPMT(10%,7,10,FV(10%,3,,10000)) = $1, PPMT8 =PPMT(10%,8,10,FV(10%,3,,10000)) = $1, PPMT9 =PPMT(10%,9,10,FV(10%,3,,10000)) = $1, PPMT10 =PPMT(10%,10,10,FV(10%,3,,10000)) = $1, IPMTt = Ad - PPMTt")

68

Retirement Planning Sooner is better than later in investing!

Remember the power of the exponent! Start investing NOW!

71

Example 3.17 Immediately after beginning her engineering career, Maria establishes an investment plan and invests 10% of her $60,000 salary. If her salary increases by 10% per year over her professional career and she is able to earn 8% annually on her investments, how much will be in her investment account after 40 years if she continues to invest 10% of her salary? F = $6000(F|A1 8%,10%,40) F = $6000( ) F = $7,060,420.00

F = $6000( ) F = $7,060,")

72

Example 3.18 Franklin decides to postpone investing until he can “comfortably” do so. His salary is identical to Maria’s and increases 10% annually. If he waits 20 years to begin investing and earns 8% on his investments, what must be the size of his initial investment in order to accumulate the same amount in his investment account? After 20 years, his salary will be $60,000(F|P 10%,20), or $403, If he invests 10% of his salary for 20 years at 8% annually, he will accumulate F = $40,365.00(F|A1 8%,10%,20) F = $40,365.00( ) F = $4,170,800.00 To achieve a balance of $7,060,420, Franklin must invest P = ($7,060,420 - $4,170,800)(P|F 8%,20) P = $2,889,620( ) P = $619, (Where will he get the $619,968?)

, or $403, If he invests 10% of his salary for 20 years at 8% annually, he will accumulate. F = $40,365.00(F|A1 8%,10%,20) F = $40,365.00( ) F = $4,170, To achieve a balance of $7,060,420, Franklin must invest. P = ($7,060,420 - $4,170,800)(P|F 8%,20) P = $2,889,620( ) P = $619, (Where will he get the $619,968 )")

73

Justifying an Engineering Degree HS vs BSENG

Assume 8% TVOM Assume HS diploma lets you earn $18,000/yr, which increases 4%/yr for 47 years until age 65 Assume spend $10,000/yr for 4 yrs to get BSENG; starting salary of $60,000 increases at 6%/yr for 43 years until age 65 PW(HS) = $376,468.65 PW(BSENG) = $1,203,157.29 ROI(BSENG – HS) = 29.04%

= $376, PW(BSENG) = $1,203, ROI(BSENG – HS) = 29.04%")

74

Justifying an Advanced Degree BSENG vs MSENG

Assume 8% TVOM Assume takes 2 years to obtain MSENG; graduate school costs $12,000/yr Assume MSENG starting salary of $75,000 increases at 7%/yr for 41 years to age 65 PW(BSENG) = $1,203,157.29 PW(MSENG) = $1,479,707.57 ROI(MSENG – BSENG) = 15.39%

= $1,203, PW(MSENG) = $1,479, ROI(MSENG – BSENG) = 15.39%")

75

Justifying an Advanced Degree MSENG vs PhD

Assume 8% TVOM Assume takes 4 yrs after BSENG to get PhD Assume pay $10,000/yr for 4 yrs and $12,000/yr for 4 yrs Assume starting salary of $90,000 and annual increases at 8%/yr for 39 years to age 65 PW(MSENG) = $1,479,707.57 PW(PhD) = $1,738,560.87 ROI(PhD – MSENG) = 14.20%

= $1,479, PW(PhD) = $1,738, ROI(PhD – MSENG) = 14.20%")

76

Justifying an Advanced Degree MSENG vs PhD

Assume 8% TVOM Assume takes 4 yrs after BSENG to get PhD Assume $25,000 assistantship for each of 4 yrs Assume pay no tuition or fees Assume starting salary of $90,000 and annual increases at 8%/yr for 39 years to age 65 PW(MSENG) = $1,479,707.57 BTPW(PhD) = $1,828,647.82 ROI(PhD – MSENG) = %

= $1,479, BTPW(PhD) = $1,828, ROI(PhD – MSENG) = %")

77

Present Worth of Lifetime Earnings

j denotes annual increase in salary for the particular education alternative Lifetime defined to be from age 18 to age 65

78

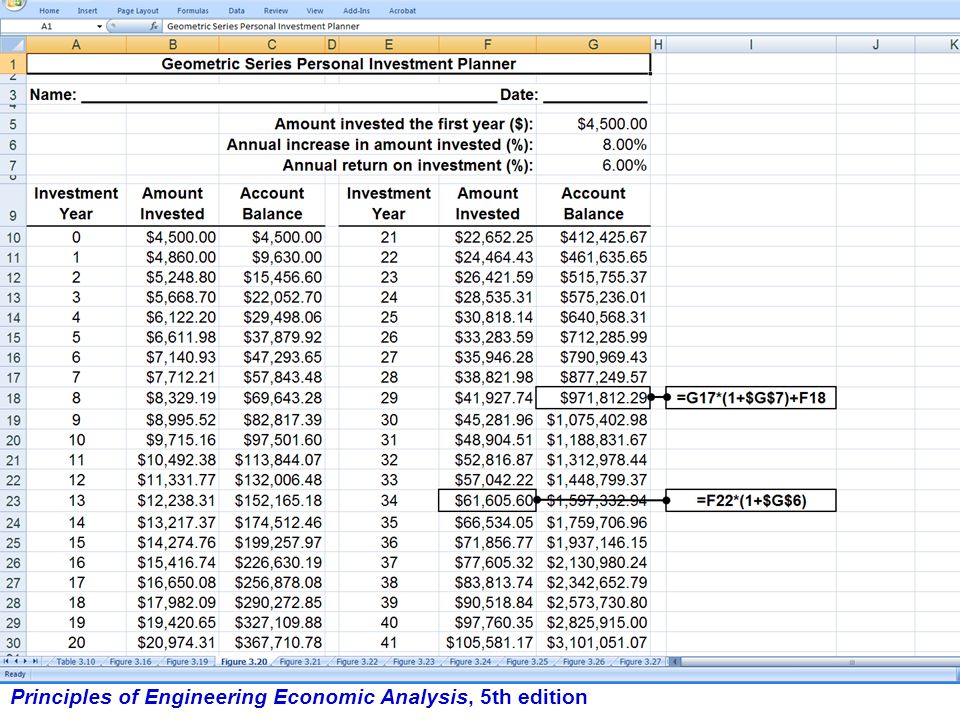

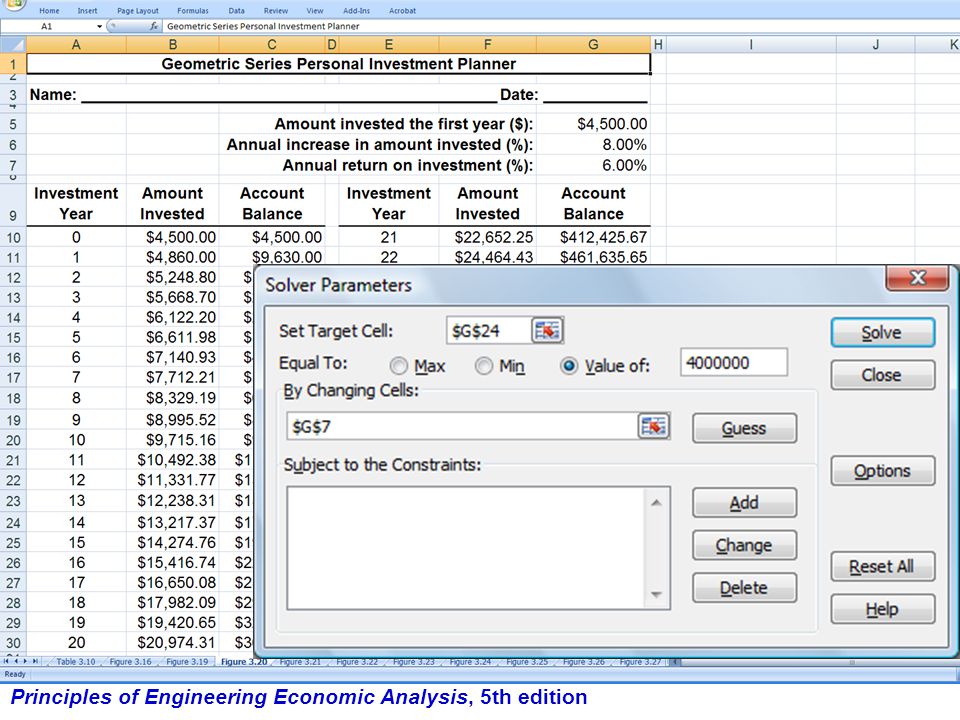

Example 3.20 Develop a spreadsheet that can be used to determine the size of an investment portfolio based on annual deposits that increase geometrically over a period of 40 years. Use, as input parameters, the magnitude of the 1st deposit, the annual increase in the deposits made, and the annual return on investment expected.

80

Example 3.21 Use the spreadsheet you developed to determine the magnitude of the investment portfolio after 40 years, if the 1st deposit is $4500 and the annual increase in the deposits made is 8%. Determine what your annual return on investment must be in order for the investment portfolio to total $4 million after 35 years.

83

Note: you can grad the SOLVER Parameter box and move it around or change its size.

84

Equivalence Two cash flow streams are said to be equivalent at k% interest if and only if their present worths are equal at k% interest.

85

Equivalence Example What uniform series over periods [1,8] is equivalent at 15% to the following cash flow profile? End of Period Cash Flow 1 $100 3 $200 4 5 $300

![Equivalence Example What uniform series over periods [1,8] is equivalent at 15% to the following cash flow profile](http://slideplayer.com/slide/5747094/19/images/85/Equivalence+Example+What+uniform+series+over+periods+%5B1%2C8%5D+is+equivalent+at+15%25+to+the+following+cash+flow+profile.jpg "End of Period. Cash Flow. 1. $ $ $300.")

86

Equivalence Example What uniform series over periods [1,8] is equivalent at 15% to the following cash flow profile? Solution: [100(F|P 15%,7)+200(F|P 15%,5)+100(F|P 15%,4) +300(F|P 15%,3)](A|F 15%,8) = $94.86 Answer: $94.86 End of Period Cash Flow 1 $100 3 $200 4 5 $300

![Equivalence Example What uniform series over periods [1,8] is equivalent at 15% to the following cash flow profile](http://slideplayer.com/slide/5747094/19/images/86/Equivalence+Example+What+uniform+series+over+periods+%5B1%2C8%5D+is+equivalent+at+15%25+to+the+following+cash+flow+profile.jpg "Solution: [100(F|P 15%,7)+200(F|P 15%,5)+100(F|P 15%,4) +300(F|P 15%,3)](A|F 15%,8) = $ Answer: $ End of Period. Cash Flow. 1. $ $ $300.")

87

Example 3.22 What single sum at t=6 is equivalent at 10% to the following cash flow profile? End of Period Cash Flow 1 -$400 2-4 +$100 6-8

88

Example 3.22 What single sum at t=6 is equivalent at 10% to the following cash flow profile? Solution: [ (P|A 10%,3)](F|P 10%,5) + 100(P|A 10%,3)(F|P 10%,1) = $29.85 Answer: $29.85 End of Period Cash Flow 1 -$400 2-4 +$100 6-8

+](http://slideplayer.com/slide/5747094/19/images/88/Example+3.22+What+single+sum+at+t%3D6+is+equivalent+at+10%25+to+the+following+cash+flow+profile+Solution%3A+%5B+%28P%7CA+10%25%2C3%29%5D%28F%7CP+10%25%2C5%29+%2B.jpg "100(P|A 10%,3)(F|P 10%,1) = $ Answer: $ End of Period. Cash Flow. 1. -$ $")

89

Example 3.22 (Alternative Solution)

What single sum of money at t=6 is equivalent to the following cash flow profile if i = 10%? Solution: F = [$100(F|A 10%,7)-$400(F|P 10%,7)-$100(F|P 10%,3)](P|F 10%,2) F = [$100( )-$400( )-$100( )]( ) F = $29.86 Answer: $29.86 End of Period Cash Flow 1 -$400 2 $100 3 4 5 $0 6 7 8

-$400(F|P 10%,7)-$100(F|P 10%,3)](P|F 10%,2) F = [$100( )-$400( )-$100( )]( ) F = $ Answer: $ End of Period. Cash Flow. 1. -$ $ $")

90

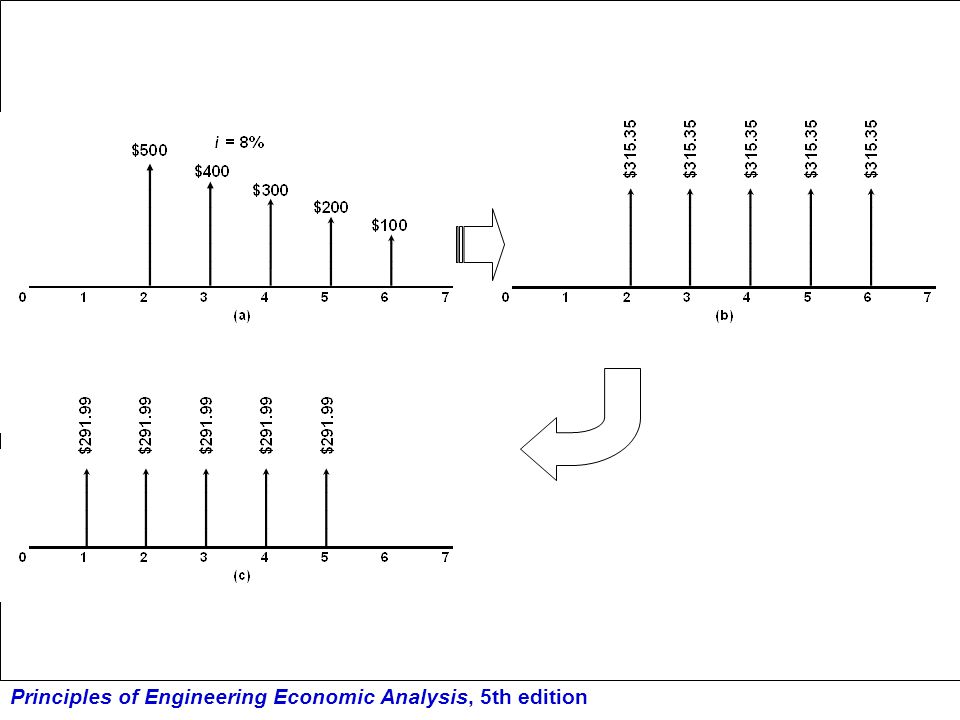

Example 3.23 What uniform series over [1,5] is equivalent to the following cash flow profile if i = 8%? End of Period Cash Flow 1 $0 2 $500 3 $400 4 $300 5 $200 6 $100 7

![Example 3.23 What uniform series over [1,5] is equivalent to the following cash flow profile if i = 8%](http://slideplayer.com/slide/5747094/19/images/90/Example+3.23+What+uniform+series+over+%5B1%2C5%5D+is+equivalent+to+the+following+cash+flow+profile+if+i+%3D+8%25.jpg "End of Period. Cash Flow. 1. $0. 2. $ $ $ $ $")

91

Example 3.23 What uniform series over [1,5] is equivalent to the following cash flow profile if i = 8%? Solution: The uniform series equivalent over [2,6] is A = $500 - $100(A|G 8%,5) or $500 - $100( ) = $315.35 The uniform series equivalent over [1,5] is A = $315.35(P|F 8%,1) or $315.35( ) = $291.99 Answer: $291.99 End of Period Cash Flow 1 $0 2 $500 3 $400 4 $300 5 $200 6 $100 7

![Example 3.23 What uniform series over [1,5] is equivalent to the following cash flow profile if i = 8%](http://slideplayer.com/slide/5747094/19/images/91/Example+3.23+What+uniform+series+over+%5B1%2C5%5D+is+equivalent+to+the+following+cash+flow+profile+if+i+%3D+8%25.jpg "Solution: The uniform series equivalent over [2,6] is A = $500 - $100(A|G 8%,5) or $500 - $100( ) = $ The uniform series equivalent over [1,5] is A = $315.35(P|F 8%,1) or $315.35( ) = $ Answer: $ End of Period. Cash Flow. 1. $0. 2. $ $ $ $ $")

93

Example 3.24 Determine the value of X that makes the two CFDs equivalent. FW(LHS) = $200(F|A 15%,4) + $100(F|A 15%,3) + $100 FW(RHS) = [$200 + X(A|G 15%,4)](F|A 15%,4) Equating the two and eliminating the common term of $200(F|A 15%,4), $100( ) + $100 = X( )( ) Solving for X give a value of $67.53.

= [$200 + X(A|G 15%,4)](F|A 15%,4) Equating the two and eliminating the common term of $200(F|A 15%,4), $100( ) + $100 = X( )( ) Solving for X give a value of $")

94

Note: you can grab the SOLVER Parameter Box and move it or change its size

95

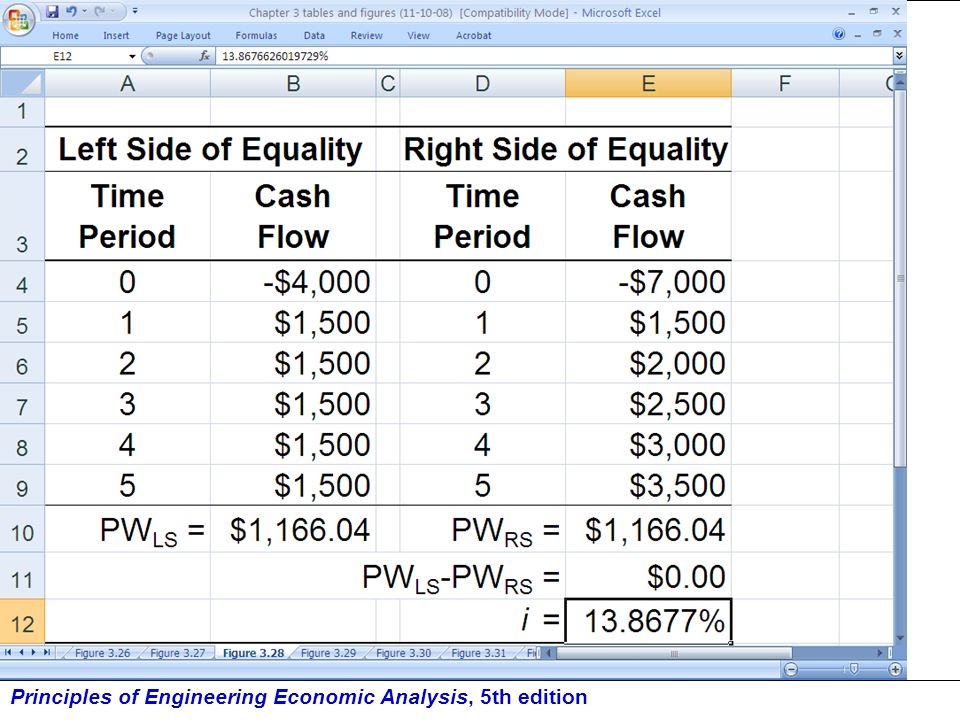

Example 3.25 For what interest rate are the two cash flow diagrams equivalent?

96

Example 3.25 (Continued) For what interest rate are the two cash flow diagrams equivalent? -$4000(A|P i%,5) + $1500 = -$7000(A|P i%,5) + $ $500(A|G i%,5) i ≈ % (by interpolation)

+ $ $500(A|G i%,5) i ≈ % (by interpolation)")

99

Bond Problems We consider investments in bonds because they are good examples of equivalency, they allow us to introduce investment measures considered in Chapter 4, they are popular vehicles for generating capital for a firm, and they are attractive investments for individuals.

100

Terminology V = par or face value of bond P = purchase price of bond

F = sales price (redemption value) of bond = V (if bond is redeemed at the end of its life) r = bond rate per interest period i = yield rate (ROI) per interest period n = number of bond payments received by bondholder A = coupon payment or interest received = Vr

of bond. = V (if bond is redeemed at the end of its life) r = bond rate per interest period. i = yield rate (ROI) per interest period. n = number of bond payments received by. bondholder. A = coupon payment or interest received. = Vr.")

101

Types of Bond Problems Given P, r, n, V and a desired i, find F

Given F, r, n, V, and desired i, find P Given P, F, r, n, and V, find i

102

Example 3.26 A $5000, 5-year bond is purchased on the date of issuance for $5000; the stated bond rate is 10% semiannually. If the bond is redeemed at maturity, what equivalent annual return will be earned on the investment?

103

Example 3.26 A $5000, 5-year bond is purchased on the date of issuance for $5000; the stated rate is 10% semiannually. If the bond is redeemed at maturity, what equivalent annual return will be earned on the investment? (Answer: effective annual interest rate for 10% per annum compounded semiannually or 10.25%) Semiannual payments of 10%/2, or 5% will be earned; thus, 0.05($5000), or $250 payments will be earned semiannually over a 5-year period. Setting the present worth of the outflow equal to the present worth of the inflow yields $5000=$250(P|A i%,10) + $5000(P|F i%,10). Solving for i yields 5% every 6 months, or an annual return of 10.25%.

Semiannual payments of 10%/2, or 5% will be earned; thus, 0.05($5000), or $250 payments will be earned semiannually over a 5-year period. Setting the present worth of the outflow equal to the present worth of the inflow yields $5000=$250(P|A i%,10) + $5000(P|F i%,10). Solving for i yields 5% every 6 months, or an annual return of 10.25%.")

104

Example 3.26 (Continued) A $5000, 5-year bond is purchased on the date of issuance for $5000; the stated bond rate is 10% semiannually. If the bond is redeemed at maturity, what equivalent annual return will be earned on the investment? Can be solved using Excel’s RATE financial function. =RATE(10,250,-5000,5000) = 5% → 5%/6 mo. or (1.05)2-1 = 10.25% equivalent annual return

= 5% → 5%/6 mo. or. (1.05)2-1 = 10.25% equivalent annual return.")

105

Example 3.26 (Continued) Now, suppose the $5000, 5-year bond is purchased for $5500 and the stated bond rate is 10% semiannually. If the bond is redeemed at maturity, what equivalent annual return will be earned on the investment? Can be solved using Excel’s RATE financial function. =RATE(10,250,-5500,5000) = 3.781%/6 mo. or ieff =(1+RATE(10,250,-5500,5000))^2-1 = 7.704% equivalent annual return

= 3.781%/6 mo. or. ieff =(1+RATE(10,250,-5500,5000))^2-1. = 7.704% equivalent annual return.")

106

Example 3.27 A $1000, 12% semiannual bond is purchased for $1050 and is to be sold after 3 years (after receipt of the 6th bond payment). What must it sell for in order to yield 5% per 6-month period?

. What must it sell for in order to yield 5% per 6-month period")

107

Example 3.27 A $1000, 12% semiannual bond is purchased for $1050 and is to be sold after 3 years (after receipt of the 6th bond payment). What must it sell for in order to yield 5% per 6-month period? P = Vr(P|A i%,n) + F(P|F i%,n) $1050 = $1000(0.06)(P|A 5%,6) + F(P|F 5%,6) $1050 = $60( ) F F = $998.98 F =FV(5%,6,60,-1050) = $998.99

. What must it sell for in order to yield 5% per 6-month period P = Vr(P|A i%,n) + F(P|F i%,n) $1050 = $1000(0.06)(P|A 5%,6) + F(P|F 5%,6) $1050 = $60( ) F. F = $ F =FV(5%,6,60,-1050) = $")

108

Example 3.28 A $1000, 12% semiannual bond is purchased. It is sold at par value after receipt of the 6th bond payment. What must be the purchase price in order to yield 7% per 6-month period?

109

Example 3.28 A $1000, 12% semiannual bond is purchased. It is sold at par value after receipt of the 6th bond payment. What must be the purchase price in order to yield 7% per 6-month period? P = Vr(P|A i%,n) + F(P|F i%,n) P = $1000(0.06)(P|A 7%,6) + F(P|F 7%,6) P = $60( )+$1000( ) P = $952.23 P =PV(7%,6,60,1000) = -$952.33

+ F(P|F i%,n) P = $1000(0.06)(P|A 7%,6) + F(P|F 7%,6) P = $60( )+$1000( ) P = $ P =PV(7%,6,60,1000) = -$")

110

Example 3.29 A $1000, 12% quarterly bond is purchased for $1020 and sold for $950 after receipt of the 12th bond payment. What were the quarterly yield and the effective annual return on the investment?

111

Example 3.29 A $1000, 12% quarterly bond is purchased for $1020 and sold for $950 after receipt of the 12th bond payment. What were the quarterly yield and the effective annual return on the investment? P = Vr(P|A i%,n) + F(P|F i%,n) $1020 = $1000(0.03)(P|A i%,12) + $950(P|F i%,12) Solving yields a value of i = % per quarter. The effective annual return is [( )4 -1] (100%) = % iqtr =RATE(12,30,-1020,950) = % ieff =EFFECT(4*RATE(12,30,-1020,950),4) = %

+ F(P|F i%,n) $1020 = $1000(0.03)(P|A i%,12) + $950(P|F i%,12) Solving yields a value of i = % per quarter. The effective annual return is [( )4 -1] (100%) = % iqtr =RATE(12,30,-1020,950) = % ieff =EFFECT(4*RATE(12,30,-1020,950),4) = %")

112

Variable Interest Rates

Consider the case in which different interest rates apply for different time periods. Let At denote the magnitude of the cash flow at the end of time period t, t = 1, …, n. Let is denote the interest rate during time period s, s = 1, …, t. The present worth of {At} is given by

113

Example 3.30 You deposit $1000 in a fund paying 8% annual interest; after 3 years the fund increases its interest rate to 10%; after 4 years of paying 10% interest the fund begins paying 12%. How much will be in the fund 9 years after the initial deposit?

114

Example 3.30 You deposit $1000 in a fund paying 8% annual interest; after 3 years the fund increases its interest rate to 10%; after 4 years of paying 10% interest the fund begins paying 12%. How much will be in the fund 9 years after the initial deposit? Solution: let Vt = value of fund at time t V3 = $ (F|P 8%,3) = $ V7 = $ (F|P 10%,4) = $ V9 = $ (F|P 12%,2) = $

= $ V7 = $ (F|P 10%,4) = $ V9 = $ (F|P 12%,2) = $")

115

Example 3.30 You deposit $1000 in a fund paying 8% annual interest; after 3 years the fund increases its interest rate to 10%; after 4 years of paying 10% interest the fund begins paying 12%. How much will be in the fund 9 years after the initial deposit? Solution: let Vt = value of fund at time t V3 = $ (F|P 8%,3) = $ V7 = $ (F|P 10%,4) = $ V9 = $ (F|P 12%,2) = $ V9=FVSCHEDULE(1000,{8%,8%,8%,10%,10%, 10%,10%,12%,12%}) = $2,313.55

= $ V7 = $ (F|P 10%,4) = $ V9 = $ (F|P 12%,2) = $ V9=FVSCHEDULE(1000,{8%,8%,8%,10%,10%, 10%,10%,12%,12%}) = $2,")

116

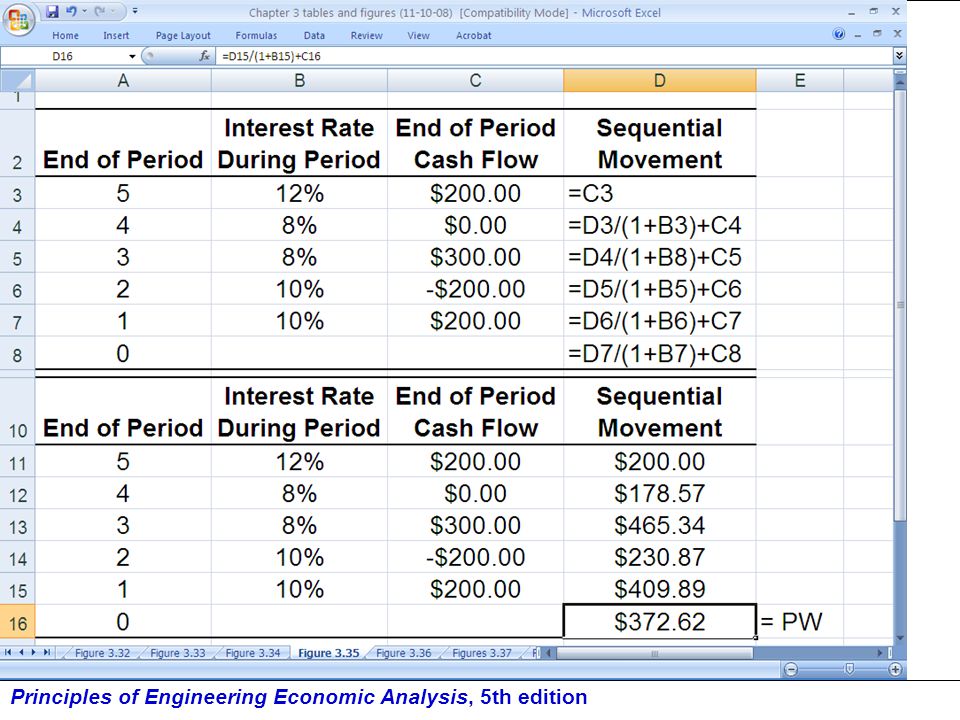

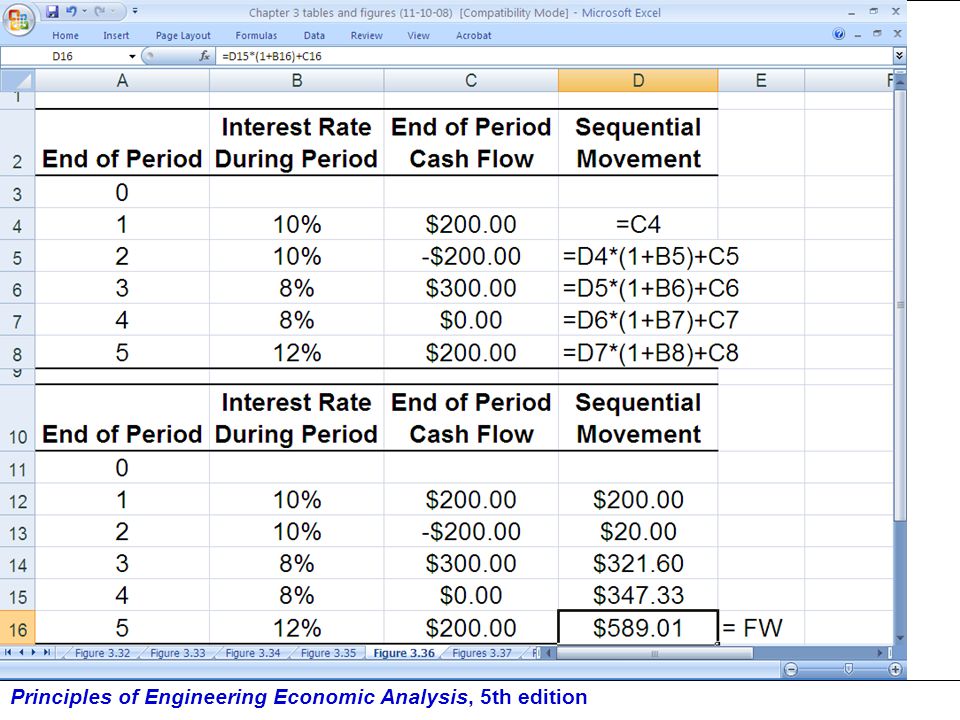

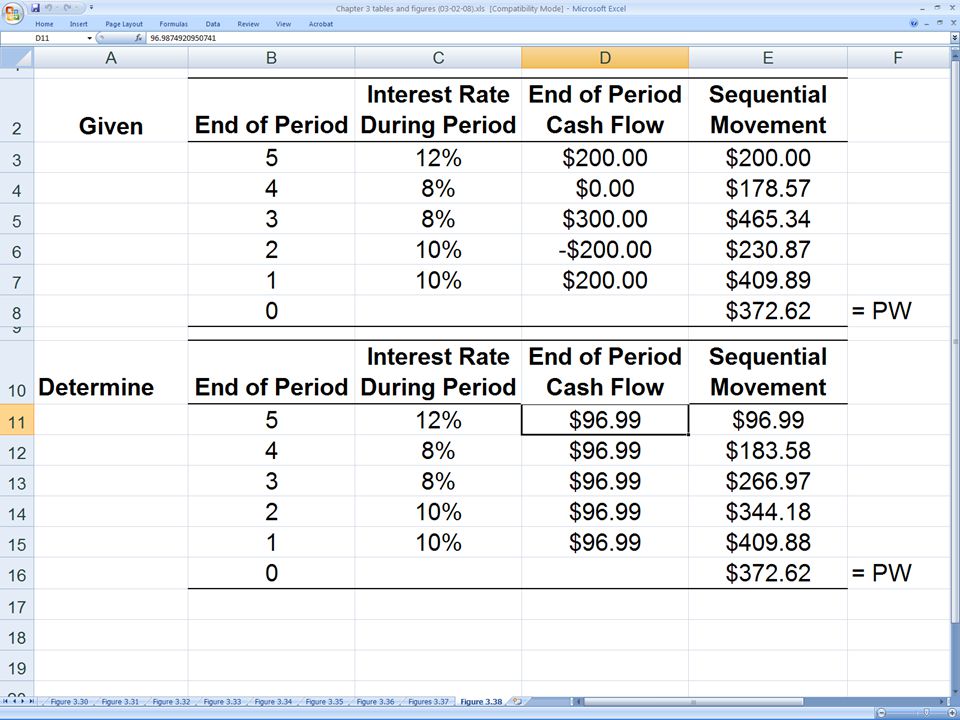

Example 3.31 Consider a cash flow profile in which $200 is received at t=1, spent at t=2, and received at t=5, and $300 is received at t=3. Suppose the interest rate is 10% the first 2 periods, 8% the next two periods, and is 12% the 5th period. What are the equivalent present worth, future worth, and uniform series for the cash flow profile? [note: t denotes end of period t]

117

Example 3.31 Solution: P = $200(P|F 10%,1) - $200(P|F 10%,2) +

$200(P|F 12%,1)(P|F 8%,2)(P|F 10%,2) P = $372.63

(P|F 8%,2)(P|F 10%,2) P = $")

119

Example 3.31 (Continued) F = $200 + $300(F|P 8%,1)(F|P 12%,1) –

$200(F|P 10%,1)(F|P 8%,2)(F|P 12%,1) F = $589.01 F =FVSCHEDULE(200,{0.1,0.08,0.08,0.12}) -FVSCHEDULE(200,{0.08,0.08,0.12}) +FVSCHEDULE(300,{0.08,0.12})+200

(F|P 8%,2)(F|P 12%,1) F = $ F =FVSCHEDULE(200,{0.1,0.08,0.08,0.12}) -FVSCHEDULE(200,{0.08,0.08,0.12}) +FVSCHEDULE(300,{0.08,0.12})+200.")

121

Example 3.31 (Continued) To solve for the uniform series equivalent, notice F = A[1+(F|P 12%,1)+(F|P 8%,1)(F|P 12%,1)+ (F|P 8%,2)(F|P 12%,1)+ (F|P 10%,1)(F|P 8%,2)(F|P 12%,1)] = A[ (1.12) (1.12) +1.1(1.08)(1.12)] = $589.01 $ = 6.073A A = $589.01/6.073 = $96.99

(F|P 12%,1)+ (F|P 10%,1)(F|P 8%,2)(F|P 12%,1)] = A[ (1.12) (1.12) +1.1(1.08)(1.12)] = $ $ = 6.073A. A = $589.01/6.073 = $")

122

Note: SOLVER Parameter Box can be grabbed, moved, and re-sized

124

Pit Stop #3— Checking Your Vital Signs

True or False: If you can earn 8% on your investments and you can borrow money at an annual compound rate of 6%, then (of the four repayment methods described in the chapter) you would prefer to repay the loan with equal monthly payments. True or False: In purchasing a house, the points and other closing costs you pay are included in the stated interest rate for a 30-year conventional loan. True or False: The annual percentage rate is the same as the effective annual interest rate. True or False: When repaying a loan with equal monthly payments, the amount of interest and the amount of principal in a loan payment remain proportionately the same over the loan period. True or False: If you purchase a $1000, 8% semiannual bond for $1000 and sell it after 5 years for $1000, then your effective annual yield on the bond is 8%.

you would prefer to repay the loan with equal monthly payments. True or False: In purchasing a house, the points and other closing costs you pay are included in the stated interest rate for a 30-year conventional loan. True or False: The annual percentage rate is the same as the effective annual interest rate. True or False: When repaying a loan with equal monthly payments, the amount of interest and the amount of principal in a loan payment remain proportionately the same over the loan period. True or False: If you purchase a $1000, 8% semiannual bond for $1000 and sell it after 5 years for $1000, then your effective annual yield on the bond is 8%.")

125

Pit Stop #3— Checking Your Vital Signs

True or False: If you can earn 8% on your investments and you can borrow money at an annual compound rate of 6%, then (of the four repayment methods described in the chapter) you would prefer to repay the loan with equal monthly payments. FALSE True or False: In purchasing a house, the points and other closing costs you pay are included in the stated interest rate for a 30-year conventional loan. FALSE True or False: The annual percentage rate is the same as the effective annual interest rate. FALSE True or False: When repaying a loan with equal monthly payments, the amount of interest and the amount of principal in a loan payment remain proportionally the same over the loan period. FALSE True or False: If you purchase a $1000, 8% semiannual bond for $1000 and sell it after 5 years for $1000, then your effective annual yield on the bond is 8%. FALSE

you would prefer to repay the loan with equal monthly payments. FALSE. True or False: In purchasing a house, the points and other closing costs you pay are included in the stated interest rate for a 30-year conventional loan. FALSE. True or False: The annual percentage rate is the same as the effective annual interest rate. FALSE. True or False: When repaying a loan with equal monthly payments, the amount of interest and the amount of principal in a loan payment remain proportionally the same over the loan period. FALSE. True or False: If you purchase a $1000, 8% semiannual bond for $1000 and sell it after 5 years for $1000, then your effective annual yield on the bond is 8%. FALSE.")

Similar presentations

Suppose you wanted to become a millionaire at retirement. If an annual compound interest rate of.>")

Click here for Streaming Audio To Accompany Presentation.>")

>")