Download presentation

Presentation is loading. Please wait.

1

European Monetary Policy 13 th April 2010 Morgan Goble, James Hurrell, Karina Melamed, Andre Watson & Tian Wang

2

The European Community became the European Union (EU) in 1993 and is now comprised of 27 member countries within Europe. 16 of the EU countries use a single currency, the euro, and collectively make up the Eurozone. Source: http://www.ecb.int/ecb Source: http://www.ecb.int/ecb/educational/facts/orga/html/or_001.en. Comprises: Belgium, Germany, Ireland, Greece, Spain, France, Italy, Cyprus, Luxembourg, Malta, The Netherlands, Austria, Portugal, Slovenia, Slovakia, Finland The European System of Central Banks (ESCB ) The Eurozone Comprises: - The European Central Bank (ECB) - The National Central Banks (NCB) of all 27 member states (see below) - But a subset called Eurosystem focuses on monetary policy for Eurozone only

The Eurozone Comprises: - The European Central Bank (ECB) - The National Central Banks (NCB) of all 27 member states (see below) - But a subset called Eurosystem focuses on monetary policy for Eurozone only.")

3

The ECB focuses on formulating the policies and ensuring that the NCBs implement these policies consistently, whereas the NCBs themselves implement the monetary policy operations in member states. Source: http://www.ecb.int/ecb/educational/facts/orga/html/or_001.en. 1. Eurosystem: A subset of the ESCB called the Eurosystem is dedicated to the 16 member states whose common currency is the Euro. It is comprised of the ECB and the NCBs of the 16 states. The core tasks of the Eurosystem are: 1)Monetary policy 2)Foreign Exchange operations 3)Promote smooth operation of payment systems (transfer of money from credit to monetary institutions – essential in implementation of monetary policy) 4)Hold and manage foreign reserves 2. Non-Eurozone: Non-Eurozone NCBs are committed to the principles of EU monetary policy and cooperate in many areas such as exchange rate policy, but maintain their monetary sovereignty and are not involved in the monetary policy of the euro area (Eurosystem). They make up the ‘General Council’ of the ECB and also focus on recruiting additional members to Eurozone. 3. Use of NCBs (decentralized system): NCBs are critical in the implementation of any Eurosystem policy as established by the ECB. This reflects the heterogeneity of languages and cultures endemic on the Eurozone. Most print their own euro banknotes (ECB sets regulation for the amount to print) and perform country specific financial and administrative activities for their governments. The ECB and the NCBs jointly contribute to attaining the Eurosystem's common goals (see ‘Governing Council’ below). However, the ECB must ensure that all tasks are carried out properly and consistently. To ensure this across the euro area, the ECB has the power to issue guidelines and instructions to the NCBs. 4. The Governing Council (NCB/ECB interaction and decision making): This is the main decision making body of the Eurosystem and is made up of the executive board members of the ECB as well as the presidents of the NCBs of the Eurozone. The council meets twice a month and, when making decisions, all members act independently of their states and in the best interests of the Eurozone. The responsibilities of the council include: - Formulating the monetary policy of the Eurozone. - Issuing guidelines for operations of the NCBs. - Taking the necessary steps to ensure NCB compliance with ECB. - Authorizing the issuance of euro currency within the Eurozone. - Establishing the necessary rules for the accounting and reporting of operations undertaken by the NCBs.

Monetary policy 2)Foreign Exchange operations 3)Promote smooth operation of payment systems (transfer of money from credit to monetary institutions – essential in implementation of monetary policy) 4)Hold and manage foreign reserves 2. Non-Eurozone: Non-Eurozone NCBs are committed to the principles of EU monetary policy and cooperate in many areas such as exchange rate policy, but maintain their monetary sovereignty and are not involved in the monetary policy of the euro area (Eurosystem). They make up the ‘General Council’ of the ECB and also focus on recruiting additional members to Eurozone. 3. Use of NCBs (decentralized system): NCBs are critical in the implementation of any Eurosystem policy as established by the ECB. This reflects the heterogeneity of languages and cultures endemic on the Eurozone. Most print their own euro banknotes (ECB sets regulation for the amount to print) and perform country specific financial and administrative activities for their governments. The ECB and the NCBs jointly contribute to attaining the Eurosystem s common goals (see ‘Governing Council’ below). However, the ECB must ensure that all tasks are carried out properly and consistently. To ensure this across the euro area, the ECB has the power to issue guidelines and instructions to the NCBs. 4. The Governing Council (NCB/ECB interaction and decision making): This is the main decision making body of the Eurosystem and is made up of the executive board members of the ECB as well as the presidents of the NCBs of the Eurozone. The council meets twice a month and, when making decisions, all members act independently of their states and in the best interests of the Eurozone. The responsibilities of the council include: - Formulating the monetary policy of the Eurozone. - Issuing guidelines for operations of the NCBs. - Taking the necessary steps to ensure NCB compliance with ECB. - Authorizing the issuance of euro currency within the Eurozone. - Establishing the necessary rules for the accounting and reporting of operations undertaken by the NCBs..")

4

The main differences between the ECB (Eurozone) and the Fed (USA) are around the nature of their primary objectives and the approach to decision making. Federal Open Market Committee (FOMC) Board (7 chairs) 5 of 12 regional Feds on rotation (exception of N.Y) Governing Council (see slide above) Exec Board (6 chairs) 16 NCB Presidents Source : http://www.federalreserve.gov Source: http://www.ecb.int/ecb/

Board (7 chairs) 5 of 12 regional Feds on rotation (exception of N.Y) Governing Council (see slide above) Exec Board (6 chairs) 16 NCB Presidents Source : Source:")

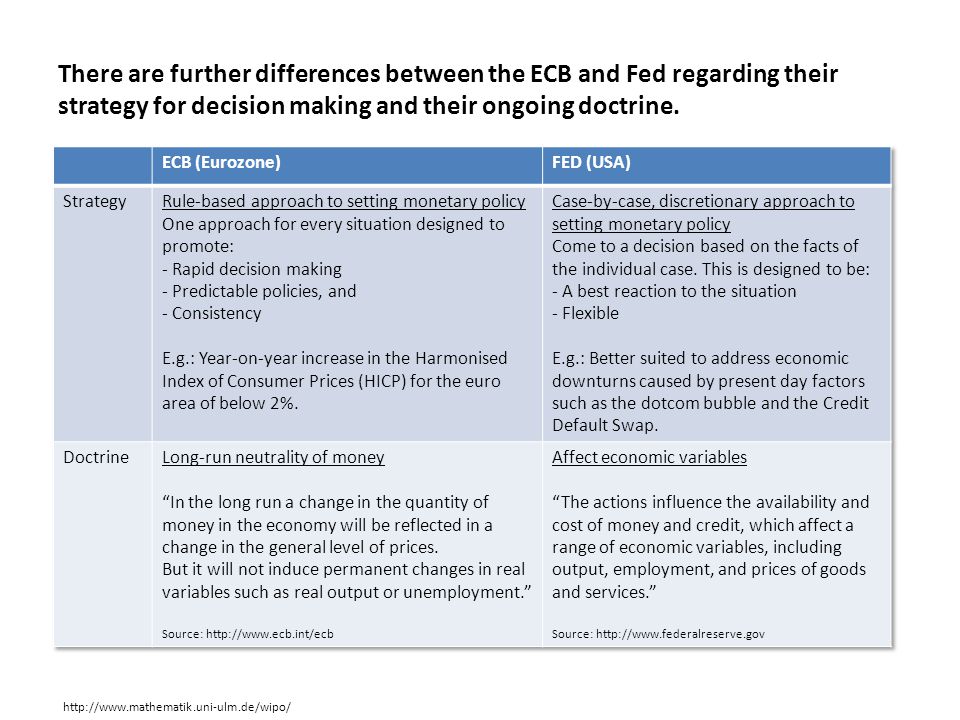

5

There are further differences between the ECB and Fed regarding their strategy for decision making and their ongoing doctrine. http://www.mathematik.uni-ulm.de/wipo/

6

Eurozone expected inflation for March 2010 is 1.5%. European Central Bank aims for inflation rates below or close to 2.0%. In 2008, the inflation rate for the Eurozone hit 3.8%, the highest in a decade due to soaring commodity prices. Such high inflation was quickly followed by a financial and economic crisis, forcing a decline in not only commodity prices but also manufactured goods. During 2010, three factors will have a significant impact on the inflation rate: energy prices, industrial goods prices, and wages. In January, the energy component was 5.1% higher than one year ago with expected oil prices to average US$78/barrel in 2010, well above the low of US$40/barrel in 2009, this is likely to stay high in the near term. The EU is facing extreme weakness in the pricing power of goods, which will continue through 2010. Wage inflation, effected the least during the crisis, is currently 3.5% year-on-year, in-line with long term averages. However, with employment decreasing and with the weakening of labor’s bargaining power, a reduction in wage inflation is expected. Sources: European Central Bank Statistical Warehouse (www.sdw.ecb.europa.eu) and Economist Intelligence Unit (www.eiu.com)

7

Eurozone GDP is stable. Recovery through 2014 is expected, but will be weak. Source: Economist Intelligence Unit (www.eiu.com) Eurozone GDP in 2010 is expected to be 0.7%, with little contribution from private consumption and gross investment. Slow recovery can be attributed to a myriad of factors: Within the banking system, the supply of credit is still low; stock of bank lending to non- financial companies has contracted every month since February 2009 Capacity utilization is at an all time low Construction is expected to be considerably weaker over the next 5 years compared to the last Private consumption is the largest single factor component of growth. Estimated to be 0.3% in 2010, it directly suffers from a downturn in employment, which is expected to continue in 2010. Government spending efforts are expected to slow, which may have caused a temporary relief in GDP growth -The slight growth in 2010 is expected to come mostly from the government, which will seek to offset GDP in the short term, but will likely switch gears in the long term and focus on reversing recent large increases in public debt.

8

The European Central Bank has kept the Eurozone’s interest rate at a record low level of 1% for the past 11 months. Source: European Central Bank (http://www.ecb.int/home/html/index.en.html) The 3 key interest rates for the Eurozone are the Main Refinancing Operations, Deposit Facility, and Marginal Lending Facility rates. The main refinancing operations rate is equivalent to the current short term interest rate. The deposit facility rate is the lowest possible interest rate that could be offered to a bank for depositing money to the ECB, while the marginal lending facility rate is the highest possible rate that can be charged to a bank for borrowing money from the ECB. As illustrated by the graph above, short term interest rates have steadily decreased in the recent past, as of October 2008. Since its inception, the ECB has changed the way it calculates the main refinancing operations rate from a fixed rate to a variable rate, where central banks placed bids on the short-term interest rate, and most currently back to a fixed rate.

9

The Eurozone’s short-term interest rate of 1% is set too high, based on Taylor’s Rule. The Eurozone strives to maintain a stable inflation rate below, but close to 2%. The Eurozone currently is experiencing an inflation rate of 1.5%, which is on target. However, based upon the Eurozone’s negative GDP growth (-1.8%), Taylor’s Rule suggests that the Eurozone should reduce interest rates more aggressively. i = r* + + a 1 ( - a 2 (y - y*).35 = 1 + 1.5 +.5 (1.5 - 2) +.5 (-1.8 - 2) Based on Taylor’s Rule, the optimal main refinancing operation (short-term) interest rate is 0.35%. Source: European Commission (www.tradingeconomics.com)

, Taylor’s Rule suggests that the Eurozone should reduce interest rates more aggressively. i = r* + + a 1 ( - a 2 (y - y*).35 = ( ) +.5 ( ) Based on Taylor’s Rule, the optimal main refinancing operation (short-term) interest rate is 0.35%. Source: European Commission (")

10

Taylor’s Rule for individual member countries suggested otherwise: The short-term interest rate is high for some and low for others. Member countries’ annualized inflation rate for year 2009 range from (1.70)% to 1.80% Member countries’ forecasted GDP growth for year 2010 range from (1.40)% to 1.90% Result from Taylor’s Rule calculation range from (1.05)% to 1.90% Conclusion: Taylor’s Rule is more difficult to use for ECB compare to FED because of Eurozone’s unique political structure. Each country has its own economic and political agenda while United States is only one country with one agenda. Source: European Commission Eurostat ( http://epphttp://epp.eurostat.ec.europa.eu/portal/page/portal/eurostat/home/) Inflation Rate(%) GDP Growth(%) Optimal Interest Rate Austria 0.40 1.10 1.25 Belgium - 0.60 0.80 Cyprus 0.20 0.10 0.65 Finland 1.60 0.90 1.75 France 0.10 1.20 1.15 Germany 0.20 1.20 Greece 1.30 (0.30) 1.00 Ireland (1.70) (1.40) (1.05) Italy 0.80 0.70 1.25 Luxembourg - 1.10 1.05 Malta 1.80 0.70 1.75 Netherlands 1.00 0.30 1.15 Portugal (0.90) 0.30 0.20 Slovakia 0.90 1.90 Slovenia 0.90 1.30 1.60 Spain (0.30) (0.80) (0.05)

% to 1.80% Member countries’ forecasted GDP growth for year 2010 range from (1.40)% to 1.90% Result from Taylor’s Rule calculation range from (1.05)% to 1.90% Conclusion: Taylor’s Rule is more difficult to use for ECB compare to FED because of Eurozone’s unique political structure. Each country has its own economic and political agenda while United States is only one country with one agenda. Source: European Commission Eurostat ( Inflation Rate(%) GDP Growth(%) Optimal Interest Rate Austria Belgium Cyprus Finland France Germany Greece 1.30 (0.30) 1.00 Ireland (1.70) (1.40) (1.05) Italy Luxembourg Malta Netherlands Portugal (0.90) Slovakia Slovenia Spain (0.30) (0.80) (0.05).")

11

Eurozone’s short-term interest rate over the next 6 months will continue to be 1%, while the US’s short-term interest rate will likely grow by a small amount. ECB (Eurozone) FED (USA) Current Rate1%Around 0.10% Expected Rate1%Around 0.30% Economical CircumstancesSlow and steady recovery in some of the member countries, but concern with growth and sovereign indebtedness in some other members, such as Greece. Most member countries would be in favor of a expansionary Monetary policy. US economy is recovering at a slow but steady rate. An expansionary Monetary policy is the common consent. Political ConsiderationIndividual sovereign countries with different political agendas and economic concerns will call for different interest rate policies. However, it is very difficult to implement a rate lower than 1% due to historical rates. US government is in favor of a lower interest rate due to the need to resolve both high government deficit and high unemployment rate Policy OriantationSince price stability is the primary objective, interest rates will stay above Taylor Rule for member countries with lower growth in order to control possible inflation for member countries with higher growth Trade-off between stable prices (low inflation)and economical growth (full employment)

FED (USA) Current Rate1%Around 0.10% Expected Rate1%Around 0.30% Economical CircumstancesSlow and steady recovery in some of the member countries, but concern with growth and sovereign indebtedness in some other members, such as Greece. Most member countries would be in favor of a expansionary Monetary policy. US economy is recovering at a slow but steady rate. An expansionary Monetary policy is the common consent. Political ConsiderationIndividual sovereign countries with different political agendas and economic concerns will call for different interest rate policies. However, it is very difficult to implement a rate lower than 1% due to historical rates. US government is in favor of a lower interest rate due to the need to resolve both high government deficit and high unemployment rate Policy OriantationSince price stability is the primary objective, interest rates will stay above Taylor Rule for member countries with lower growth in order to control possible inflation for member countries with higher growth Trade-off between stable prices (low inflation)and economical growth (full employment).")

Similar presentations

is an organization of European countries dedicated to increasing economic integration and.>")