Download presentation

Presentation is loading. Please wait.

1

MODERN AUDITING 7th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State University Walter G. Kell University of Michigan Developed by: Dr. Raymond N. Johnson, CPA Gregory K. Lowry, MBA, CPA John Wiley & Sons, Inc.

2

CHAPTER 14 AUDITING THE REVENUE CYCLE u Nature of the Revenue Cycle u Control Activities — Credit Sales Transactions u Control Activities — Cash Receipts Transactions u Control Activities — Sales Adjustment Transactions u Substantive Tests of Accounts Receivable u Value-Added Services

3

An entity’s revenue cycle For a merchandising company, the classes of transactions in the revenue cycle include: 1. credit sales (sales made on accounts), 2. cash receipts (collections on accounts and cash sales), and 3. sales adjustments (discounts, sales returns and allowances, and uncollectable accounts [provisions and writeoffs]). Nature of the Revenue Cycle

, 2. cash receipts (collections on accounts and cash sales), and 3. sales adjustments (discounts, sales returns and allowances, and uncollectable accounts [provisions and writeoffs]). Nature of the Revenue Cycle.")

4

The Revenue Cycle Figure 14-1

5

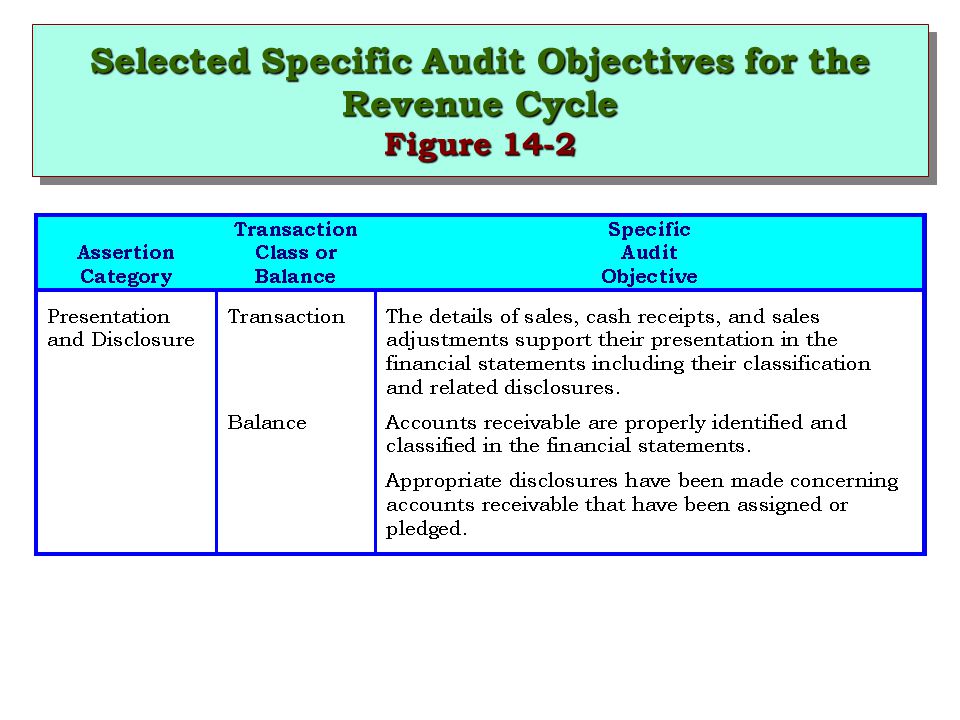

Selected Specific Audit Objectives for the Revenue Cycle Figure 14-2

8

Understanding the Client’s Business and Industry Auditors develop audit strategy based on the risk of material misstatement. The first step in assessing risk is obtaining an understanding of the client’s business and industry because it assists the auditor in: 1.Developing an expectation of total revenues by understanding the client’s capacity, market place, and the client’s business risks in the revenue cycle. 2.Developing an expectation of gross margin by understanding the client’s market share, competitive advantage in the market place, and drivers of net sales. 3.Developing an expectation of net receivables based on the average collection period for the client and industry. 4.Understanding industry accounting practices. Nature of the Revenue Cycle

9

Business and Industry Mfg. of household appliance Mfg. of electronic computers Retail grocer Hotel Local school district Understanding drivers of total revenue and related risks Understanding likely gross margins Evaluating receivable collections Unique accounting practices

10

Nature of the Revenue Cycle Materiality (Tolerable Misstatement) Revenues are a measure of volume of activity for virtually every entity. The accounts receivable produced by credit sales transactions are almost always material to the balance sheet. Receivables are costly to audit with substantive tests of details.

11

Inherent Risk Pervasive factors that may affect assertions in several cycles. 1.Pressures to overstate revenues in order to report achieving announced revenue or profitability targets or industry norms that were not achieved in reality owing to such factors as: – Global, national, or regional economic conditions – The impact of technological developments on the entity’s competitiveness – Poor management. 2.Pressures to overstate gross receivables or understate the allowance for doubtful accounts in order to report a higher level of working capital in the face of the need to meet debt covenants. Nature of the Revenue Cycle

12

Inherent Risk Other factors: 1. The volume of sales, cash receipts, and sales adjustment transactions is often high, resulting in numerous opportunities for errors to occur. 2. The timing and amount of revenue to be recognized may be contentious owing to factors such as ambiguous accounting standards, the need to make estimates, the complexity of the calculations involved, and purchasers’ rights of return. 3. When receivables are factored with recourse, the correct classification of the transaction as a sale or a borrowing may be contentious. Nature of the Revenue Cycle

13

Inherent Risk 4. Receivables may be misclassified as current or noncurrent owing to difficulties in estimating the likelihood of collection within the next year or the source of events on which collection is contingent. 5. Cash receipt transactions generate liquid assets that are particularly susceptible to misappropriation. 6. Sales adjustment transactions may be used to conceal thefts of cash received from customers by overstating discounts, recording fictitious sales returns, or writing off customers’ balances as uncollectable. Nature of the Revenue Cycle

14

Analytical Procedures Risk Analytical procedures risk is the element of detection risk that analytical procedures will fail to detect material misstatements. – Cost effective – Rely on the auditor’s knowledge of the business and industry. – Effective in identifying issues that may result in providing value-added services. The first step in performing analytical procedures is obtaining an understanding of total revenues given: 1. the client’s capacity and 2. the client’s market place for those products. Nature of the Revenue Cycle

15

Analytical Procedures Analytical procedures are an important way to quantify the auditor’s understanding of the business and industry and an entity’s business risks. Reported Financial Performance Underlying Business Activity

16

The auditor should obtain an understanding of the client’s capacity -- the maximum volume of sales that it could generate if it fully utilized its facilities and employees to manufacture and deliver products or services. The volume of sales that an entity records given its capacity The number of shifts that an entity operates Seasonal variations in the industry. Nature of the Revenue Cycle

17

One important analytical procedure is understanding the client’s market share, which compares the client’s revenues with total revenues in the market for the client’s product. This is particularly important because companies with dominant market shares often obtain premium gross margins. Finally, it is important for the auditor to evaluate the client’s accounts receivable turn days, or average collection period, and be able to compare the collection period with industry norms. Nature of the Revenue Cycle

18

Analytical Procedures Commonly Used to Audit the Revenue Cycle Figure 14-3

20

Control Activities — Credit Sales Transactions Obtaining an Understanding and Assessing Control Risk The auditor should obtain an understanding of the sales cycle that is sufficient to plan the audit. That is, the auditor needs to have a sufficient understanding to be able to: 1. identify the types of potential misstatements, 2. consider factors that affect the risk of material misstatements, and 3. design substantive tests.

21

Consideration of Internal Control Control Environment Risk Assessment Information and Communication –Initiate transactions –Deliver (receive) goods or services –Record Transactions –Consideration Control Activities Monitoring

goods or services –Record Transactions –Consideration Control Activities Monitoring")

22

Credit Sales Common Documents and Records Customer Order Sales Order Authorized Price List Shipping Documents (Bill of Lading and Packing Slip) Sales Invoice Sales Transaction File Sales Journal Customer Master File Accounts Receivable Master File Customer Monthly Statement

Sales Invoice Sales Transaction File Sales Journal Customer Master File Accounts Receivable Master File Customer Monthly Statement")

23

Credit Sales Functions Initiating Sales –Accepting customer orders –Approving credit Delivery of Goods and Services –Filling sales orders –Shipping sales orders Recording Sales –Billing customers –Recording sales

24

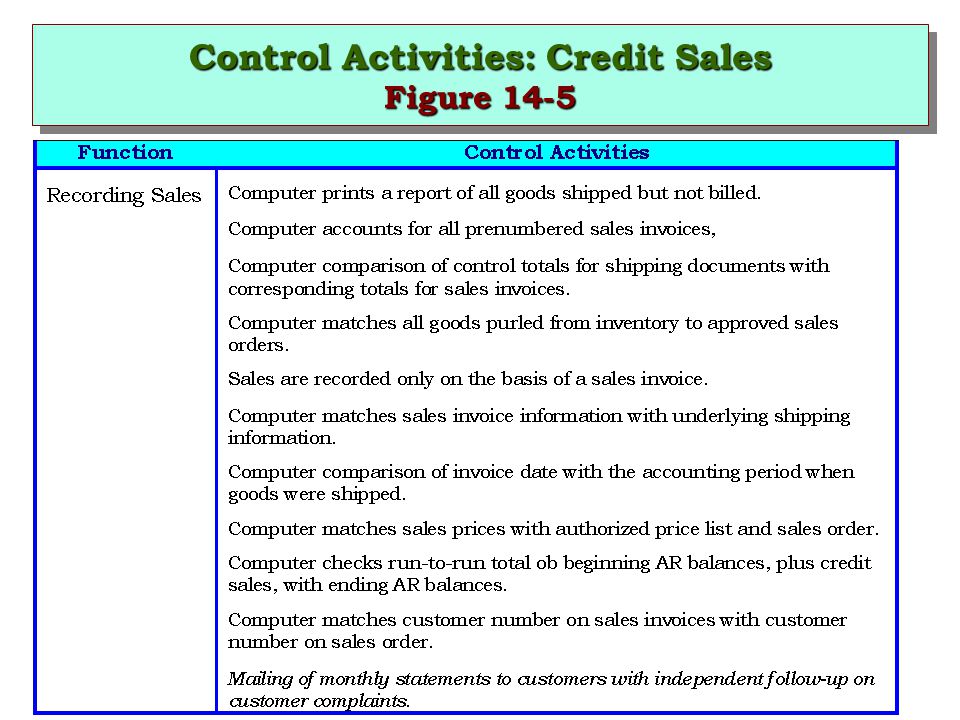

Control Activities: Credit Sales Figure 14-5

26

Cash Receipts Common Documents and Records Remittance advice Prelist Cash count sheets Daily cash summary Validated deposit slip Cash receipts transactions file Cash receipts journal

27

Cash Receipts Functions Cash Receipts –Receiving cash receipts –Depositing cash in bank –Recording the receipts

28

Control Activities: Cash Receipts Figure 14-7

29

Control Activities — Sales Adjustment Transactions Sales adjustment transactions involve the following: 1.Granting cash discounts 2.Granting sales returns and allowances (credit memo) 3.Determining uncollectable accounts (writeoff authorization memo)

3.Determining uncollectable accounts (writeoff authorization memo)")

30

Substantive Tests of Accounts Receivable The sales that are most likely to represent potential misstatements are the uncollected sales. To design substantive tests for these accounts, the auditor must first determine the acceptable level of tests of details risk for each significant related assertion.

31

Correlation of Risk Components — Accounts Receivable Assertions Figure 14-8

32

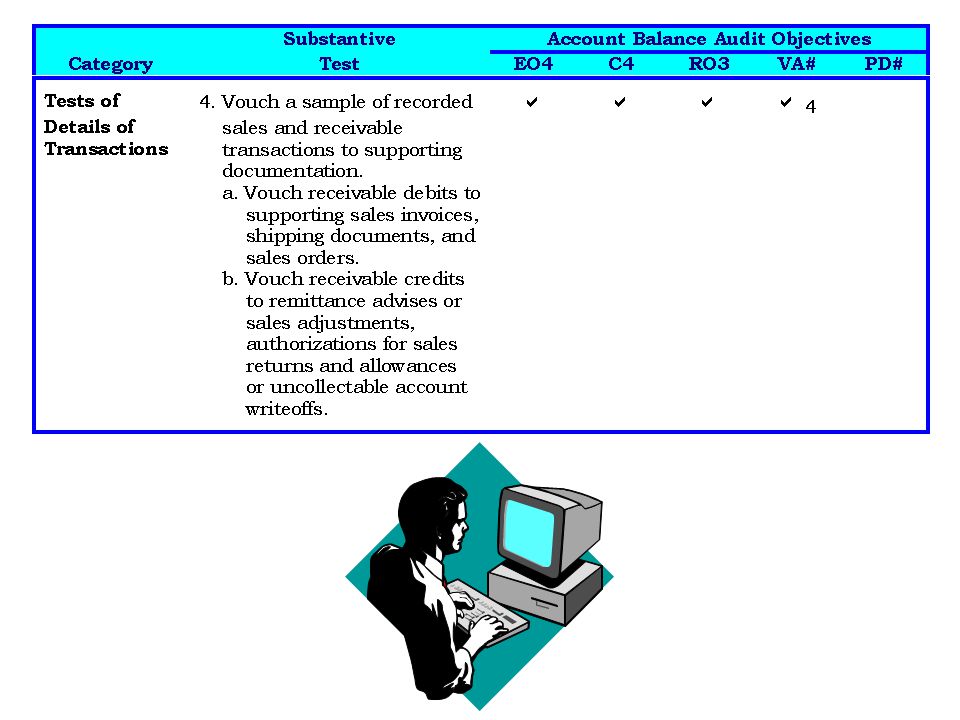

Substantive Tests of Accounts Receivable Designing Substantive Tests The next step is to finalize the audit program to achieve the specific audit objective for each category of account balance assertions. The specific objectives addressed are the ones listed in the Account Balance Audit Objectives column of Figure 14-9.

33

Correlation of Risk Components — Accounts Receivable Assertions Figure 14-9

42

Substantive Tests of Accounts Receivable Confirm Receivables Confirmation of accounts receivable involves direct written communication between individual customers and the auditor. This substantive test is used extensively by the auditor.

43

Generally Accepted Auditing Procedures The confirmation of receivables is a generally accepted auditing procedure. AU 330, The Confirmation Process (SAS 67), states that there is an presumption that the auditor will request the confirmation of receivables during an audit unless: 1. Accounts receivable are immaterial to the financial statements. 2. The use of confirmations would be ineffective as an audit procedure. Substantive Tests of Accounts Receivable

, states that there is an presumption that the auditor will request the confirmation of receivables during an audit unless: 1. Accounts receivable are immaterial to the financial statements. 2. The use of confirmations would be ineffective as an audit procedure. Substantive Tests of Accounts Receivable.")

44

3. The auditor’s combined assessment of inherent risk and control risk is low and that assessment, in conjunction with evidence expected to be provided by analytical procedures or other substantive tests of details, is sufficient to reduce audit risk to an acceptably low level for the applicable financial statement assertions.

45

Forms of Confirmation There are 2 forms of confirmation request: 1.the positive confirmation, which requires the debtor to respond whether or not the balance shown is correct, 2.the negative confirmation, which requires the debtor to respond only when the balance shown is incorrect. Substantive Tests of Accounts Receivable

46

Generally accepted auditing standards do not require that the auditor perform value-added services. The client and its board of directors usually want to take full advantage of the auditor’s knowledge of -- – The entity’s competitive advantage or disadvantage – Business risks – Potential improvements in information system – Potential steps to improve business performance Value-Added Services

47

In the process of performing the audit, the auditor may benchmark company performance against others in the industry. The auditor might address, for example, whether: 1. The company is effectively utilizing assets to generate sales based on a ratio of sales to total assets. 2. Receivables are growing faster than sales, thereby consuming valuable cash flows. 3. The company has appropriately addressed risks associated with a changing or maturing market place. 4. The company is bringing successful new product innovations to market and is enjoying a high percentage of revenues from new products, relative to the competition. Value-Added Services

48

CHAPTER 14 AUDITING THE REVENUE CYCLE

49

CopyrightCopyright Copyright 2001 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make backup copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Similar presentations