Download presentation

Presentation is loading. Please wait.

1

Sri Lanka Tea Industry Hasitha De Alwis Director (Promotion)

Sri Lanka Tea Board

2

Sri Lanka – Wonder of Asia

Island is united ending 30 years long conflict. Multi-ethnic, multi-cultural, multi-religious and multi-linguistic nation once again in harmony. Immense opportunities for sustainable growth in all sectors and tea industry is no exception. Probably the safest country today in South Asia. Peace dividends results in leap-frog development in Sri Lanka’s infra-structure & other sectors of economy.

3

INTRODUCTION Sri Lanka tea industry proudly celebrates 145 years of commercial history in 2012. Tea industry continues to occupy a pivotal position in terms of foreign exchange earnings & employment. Tea export earnings reached USD 1.5 Billion in 2011 a historical high contributing 15% to the nation’s foreign exchange. Generating 65% of export agriculture revenue, tea industry contributes approx. 2% of island’s GDP. With 2 Million employed directly & indirectly 10% of the population of Sri Lanka depends on the industry.

4

AGRO-CLIMATIC TEA GROWING REGIONS OF SRI LANKA

5

SRI LANKA TEA PRODUCTION ELEVATION WISE (Mn. KGS)

Year High Grown (%) Mid Low Total 2005 80.3 25 55.1 18 181.7 57 317.1 2006 74.7 24 51.6 17 184.5 59 310.8 2007 72.5 54.4 177.7 304.6 2008 84.4 26 49.0 15 185.3 318.7 2009 72.8 44.7 173.1 60 290.6 2010 79.1 56.1 196.2 331.4 2011 79.2 52.5 16 196.6 328.4

Mid. Low. Total")

6

CATEGORY-WISE TEA PRODUCTION (Mn.KGS)

2006 (%) 2007 2008 2009 2010 2011 Orthodox 288 93 283 297 271 310 94 303 92 CTC 18 5 16 17 22 7 Green Tea 3 1 4 2 Others - Total 311 100 305 319 291 331 100 328

Orthodox CTC Green Tea Others. - Total")

7

AREA OF TEA PLANTED IN SRI LANKA

Elevation Planted (Ha) Share High Grown 41,137 19% Mid Grown 71,018 32% Low Grown 109,814 49% Total 221,969 100

Share. High Grown. 41, % Mid Grown. 71, % Low Grown. 109, % Total. 221,")

8

SRI LANKA TEA EXPORTS (Mn. KGS)

2006 2007 2008 2009 2010 2011 Bulk 197.8 179.9 178.0 164.6 176.8 Packets 79.4 72.7 84.3 75.5 89.8 95.8 Tea Bags 19.1 22.0 20.3 18.7 25.7 24.6 Others 18.6 19.7 21.2 1.8 2.9 Re- Exports 12.5 15.6 10.6 20.5 Total 327.4 309.9 319.8 290.6 305.7 323.7 Value Billion USD 0.882 1.01 1.26 1.18 1.37 1.51

9

RE-EXPORTS (CEYLON TEA BLENDED WITH OTHER ORIGINS)

Year Qty (MT) Value (Rs. Mn) (USD Mn) 2005 11,456 4,154 41.33 2006 12,499 5,330 51.20 2007 15,597 6,617 59.80 2008 18,577 10,683 98.61 2009 10,574 5,089 44.27 2010 18,607 11,567 102.30 2011 20,529 13,363 118.30

Value. (Rs. Mn) (USD Mn) ,456. 4, ,499. 5, ,597. 6, , , ,574. 5, , , , ,")

10

Tea Imports to Sri Lanka

Year Quantity (Kgs) Value (Rs. Million ) (USD M.) 2007 13,683,732 3,141.6 28.56 2008 14,598,248 3,754.8 34.13 2009 9,960,129 2,979.4 27.08 2010 12,172,753 3,768.0 34.25 2011 11,406,044 3,770.4 34.28

Value. (Rs. Million ) (USD M.) ,683,732. 3, ,598,248. 3, ,960,129. 2, ,172,753. 3, ,406,044. 3,")

11

Tea Imports to Sri Lanka (Country Wise)

Qty in Kgs. 2009 2010 2011 India 4,708,695 4,776,141 4,353,513 China 1,755,521 2,802,873 2,895,761 Kenya 2,867649 3,871,167 3,690,453 Vietnam 240,725 352,203 97,909 Indonesia 203,260 207,068 182,620 Malawi 129,580 143,104 150,660 Germany 33,080 10,805 23,898 Taiwan 8,888 7392 - Japan 5,600 900 U.K 5,130 9980 Nepal 2,001 1100 1250 TOTAL 9,960,129 12,172,753 11,406,044

12

MAJOR DESTINATIONS FOR CEYLON TEA

2009 Country Qty. % Russia 42.4 15.1 UAE 30 10.7 Syria 29.4 10.5 Iran 27.7 9.9 Turkey 15.7 5.6 Jordan 13.4 4.8 Kuwait 10.1 3.6 Iraq 9.8 3.5 Japan 9.5 3.4 Libya 8.1 2.9 2010 Country Qty. % Russia 45.5 15.2 UAE 29.6 9.9 Iran 27.6 9.2 Syria 26.3 8.8 Turkey 18.4 6.2 Jordan 17.3 5.8 Iraq 13.6 4.6 Libya 10.9 3.7 Kuwait 10.8 3.6 Japan 10.3 3.4 2011 Country Qty % Russia 47.3 14.8 Iran 30.8 9.6 Syria 28.5 8.9 Iraq 22.2 6.9 UAE 21.5 6.7 Turkey 18.9 5.9 Azerbaijan 11.8 3.7 Japan 11.3 3.5 Kuwait 9.1 2.8 Ukraine 7.8 2.4

13

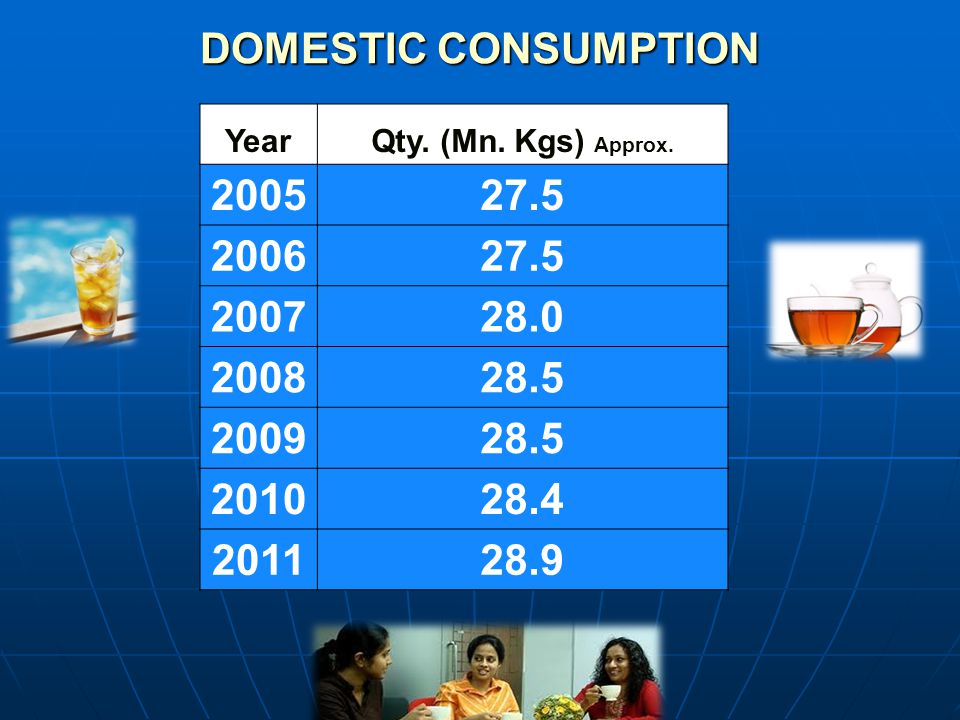

DOMESTIC CONSUMPTION Year Qty. (Mn. Kgs) Approx. 2005 27.5 2006 2007 28.0 2008 28.5 2009 2010 28.4 2011 28.9

14

DISTRIBUTION CHANNELS

Type Percentage Supermarkets % Grocery retailing % Convenience stores % Tea Shops / Tea Houses % Others %

15

TYPE OF PRODUCTS (Domestic Market )

Volume Value Loose Tea 68% 67% 61% 59% Packet Tea 30% 36% 37% Tea Bags 2% 3% 4%

16

Value Growth on Consumer Prices for Share of Throat

Item Share of Throat Value Growth (per Annum) Average Price Tea 26.5% 9% Rs. 715/Kg Coffee 2.5% 22% Rs. 1,335/Kg Malt 15.5% 23% Rs.167/Ltr Soft Drinks (Carbonated) 36.0% 43% Rs.124/Ltr Others 19.5%

Average Price. Tea. 26.5% 9% Rs. 715/Kg. Coffee. 2.5% 22% Rs. 1,335/Kg. Malt. 15.5% 23% Rs.167/Ltr. Soft Drinks (Carbonated) 36.0% 43% Rs.124/Ltr. Others. 19.5%")

17

Household Expenditure

2009/2010 (Rs. 1,750B.) Monthly Household Expenditure Rs. 32,446/-

Monthly Household. Expenditure Rs. 32,446/-")

18

MACRO ECONOMIC FUNDAMENTALS IN SRI LANKA 2005 VS. 2011

(Est/Prov) Real GDP Growth 6.2 8.3 GDP (US $) 24.4 59.1 GDP per capita (US $) 1,241 2,830 Trade : Exports (US$ bn) 6.3 10.5 Imports (US $ bn) 8.9 20.0 Workers’ Remittances (US$ bn) 1.9 5.2 Tourist Arrivals (‘000) 549 850 Earnings from Tourism (US $ bn) 0.3 0.8 FDI (US$ bn) 1.0

Real GDP Growth GDP (US $) GDP per capita (US $) 1,241. 2,830. Trade : Exports (US$ bn) Imports (US $ bn) Workers’ Remittances (US$ bn) Tourist Arrivals (‘000) Earnings from Tourism (US $ bn) FDI (US$ bn) 1.0.")

19

Hasitha De Alwis Director (Promotion) Sri Lanka Tea Board

Thank You Hasitha De Alwis Director (Promotion) Sri Lanka Tea Board

Sri Lanka Tea Board.")

Similar presentations

, MBS. MANAGING DIRECTOR TEA BOARD OF KENYA May 2010.>")

TEA DIRECTORATE Samuel Ogola Technical Services Manager-Tea Directorate.>")

2.UNEMPLOYMENT 3.INFLATION 4.INCOME PER CAPITA 5.BALANCE OF PAYMENTS: EXPORTS.>")

>")

>")