Download presentation

Presentation is loading. Please wait.

1

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Standard Costs and Variance Analysis Chapter Ten & Eleven

2

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Standard Costs Standards are benchmarks or “norms” for measuring performance. Two types of standards are commonly used. Quantity standards specify how much of an input should be used to make a product or provide a service. Cost (price) standards specify how much should be paid for each unit of the input.

standards specify how much should be paid for each unit of the input..")

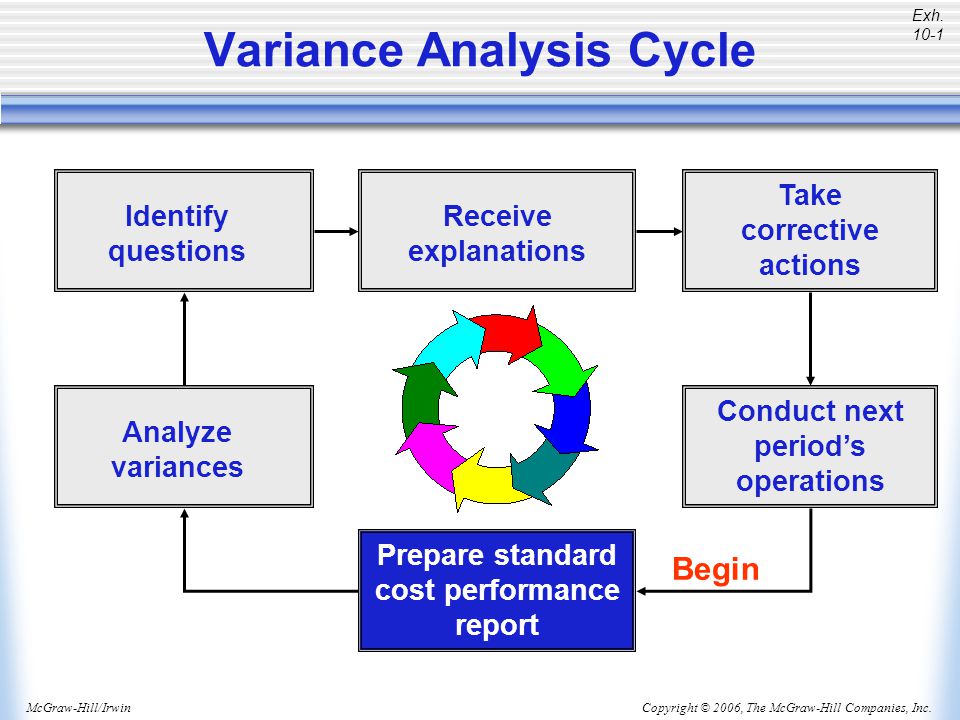

3

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Variance Analysis Cycle Prepare standard cost performance report Analyze variances Begin Identify questions Receive explanations Take corrective actions Conduct next period’s operations Exh. 10-1

4

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Standard Cost Card – Variable Production Cost A standard cost card for one unit of product might look like this:

5

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin A General Model for Variance Analysis Variance Analysis Price Variance Difference between actual price and standard price Quantity Variance Difference between actual quantity and standard quantity

6

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin A General Model for Variance Analysis (AQ × AP) – (AQ × SP) (AQ × SP) – (SQ × SP) AQ = Actual Quantity SP = Standard Price AP = Actual Price SQ = Standard Quantity Price VarianceQuantity Variance Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price

– (AQ × SP) (AQ × SP) – (SQ × SP) AQ = Actual Quantity SP = Standard Price AP = Actual Price SQ = Standard Quantity Price VarianceQuantity Variance Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price")

7

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Budget Variance Volume Variance FR = Standard Fixed Overhead Rate SH = Standard Hours Allowed DH = Denominator Hours SH × FR Actual Fixed Fixed Fixed Overhead Overhead Overhead Incurred Budget Applied Fixed Overhead Variances DH × FR

8

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Illustration

9

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Variance Analysis

10

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Responsibility for Labor Variances Production Manager Production managers are usually held accountable for labor variances because they can influence the: Mix of skill levels assigned to work tasks. Level of employee motivation. Quality of production supervision. Quality of training provided to employees.

11

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Efficiency Variance Controlled by managing the overhead cost driver. Variable Overhead Variances – A Closer Look

12

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Fixed Overhead Variances – A Closer Look Budget Variance Results from spending more or less than expected for fixed overhead items.

13

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Volume Variance – A Closer Look Volume Variance Results when standard hours allowed for actual output differs from the denominator activity. Unfavorable when standard hours < denominator hours Favorable when standard hours > denominator hours

14

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin Variance Analysis and Management by Exception How do I know which variances to investigate? Larger variances, in dollar amount or as a percentage of the standard, are investigated first.

15

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin End of Chapter 10

Similar presentations