Download presentation

Presentation is loading. Please wait.

1

Probabilistic Asymmetric Information and Lending Relationships Philip Ostromogolsky Yale School of Management

2

Background Often banks lend to small business customers over several periods. Banks may offer a customer a first-time loan with the possibility that the customer may be able to get another, future loan from the bank if he does a good job repaying the first loan. Over the period of the first loan the bank can monitor his borrower, learn about him, and use that information to extend or curtail future credit. More information than is revealed by simply observing whether or not the customer repays his first-time loan.

3

How do banks compete over small business borrowers? They bargain, just like stock brokers or shoppers at a public market. This can be modeled as an English auction. Banks are the bidders. The potential small business borrower is the auctioneer.

4

A Simple Story About an Auction

5

?

7

Bill I’m coming back to the White House

8

Ben Bill I’m coming back to the White House What would Greenspan do?

9

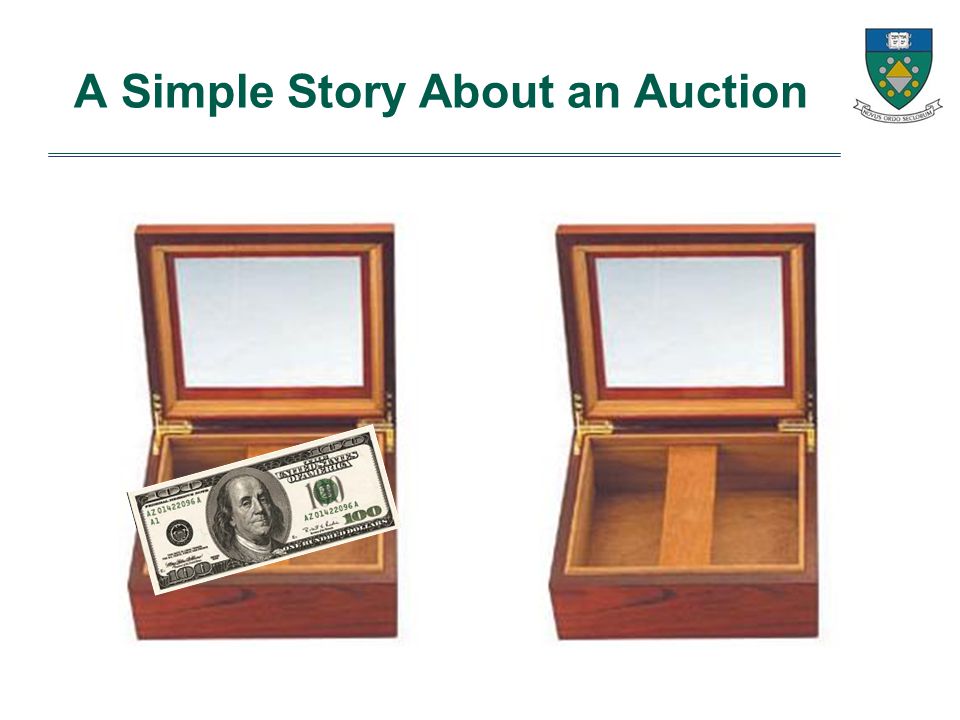

A Simple Story About an Auction

10

The auctioneer says: We will now conduct the auction, the highest bid ≥ 0 wins. There is some probability p* [0,1] that the box contains a $100 bill. I am not going to publicly disclose p*. But, I will tell you that p* ~U[0,1] I like Bill, so I am going to walk over to Bill and whisper in his ear the value of p*. Ben is not going to be told anything about p*. The auctioneer walks over to Bill and whispers the value of p* into his ear.

11

A Simple Story About an Auction Bill is informed Ben is uninformed Bill makes the first bid Bill’s bid = $0.00 What should Ben do?

12

A Simple Story About an Auction Ben Thinks: Suppose probability that the box contains $100 = p* = 0.5, and of course Bill knows this. Bill knows that the expected value of the box’s contents = 100p* = 50. Bill will continue bidding up until Bill’s bid = 50. If at some point Bill bids 50 and I then bid 51, I will win. When the auctioneer announces that I have won my expected profit will = 100p* – my bid = 100*0.5 – 51 = 50 – 51 = -1. So, when I am announced as the winner I will expect to have a profit of -1 < 0.

13

A Simple Story About an Auction Ben Thinks: If at some point I (Ben) bid 50, I will win. When the auctioneer announces that I have won my expected profit will = 100p* – my bid = 100*0.5 – 50 = 50 – 50 = 0. So, when I am announced as the winner I will expect to have a profit of 0. If I ever bid some bid, Ben’s bid < 50, I of course will not win. Thus, if p* = 50 and I don’t know that, I can never win, and I might actually lose!!!

14

A Simple Story About an Auction Ben Thinks: As of right now, the last bid, was Bill’s bid = 0. I don’t actually know p*. The lowest I could bid is $1. If p* > 0.01 then the best I could hope for would be go get a profit of π = 0. If p* < 0.01, then my profit would = π = 100p* – 1 < 100*0.01 – 1 < 0 And, I would lose money!!! Pr(p* < 0.01) = 0.01. So, if I bid $1, the expected value of my profits = E[π] = 0.01(100p* - 1) = p* - 0.01 < 0 !!!

= So, if I bid $1, the expected value of my profits = E[π] = 0.01(100p* - 1) = p* < 0 !!!.")

15

A Simple Story About an Auction Thus, Ben drops out of the auction and Bill obtains the contents of the box for a winning bid of $0. Bill’s interim expected profits from this game are thus E[π|p*] = 100p* – 0 = 100p* Bill’s ex ante expected profits from this game are E p* [E[π|p*]] = 100E[p*]– 0 = 50.

16

A Simple Story About an Auction Bill’s knowledge of p* does not just let him make a more accurate forecast of the expected value of the contents of the box. this is an old idea. It also gives him a credible deterrence device, through which he can force his opponent to exit the auction, and ensure himself maximum possible profits. this is new idea.

17

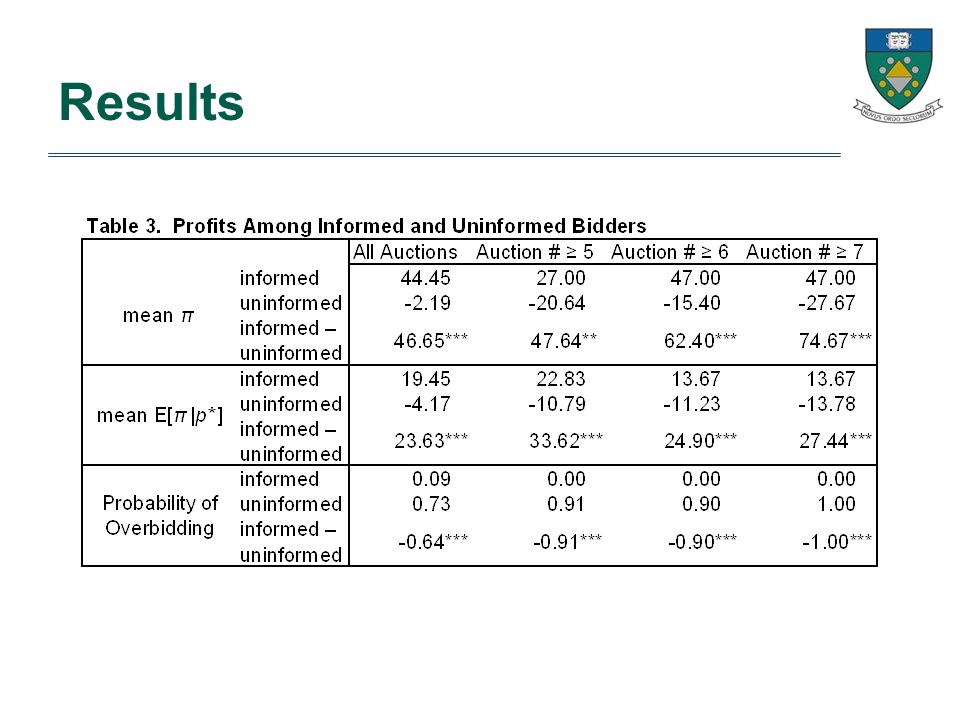

The Experiment 4 Simultaneous Auctions run by Boudhayan, Foong Soon, Michael, and me. Each auction had 3 bidders. Selection of informed bidder, randomization of p* and realization of box contents performed using random draws of poker chips. Induce risk neutrality by giving each student an initial endowment of 10,000 point. Incentivize strategic behavior by offering prizes for the 3 students having the most aggregate profit.

18

Results – Looks Good

19

Results – Some Participants Seem Almost Risk Loving

20

Results

Similar presentations

auctions Vincent Conitzer v() = $5 v() = $3.>")

www.econ.ucsb.edu Or at www.econ.ucsb.edu\~tedbwww.econ.ucsb.edu\~tedb.>")

(4/27) Final (50%) (6/22) Term grades based on relative ranking. Mon 1:30-2:00 ( 社科 757)>")

Nikos Nikiforakis The University of Melbourne.>")