Download presentation

Presentation is loading. Please wait.

1

Corporate Finance Lecture 2

2

Outline for today The application of DCF in capital budgeting The application of DCF in capital budgeting –Identifying Cash Flows –Calculating Cash Flows –Example: Blooper Industries

3

Incremental Cash Flows Cash flows matter — not accounting earnings. Cash flows matter — not accounting earnings. Sunk costs don ’ t matter. Sunk costs don ’ t matter. Incremental cash flows matter. Incremental cash flows matter. Opportunity costs matter. Opportunity costs matter. Side effects like synergy and erosion matter. Side effects like synergy and erosion matter. Taxes matter: we want incremental after- tax cash flows. Taxes matter: we want incremental after- tax cash flows. Inflation matters. Inflation matters.

4

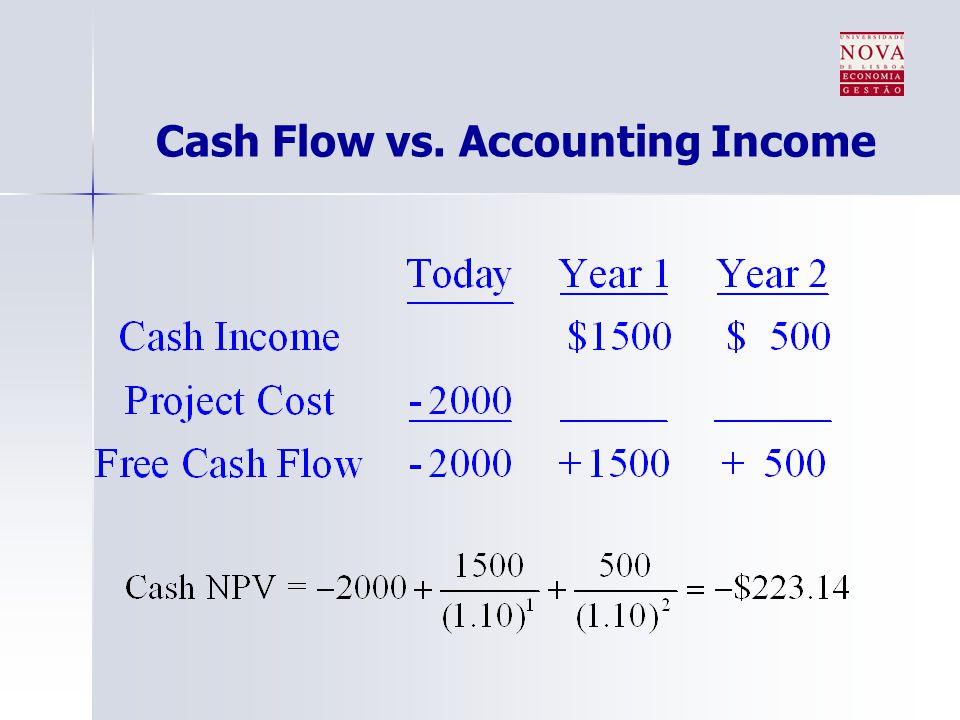

Cash Flow vs. Accounting Income Discount actual cash flows instead of accounting profits Discount actual cash flows instead of accounting profits Example A project costs $2,000 and is expected to last 2 years, producing cash income of $1,500 and $500 respectively. The cost of the project can be depreciated at $1,000 per year. Given a 10% required return, compare the NPV using cash flow to the NPV using accounting income.

5

Cash Flow vs. Accounting Income

7

Incremental Cash Flows Discount incremental cash flows Discount incremental cash flows Important question: Would the cash flow still exist if the project does not exist? Incremental Cash Flow cash flow with project cash flow without project = -

8

Separation of Investment & Financing Decisions When valuing a project, should you consider the cash flows from financing decisions? When valuing a project, should you consider the cash flows from financing decisions?

9

Project Evaluation Operating cash flow (+) Sales revenue (-) operating costs (-) Tax (%) Investment cash flow (-) Capital Expenditure (Investment in machine) (-) Opportunity cost (-) Change in net working capital Net cash flow

Sales revenue (-) operating costs (-) Tax (%) Investment cash flow (-) Capital Expenditure (Investment in machine) (-) Opportunity cost (-) Change in net working capital Net cash flow")

10

Blooper Industries (,000s)

")

11

Blooper Industries Cash Flow From Operations (,000s)

")

12

Blooper Industries Net Cash Flow (entire project) (,000s) NPV @ 12% = $4,222,350

(,000s) 12% = $4,222,350")

Similar presentations