Download presentation

Presentation is loading. Please wait.

1

Xavier Sala-i-Martin Columbia University July 2008

6

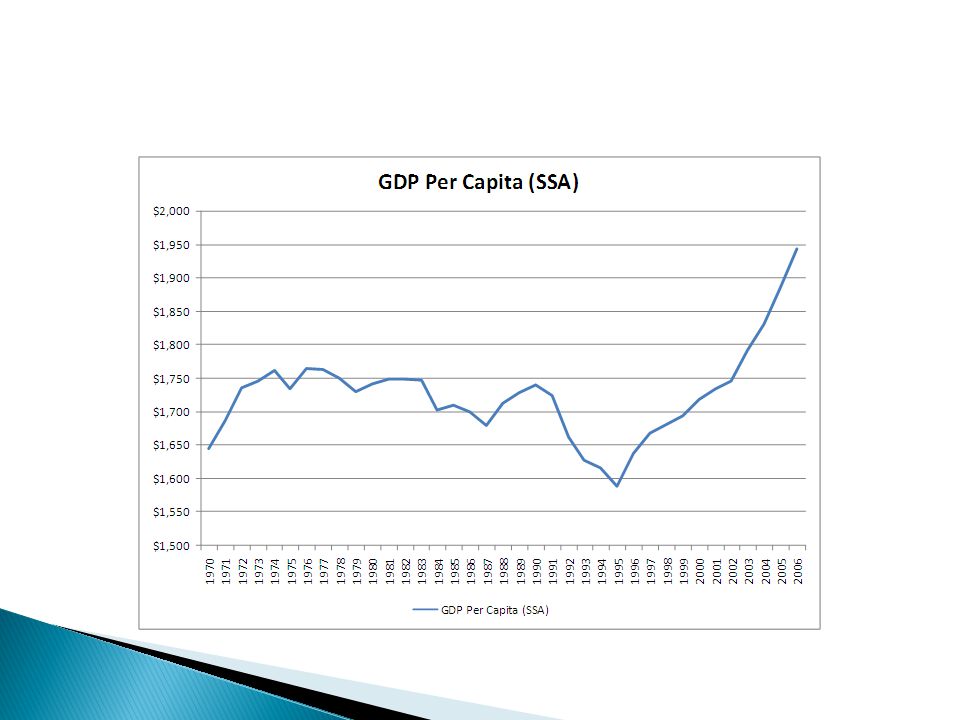

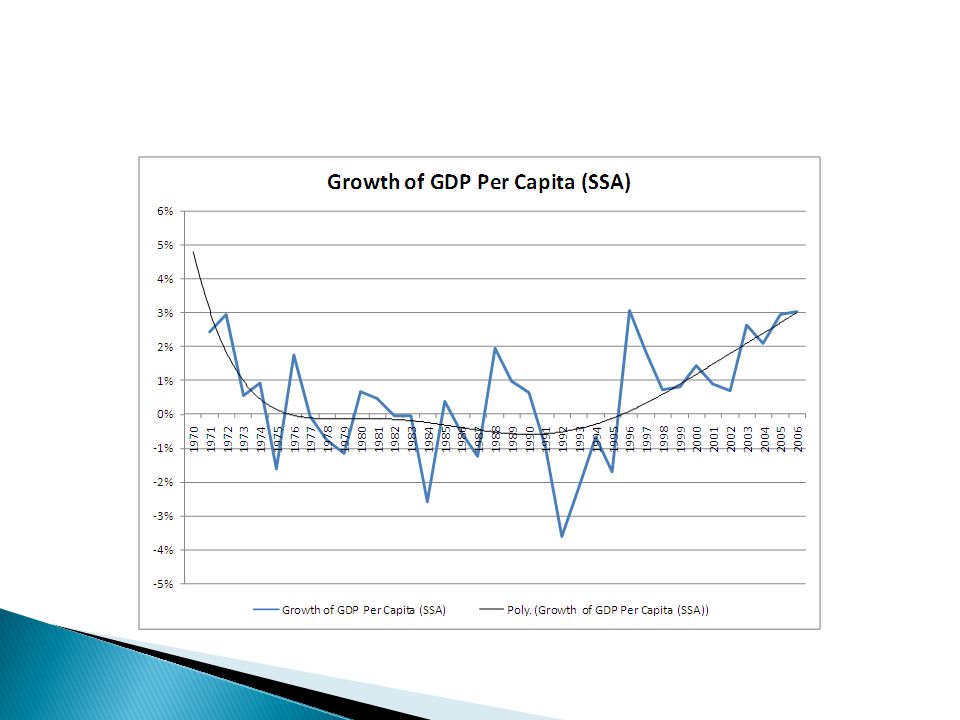

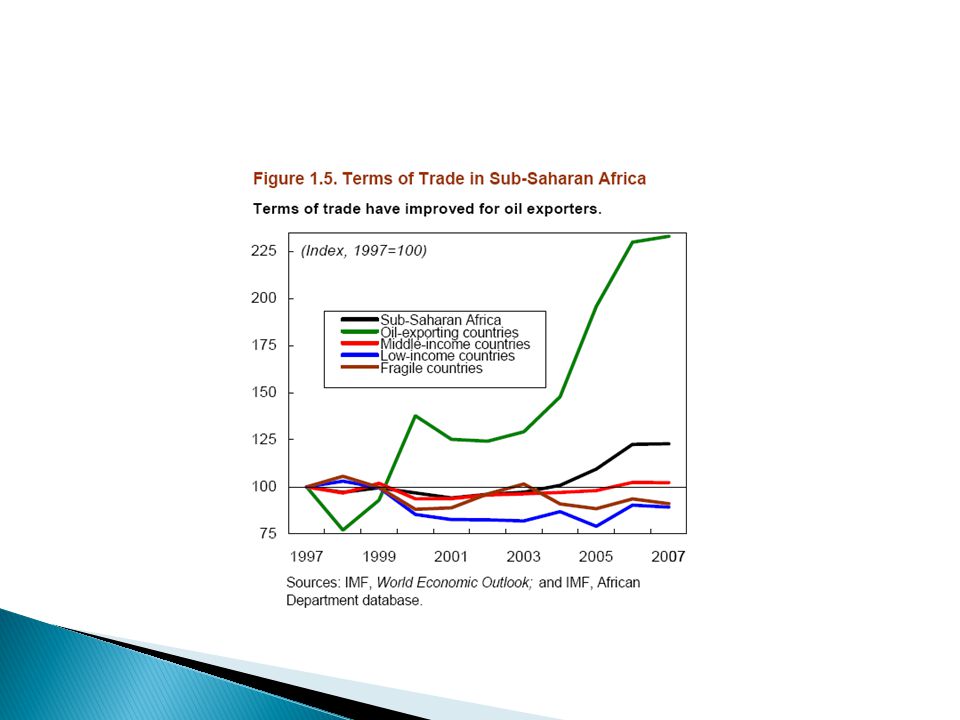

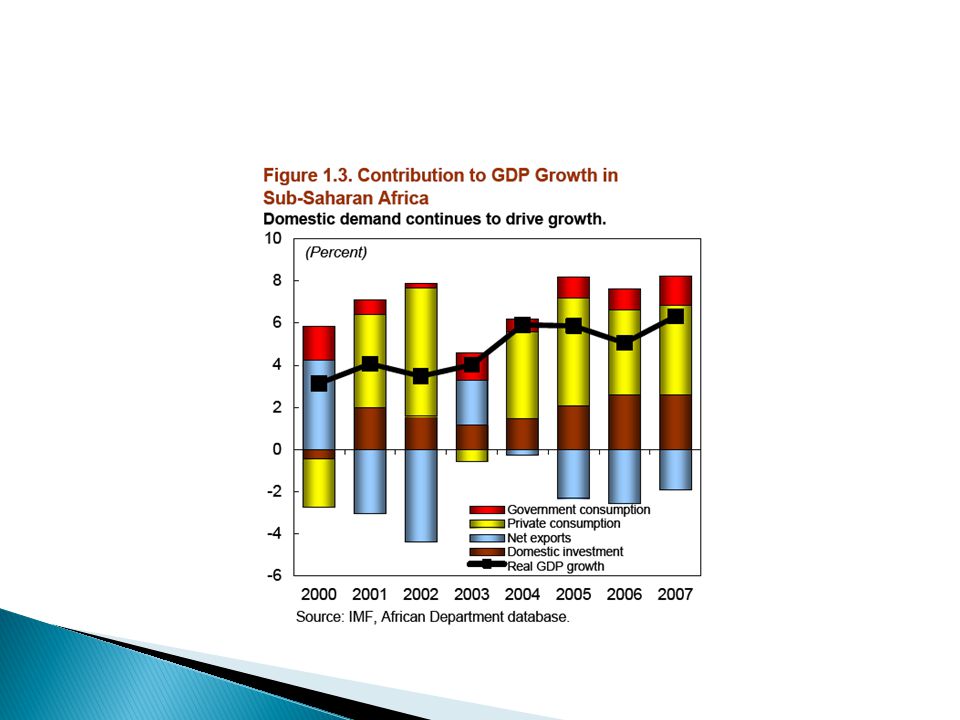

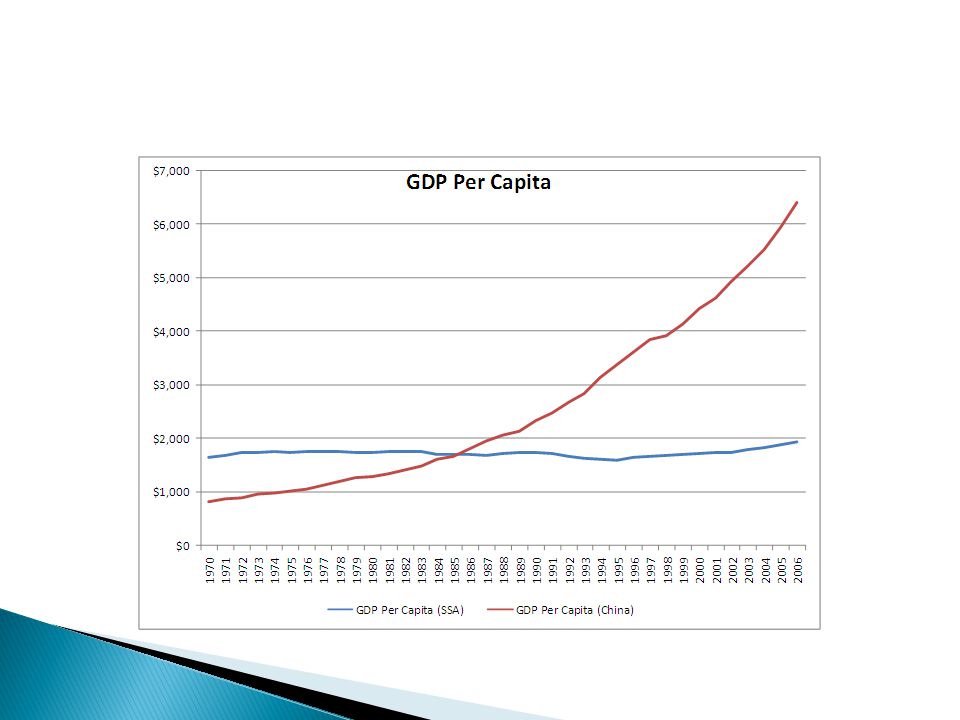

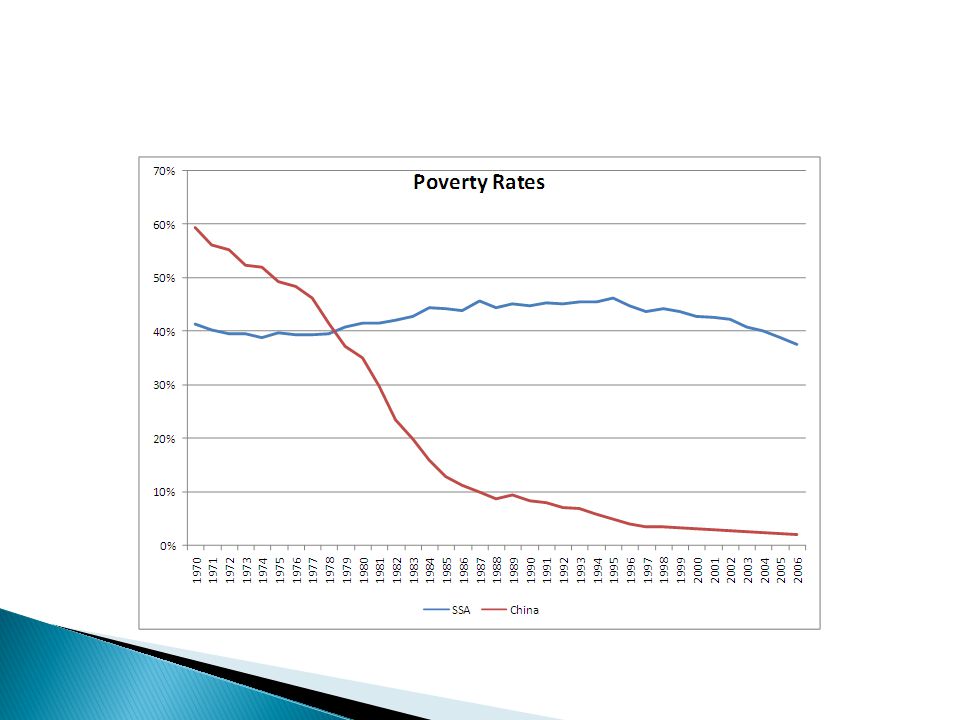

There has been some success since mid 1990s (even though the MDG people want us to believe that Africa is a disaster because it is far away from MDGs).

.")

7

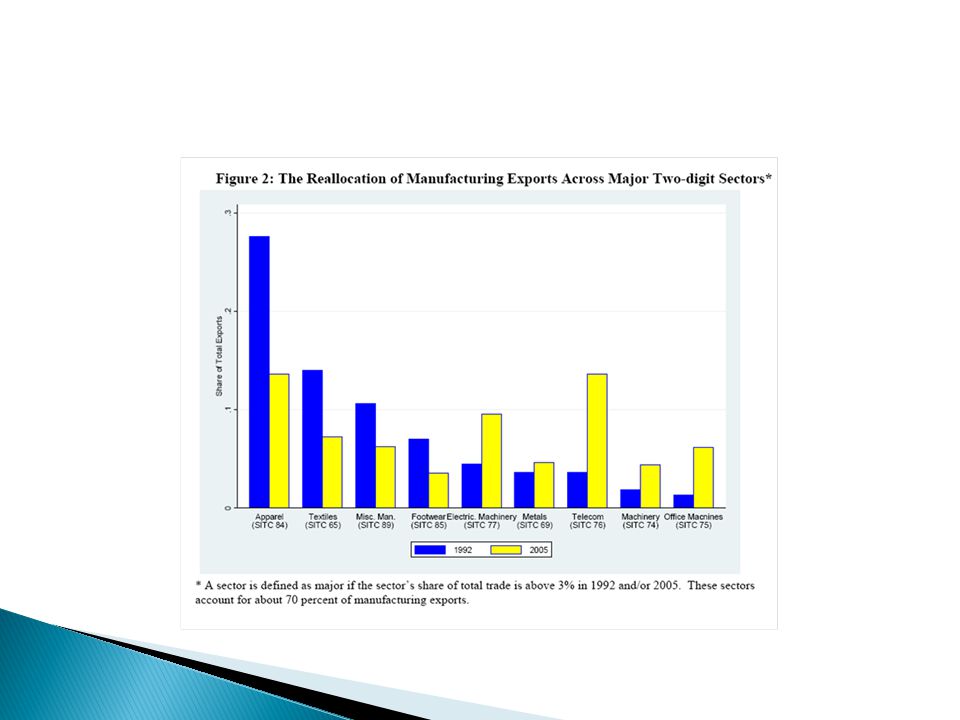

Of course: ◦ Part of it is commodity boom ◦ But non-oil exporters have not had an improvements in TOT (they import oil!): growth does not come from exports of commodities but domestic demandnon-oil exporters have not had an improvements in TOTdomestic demand Of course: ◦ “Africa” does not mean anything as a unit: lots of heterogeneity: landlocked vs non-landlocked oil vs non-oil democracies vs non-democracies war vs non-war). I think there are four factors that should be cause for optimism

8

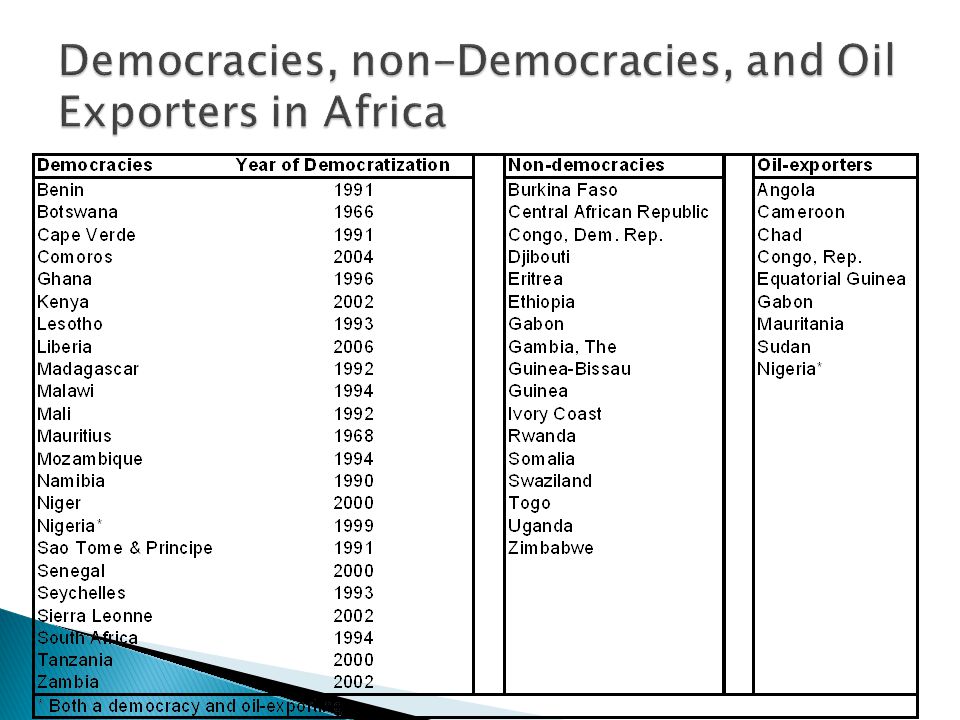

1989 – 3 democracies 2006 – 23 democracies Reasons: ◦ End of cold war ◦ End of SA apartheid ◦ Both of them brought more freedom. Some are fragile (Kenya), but still a change.

, but still a change..")

9

Note: To qualify as a democracy, a country must score 4 or less on the combined Freedom House score AND 2 or more on the polity score from Polity IV.

14

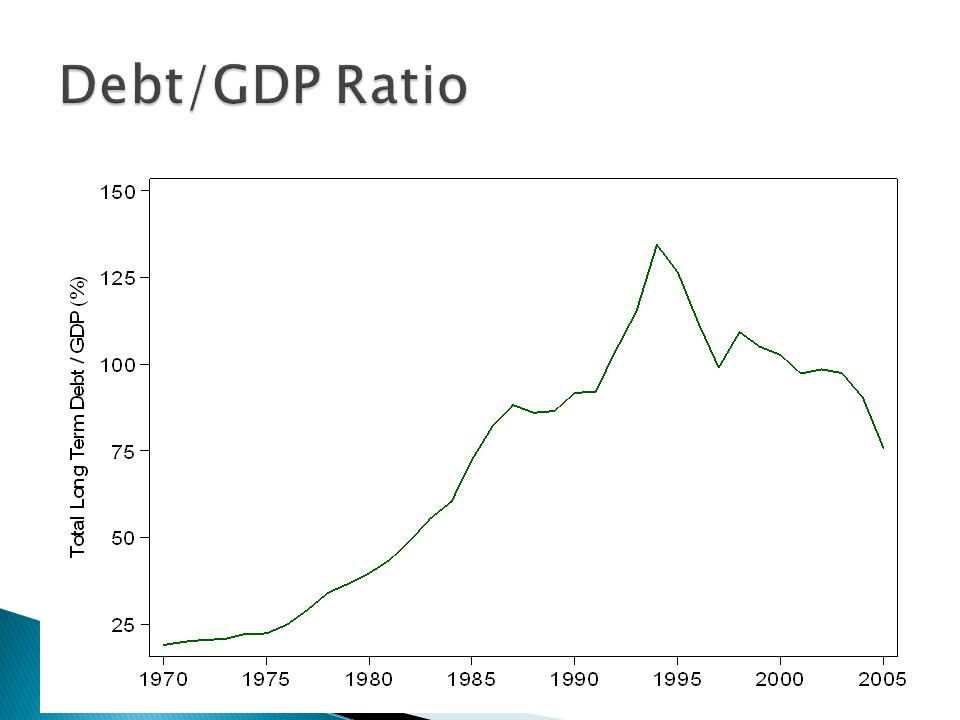

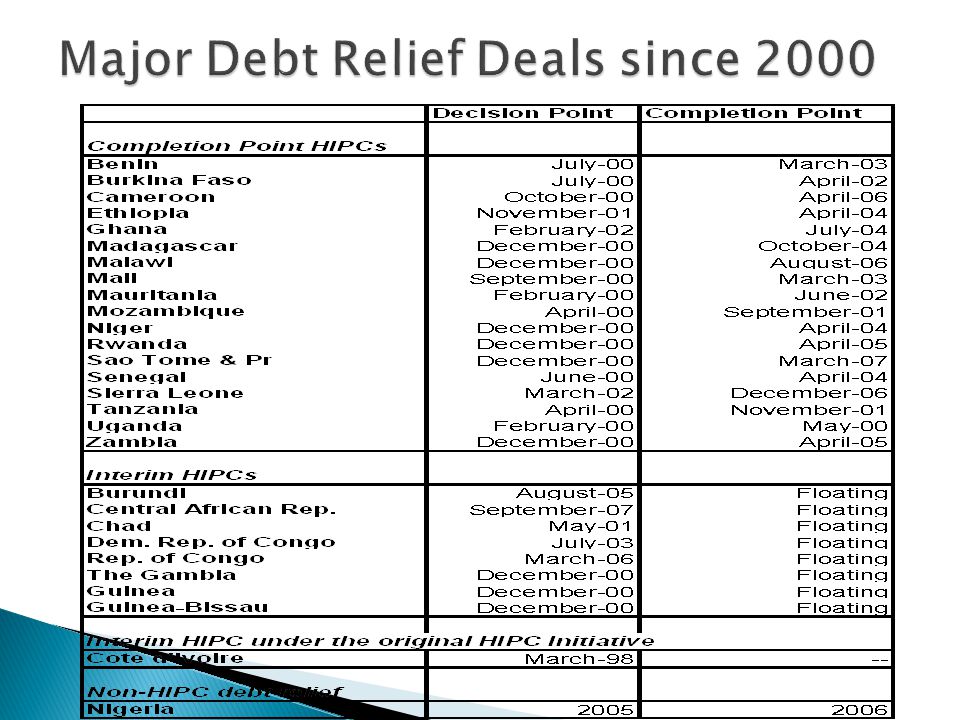

HIPC initiative, etc: DEBT is no longer an issue

17

Debt relief frees up resources Debt relief changes the relation with the donor community: African countries no longer need the IMF and the WB ◦ Note: Opens up the role for China Countries take up their own responsibilities and may make their own policies and reforms with fewer constraints

18

Example: Cell Phone penetration New businesses associated with these technologies (creativity, innovation, entrepreneurship) Potential “skipping” of stage of development (no fixed telephony) New Means of payments (sms-transfers with potential implications for international capital flows: sms-remittances)

Potential skipping of stage of development (no fixed telephony) New Means of payments (sms-transfers with potential implications for international capital flows: sms-remittances)")

19

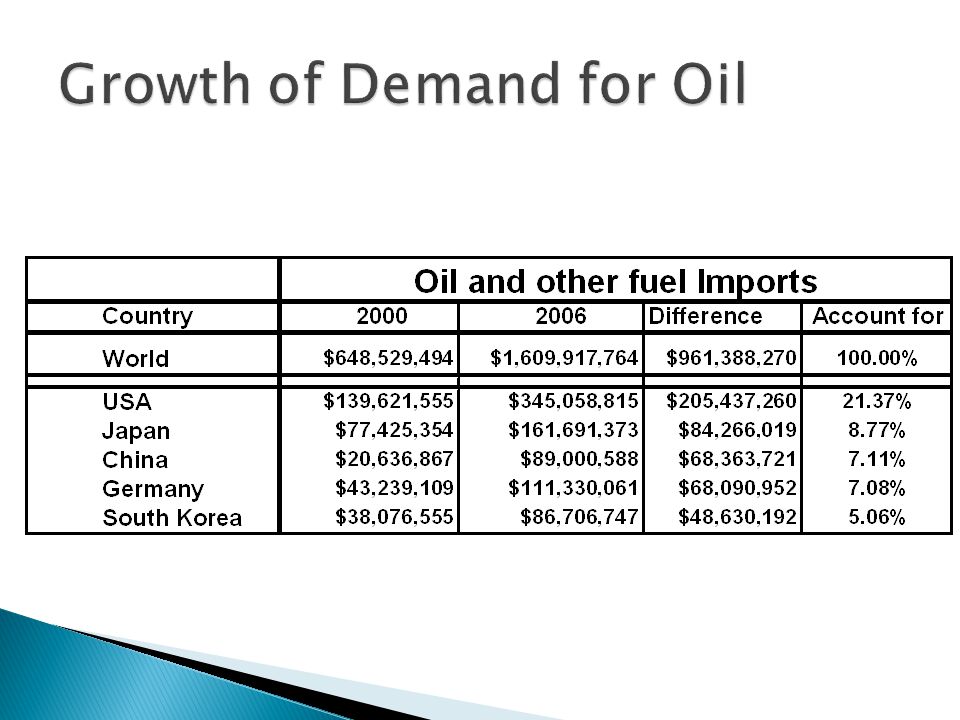

In General (for the whole world), China is: ◦ A customer ◦ A competitor: Increasingly in “sophisticated manufacturing” (electronics, telecoms, transportation,…): maybe not direct competition to Africa (African manufactures are below in the sophistication ladder)sophisticated manufacturing ◦ A Lender (in exchange for future supplies of primary commodities) A future debt crisis? ◦ A Partner (Investment) ◦ A Financial Investor (Massive Sovereign funds, and it is not clear what they will do with them) ◦ A Contributor to increase price of commodities Main increase in world demand of oil come from USA, but for the rest of materials it is China ◦ A Contributor to decrease price of manufacturing (so lower inflation) ◦ A “Global Hunter for Energy” ◦ A Substitute for IFIs when it comes to aid

◦ A Financial Investor (Massive Sovereign funds, and it is not clear what they will do with them) ◦ A Contributor to increase price of commodities Main increase in world demand of oil come from USA, but for the rest of materials it is China ◦ A Contributor to decrease price of manufacturing (so lower inflation) ◦ A Global Hunter for Energy ◦ A Substitute for IFIs when it comes to aid.")

20

FDI is still dominated by South Africa and the UK But the fact that China is moving towards Africa ◦ They may be better equipped to do business in economies with fewer resources, with corrupt local officials, with less regard for workers rights than Europeans and Americans. And they do not have former colonial ties (or slavery trade guilt) This is an important indicator to others ◦ The move in the commodities sector, but also in manufacturing ◦ Europeans and US are monitoring and may disembark soon Anecdotal evidence (investment banks –JP Morgan- and hedge funds are increasingly coming to Columbia GSB looking for experts in African business)

This is an important indicator to others ◦ The move in the commodities sector, but also in manufacturing ◦ Europeans and US are monitoring and may disembark soon Anecdotal evidence (investment banks –JP Morgan- and hedge funds are increasingly coming to Columbia GSB looking for experts in African business).")

21

A Model of development (a mirror) ◦ It Can Be Done!!! It Can Be Done ◦ How it can be done: Commitment to education (good) Embrace globalization (good) Maintain role of state in planning/directing/Clusters (because of China, most countries are setting up “competitiveness councils” where PPP are discussed) Not clear this is a good idea since governments, still, are not equipped to “pick winners” Entrepreneurial spirit / business as opposed to aid as a way to develop

Embrace globalization (good) Maintain role of state in planning/directing/Clusters (because of China, most countries are setting up competitiveness councils where PPP are discussed) Not clear this is a good idea since governments, still, are not equipped to pick winners Entrepreneurial spirit / business as opposed to aid as a way to develop.")

22

Is this time the real turning point for Africa?

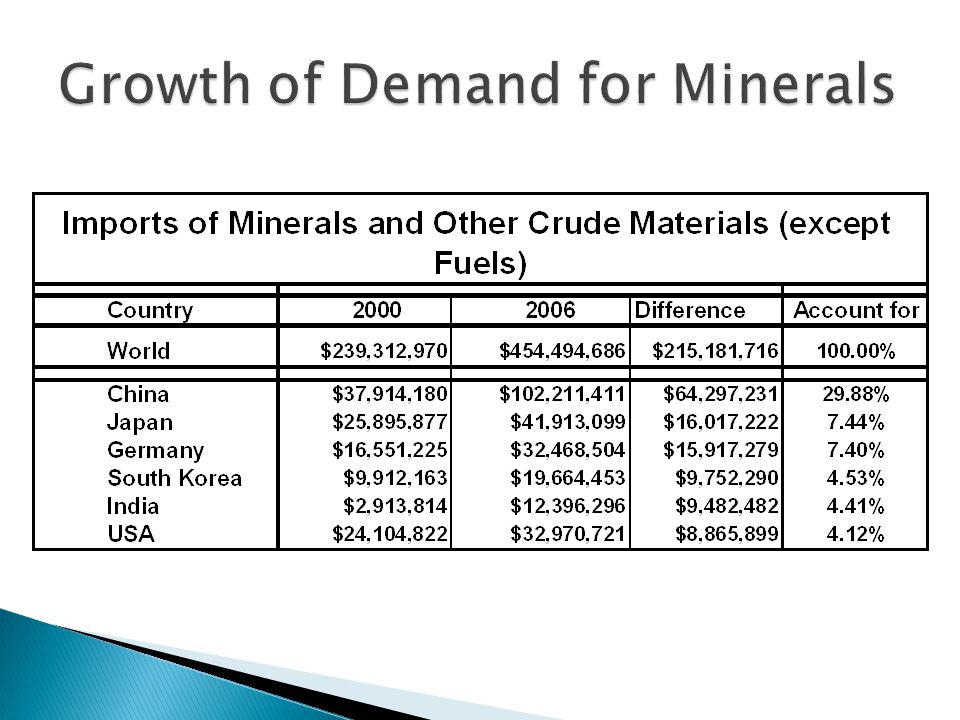

33

Crude Oil and Related Imports: China and Major Importers, 2000-2006 Quantity of Kilograms ___________________________________________________________ Country 2000 2006 __________________________________________________________ China 70,265,318 145,174,839 USA 464,801,236 861,259,894 Japan 211,981,499 208,694,845 Germany 105,292,884 109,503,671 South Korea 120,651,685 120,152,663 _________________________________________________________ Source: COMTRADE, 2008.

34

Nov. 2007 →

Similar presentations

lending Lending to developing countries on non- concessional terms (with rates of interest and.>")

Lecturer: Dr B. M. Nowbutsing Topic: Open economy macroeconomics.>")

>")

Alphametrics Ltd. The Cambridge Alphametrics Model LINK.>")