Download presentation

Presentation is loading. Please wait.

1

The Agricultural Lending Industry: Commercial Banks and the Farm Credit System Chapter 8

2

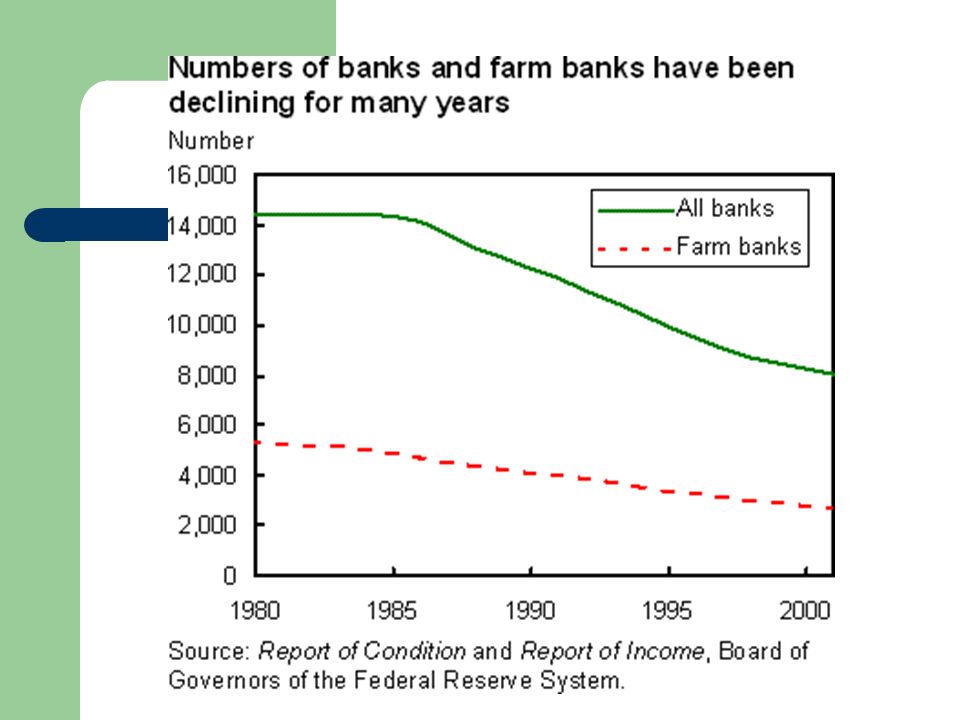

Commercial Banks In US today there are 8,000 independently chartered banks. Chartering of first bank came in 1791

3

Regulatory History National Banking act of 1863 - congresses third attempt to regulate banking at the federal level. Federally Chartered – office of the Comptroller of the Currency. State Chartered – all states already had their own state chartering agencies, thus the beginning of our dual banking system.

4

Regulatory History Federal Reserve Act established our current national bank in 1913. Fed’s original task was to provide liquidity to banks as a lender of last resort. Federal Reserve was established as a system of twelve district banks. Great Depression Price Deflation

5

Mergers The banking industry is consolidating Ultimately the nation may have just 2000 or so chartered banks Will this improve the lot of the consumer?

8

REAL PRIME INTEREST RATES

9

Bank Balance Sheets AssetsLiabilities and Equity Cash and Reserves $ 2,000 Demand Deposits $20,000 Securities 26,000 Savings Deposits 65,000 Consumer Loans 20,000 Bank Debentures 17,000 Real Estate Loans 25,000 Other Borrowings 0 Commercial Loans 31,000 Common Stock @par 2,000 Less Loan Reserves 2,000 Excess paid in Capital 1,000 Premises & Equipment 4,000 Retained Surplus 5,000 Total Assets$110,000Total Liabilities &Equity $110,000

10

Liabilities Banks earn maintenance fees on traditional demand deposit accounts. Demand deposits have been shrinking as a percentage of total since 70s due to money market accounts. Savings include passbook savings, CDs, educational savings funds and IRAs Interest Rate Differences.

11

Equity Remaining accounts on RHS are Ownership Accounts or Equity Common Stock @ Par Excess Paid in Capital Retain Surplus or Retained Earnings – How banks use this is a matter or asset financial management

12

Assets Cash and Reserves – Fed Requires approx. 10% of bank demand deposits to be placed in reserve. – Not a significant source of liquidity for the bank Securities Portfolio Loan Portfolio Premises and Equipment

13

Introduction Many farmers have long argued that credit for agriculture has not been met by conventional financial institutions. Private lending procedures, sources of funds, and loan terms are not beneficial to the needs of agriculture.

14

History Government began to make direct loans to farmers for short term credit requirements in the 1920’s. In the 1930’s FCS, FmHA, REA, and CCC were created. All of these agencies continue to operate although the names and scope of work have changed over time.

15

Farm Credit System Long Term FCS loans are made to farmers, corporations producing farm products, agribusinesses, and rural homeowners. Loans can be used to acquire land, equipment, and livestock or to refinance existing debt. The largest holders of farm real estate debt are the FCS and commercial banks.

16

Farm Credit System Short and intermediate term FCS loans can be used for the production of farm products, aquatic products, and purchase or repair of rural homes. FCS holds 20% of non real estate farm debt.

17

Government-Sponsored Enterprise Farm Credit began as a government sponsored cooperative effort to provide a system through which farmers could provide their own credit. FCS is now self-supporting. As a GSE, FCS can borrow money from the US Treasury cheaper than commercial banks. In turn, FCS can usually loan out money cheaper than commercial banks.

18

FCS Independence FCS became wholly user owned when the last government loan was repaid in 1968. In 1985 FCS lost $2.7 billion through mortgage and loan defaults. Several of the FCS banks had become insolvent and Congress responded with a Federal bailout. Now FCS is run by the Farm Credit Administration which is an agency of the U.S. Executive Branch.

19

USDA USDA has a number of credit programs for ag and rural areas. FSA is the direct lending arm in agriculture. Rural Development is the direct lending agency for rural programs.

20

FmHA Farmers Home Administration was created to implement all direct lending, loan insurance, and grant programs for low income farmers. FmHA was abolished in 1994 and its farm credit programs were transferred to the newly created FSA.

21

Farm Service Agency Lender of last resort to farmers. Loans are for farmers who can not get credit with commercial banks or FCS. FSA makes farm ownership loans, operating loans, and emergency loans.

22

Farm Service Agency Emergency loans are made only to counties designated as a disaster area. Interest rates on FSA loans are significantly lower than those of commercial banks. FSA held 4.1% of total US farm business debt in 2000. Because of their risky loans, many FSA loans result in default.

23

Rural Development Rural Development includes the Rural Housing Service, Rural Business Cooperative Service, and Rural Utilities Service. Direct loans, loan guarantees, and rental assistance are available to low income people in rural areas which include cities with populations up to 50,000.

24

Rural Development The Rural Business-Cooperative Service administers the business assistance programs. Grants are made to non profits and public bodies for business development. Large loan guarantees are also available to businesses.

25

Rural Development Rural Utilities Service provides large loans and grants for electricity, water, and sewer. Assistance is available to public bodies and utility districts for expanded utility programs.

26

Commodity Credit Corporation Farmers would pledge a quantity of a commodity as collateral and obtain a recourse loan from the CCC. Farmers can either repay the loan with interest within a period of time or they must forfeit their commodity to the CCC.

27

Effects of Subsidized Credit Immediate effects are to reduce interest rates and to increase the amount of credit used in agriculture. This contributes to increased production and larger, more highly mechanized farms. It is harmful to nonusers because it increases output and decreases product prices.

28

Problems with Subsidized Credit Moral Hazards Government restrictions reduced diversification in bank loan portfolios, thereby increasing risk and likelihood of bank failure. These instances have made it difficult to make a case for subsidized credit to agriculture.

Similar presentations