Download presentation

Presentation is loading. Please wait.

1

Michigan Saves Home Energy Loan Program

Contractor Training

2

Part 1: What is Michigan Saves?

2

3

What is Michigan Saves? Our mission is to make energy improvements easy and affordable. We provide financing for energy efficiency improvements. Our financing is a better deal than you’ll find elsewhere, and it’s less of a burden to apply and get approved. Our goal is to give you and your customers the best financing option available in Michigan. 3

4

What can Michigan Saves do for you?

Our financing helps customers purchase improvements from you that they would otherwise couldn’t purchase. Our financing helps customers purchase a larger scope of work from you than they otherwise could. 4

5

Home Energy Loan Program (HELP)

Easy, affordable loans for homeowners Immediate loan decisions Authorized contractors Qualifying improvements Easy, affordable loans The rate is typically 7%. This is better than loans you’ll find elsewhere, which typically have rates of … The loans have lenient criteria. That means more people will be able to qualify for them than for typical loans. Loans are approved or denied with one quick phone call, which means you can often know whether or not a person is approved right after making a pitch or signing a contract. Exclusive program – Customers can only access loan through a Michigan Saves authorized contractor. We have guidelines for what improvements qualify or not. More on that later. 5 5

6

Nuts & Bolts: Customer Eligibility

Owner-occupied (buildings with up to 4 units) No rentals or income properties at this time Loan criteria Credit Score 640 or higher Monthly debt to gross income of 50% (post loan) No bankruptcies, tax liens, outstanding collections 6 6

No rentals or income properties at this time. Loan criteria. Credit Score 640 or higher. Monthly debt to gross income of 50% (post loan) No bankruptcies, tax liens, outstanding collections")

7

Nuts & Bolts: Loan Terms

Unsecured, up to $30,000 Rates as low as 4.25% Loans $4,999 or less: Term is 1 year per $1,000 Loans $5,000 or more: Any term to 10 years Make sure to mention what unsecured means for contractors practically—that more customers will qualify than for conventional loans. 7 7

8

Nuts & Bolts: What Qualifies as Efficient?

Anything with an Energy Star® label is eligible (See Eligible Measures list for information on efficiency requirements) HVAC measures Roofing Windows/doors Appliances Solar thermal Solar PV Insulated vinyl siding Solar pool heaters Air Sealing & Insulation must be financed with Whole Home Energy Audit

HVAC measures. Roofing. Windows/doors. Appliances. Solar thermal. Solar PV. Insulated vinyl siding. Solar pool heaters. Air Sealing & Insulation must be financed with Whole Home Energy Audit.")

9

Nuts & Bolts: Health, Safety & Pre-Existing Environmental Hazards

Michigan Saves will finance remediation of health, safety and pre-existing environmental hazards. Remediation work must be coupled with an appropriate efficiency measure related to the remediation. Asbestos remediation with new boiler installation Knob-and-tube wiring removal with wall insulation Roof repairs with attic insulation

10

Nuts & Bolts: Our Hope for Contractors

Long term relationship Shared marketing Mutual benefits Info about building a long term relationship, where we highlight the excellent work you do to transform families’ experiences of their homes, and you highlight our role in the process.

11

Nuts & Bolts: Contractor Expectations

Provide high level of professionalism and customer service Complete 1 loan per calendar year Provide 1 year warranty on labor All equipment must carry manufacturers warranty

12

Nuts & Bolts: Michigan Saves Contractor Fee

All authorized contractors charged fee of 1.99% of loan value Fee supports Michigan Saves operations For most lenders, fee automatically deducted from contractor payment – no invoicing

13

Nuts & Bolts: Current Lenders

14

Nuts & Bolts: Helpful Resources

Implementation Guide Eligible Measures List Program Forms Marketing Tools This is the guide you’ll want to get familiar with. It has everything you need to know. We’re going to go through some things together today, but if you ever have questions or need clarification, this can be a useful resource. All can be found at: michigansaves.org/resource/contractors-res 14 14

15

Program Results Loan results (through February 2015)

Total loans approved – 4,327 (62% approval rate) Total loans closed – 4,318 (99% closure rate) Total value of closed loans - $37,980,529 Average loan size - $8,799 Average FICO score of approved applicants - 739 Average FICO score of all applicants – 696

Total loans closed – 4,318 (99% closure rate) Total value of closed loans - $37,980,529. Average loan size - $8,799. Average FICO score of approved applicants Average FICO score of all applicants – 696.")

16

Program Results Contractor participation to date 567 applications

436 applications have been approved 313 Authorized Contractors 169 Mechanical contractors (51%) 94 Building contractors/remodelers (32%) 16 Energy auditors (5%) 12 Home performance contractors (5%) 21 Solar PV contractors (7%) 1 Electrical Contractor

94 Building contractors/remodelers (32%) 16 Energy auditors (5%) 12 Home performance contractors (5%) 21 Solar PV contractors (7%) 1 Electrical Contractor.")

17

Part 2: Loan Application Process

17

18

Process Details: MSU Federal Credit Union

Uses a merchant lending model: Contractor fills out paperwork, submits electronically to MSUFCU who provides instant decision Upon project completion, contractor prints out loan documents for customer’s signature Contractor – in effect – issues loan to customer, then resells loan to MSUFCU MSUFCU pays contractor through direct deposit Contact Stephanie Minott for details ( )

")

19

4 Step Process Explain role of the Loan Application Center here (not in great detail, as that will become clear in next two slides, but enough to understand them as an intermediary that helps in the process.)

")

20

1 Secure the Job. Customer and contractor agree on a work scope.

Customer identifies Michigan Saves authorized contractor from website or contractor promotes program to customer Contractor provides information on Michigan Saves loan and initiates loan application process Customer provides information to loan application center and receives decision within minutes Loan application center passes completed and approved loan application to lender, which may conduct income verification Contractor uses own contracting process to secure job Contractor initiates application process. Customer calls loan application center. Loan application center passes completed application to lender.

21

2 Do the Work. 1 Secure the Job. Contractor begins work.

While work is in progress, customer completes membership application, if not already a member Upon completion of the work, contractor obtains customer’s signature on certification of completion and sends to lender, which triggers loan closing Customer becomes member of credit union. Contractor completes work. Contractor sends Certificate of Completion to Lender.

22

3 Get paid. 1 Secure the Job. 2 Do the Work.

Lender prepares closing documents for customer. Loan initiation. Lender prepares final loan documents and arranges for closing; Customer signs loan closing documents Upon receipt of signed loan documents, lender pays contractor directly while customer begins monthly payments on the loan Customer signs loan closing documents. Lender pays contractor directly. Customer begins monthly payments.

23

4 Submit Forms. 1 Secure the Job. 2 Do the Work. 3 Get paid.

Contractor completes project record. Submit Michigan Saves Forms. Contractor completes project record (aka “spec sheet”) through Michigan Saves Online Contractor Portal. Contractor submits project record.

through Michigan Saves Online Contractor Portal. Contractor submits project record.")

24

1 Secure the Job. 2 Do the Work. 3 Get paid. 4 Submit Forms.

25

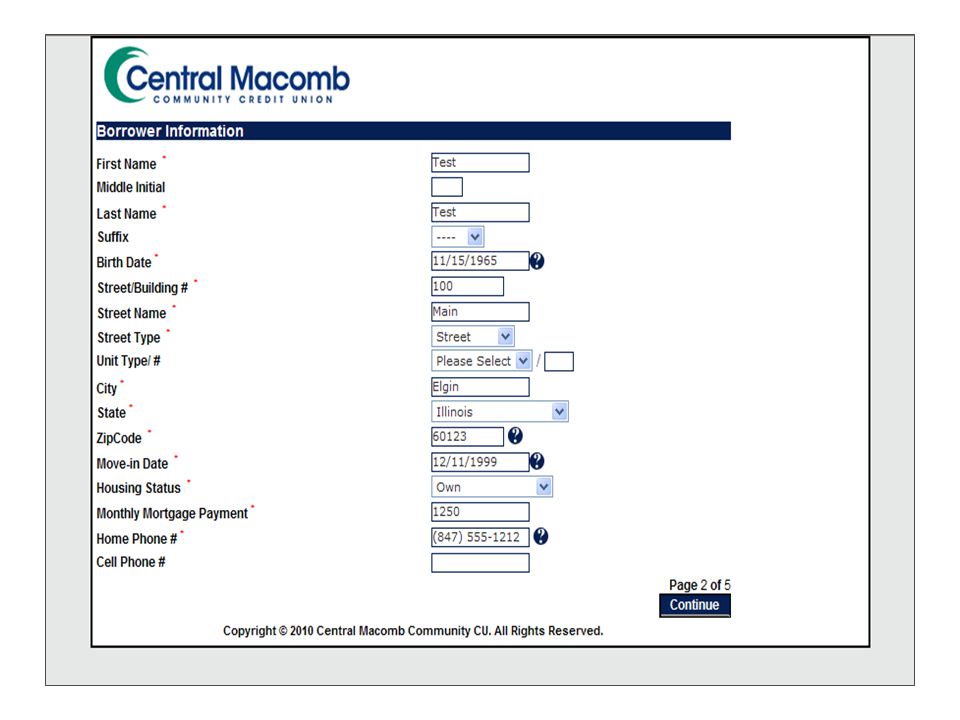

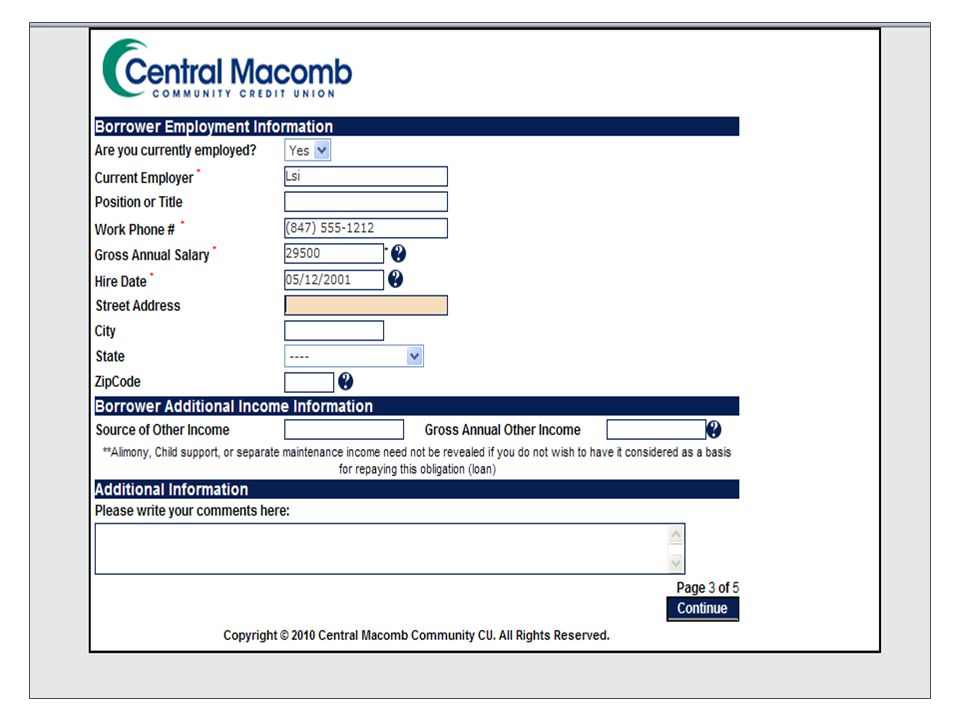

Process Details: Loan Application Center

Contractor accesses loan application center using Michigan Saves contractor identification # Provide number via phone or through Web portal Set of 10 cards and ID nos. sent upon completion of application & training

26

Process Details: Loan Application Website

27

Process Details: Loan Application Website

32

Process Details: Credit Insurance

Offered with every loan through loan application center Protects customer’s credit score in the event that they cannot pay off the loan due to death and disability Fee can be 10-30% of amortized loan amount Only available to customers under the age of 71 Automatically ends the month of the customer’s 71st birthday This is an optional insurance product that a customer can choose to accept or deny 32

33

Process Details: Loan Approval

CONGRATULATIONS! Your application has been approved. A loan representative will contact you by the next business day with closing information. We here at Central Macomb Community Credit Union value your membership and welcome this opportunity to serve you. Thank you for choosing Central Macomb Community Credit Union for your financial needs. **If the loan amount is above $3,000 or if your credit score is below 720, verification of income will be required. Note for Contractor: Please mail the certificate of completion to: Central Macomb Community Credit Union 34642 Van Dyke Ave. Sterling Heights, MI 48312 NOTE: Copy of certificate of completion also sent to Michigan Saves

34

Process Details: Loan Denial/Pending

“Unable to honor request” messages always means that the customer does not qualify for Michigan Saves loan. Example: Thank you for applying with Central Macomb Community Credit Union. We have processed your application and are unable to honor your request at this time. A notice will be mailed to you indicating the reason for this decision. “Application being processed” or “Someone will call you back” message may mean Customer not approved, but not denied either Customer has been victim of identity theft, flag on credit report They are self-employed (lender doing income verification) Example : Thank you for applying to Central Macomb Community Credit Union. Your application is being processed. A representative will be responding to you shortly. We appreciate the opportunity to serve you.

Example : Thank you for applying to Central Macomb Community Credit Union. Your application is being processed. A representative will be responding to you shortly. We appreciate the opportunity to serve you.")

35

Process Details: Submitting Forms

Project Record (a.k.a. Specification Sheet) Exists in Online Contractor Portal (OCP) Home & project specifications Certificate of Completion (COC) Signed by customer and contractor Affirms that job has been satisfactorily completed and provides customer information release Mailed to lender at the address provided during initial loan approval Receipt by lender triggers loan closing and contractor payment Scan and attach to project Record Most lenders will hold off on loan closing documents until CoC is received. Expect payment within 14 days or less. Approval will not be reversed unless customer has been fraudulent. Consider one document with spec sheet 35

Exists in Online Contractor Portal (OCP) Home & project specifications. Certificate of Completion (COC) Signed by customer and contractor. Affirms that job has been satisfactorily completed and provides customer information release. Mailed to lender at the address provided during initial loan approval. Receipt by lender triggers loan closing and contractor payment. Scan and attach to project Record. Most lenders will hold off on loan closing documents until CoC is received. Expect payment within 14 days or less. Approval will not be reversed unless customer has been fraudulent. Consider one document with spec sheet. 35.")

36

Review of Online Contractor Portal

37

Part 3: Quality Assurance

37 37 37

38

Quality Assurance Objectives

Verify that there are no fraudulent or misleading actions Confirm customer satisfaction Verify that program requirements are met 38 38

39

QA Methods Review documentation Periodic site inspections

Customer surveys Coordinated with other programs (utilities, BPI), where possible, to avoid overlap

, where possible, to avoid overlap.")

40

Michigan Saves Role File Review

Review Project Record/Spec Sheet All information included for installed and removed measures All measures eligible under program All diagnostics testing results included where appropriate Review Certificate of Completion Dated, signed by customer and signed by contractor Flag projects that violate program requirements 40

41

Michigan Saves Site Inspection

Michigan Saves schedules site visit with homeowner Site inspection Installed measures match items on specification sheet Measures are installed to manufacturer guidelines or best practices Confirm customer satisfaction Replicates ‘test-out’ procedures (assessment-based only)

")

42

Deficiencies Michigan Saves sends Corrective Action Request (CAR) to contractor Three types: Safety, Workmanship, Programmatic If safety or workmanship CAR then contractor must document actions to fix the issue. Contractor must respond to CAR within designated timeframe Michigan Saves makes determination of contractors status Enhanced Supervision, Suspended or Terminated

43

Safety CARs Must be resolved within 48 hours! Examples:

Electrical, fire, or structural hazards were part of the installation. Failed combustion safety testing results. Gas leaks located.

44

Workmanship CARs Examples: Poor workmanship

Test-out diagnostics incomplete or inaccurate.

45

Programmatic CARs Examples:

Failure to submit Certificate of Completion or Specification Sheet in a timely manner. Financing of non-qualifying measures.

46

Part 4: Marketing Michigan Saves

When fully operational…available to all types of energy consumers Michigan Saves finances qualifying energy improvements Loan capital provided by network of lenders through a centralized loan application center Loans serviced by lenders (utility on-bill programs in some cases) Michigan Saves uses $6.5 million trust fund for credit enhancements to attract lender/investor capital at affordable rates and terms

Michigan Saves uses $6.5 million trust fund for credit enhancements to attract lender/investor capital at affordable rates and terms.")

47

Key Marketing Messages

EASY Convenient Fast Seamless AFFORDABLE Save money and energy Flexible repayment terms Low interest rates SMART Save energy and environment Make wise investment Improve comfort Help Michigan’s economy EASY • Convenient—Find an authorized contractor and they’ll do it all, or your contractor will suggest a Michigan Saves loan to you. The loan application can be completed in your home during the contractor visit. • Fast—The loan application process is fast and we only collect a minimal amount of information. The application process is “Easy As 1-2-3” and you’ll have a decision in minutes. • Seamless—The contractor will help make the loan process even easier by showing you how to apply and providing you with support. AFFORDABLE • Save Money and Energy—With the Michigan Saves Home Energy Loan Program, there is no upfront cost, and over time you’ll be saving energy in your home. You’ll have more money in your pocket faster by investing in energy improvements today. • Flexible Repayment Terms—Your payments can be structured to match your available budget. Low Interest Rates—For qualified homeowners, these are lower than market rates for unsecured loans. There are no property appraisals needs or home equity required. SMART • Save Energy—A Michigan Saves Home Energy Loan will help you quickly save energy in your home. You’ll be contributing to a healthier environment and investing in your biggest asset at the same time. It’s A Wise Investment—Energy-saving investments improves your bottom line—and your energy bills. You’ll Be More Comfortable—Making energy efficiency improvements means your home will be more comfortable. Helping The Economy—You’ll be supporting job creation here in the State of Michigan.

48

Rack Card Can be used as leave-behind or direct mailer 48

49

Case Studies

50

More than 400 authorized commercial and residential contractors

51

HELP Program Updates Lower Interest Rates

UP State Credit Union – % Coming soon - Washtenaw Federal Credit Union 0% finance for 48 months will be available 4/1 in the overlapping Lansing Board of Water & Light electric service territory and Consumers Energy gas service territory 51 51

52

BEF Program Business Energy Financing Program

Leases from $2,000 to $250,000 0% for 24 months, up to $50k is currently available in DTE, Consumers Energy or Lansing Board of Water & Light Service Territory Training is every 4th Thursday of the month 52 52

53

Questions and Comments

For all contractor questions, concerns, and feedback, contact Kait Wyckoff or Todd Parker Kait – (517) Todd – (517) We welcome your suggestions! Please follow us on Facebook & Twitter! @MichiganSaves 53 53

Todd – (517) We welcome your suggestions! Please follow us on Facebook & Twitter!")

Similar presentations

makes energy saving upgrades affordable Me 2 financing.>")

286-5593>")

Program San Antonio Office of Environmental Policy December 16, 2009.>")