Download presentation

Presentation is loading. Please wait.

1

Samuel M. Meyler Meyler Legal, PLLC 8201 164 th Ave. N.E., Suite 200 Redmond, WA 98052 425-881-3680 samuel@meylerlegal.com

3

» Understanding the structure of the DOL. » Understanding DOL Procedure for handling and investigating complaints. » Recognize common issues that result in disciplinary action. » Understanding what sanctions are.

4

Pat Kohler

8

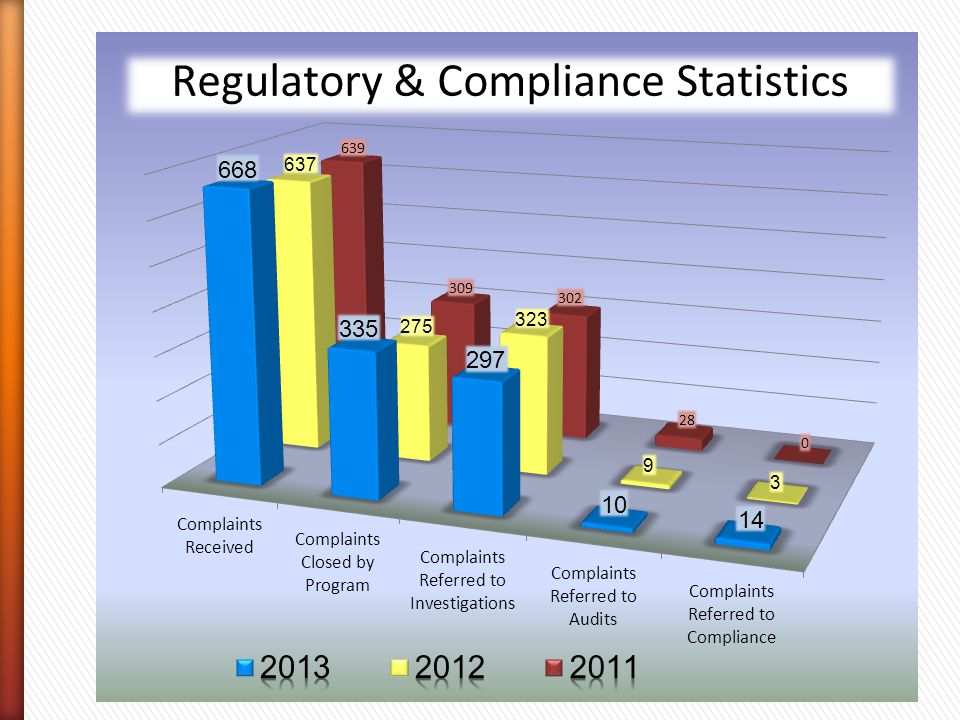

» In order to investigate a complaint it must fall under the jurisdiction of the Real Estate Unit of the Department of Licensing. » Must be a violation of License Law or the Law of Agency. » Approx. 60% of complaints are closed before investigation.

9

» Unlicensed Activity » Misrepresentation » Deal Honestly and In Good Faith » Exercise Reasonable Care and Skill » First Applicant/ Conviction » Civil » Failure to Respond to the Department » Property Management Agreements » Advertising without Company Name » Trust Account Prop Mgmt., Sales, General. » Ethics » Conversion » Statements/ Negligence » Fraudulent/Dishonest Dealing » Incompetency

11

» LICENSE HISTORY » HISTORY OF PREVIOUS VIOLATIONS; INCLUDING WHEN AND RELATIONSHIP TO CURRENT ALLEGATIONS » HARM AND SEVERITY OF HARM TO CONSUMERS OR OTHERS » NATURE, EXTENT, AND TIME FRAMES OF THE ACTS » HOW VIOLATION WAS SOLVED AND/OR CORRECTED » EVIDENCE OF DUE DILIGENCE ON THE PART OF THE LICENSEE » LEVEL OF SUPERVISION INVOLVED FROM MANAGING OR DESIGNATED BROKER(S) » LICENSEE INTENTION, ACCOUNTABILITY AND ACKNOWLEDGEMENT » PERSONAL GAIN OR BENEFITS OBTAINED BY LICENSEE OR OTHERS INVOLVED » COOPERATION BY RESPONDENT » CRIMINAL OR CIVIL JUDGMENTS/CONVICTIONS » MONETARY JUDGMENTS » OTHER MITIGATING CIRCUMSTANCES » OTHER AGGRAVATING CIRCUMSTANCES

» LICENSEE INTENTION, ACCOUNTABILITY AND ACKNOWLEDGEMENT » PERSONAL GAIN OR BENEFITS OBTAINED BY LICENSEE OR OTHERS INVOLVED » COOPERATION BY RESPONDENT » CRIMINAL OR CIVIL JUDGMENTS/CONVICTIONS » MONETARY JUDGMENTS » OTHER MITIGATING CIRCUMSTANCES » OTHER AGGRAVATING CIRCUMSTANCES")

12

» What is it? ˃Statement regarding jurisdiction and venue ˃License History ˃Statement of Charges (Allegations) ˃Request for Sanctions » Matters subject to B.A.P. ˃Disciplinary Action to be taken ˃Reasons for disciplinary action ˃How to dispute ˃What happens if you don’t dispute

˃Request for Sanctions » Matters subject to B.A.P. ˃Disciplinary Action to be taken ˃Reasons for disciplinary action ˃How to dispute ˃What happens if you don’t dispute.")

17

WAC 308-124I-050 Audits. (1) Real estate firms are subject to routine audits. Routine audits are scheduled approximately every three years. (2) Audits will be conducted at the location the real estate firm is licensed to conduct real estate brokerage activity or a facility chosen by the department. (3) All requests for records will be issued by an authorized representative of the director, such as auditors, investigators, program staff or other designee. (4) An audit can be initiated at any time based upon the results of the previous audit or complaint. (5) Audits are not scheduled, but they are normally done between the hours of 8:00 a.m. and 5:30 p.m., Monday through Friday, excluding state holidays. An auditor may not forcibly enter a licensed business location unless accompanied by law enforcement personnel pursuant to a valid search warrant. Licensees are advised that refusal to permit access may result in disciplinary action under chapters 18.85 and 18.235 RCW. (6) An auditor may appear at a licensed business location, unannounced, during the hours described above. A licensee may be required to produce to the auditor at that time all records the licensee is required to keep by the statutes and rules governing licensees. Licensees are advised that refusal to permit access may result in disciplinary action under chapters 18.85 and 18.235 RCW. (7) The department may not charge for the cost of routine audits to the licensee. Audit costs may be charged to the licensee pursuant to RCW 18.235.110(2) when the department has audited pursuant to a complaint, violations have been found, and the director has issued an order imposing any of the sanctions described in RCW 18.235.110(1). (8) An auditor and licensee may mutually agree to complete or continue an audit outside the time and date limitations.

Audits will be conducted at the location the real estate firm is licensed to conduct real estate brokerage activity or a facility chosen by the department. (3) All requests for records will be issued by an authorized representative of the director, such as auditors, investigators, program staff or other designee. (4) An audit can be initiated at any time based upon the results of the previous audit or complaint. (5) Audits are not scheduled, but they are normally done between the hours of 8:00 a.m. and 5:30 p.m., Monday through Friday, excluding state holidays. An auditor may not forcibly enter a licensed business location unless accompanied by law enforcement personnel pursuant to a valid search warrant. Licensees are advised that refusal to permit access may result in disciplinary action under chapters and RCW. (6) An auditor may appear at a licensed business location, unannounced, during the hours described above. A licensee may be required to produce to the auditor at that time all records the licensee is required to keep by the statutes and rules governing licensees. Licensees are advised that refusal to permit access may result in disciplinary action under chapters and RCW. (7) The department may not charge for the cost of routine audits to the licensee. Audit costs may be charged to the licensee pursuant to RCW (2) when the department has audited pursuant to a complaint, violations have been found, and the director has issued an order imposing any of the sanctions described in RCW (1). (8) An auditor and licensee may mutually agree to complete or continue an audit outside the time and date limitations..")

19

» Failure to Maintain Transaction Records » Failure to disclose relationship with service providers » Failure to Retain Records » Failure to Notify office Change of Address » Failure to keep records up to date. » Failure to Perform Monthly Trial Balance » Failure to Identify Client Funds as Trust » Failure to do Business in the Name as Licensed » Failure to keep the Trust Account in Balance » Failure to Deliver Funds within One Banking Day

20

» What can they do to you and what are the considerations? » Goal to change licensee behavior. » Repeat or habitual offenders - Propensity to reoffend » Actions that are a high risk of harm to the: ˃Public ˃Agency ˃Staff ˃Industry ˃Individuals » Nexus of actions to the program and their practice to the reason the program exists. » Identify who or what has been or may be harmed. ˃Public at large ˃Individual person ˃Industry integrity ˃Property ˃Money » Identify the nature, extent, and time frames of the violation. » Previous investigations, inspections or audits » Following a consistent process used to determine sanctions. » Consistency within a program and the division. » collateral consequences of our decision or action.

21

» Fact pattern 1 » Fact pattern 2 » Fact pattern 3 » Fact pattern 4

Similar presentations