Download presentation

Presentation is loading. Please wait.

1

“Rolling Out the Plan” PRESENTING YOUR CASE PROJECT TO YOUR CLASSMATES.

2

Category Snapshot TOTAL AUTOMATIC DISHWASHER COMPOUNDS (DETERGENTS) LBS. Total Dollars Behavior Scape Framework LifeStyle BehaviorStage Cosmopolita n Centers Affluent Suburban Spreads Comfortable Country Struggling Urban Cores Modest Working Towns Plain Rural Living Total Start-Up Families HHs with Young Children Only < 6 12414914583119124126 Small Scale Families Small HHs with Older Children 6+ 108142126399389103 Younger Bustling Families Large HHs with Children (6+), HOH <40 10516616195140134136 Older Bustling Families Large HHs with Children (6+), HOH 40+ 14818316879131140149 Young Transitionals Any size HHs, No Children, < 35 67101963673 70 Independent Singles 1 person HHs, No Children, 35-64 49696126403445 Senior Singles 1 person HHs, No Children, 65+ 49655527404245 Established Couples 2+ person HHs, No Children, 35-54 1051301326393100107 Empty Nest Couples 2+ person HHs, No Children, 55-64 10714013357109106116 Senior Couples 2+ person HHs, No Children, 65+ 11514314055105107117 Total 93135125538992100

, HOH < Older Bustling Families Large HHs with Children (6+), HOH Young Transitionals Any size HHs, No Children, < Independent Singles 1 person HHs, No Children, Senior Singles 1 person HHs, No Children, Established Couples 2+ person HHs, No Children, Empty Nest Couples 2+ person HHs, No Children, Senior Couples 2+ person HHs, No Children, Total")

4

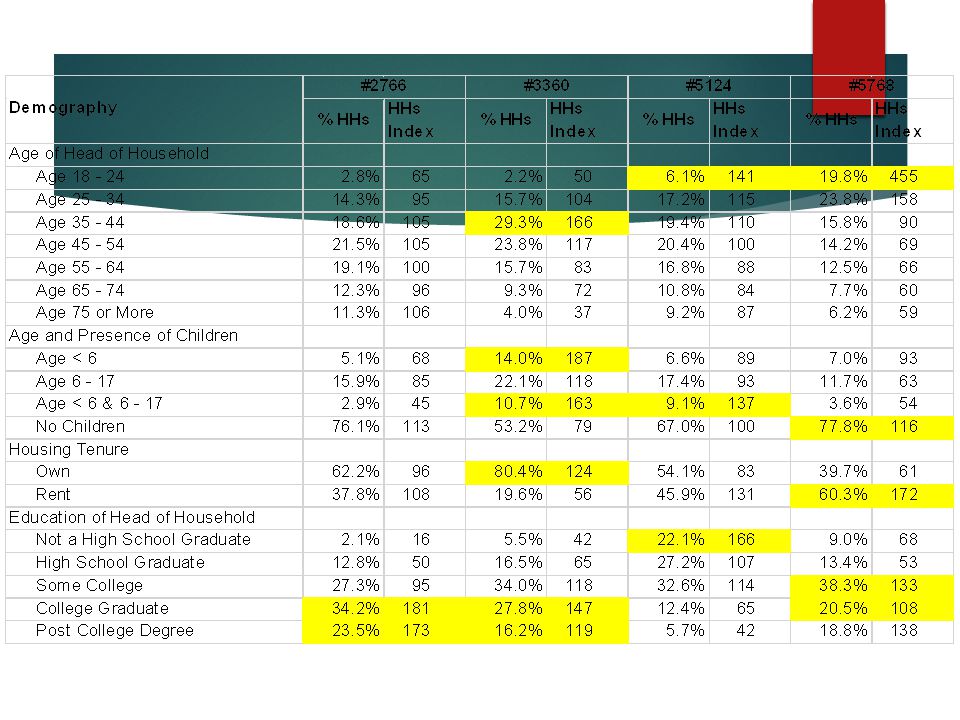

Demographic Variables % Total $Index% Total $Index% Total $Index% Total $Index Race of Head of Household White52.6%7664.6%9357.8%8464.8%94 Black24.7%20716.6%13919.5%16313.0%109 Hispanic15.4%12413.6%10915.7%12714.3%116 Asian3.1%732.9%674.6%1075.4%126 Other4.1%1912.4%1102.3%1072.5%113 Number of Persons 1 Person20.1%7417.7%6519.5%7218.9%70 2 Persons31.6%9736.2%11133.9%10533.9%104 3 Persons17.6%10917.7%10917.3%10716.9%105 4 Persons13.5%10214.4%10914.1%10615.1%115 5+ Persons17.3%15614.2%12715.2%13715.2%136 Household Income Under $10,00011.0%1397.7%977.2%907.9%99 $10,000 - $19,99914.0%12012.6%10910.9%9310.8%93 $20,000 - $29,99914.9%13212.2%10811.2%9910.8%96 $30,000 - $39,99912.3%11611.8%11211.1%10511.3%107 $40,000 - $49,99910.7%11610.1%10910.3%11110.7%116 $50,000 - $74,99916.9%9418.1%10018.2%10017.9%99 $75,000 - $99,9998.8%7511.2%9611.9%10111.3%97 $100,000 - $149,9996.7%5810.4%9111.5%10112.0%105 $150,000 or More4.7%585.9%737.9%987.3%91 AjaxDawnPalmolivePrivate Label

5

Step Two: Category Role Share some personal interest in the category, maybe employment was an issue. Size, in U.S. sales: >$1 billion = high <$100 million = small Marsh Supermarket Data on the broader category Interest in penetration, purchase cycles, deal

6

ITEM $ (000)DOLLAR SHARE ITEM BUYERS (000) ITEM PENETRATIO N ITEM $ PER ITEM BUYER PURCHASE CYCLE (IN ELAPSED DAYS) % REPEAT BUYERS (% 2+ TIME BUYERS) LOYALTY (SHARE OF $ REQ.) % ITEM $ ON DEAL % DOLLARS WITH MANUFACTURER COUPON SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 174,090.3100.037,100.232.0$4.6989.545.6100.020.77.7 WEST SOUTH CENTRAL 19,163.0100.04,499.734.6$4.2690.446.1100.016.29.0 SHAVE CREAMS - WOMEN'S TOTAL U.S. 84,697.0100.016,981.214.6$4.9972.943.7100.025.510.2 WEST SOUTH CENTRAL 8,840.7100.02,013.415.5$4.3976.141.4100.018.29.3 AVEENO - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 3,627.02.1632.50.5$5.7390.328.559.78.11.9 WEST SOUTH CENTRAL NA BARBASOL - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 20,565.311.810,280.38.9$2.00102.328.657.011.70.6 WEST SOUTH CENTRAL 1,892.39.91,159.18.9$1.63100.025.152.53.70.2 COLGATE - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 3,751.42.22,115.58.9$1.7765.210.344.424.50.0 WEST SOUTH CENTRAL 432.52.3244.11.9$1.7767.87.347.422.80.0 CTL BR - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 3,750.32.21,549.41.3$2.42100.113.146.425.00.1 WEST SOUTH CENTRAL 466.12.4248.61.9$1.8892.99.654.48.70.0 CTL BR - SHAVE CREAMS - WOMEN'S TOTAL U.S. 2,142.82.5695.10.6$3.0890.021.344.818.30.0 WEST SOUTH CENTRAL NA EDGE ACTIVE CARE ADVANCED - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 5,655.13.31,946.31.7$2.9189.114.437.833.816.3 WEST SOUTH CENTRAL 588.23.1221.81.7$2.65102.618.338.326.117.6 EDGE ADVANCED - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 52,976.230.411,673.410.1$4.5497.031.769.824.79.6 WEST SOUTH CENTRAL 5,611.429.31,420.510.9$3.95100.035.767.318.79.1 ENVI - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 2,798.01.61,158.31.0$2.4281.623.749.91.90.0 WEST SOUTH CENTRAL 523.92.7223.11.7$2.3588.725.651.10.60.0 GILLETTE FOAMY - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 11,979.06.94,578.33.9$2.62106.227.757.813.52.2 WEST SOUTH CENTRAL 1,548.78.1609.34.7$2.54107.833.560.714.55.9 GILLETTE FUSION HYDRA GEL - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 12,886.27.42,964.42.6$4.3595.024.757.035.524.9 WEST SOUTH CENTRAL 1,548.18.1337.82.6$4.58106.932.063.232.630.4 GILLETTE SATIN CARE - SHAVE CREAMS - WOMEN'S TOTAL U.S. 17,893.121.15,374.24.6$3.3371.030.456.031.616.8 WEST SOUTH CENTRAL 2,218.425.1639.94.9$3.4770.732.363.323.412.3 GILLETTE SERIES - SHAVE CREAM - OTHER THAN WOMEN'S TOTAL U.S. 19,929.211.56,254.15.4$3.1989.124.549.924.511.6 WEST SOUTH CENTRAL 2,233.511.7771.45.9$2.9088.923.849.323.016.7 PURE SILK - SHAVE CREAMS - WOMEN'S TOTAL U.S. 5,871.76.93,073.42.7$1.9191.718.745.29.01.8 WEST SOUTH CENTRAL 741.88.4347.32.7$2.1479.318.753.03.81.0 SKINTIMATE - SHAVE CREAMS - WOMEN'S TOTAL U.S. 56,583.866.811,428.89.8$4.9580.036.882.726.39.8 WEST SOUTH CENTRAL 5,599.163.31,365.010.5$4.1080.133.982.218.79.6

7

Assigning a Role to the Category

8

Why Gin? (Spring 2008) Gin accounted for 4.4% of the market share in the liquor industry in 2007. That’s $138,739,800! The suppliers are more in control in the liquor industry because of the increasing demand for it. As long as there’s excess demand, suppliers will continue to make more and more product. No private brands Not your typical category. Lots of small manufacturers. Courtney

9

Retailers Audited Store# SKU% of Cat WM66038.22% WMJ8252.23% IGA5031.85% SAMS21.27% TARGET21.27% ALDI53.18% WG53.18% Harps W4528.66% Harps G6843.31% NHM (S)8453.50% NHM (F)4327.39% Springdale NHM had the most assortment with 53.50% of all the SKU’s found!! Many times the PL is placed directly next to the “Grade A” brand to encourage consumers to purchase based on price

10

Stores Audited Fayetteville Aldi’s-1 Deal’s Dollar Store-2 Dollar General-1 Harp’s-39 (deepest) Ozark Natural Foods-9 Sam’s-1 Target-6 Wal-Mart 6 th Street-21 St. Louis Schnuck’s-32 Target-8 Rogers Wal-Mart-25 Bentonville Wal-Mart Neighborhood Market- 20 Van Buren CV’s IGA-27 Price Cutter-27 Walgreen’s-1

11

Changes in Category Have any new suppliers or brands appeared since a recent audit was conducted (semester of last audit)? What has happened to prices and a prior group’s gross margin estimates? Changes in share of display, at specific stores? Changes were minor or major? Category predictions, its role for the retailer, needs, etc.

12

The Suppliers Introduction to suppliers and their brands What did you describe as a dominant brand—why? SKUs? Number of stores stocking the brand? Stocking rate? Were there some surprising losers? Any major firms with little shelf space, a single facings, strange or low margins.

13

SKU’s 94 SKU’s discovered in audit Supplier w/the most SKU’s of the identical product/formulation - Ocean Spray had 34 SKU’s - Private Label had 37 SKU’s This leaves 23 SKU’s for the other five brands found Adjacencies next to Cranberry Juices: Other Juices i.e. Grape Juice, V-8 Juices, etc. Location: in the middle of the aisle

14

LISTING OF FIRMS DOMINANT BRANDS Pinnacle Foods (Duncan Hines) Lindt & Sprungli (Ghirardelli) General Mills (Betty Crocker & Pillsbury) Aldi’s Ozark Natural Foods Harps STRUGGLING BRANDS Gluten-free pantry All of the OzarkNF brands Martha White Bakers Corner Nature’s Path Dr. Oetker No Pudge Arrowhead Mills Bob’s Red Mill Cherry Brook Kitchen Namaste Foods Market Pantry Best Choice Always Save

15

Stores Audited Total number of stores audited by group Listing of stores Trade area demographics for specific stores Anticipated depth for the stores of interest to group members Store without any evidence at category management—no relationship between demographics and category depth

16

Jams and Jellies

17

How did your group determine gross margin? What brands had the highest costs, what was it costs per ounce? What were the estimates for private label, costs per ounce? What adjustments for sizes, deals, negative gross margins did you have to make? SPSS, 5-6 stores—of interest, showing average gross margin by brand, % of Total, mean %

18

Circular Trade Areas: Phoenix Area Supercenters

20

A.C. Nielsen Circular Trade Areas Required component, some evidence in your PowerPoint file. Does it explain differences in depth? Does it explain different in shares of gross margin? Does it explain difference in average gross margins?

21

FACINGS Most PL gained best part in share of facings and share of SKUs in small stores (niche market such as DG, IGA) But strong national brands such as Windex and Clorox try to fight back and also has strong influence in big stores (Wal-Mart, Harps).

But strong national brands such as Windex and Clorox try to fight back and also has strong influence in big stores (Wal-Mart, Harps).")

22

Gross Margin by Store and Manufacturer

25

Private label “success” Share of a category Acceptance by households Consumer “happiness” Ability to evaluate quality differences Brand identity, internal & external Retail concentration & differentiation Category & retailer profitability Economic factors Structure of supply Retailer format success

26

“Good losers? Snacks and confectionary Cosmetics Baby food Alcoholic beverages “Success!” Paper, plastic, and wipes Refrigerated food Frozen food Shelf stable juices Bad winners? – no one but ourselves to blame. Pet food Healthcare Diapers and feminine hygiene Price gap with manufacturer brands High>30% Low<30% Private label share Low <12%High > 12% “Bad stuff” – why? Home care Nonalcoholic beverages Personal care Global private label share and price gap

27

Spring 2014

28

Fall 2012

29

Fall 2010

30

Writing Follow guidelines for double-spaced number of pages (26 lines, 3-4 paragraphs per page). If you’re assigned to write a section—be sure all group members re-read it. Include Heading for each of the eight sections and page breaks to separate sections/steps Use subheadings within section if discussion in section is more than one page.

Similar presentations