Download presentation

Presentation is loading. Please wait.

1

Housing Associations and Welfare Reform October 2013 Mary Taylor Chief Executive SFHA

2

Overview HAs in Scotland Current challenges – welfare What is needed

3

Sector profile 280,000 homes for rent, – plus shared homes, part ownership and factoring – plus mid market and intermediate rents 11% of all housing in Scotland – 46% of all affordable rented housing 150 HAs and co-ops – Range of sizes: 400, 4000, 40,000. Typical around 1800. – Roles vary – All regulated social landlords (RSLs) by the Scottish Housing Regulator More than just housing – Support, care, regeneration, employment training, social enterprise, garden schemes and more Rent debit c£1bn – c55% of all rental income indirectly from HB – wide variation

by the Scottish Housing Regulator More than just housing – Support, care, regeneration, employment training, social enterprise, garden schemes and more Rent debit c£1bn – c55% of all rental income indirectly from HB – wide variation.")

5

Social Housing in Scotland Social Rented sectorPrivate Rented sector Mobility40% in their home for more than 10 years A third in their home for less than a year Size576,000 (24%)325,000 (14%) Property size~80% one or two bedroom~60% one or two bedroom Turnover12% 1br available (69,000)At least a third? (107,000) Demand~350,000? Housing Benefit65% claim HB, equates to 55% of rent received 30% claim LHA Housing need~45% ‘vulnerable’Job movers, students Age of tenants54% are 45 or older52% under 35 Economically inactive52% (older tenants)36% (student renters) Cost (rent per week)£62~£160

Demand~350,000. Housing Benefit65% claim HB, equates to 55% of rent received 30% claim LHA Housing need~45% ‘vulnerable’Job movers, students Age of tenants54% are 45 or older52% under 35 Economically inactive52% (older tenants)36% (student renters) Cost (rent per week)£62~£160.")

6

Housing in Scotland cf GB High proportion of social housing stock High proportion of new housing starts as social housing o = to NI High proportion of government spend on housing o 3.3% cf 5.1% in NI High spend on housing per household Lowest average rent as a proportion of average earnings Lowest proportion of social tenants on HB Lowest average weekly HB spend for social renters

7

Current challenges in Scotland High demand Highest proportion of new HA lets going to homeless households Higher proportion of social housing as temporary accommodation Higher than average unemployment rate Rising demand for intermediate rent property in some locations Supply constraints Highest RTB sales as a proportion of social housing stock – RTB to be abolished Greatest loss of social housing over past 20 years Lower than average RSL spend per unit when including private finance Falling subsidy per unit drives rents up when changes to HB makes harder to afford

8

Welfare Cuts in Scotland £1.66bn (24%) Annual impact in 2014/15

Annual impact in 2014/15")

9

Est’d Impact of welfare cuts on Housing Associations in Scotland

10

Distribution of HAs’ arrears

11

Bedroom Tax Share of LA Arrears

12

…if three wishes? 1.Time to organise downsizing 2.Recognition that social housing requires investment 3.Housing Benefit is a subsidy for housing

13

1. Time to help tenants to downsize

14

2. Recognition that social housing requires investment Housing is not like other commodities Imperfections Supply Info Location Finance Equity Fair access Hence intervention and public investment

15

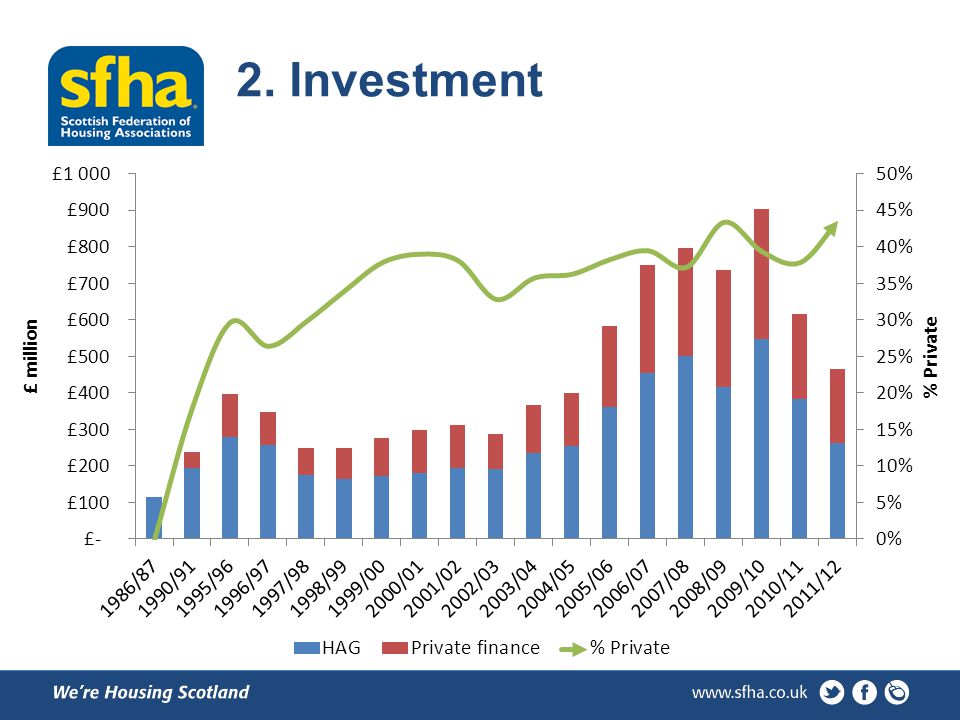

2. Investment

18

3. Housing Benefit is a Subsidy for Housing

19

Housing Subsidy Spending in Scotland Devolved Reserved

20

If I had just one wish?

21

What challenges lie ahead People – governing bodies, employees, customers Demands and expectations of customers Values of providers Intellectual demands of future strategy Emotional demands - morale and resilience Attitude to risk Leadership

22

Doing things differently? Diversify e.g. into mid-market rent? New forms of finance – bonds, securitisation Different relationships with other bodies – Contracting, partnerships, subsidiaries Services to people – older, poorer, more vulnerable – relationship to health and social care agenda Any change could mean greater risks – all sorts, everywhere … – governance implications of assessing and treating risk

23

Prospects?

24

Shift from capital to revenue subsidy Greater risk with reduced Housing Benefits Greater dependence on private finance Cuts to Housing Benefit to control welfare spending 1% cap undermines ability to inflate rents Direct payments undermine ability to collect rents Enough additional cash to support borrowing? Depressed value of the homes used as loan security Downward pressure on credit ratings Increased risk of alternative funding sources relative to inflation Risks no new homes for social rent

25

Worst that could happen? Drop in demand, higher turnover Repossessions and abandonments Less funding (rent and borrowing) Costlier procurement Job losses and less contractor capacity Reputational damage from getting it wrong Sharing, partnering, merging

Costlier procurement Job losses and less contractor capacity Reputational damage from getting it wrong Sharing, partnering, merging.")

26

Best that could be achieved? New rented markets & business opportunities – Eg selling services to others Opportunity to get closer to customer – better customer relations Challenges provide imperative to – greater efficiency – focus on asset management Sharing, partnering, merging

27

Further information Please contact: Regina Serpa Research and Information Officer Email: rserpa@sfha.co.ukrserpa@sfha.co.uk Tel: 0141 332 8113 Mob: 07887 888 346

Similar presentations

about The New Affordable Rent Model Brendan Sarsfield.>")