Download presentation

Presentation is loading. Please wait.

3

This presentation does not contain, and shall not be held to contain, any professional advice. The presentation does not constitute legal advice. Accordingly the matter of the presentation may not be relied upon for any professional purpose and independent legal opinion should be obtained before taking action as a result of any matter or thing contained in this presentation.

4

Terms & Conditions of Grant Funder specific formats Contractual Arrangements Specific formats Public Persona / Reputation Statutory Reporting “fall back” position Fund Raising - Public Expectations Perceived Promises Government funding for transfer of Community Service Obligations Corporate Funding - Philanthropy, Corporate Conscience Where is the money coming from and what are the Terms it comes on ?

5

Range of requirements – usually linked to the value of the Grant Some Grant acquittances require ‘surrender” of original corporate documents Conflict with record requirements of regulatory legislation Monitoring and complying with auspice arrangements Periodic reporting in prescribed form Financial & non- financial criteria Acknowledgement Publicity Challenges for records integrity

6

Problem is common to a vast range of entities Solutions are diverse How to select the solutions most appropriate for your circumstances? Driven by: Your funding sources Your type of entity/incorporation Public accountability on a variety of levels; Your Members Your Customers/Clients Your suppliers/business partnerships General Public “probity” concerns

7

WHERE TO START? Generally best to start with WHO we are discussing. Non Government Organisation – NGO’s CORE Government activities are: CORE Government activities are: Health, Education Defence and Health, Education Defence and Transportation infrastructure Transportation infrastructure The Australian Federal and State Governments now deliver more than half of their “non-core” Community Service Obligations using “Not for Profit” intermediaries. Public reliance on “NGO’s”

8

CHARACTERISTICS OF NGO’S INCORPORATED ENTITIES: Legal existence, capable of holding asset title, capable of being sued Governance requirements and enforceable accountability UPON Management Committees Meets governance requirements of Funder Legislative framework provides minimum levels of confidence to all concerned in activity/objectives VOLUNTARY MANAGEMENT & FREQUENTLY OPERATIONAL STAFF: Commitment to objectives, needs or service to be delivered – not “just a job” Restricted time available Limited skills base Limited economic capacity to “buy” skills required

9

CHARACTERISTICS OF NGO’S LOCAL TO THE AREA OF DELIVERY: Capacity for prompt and directed response to delivery Not subject to all the daily “red tape” of Public Sector Focus can be very tight, ONLY one sector of community Restricted to resources WITHIN the Community in which functioning Inadequately resourced for “compliance” with “red tape” Can cease to function very quickly Politicalisation Clerical collapse

10

Incorporated associations: Each State/Territory has its own legislation – minor variations Enabling Act – Associations Incorporation Act 1981 (Queensland) – amended 30 October 2006 body corporate with perpetual succession has a seal may sue or be sued in its own name (S21) Members not liable to contribute to winding up beyond the property of the incorporated association in a person’s hands (S27) If a “winding up” becomes necessary – Corporations Law applies (S90)

– amended 30 October 2006 body corporate with perpetual succession has a seal may sue or be sued in its own name (S21) Members not liable to contribute to winding up beyond the property of the incorporated association in a person’s hands (S27) If a winding up becomes necessary – Corporations Law applies (S90)")

11

Incorporated associations: Requirements to: have a management committee hold an Annual General Meeting have an audit of financial affairs conducted lodge copies of specified reports, including audited financial report with regulator Office of Fair Trading Funding Bodies – Public & Commercial General “Public Interest”

12

Incorporated associations: Statutory enforcement of minimum standards of corporate governance and internal control over financial affairs. Including: Minimum for number of members of management committee (3) Minimum requirement to meet at least once in each 4 months Lodgment of certain changes within one month (S 60-69) Minimum Public Liability Insurance $1,100,000 (S70) Protection of rights of Members (S71)

Minimum requirement to meet at least once in each 4 months Lodgment of certain changes within one month (S 60-69) Minimum Public Liability Insurance $1,100,000 (S70) Protection of rights of Members (S71).")

13

Incorporated associations: Flexibility by way of Rules: -Adopt “Model Rules” or “Write Your Own” BUT!! – Model Rules have Legislative override - some provisions cannot be dropped or Rules will not be approved Rules will not be approved - certain changes to the Model Rules will override any specific “write your own” provisions that may have been approved in the past – generally “equity” or “common law” basis

14

Incorporated associations: Management Committee Members have to know the Model Rules and where these are the same as or conflict with the Association’s own rules. S61 – MUST have a MINIMUM of Three members One member MUST hold office of President One member MUST hold office of Treasurer and NOT also hold office as President S66 – Associations MUST have a Secretary may be elected by the Association may be appointed by Management Committee and in that case need not be a member of the association Associations MUST advise of changes in Secretary within One Month

15

Incorporated associations: Officers of Associations are deemed servantsS123 “strict liability” Liability Protection of Act is negated by willful act or negligence opening Members of Management Committee – and non-member Secretaries- become liable for loss suffered Observance of Good Governance practice can assist to demonstrate due care and so preserve limitation of liability in most circumstances

16

Incorporated associations: ACT – CONCEPT and Equity 2 to 5 year minimum to effect changes REGULATIONS – PRACTICAL – can be changed by Regulator within a few months REGULATIONS: Rules, Records and Accounting requirements Part 3 Regulation 9RECORD KEEPING Regulation 10 ACCOUNTING REQUIREMENTS Regulation 11 AUDITED RETURN Regulation 12 ADDITIONAL ACCOUNTING REQUIREMENTS Schedule 5

17

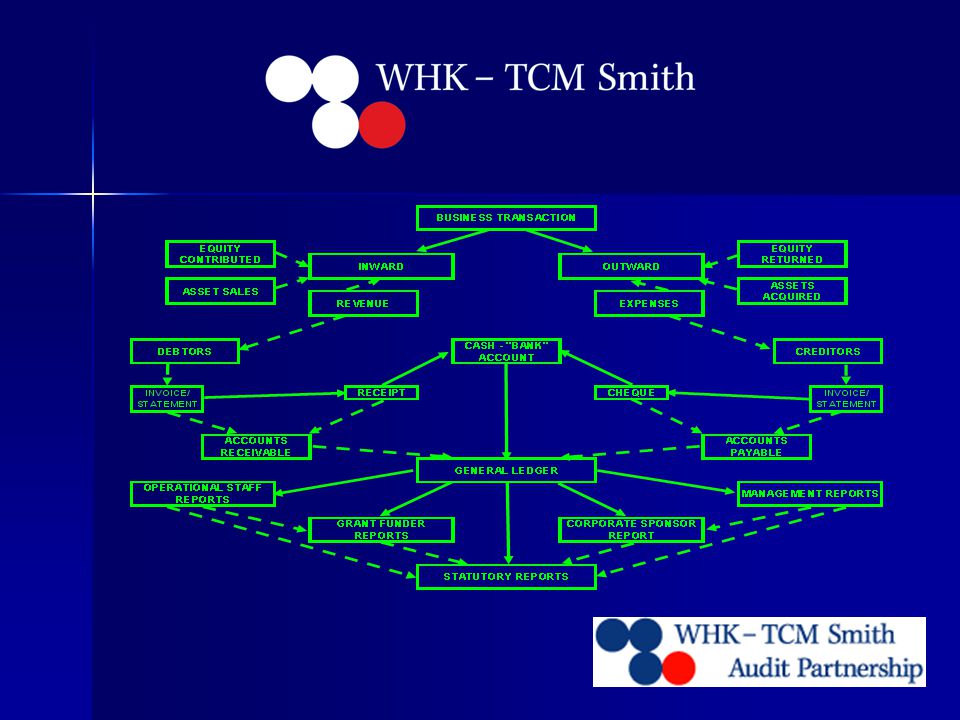

Incorporated associations: Statutory Reporting Obligations Simple – Income & Expenditure Statement agreeing to Cash Balances So what makes these more complex: When “Cash” is not the only asset When it is not adequate tooperate on a cash basis. Significant Operations, Owe to Creditors, Owed by Debtors Terms & Conditions of Grant: Contractual requirements: Australian Equivalents to International Financial Reporting Standards (AEIFRS)

.")

18

Australian Equivalents to International Financial Reporting Standards (AEIFRS) apply to “general” purpose financial reports. “Reporting Entity” where the persons making economic decisions have ONLY the statutory financial report to base decisions on. Usually not applying to Incorporated Associations because: Close membership; Management drawn from memberships; Other funders, bankers, Government Departments have the power to obtain detailed information on request. Denial of these rights would force transition to “general purpose” Member request to move to “general purpose” or Funding body may make “general purpose” a Grant requirement

19

Terms & Conditions of Grant: Generic requirements: Audit of financial statements Financial reporting against funded budget lines Controls over process of acquisition of “capital” items or expenditures in excess of $1,000 Key Performance Indicators (KPI’s) Periodic reporting on projects Right of entry to records to conduct their own review if they wish Greater cost of compliance with accounting requirements

Periodic reporting on projects Right of entry to records to conduct their own review if they wish Greater cost of compliance with accounting requirements")

20

Philanthropic Entities: Commercial Enterprises seeking to display a “public conscience” Needing to display effective Corporate Governance and satisfy “general purpose” reporting standards of their own. Pressure on Not-For-Profits to be clearly accountable in comparable formats Significant reliance on audit opinion, additional requirements in audit plan Must be considered if seeking the Corporate $ Funding is less constrained to specific uses, programmes More reliance on PROBITY

21

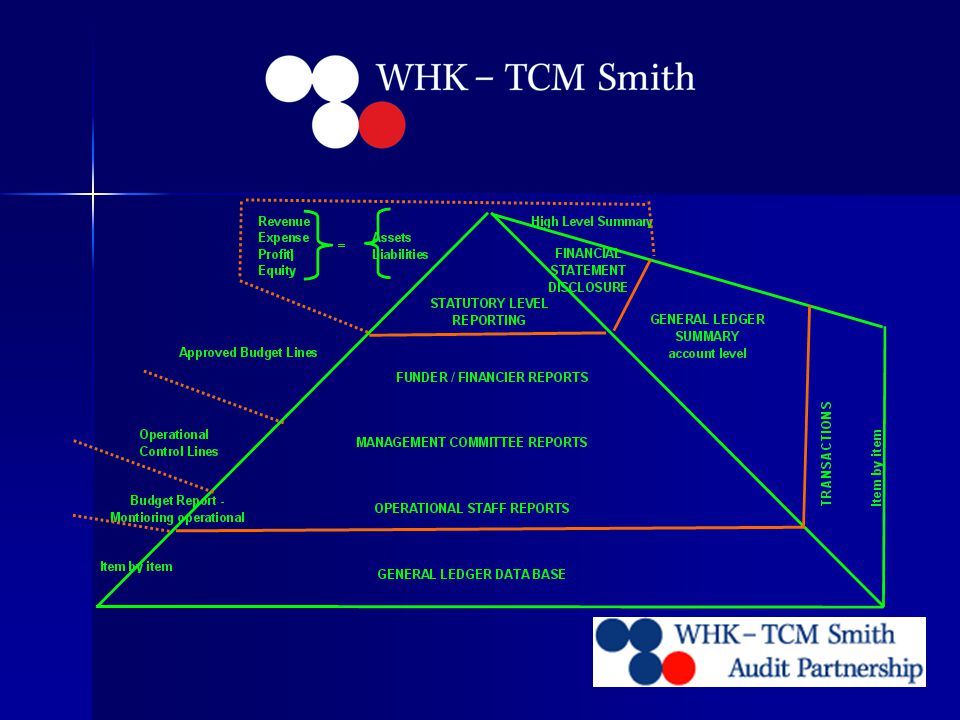

Management Reporting: “Statutory” and “Grant/Financier” Reporting are both wholly historical, already fixed because it has happened Management reporting has to be current and, at its best, forward and active They have to be reconcilable to each other to prove the integrity of their results Most effective if they come from the same data Multiple files are a severe risk of undetected error and fraud, Cost more to maintain and As EACH record has to be audited, more records mean more cost

24

CORPORATE GOVERNANCE IN A VOLUNTARY ORGANISATION The big “untruths” – As this is voluntary everyone can make their own rules – The rules made by the strongest personality win – The longest serving person has to be recognised as the strongest – New blood and ideas have to be better than what we have been doing – People with Certificates and Degrees know more than anyone else –People we pay to do things cannot do them as well as volunteers can

28

CORPORATE GOVERNANCE IN A VOLUNTARY ORGANISATION Agree to a Code of Practice that suits your organisation Especially where Management Committee members may also have a “hands on” volunteer role be clear about the separation of the two roles Be clear about what you “delegate” to employed staff Set out clearly what you really need to monitor how they use your “delegation” and in what circumstances you will withdraw that privilege – then Leave them to it

29

CORPORATE GOVERNANCE IN A VOLUNTARY ORGANISATION This then allows you to reduce the volume of data, financial and otherwise, that bombards you The framework you set assists to identify what you need to be sure things are “on track” You can see where each “external” prescription impacts on what you do and how they can be used to assist you to manage Everyone can at least come to row in the same direction even if not at the same speed. You build the capacity for your organisation to grow, expand and become self perpetuating, including planning for future governance when voluntary doesn’t work any more without losing your ethos (character)

.")

30

WHERE DOES “AUDIT” FIT? statutory monitoring function legal requirement to report on “breaches” Regulatory/funding body review processes to reduce their workload by transfer of responsibility to someone else (i.e. “the auditor”) Audit reports ON Management Audit reports to “Owners” “Regulators” and “Funders” and to anyone else who can establish their right to the information and obtain consent of owners/managers

Audit reports ON Management Audit reports to Owners Regulators and Funders and to anyone else who can establish their right to the information and obtain consent of owners/managers.")

31

WHAT IS AN AUDIT? an assessment of transactions and actions measured against a set of standards and requirements WHAT DOES IT DO? identifies which rules apply to you examines how and what you have done considers the adequacy and process of how you did it compares the “rules” and “reality” reports to the identified group(s) on the comparison reports on risks identified, especially those not adequately addressed.

on the comparison reports on risks identified, especially those not adequately addressed..")

32

WHAT DOESN’T AUDIT DO Audit is only permitted to assist you in extracting your financial statements in very limited circumstances even though it will be involved in ensuring you prepare the right ones in the right way Audit will not make decisions about what you do or how you should do things even though it may advise you on what you should NOT do or what is best practice discover fraud even though it can tell you how it happened and often how to prevent it and have probably warned you it could happen for years

33

FRAUD most fraud is discovered by you, often when one of the parties to it gets honest or falls out with partners in crime. Except where collusion has allowed the fraud, if you have to wait for audit to tell you fraud has occurred we can be sure that: your records are in a mess; your committee has not been effective in controlling your activities; it will be almost impossible to pursue the culprit(s) or recover any money. Fraud destroys “trust” and many voluntary organisations will never recover from it The best DEFENCE against fraud is to have clear Procedures, good reporting from delegates and strong monitoring at Committee level This can only happen if the Management Committee can understand what the reports they receive are meant to show

or recover any money. Fraud destroys trust and many voluntary organisations will never recover from it The best DEFENCE against fraud is to have clear Procedures, good reporting from delegates and strong monitoring at Committee level This can only happen if the Management Committee can understand what the reports they receive are meant to show.")

34

WHY DOES AUDIT COST SO MUCH? The smaller and more restricted the administrative resources are the poorer the records tend to be Where operations are complex and accounting processes are not or do not match the organisation the records will either be inadequate to answer the questions or there will be several sets being kept to answer the questions If clear directions about what has to come OUT of an accounting process are not identified the records probably won’t give you what you want UNDERSTANDING!

35

ACCOUNTING PROCESS – USE OF COMPUTER SOFTWARE Computer software is designed to allow the user to be in control, save money on accounting costs Computer software, set correctly, can overcome the limitation of access to skills of bookkeepers and accountants Computer software, set incorrectly, will consistently do everything wrong Computer software, used incorrectly, cannot provide a trustworthy result This will increase audit costs because of the need to sort out frequent errors, reversals, simple incorrect usage and potential deliberate misuse

36

ACCOUNTING PROCESS – USE OF COMPUTER SOFTWARE It is important to know what you need OUT of your computer software What the computer software within your budget CAN do What level of skill your operator has to use program flexibilities Where you can use the computer software, and other information you maintain, to work together to overcome program/user skill limitations This requires and understanding of: – what your activities and objectives are – what are the real measures of achievement – what is imposed upon you that you can use with minimum extra effort

37

ACCOUNTING PROCESS – USE OF COMPUTER SOFTWARE The most expensive system and the cheapest one work on the same basis –Transactions recorded according to type –Accumulated in a summary record –Reports available from that summary And, most importantly R I R O Rubbish In –Rubbish Out The best system will be defeated by poor use!

38

ACCOUNTING PROCESS – USE OF COMPUTER SOFTWARE If you do not match your needs with the capacities of the software and the abilities of the user it is unlikely you will be able to obtain the output you require. People can be trained, output formats can be adjusted and sometimes you have to accept that what you really want is not possible So – what can you expect any accounting software program to be capable of?

40

RECAPITULATION: Be clear about: What OTHER people/organisations want from you What you REALLY need to MANAGE/MONITOR properly What the CONFLICTS between those criteria are What is the best use of your resources to RESOLVE the conflicts What the EFFECTIVE DIVISION of responsibilities and “powers” need to be Your COMMITMENT to good Governance is the key to good management, good operations and The ability to sleep soundly at night!

41

RESOURCES FOR ASSOCIATIONS, COMMITTEES & MEMBERS: These slides Associations Incorporation Act Regulations: Regulation 33 Schedule 5 Places to go for more information: Office of Fair Trading – www.fairtrading.qld.gov.au Office of Fair Trading – www.fairtrading.qld.gov.au follow the links to the Legislation and advisory publications

Similar presentations

B. Bidding.>")