Download presentation

Presentation is loading. Please wait.

1

Michael Orr Director Center for Real Estate Theory and Practice March 10, 2015 Michael Orr Director Center for Real Estate Theory and Practice March 10, 2015 Greater Phoenix Housing Market

2

Euphoria Denial Despair Hope Skepticism Optimism Enthusiasm Exhilaration Unease Pessimism Panic Capitulation Relief Optimism Enthusiasm The Market Cycle

3

Euphoria Denial Despair Hope Skepticism Optimism Enthusiasm Exhilaration Unease Pessimism Panic Capitulation Relief Optimism Enthusiasm The Market Cycle 2005 2008 2010 2015 2007 2012 2003

5

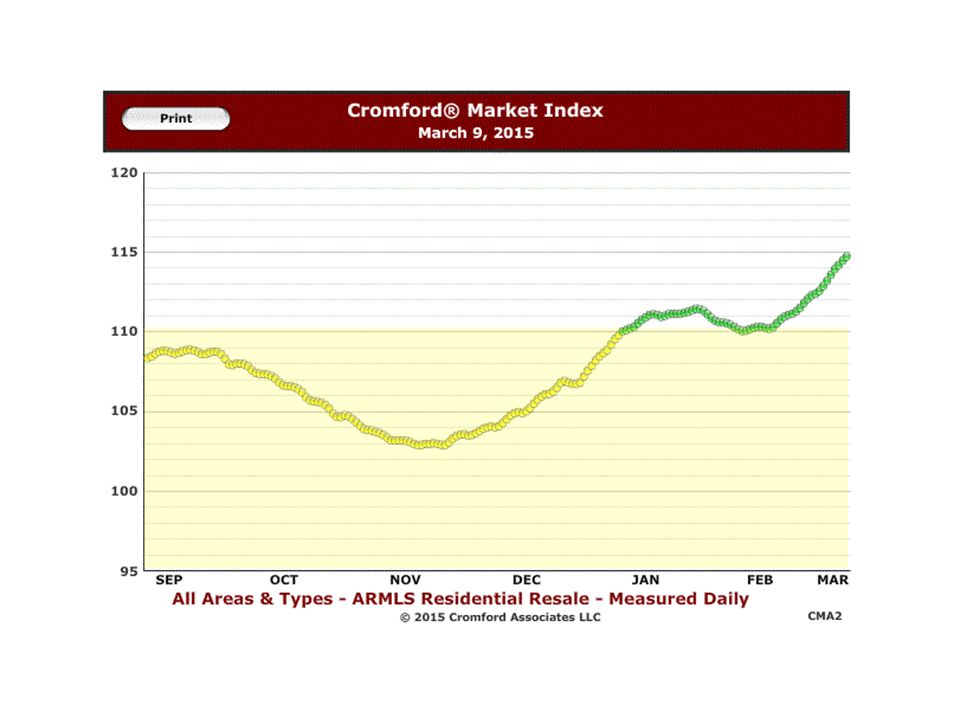

Most Home Prices Are Flat or Keeping Pace with Inflation Some Segments are Falling or Rising, but Not Much Outlook: Positive for Second Half of 2015

8

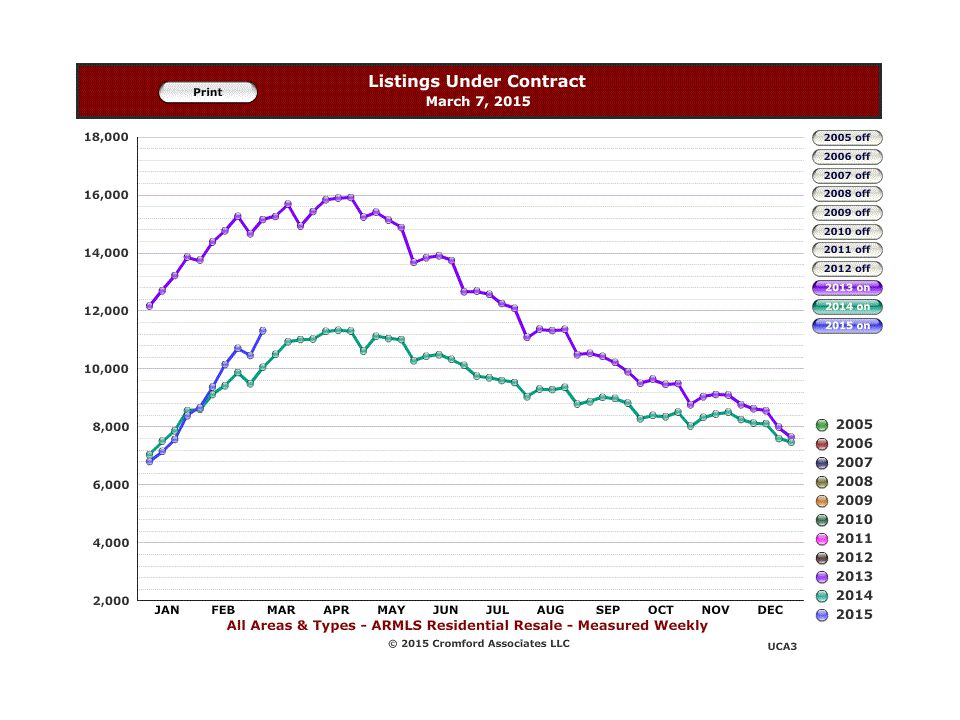

Demand for Homes to Buy Has Been Weak While Demand for Homes to Rent Is Very Strong Demand for Homes to Buy Has Been Weak While Demand for Homes to Rent Is Very Strong

9

Why Has Demand Been Weak? Investor buys dropped 41% in 2014 from 2013 Owner occupier buys up only 0.3% Many owners frozen in place – need higher prices Millennials not buying homes like their parents did – Far more living with parents, sharing or renting 1 in 4 former owners in “the Penalty Box” – 367,000 owners lost homes to foreclosure / short sale Large lenders are still very risk averse – Avg FICO for DENIED Conventional Purchase Loan = 721 – Avg FICO for CLOSED Loan = 752 Income and wealth disparity increasing Very slow income growth (0.9% for Phoenix 2011-2013) Investor buys dropped 41% in 2014 from 2013 Owner occupier buys up only 0.3% Many owners frozen in place – need higher prices Millennials not buying homes like their parents did – Far more living with parents, sharing or renting 1 in 4 former owners in “the Penalty Box” – 367,000 owners lost homes to foreclosure / short sale Large lenders are still very risk averse – Avg FICO for DENIED Conventional Purchase Loan = 721 – Avg FICO for CLOSED Loan = 752 Income and wealth disparity increasing Very slow income growth (0.9% for Phoenix 2011-2013)

Investor buys dropped 41% in 2014 from 2013 Owner occupier buys up only 0.3% Many owners frozen in place – need higher prices Millennials not buying homes like their parents did – Far more living with parents, sharing or renting 1 in 4 former owners in the Penalty Box – 367,000 owners lost homes to foreclosure / short sale Large lenders are still very risk averse – Avg FICO for DENIED Conventional Purchase Loan = 721 – Avg FICO for CLOSED Loan = 752 Income and wealth disparity increasing Very slow income growth (0.9% for Phoenix ).")

10

Single Family Rentals Investors pulling back but tenants still coming Only 1,993 SFR rental listings on MLS This is 25 days of supply Normally expect to see 4,000 to 5,000 Rents are climbing 5% to 8% per year Most of what is left is expensive (avg $1,980 pm) Supply for $900 - $1200 range is down > 50% Supply over $2000 is relatively plentiful Investors pulling back but tenants still coming Only 1,993 SFR rental listings on MLS This is 25 days of supply Normally expect to see 4,000 to 5,000 Rents are climbing 5% to 8% per year Most of what is left is expensive (avg $1,980 pm) Supply for $900 - $1200 range is down > 50% Supply over $2000 is relatively plentiful

Supply for $900 - $1200 range is down > 50% Supply over $2000 is relatively plentiful Investors pulling back but tenants still coming Only 1,993 SFR rental listings on MLS This is 25 days of supply Normally expect to see 4,000 to 5,000 Rents are climbing 5% to 8% per year Most of what is left is expensive (avg $1,980 pm) Supply for $900 - $1200 range is down > 50% Supply over $2000 is relatively plentiful")

11

Prediction Is Very Difficult, Especially About the Future - Neils Bohr (1885-1962) Prediction Is Very Difficult, Especially About the Future - Neils Bohr (1885-1962)

Prediction Is Very Difficult, Especially About the Future - Neils Bohr ( )")

14

Long term average

16

Normal Listings Priced from $175,000 to $600,000

17

Hotspots – March 2015 85043 85353 85323 85033 85035 85037 85335 85307 8534585302 85051 85017 85304 8530685053 85040 85283 85203 85204 ZIP Codes Showing Strongest Increase in Demand Versus Supply

18

Cold & Lukewarm Spots Gila Bend Carefree Fountain Hills Casa Grande Gold Canyon Coolidge Wickenburg Tonopah Litchfield Park

19

Heating Up 85326 85392 85379 85382 85027 85029 85303 85301 85019 85031 85006 85339 85041 85042 Demand Exceeds Supply in All These Areas 85044 85226 85224 8522585295 8523385234 85201 85202 85210

20

Situation Summary – March 2015 Supply is well below normal (83% of normal) Demand is low but growing (95% of normal) AZ loan delinquency below normal at 4.5% Foreclosures below long term average Lending rules starting to loosen Entry market heating up High end market cooling down Economy and jobs continue to improve Time to change from relief to optimism Supply is well below normal (83% of normal) Demand is low but growing (95% of normal) AZ loan delinquency below normal at 4.5% Foreclosures below long term average Lending rules starting to loosen Entry market heating up High end market cooling down Economy and jobs continue to improve Time to change from relief to optimism

Demand is low but growing (95% of normal) AZ loan delinquency below normal at 4.5% Foreclosures below long term average Lending rules starting to loosen Entry market heating up High end market cooling down Economy and jobs continue to improve Time to change from relief to optimism Supply is well below normal (83% of normal) Demand is low but growing (95% of normal) AZ loan delinquency below normal at 4.5% Foreclosures below long term average Lending rules starting to loosen Entry market heating up High end market cooling down Economy and jobs continue to improve Time to change from relief to optimism")

21

Michael Orr Director Center for Real Estate Theory and Practice Michael Orr Director Center for Real Estate Theory and Practice

Similar presentations

led.>")

Analyze the various sources of borrowing available to a client and.>")