Download presentation

Presentation is loading. Please wait.

1

A Presentation by: Thomas Hutcheson, Kristina Giamportone, Stevie Kindler, Brittney McQuesten, and Kevin Jones

2

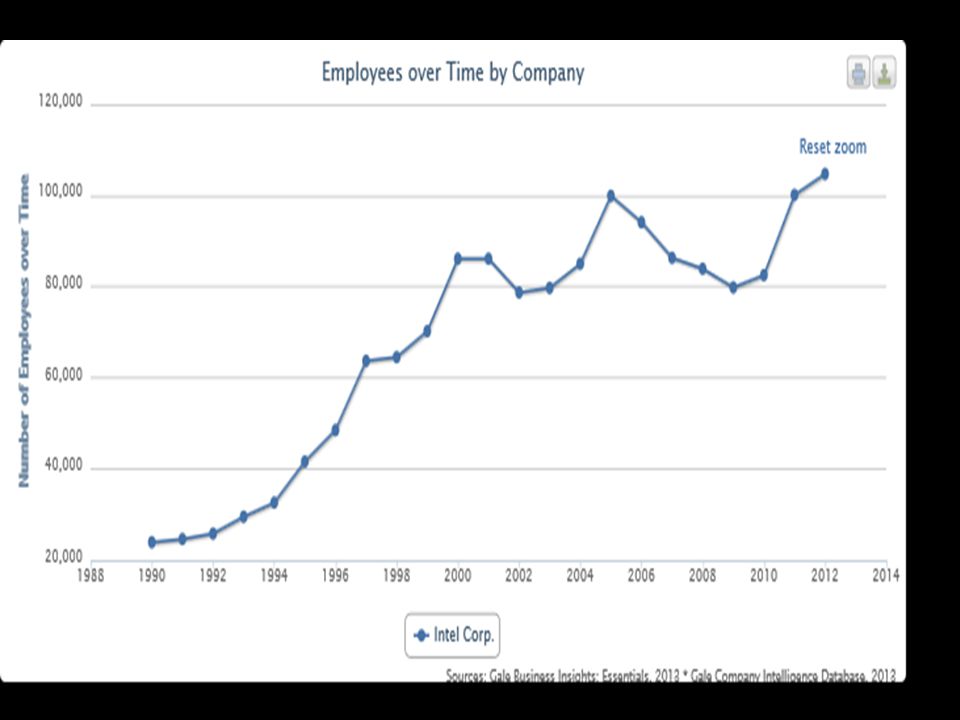

Introduction Founded by Robert Noyce and Gordon Moore in 1968. Largest semiconductor chip manufacturer in the world. Manufacturing plants found all over the world.

3

Industry Overview Industry started in 1960 and is one of the most prominent in the world. $249 billion dollar industry in revenue. Represents 10% of the worlds GDP alone. Growth rate of 13% in the past 20 years.

4

Industry Analysis Crashed in the 2008 economic crisis btu recovered fully by 2010. Moore’s law is a primary limiting factor. Cyclical supply and demand. Cost structures include large fixed costs.

5

Porter’s Five Forces Competitive Rivalry Top 5 companies have been in the same positions for 5 years. Each control different market segments. Barriers for crossing into other markets are extremely high.

6

Threat of Entrants One of the most expensive start up costs. Manufacturing plants can cost over 1$ billion. Technology changes yearly. Human capital is required, with high amounts of skilled labor. Government regulations.

7

Bargaining Power of Buyers Buyers have a high degree of power. Chips are purchased in large volumes or bulk orders. Relationships are formed between manufacturers and purchasers. Bargaining price can be influenced heavily to ensure partnerships are kept.

8

Bargaining Power of Supplier Suppliers do not have much power. With such few semiconductor manufacturers, price has to remain competitive from suppliers. Suppliers have to be able to maintain high demand for supplies in random spurts.

9

Substitute Products or Services No substitutes are available outside of the current competitors within the industry. Fake chips are currently being produced overseas. New materials are trying to be developed as substitutes.

10

Future Competitive Moves Innovation is an ongoing process in this industry. Being the first to develop new technologies wins the market segment. Intel is trying to break through into the mobile device market.

11

Intel’s Key Success Factors Strategy – retaining skilled labor force Process – Manufacturing chips and transitioning manufacturing plants with new technologies. Technical – Control and manage data for current technologies that are utilized. Helps innovate.

12

SWOT Analysis Strengths Recognized global brand. Advanced technology. First Microprocessor. Controls 80% of the market segment. Constant innovation. Large partnerships.

13

Weaknesses Strategy based on competitors. Large ego. Ignoring open market segments.

14

Opportunities Make innovations based on customer preference. Break into the mobile device market. Development of new products. Reduce fixed and variable costs.

15

Threats Changes in overseas currency. Rapid pace of the industry. Rebuilding FABS. Changing customer preference.

16

Potential Growth The semiconductor industry's average growth rate is highly stable with a annual growth rate of 12.95%. However the monthly growth rate experiences periods of rapid growth and decline such as last month were the monthly growth rate was -45.46%. This is in a large part due to new products coming available in the coming months and a shrinking of soon to be outmoded inventory

17

Barrier to Entry Intel has high security in its industry it would be extremely difficult if not impossible for firms to enter their market. Over Intel’s 45 years in the microprocessor industry they have built a stalwart reputation as the premier chipmaker in the semiconductor industry. This combination of a history of innovation and internal skill make Intel a company that could not be easily replicated. Further they have invested heavily into research and manufacturing process, these investments have kept them at the front of their industry.

18

Competition Among firms Intel is in a highly competitive industry, they benefit from being one of the largest entities in their industry, which gives them considerable leverage over their suppliers and consumers. This leverage makes it extremely difficult for any entity to compete on their level. They are able to keep their prominence in the industry because of the continued reinvestment in their manufacturing and research arms of their business.

19

product substitutability Intel’s products could be easily substituted if a competitor could manufacture a more advanced chip for cheaper. However, they have managed to keep at the forefront of the industry keeping a virtual monopoly on the PC processor industry. Their history of success makes it highly unlikely that someone would be able to make a competitive substitute on the level, quality, and quantity and tell is capable of producing.

20

Dependency on other products and services Intel is highly dependent on complimentary and supporting products because Intel is a part of a larger supply chain of the computer industry. However because of the size they make most of their suppliers and purchasers dependent on them because their abilities are not easily reproduced.

21

Political Factors Within Industry Increased regulation of chemicals used within Industry Environmental obstacles Patents, copyright, trade secrets Workers Safety

22

Intel and Political Factors Monitoring Chemicals Looking for ways to reduce water use Lawsuits with patent infringement

23

Economic Factors within Industry Concerns with World Economy Moore’s Law Taxes at home and abroad

24

Intel and Economic Factors How the World’s economic state is affecting Intel How PC’s are being replaced Intel getting into new industries to grow profits

25

Social Factors within Industry Consumers are dependent on technology Shift in social norms Corporate Corruption Focus on Corporate Social Responsibility

26

Intel and Social Factors Intel is trying to create newest and best technology What Intel is doing about Corporate Social Responsibility

27

Technological Factors within Industry Competitive industry Research and Development

28

Intel and Technological Factors Research and Development ZTE smart phones Foreign Investments

29

Competitive Factors within Industry Highly competitive Research and Development programs

30

Geographic Industry Factors Access to water Shift in location of companies

31

Categorizing the Objectives and Strategies of Competitors Intel’s competitor: Samsung Electronics Offense Approach: It is necessary for Intel to understand their competitors objectives and strategies. 5 Key Components: Competitive Scope, Strategic Intent, Market Share Objectuve, Competitive Position/Situation, Strategic Posture, Competitive Strategy

32

Competitive Scope Intel and Samsung are both Global Companies Samsung was calculated by Forbes to be the 20 th largest public, global corporation-Intel was ranked 77 th Both companies consider themselves to be the leader in global electronics

33

Strategic Intent Samsung and Intel both consider themselves to be and intend to be the leader in the memory industry Intel should be aware of Samsung’s Strategic Intent since it is the same as theirs

34

Market Share Objective Aggressive Expansion Strategy via both acquisitions and internal growth Samsung acquired Nokia Intel acquired McAfee

35

Competitive Position/Situation Both companies are well established in the memory Industry Innovation is essential Quality is necessary

36

Strategic Posture Ever-changing industry Offensive Strategy: updating technology, introducing new products, larger processors Defensive Strategy: must always catch up to the new and successful product

37

Competitive Strategy Differentiation through technological superiority New and innovative products Research and Development – Samsung spend more thena $6 Billion a year

38

Strategic Position and Action Evaluation (SPACE) Intel takes an Aggressive Posture 22-Nanometer Process Windows 8

Intel takes an Aggressive Posture 22-Nanometer Process Windows 8")

39

Weighted Competitive Strength Assessment: How Important are the Strengths? How Important are the Weaknesses? What is the cost of not responding?

40

Organizational Life Cycle Growth Stage – Business concept – Formation of business plans that obtain funding – Begins operations, establishes and expands customer base – New competitors may enter the market place – Demand for product begins to level off – Intel begins to mature

41

Organizational Life Cycle Mature Stage Pricing becomes more competitive New opportunities for existing products need to be recognized Re-enter the growth stage Maximizing Value While Remaining Mature

42

Organizational Life Cycle Decline Stage Intel has not reached the decline stage because of their ability to change, re- invent itself and re-grow Intel is dependent on the effectiveness of its leadership adopting sound values, strategies, and creating an aligned, empowered organization

43

Executive Office Andy D. Bryant- Chairman of the Board Executive Vice President William M. Holt-GM, Technology and Manufacturing Group Renée J. James-GM, Software and Services Group Thomas M. Kilroy-GM, Sales and Marketing Group Brian M. Krzanich- Chief Operating Officer Senior Vice President Sohail U. Ahmed- Director, Logic Technology Development Dian M. Bryant-GM Datacenter and Connected Systems Group Shmuel Eden- President, Intel Israel A. Douglas Melamed- General Counsel Vice President Michael A. Bell-GM, Mobile and Communications Group Rani N. Borkar-GM, Intel Architecture Development Group Robert E. Bruck-GM, Technology Manufacturing Engineering Christopher J. Bruno- President. Intel Americas Inc. Jonathan Khazman- GM, Visual and Parallel Computing Group Cary I. Klafter-Legal & Corporate Affairs, Director, Corporate Legal Corporate Secretary Michael C. Mayberry- Director, Components Research Christian Morales-GM, Europe, Middle East, Africa Babak Sabi-Director, Assembly and Test Technology Department Sunil R. Shenoy-GM Visual and Parallel Computing Group Stephen L. Smith- Director, Tablet Development Kimberly S. Stevenson- Chief Information Officer, Information Technology Douglas L. Davis-GM, Arizona Fab/Manufacturing site Hemann Eul-GM, Mobile Communications group Douglas W. Fisher-GM, Systems Software Division Ron Friedman-GM, Intel Architecture Development Group Erik Huggers-GM, Intel Media Ravi Jacob-Treasurer Joshua M. Walden-GM, Chief Operating Officer Strategy Office Xu Yang-President, Intel China Stuart C. Pann-General Manager, Business Manager Group Gregory R. Pearson- World Wide Sales and Operations Group Justin R. Rather-Director, Intel Labs, Intel Chief Technology Officer, Intel Senior Fellow Deborah S. Conrad- Chief Marketing Officer Robert B. Crooke-GM, Non-Volatile Memory Solutions Group Leslie S. Culbertson- Director, Finance Patricia Murray- Director, Leadership Strategy Kirk B. Skaugen-GM, PC Client Group Richard G. A. Taylor- Director, Human Resources David Perlmutter-GM, Intel Architecture Group, Chief Product Officer Stacy J. Smith-Chief Financial Officer and Director, Corporate Strategy Arvind Sodhani- President, Intel Capital Paul S. Otellini- President and Chief Executive Officer Intel’s Organizational Chart

44

Assessment of Cultural Elements Noyce, Moore, and Grove are the forces behind Intel

45

Assessment of Cultural Elements Executive’s style – Mentoring Program – It’s about what you want to know, not who you know Recognition of Individual – Awards and Honors Enforcement of Policies – Works with governments, organizations, and industries all around the world to enforces policies that encourage new ideas and protect resources

46

Assessment of Cultural Elements Degree of Innovation – Intel is a developer of the hardware at the heart of the modern PC Culture and Climate of Organization – Values initiative, risk taking, and confrontation of ideas Sense of Belonging to the Community – Support local schools, non profits, and educational math and science based programs all over the globe Maturity of Organization – Intel only continues to grow in size, securing more jobs all around the world

Similar presentations