Download presentation

Presentation is loading. Please wait.

1

HEALTH REFORM AND INEQUALITY USW 31, November 5, 2014 Theda Skocpol

2

On March 23, 2010, President Barack Obama signed into law the Patient Protection and Affordable Care Act

3

After two years of continuing public controversy and legal challenges from 26 states, the Supreme Court upheld the core provisions of Affordable Care on June 28, 2012

4

President Obama’s reelection on November 6, 2012 ensured that Affordable Care would survive through the initial stages of implementation.

5

U.S. Health System Before 2010 Expensive, with rapidly rising costs. Growing numbers of Americans without health insurance. Health insurance coverage – and public support for defraying its costs – skewed toward the elderly and the very poor with access to Medicare and Medicaid, and to regularly employed middle and upper income citizens whose employers offer coverage. Health insurance improves access to regular preventive care and care for chronic health problems, reduces worries about bankruptcy, and improves mental health. Some studies suggest significant improvements in physical health and longevity.

6

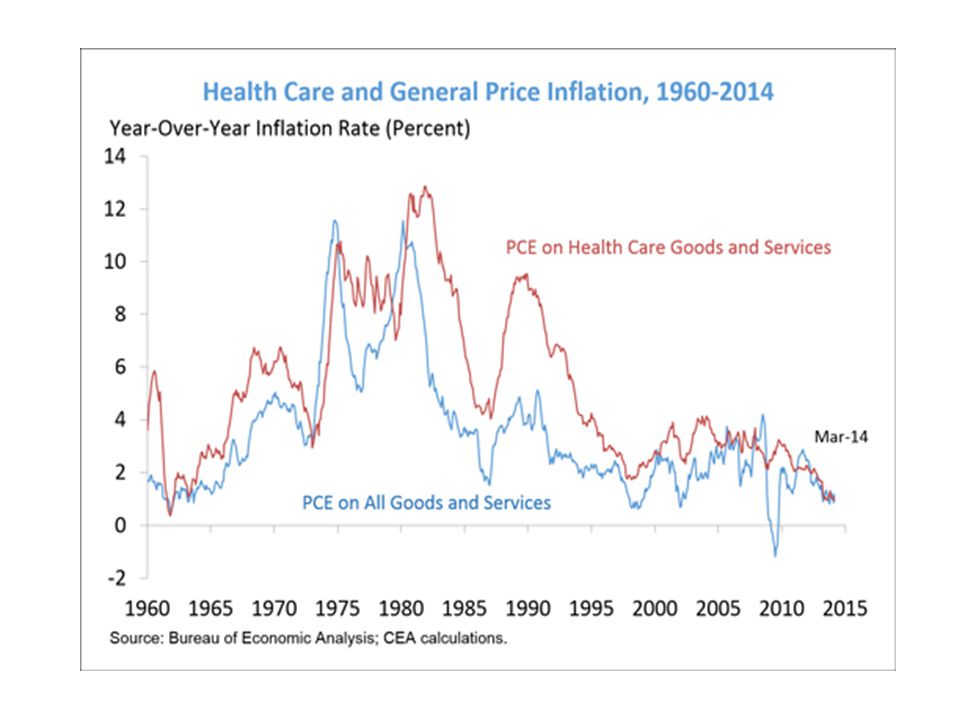

Source: SCIENTIFIC AMERICAN (April 1999), p.36. The U.S. health care system has very high -- and steeply rising -- costs.

7

Health Insurance Coverage in the U.S., 2009 NOTE: Includes those over age 65. Medicaid/Other Public includes Medicaid, CHIP, other state programs, military-related coverage, and those enrolled in both Medicare and Medicaid (dual eligibles). SOURCE: Kaiser Commission on Medicaid and the Uninsured and Urban Institute estimates based on the Census Bureau's March 2010 Current Population Survey. Total = 303.3 million

. SOURCE: Kaiser Commission on Medicaid and the Uninsured and Urban Institute estimates based on the Census Bureau s March 2010 Current Population Survey. Total = million.")

8

Uninsured Nonelderly vs. All Nonelderly, by Family Poverty Level, 2009 50.0 Million264.7 Million Under 100% 100% - 199% 200% - 399% 400% + NOTES: Data may not total 100% due to rounding. The Federal Poverty Level for a family of four in 2009 was $22,050 (according to the U.S. Census Bureau’s poverty threshold). Family size and total family income are grouped by insurance eligibility. SOURCE: Kaiser Commission on Medicaid and the Uninsured/Urban Institute analysis of 2010 ASEC Supplement to the CPS.

. Family size and total family income are grouped by insurance eligibility. SOURCE: Kaiser Commission on Medicaid and the Uninsured/Urban Institute analysis of 2010 ASEC Supplement to the CPS..")

9

Uninsured Rates Among Nonelderly by State, 2008-2009 <14% Uninsured (13 states & DC) 14 to 18% Uninsured (20 states) National Average = 18.1% SOURCE: Kaiser Commission on Medicaid and the Uninsured/Urban Institute analysis of 2009 and 2010 ASEC Supplements to the CPS., two-year pooled data. AZ WA WY ID UT OR NV CA MT HI AK AR MS LA MN ND CO IA WI SD MOKS TN NM OK TX AL MI IL OH IN KY NC PA VA WV SC GA FL ME NY NH MA VT NJ DE MD RI DC CT >18% Uninsured (17 states) NE

NE.")

10

Decrease in Employer Sponsored Insurance (million) 2.8% National Unemployment Rate Increase since 2008 (from 7.2% in Dec-08 to 10.0% in Nov-09) = 2.8 3.0 Medicaid /CHIP Enrollment Increase (million) Uninsured Increase (million) & 6.9 Note: Totals may not sum due to rounding and other coverage. Source: Based on John Holahan and Bowen Garrett, Rising Unemployment, Medicaid, and the Uninsured, prepared for the Kaiser Commission on Medicaid and the Uninsured, January 2009.Rising Unemployment, Medicaid, and the Uninsured Impact of the Rise in Unemployment on Health Coverage, 2008 to 2009

11

HOW DID THE UNITED STATES DEVELOP THIS KIND OF HEALTH CARE SYSTEM? Campaigns for government-subsidized and publicly guaranteed universal health insurance coverage repeatedly failed in the 20th-century United States. Government and private institutions ended up subsidizing employer-provided private insurance, the construction of acute-care facilities, and high-tech medicine. Private, fee-for-service physicians carved out a place for themselves as the key actors in an intricate institutional system. This persisted until recent times.

12

Patient Protection and Affordable Care Act of 2010 New rules of the game for insurance companies: make profits, but must serve more patients, better; cannot exclude sick people or those expected to become sick. Make insurance available affordable for most Americans: expansions of Medicaid and new subsidies for small businesses and lower and lower-middle income people to buy plans. Each state (or compact of states) establishes a regulated insurance exchange, on which plans are listed and can be compared by potential purchasers. Federal government sets up exchanges if states do not. Improvements in basic Medicare coverage, but cuts in high-end plans and slightly higher taxes for richest beneficiaries. New coverage for young people: parental insurance until age 26; expansions of Medicaid and subsidies to buy private plans.

establishes a regulated insurance exchange, on which plans are listed and can be compared by potential purchasers. Federal government sets up exchanges if states do not. Improvements in basic Medicare coverage, but cuts in high-end plans and slightly higher taxes for richest beneficiaries. New coverage for young people: parental insurance until age 26; expansions of Medicaid and subsidies to buy private plans..")

13

Expanding Coverage Under the Affordable Care Act * Medicaid also includes other public programs: CHIP, other state programs, Medicare and military-related coverage. The federal poverty level for a family of three in 2012 is $19,090. Numbers may not add to 100 due to rounding. SOURCE: KCMU/Urban Institute analysis of 2011 ASEC Supplement to the CPS. <139% (Medicaid) Federal Poverty Level 139-399% (Subsidies) 400%+ Private Non- Group Medicaid* Employer- Sponsored Insurance Uninsured 266 M Nonelderly

Federal Poverty Level % (Subsidies) 400%+ Private Non- Group Medicaid* Employer- Sponsored Insurance Uninsured 266 M Nonelderly.")

14

The ObamaCare Implementation Challenge Affordable Care features: –new rules for private insurance companies and employers; –subsidies and Medicaid extensions to expand coverage; –the establishment of “health insurance exchanges” to allow people to learn about eligibility for subsidies compare regulated private plans. Steps spread out 2010-2018, leaving citizens unaware of key benefits and allowing time for opponents to obstruct or undermine. Some national funding streams are set by law and HHS Secretary has considerable regulatory authority, BUT… Each of the fifty U.S. states makes pivotal decisions: –Set up exchanges? –Accept the expansion of Medicaid?

15

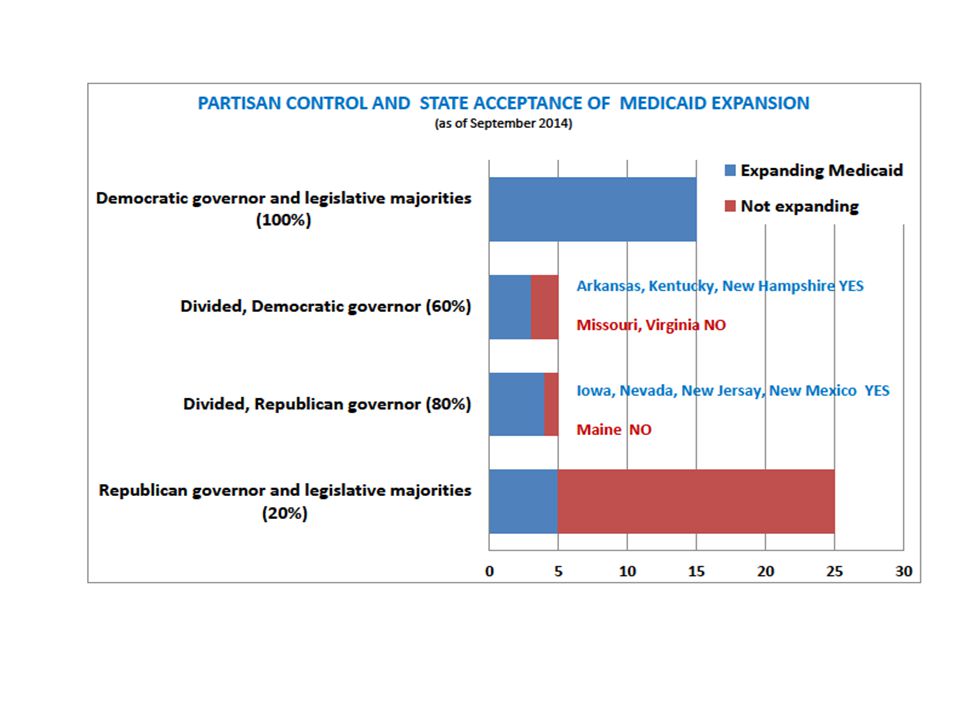

PARTISAN CONTROL AND STATE DECISIONS ABOUT OBAMACARE FULL GO STATES (n = 22) Arkansas Michigan CALIFORNIA MINNESOTA COLORADO NEVADA CONNECTICUT New Hampshire Delaware New Mexico HAWAII NEW YORK Illinois OREGON Iowa RHODE ISLAND KENTUCKY VERMONT MARYLAND WASHINGTON MASSACHUSETTS West Virginia MEDICAID WITHOUT EXCHANGE Arizona New Jersey North Dakota Ohio EXCHANGE BUT NOT MEDICAID Idaho REFUSNIK STATES ( n = 23; **= total) **Alabama Alaska North Carolina Florida **Oklahoma Georgia Pennsylvania Indiana South Carolina Kansas South Dakota Louisiana Tennessee Maine **Texas Mississippi Utah **Missouri Virginia Montana Wisconsin Nebraska **Wyoming HEALTH INSURANCE EXCHANGE? STATE-RUN or Partnership Exchange Default to the Federal Government MEDICAID EXPANSION? YES 26 states (plus DC) with 54% of US population NO 24 states with 46% of US population Partisan code from Pew: Red = strong GOP Orange = lean GOP Black = roughly even Light blue = lean Dem Blue = strong Dem Medicaid and Exchange from Kaiser Total non-cooperation from Commonwealth

with 54% of US population NO 24 states with 46% of US population Partisan code from Pew: Red = strong GOP Orange = lean GOP Black = roughly even Light blue = lean Dem Blue = strong Dem Medicaid and Exchange from Kaiser Total non-cooperation from Commonwealth.")

18

Affordable Care Implementation, Year One New and improved coverage: 17.2 to 27.7 million 6.06 to 8.41 million newly enrolled in Medicaid and Children’s Health Insurance. 9.45 to 16.14 million who have purchased qualified health plans on the exchanges. Up to 8.2 million more who purchased qualified plans outside the exchanges. 1.63 to 3.13 million young adults up to age 26 added to parents’ plans. Purchased on the Exchanges Well beyond 7 million projected for year one, and at least 85% paid so far. Young adult percentage is enough to sustain private plans. States that set up their own exchanges did better early, but later the federal exchange worked well. Leaders included California and New York and a mix of other states including Kentucky, Colorado, Vermont, Rhode Island, and Washington. Medicaid 26 states with 54% of Americans expanded Medicaid to cover near-poor in 2014. All Dem-led states expanded, most GOP-led did not; but some Republican governors have supported expansion and have gotten legislatures to go along. About 4.8 million adults, half minorities, fall into the “Medicaid gap” – they live in states not expanding the program but are too poor to get exchange subsidies. Hospitals in non-expanding states face a fiscal squeeze as federal payments for uncompensated care decline. People already eligible for Medicaid came “out of the woodwork” in all states.

22

Next Steps Medicaid will continue to add enrollments, and more states plan to expand (e.g., Pennsylvania, Utah) or may decide to accept expansion. Exchange enrollments open again in November – and major insurers have announced intentions to offer plans in additional states next year. Core funding for Medicaid expansion and premium subsidies is not subject to annual Congressional appropriations – and President Obama is likely to veto any major changes in the Affordable Care law through 2016. Congressional GOP and presidential aspirants will not stop talking about repeal, which they have promised to conservatives who want it. But especially in the Senate, many will join bipartisan votes to modify regulations and taxes. Already delayed mandates on employers may be dropped or loosened. Health care cost increases have slowed, and the Congressional Budget Office currently projects health reform as costing less than expected. Long-term cost control depends on experiments underway by hospitals, health care providers, and community clinics.

28

© 2014 The New York Times Company

30

States and Feds will Maneuver for a Decade Long-term dynamics in U.S. federalism may favor a “race to the middle” rather than the bottom. Good implementation in states like California, Kentucky, Minnesota, and Colorado may exert pressure on others. Republican-led innovators are emerging and may prove models for other Republican states. Open question whether the most conservative GOP-led states, (especially in the South where race and partisanship align) will permanently refuse to expand Medicaid. States will seek to upgrade health coverage and/or save money as coverage becomes nearly universal for legal residents: –Vermont aiming for single-payer (needs waiver in 2017) –Hawaii worries that its generous employer mandate could be undercut. –All states, especially those with high Medicaid standards, worry about reduced federal subsidies. –Some states may include a “public option” on regulated exchanges, create regional partnerships, partially privatize Medicaid, expand community clinics, or institute other reforms.

will permanently refuse to expand Medicaid. States will seek to upgrade health coverage and/or save money as coverage becomes nearly universal for legal residents: –Vermont aiming for single-payer (needs waiver in 2017) –Hawaii worries that its generous employer mandate could be undercut. –All states, especially those with high Medicaid standards, worry about reduced federal subsidies. –Some states may include a public option on regulated exchanges, create regional partnerships, partially privatize Medicaid, expand community clinics, or institute other reforms..")

Similar presentations

Arkansas Michigan CALIFORNIA MINNESOTA COLORADO NEVADA CONNECTICUT New Hampshire.>")

of 30 or higher. Body Mass.>")

Florida (FL) Georgia (GA) Mississippi (MS) Louisiana (LA) Arkansas (AR) Tennessee (TN)>")