Download presentation

Presentation is loading. Please wait.

1

BOOK KEEPING I LECTURE 5

2

GOALS OF LECTURE Part A: Journal Part B: Stock A/c Drawings

Carriage Inwards & Carriage Outwards Some Basic Ratios

3

ACCOUNTING PROCESS AND RECORDS

▲ Accounting records are any listing or book which records the transactions of a business in a logical manner. This is achieved by the use of books of prime entry and the Ledger. Journals ( Journal is one of the books of prime entry) is a detail diary in which the transactions of each day are recorded. They are used as an initial ‘store’ of information of the business transactions prior to storing the information in the ledger accounts. Step 1 Step 2 Transactions journals Ledger accounts Trial Balance Financial statements

is a detail diary in which the transactions of each day are recorded. They are used as an initial ‘store’ of information of the business transactions prior to storing the information in the ledger accounts. Step 1. Step 2. Transactions. journals. Ledger. accounts. Trial Balance. Financial. statements.")

4

The Accounting Process

Transaction Journal General Ledger (T-Accounts) Trial Balance Financial Statements (Income Statement and Balance Sheet) Documents verifying a transaction: Bank deposit documentation Invoices Cheques Stock certificates

Trial Balance Financial Statements (Income Statement and Balance Sheet) Documents verifying a transaction: Bank deposit documentation. Invoices. Cheques. Stock certificates.")

5

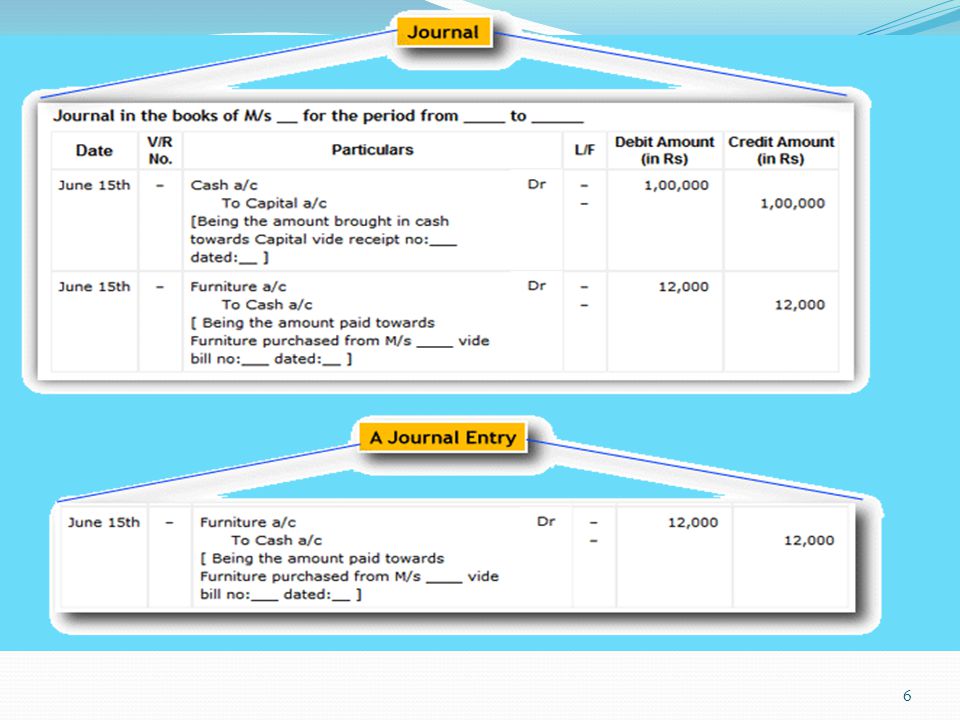

ACCOUNTING RECORDS ▲ The journal is called a book of prime entry meaning the ‘first book’. A Journal is prepared in a specific format as shown in the next slide.

7

Journal Four parts: a)Date of transaction

b)Title of account debited with dollar amount c)Title of account credited with dollar amount d)Brief explanation of transaction

Title of account debited with dollar amount. c)Title of account credited with dollar amount. d)Brief explanation of transaction.")

8

To sum up: the Journal and the Ledger

Chronological record of transactions Organized by date Ledger The book holding all the accounts and their balances Organized by account

9

Other Books of Prime Entry

Book of Prime Entry Transaction type Sales Day Book Credit Sales Purchases Day Book Credit Purchases Sales Returns day Book Returns of goods sold on credit Purchases returns day book Returns of goods bought on credit Cash Book All bank transactions Petty Cash Book All small cash transactions

10

Example of Journal: Ned Brown opened a medical practice in San Diego, California. 1 Record the preceding transactions in the journal of Ned Brown, M.D., P.C. Include an explanation. Jan 1: The business received $29,000 cash and issued common stock. Jan 2 Purchased medical supplies on account, $14,000. Jan 2 Paid monthly office rent of $2,600. Jan 3 Recorded $8,000 revenue for service rendered to patients on account.

11

Jan 1: The business received $29,000 cash and issued common stock

Cash received indicates cash increases Cash is an Asset; Assets increase with debits .Issued common stock; indicates equity is increasing Increase equity with credits DATE DESCRIPTION DEBIT CREDIT JAN 1 Cash 29000 Common Stock Issued stock Jan. 2: Purchased medical supplies on credit, $14,000. Medical Supplies, an asset, is increasing .Assets increase with debits. On credit increases accounts payable, a liability Increase liabilities with credits DATE DESCRIPTION DEBIT CREDIT JAN 2 Medical supplies 14000 Accounts payable Purchased supplies on account

12

Jan. 2: Paid monthly office rent of $2,600

Jan. 2: Paid monthly office rent of $2,600 .Paid rent, an expense, expense is increasing .Expenses increase with debits .Paid cash, cash is an asset ,decrease assets with credits DATE DESCRIPTION DEBIT CREDIT JAN 2 Rent Expense 2600 Cash Paid Office Rent Jan. 3: Recorded $8,000 revenue for service rendered to patients on credit. On credit indicates Accounts receivable increase .Accounts receivable is an Asset, Assets increase with debits .Rendered services, services are revenues, indicates revenues are increasing Increase revenues with credits DATE DESCRIPTION DEBIT CREDIT JAN 3 Accounts receivable 8000 Service Revenue Performed service on account

13

Copying amounts from the journal to the ledger

14

EXERCISES ON JOURNAL p.86-94

15

The Stock Account and the double entry bookkeeping with the Trading Account

The Opening Balance goes to trading account and the Closing Balance comes from the trading account Dr Name of Account Cr Date B/ce B/d X € Date Trading A/c X€ Date Trading A/c Y€ Date B/ce C/d Y € Date B/ce B/d Y €

16

Carriage Inwards and Carriage Outwards

Carriage refers to the costs of transporting goods to and from the firm. From the buyer’s point of view, the delivery charge would he referred to as “carriage inwards”. Any such carriage charges should be debited to the carriage inwards account in the general ledger. The carriage inwards account is written off to the trading account at the end of the accounting period.

17

When the buyer sells the goods to his customer, he incurs further delivery charges. This cost is referred to as ‘carriage outwards”. These costs are debited to the carriage outwards account in the general ledger. Any carriage outwards charges are usually included in an item called ‘selling and distribution costs”. Since this cost is incurred after the goods have been made ready for sale, the account is written off to the profit and loss account at the end of the accounting period. Each type of carriage will be an expense and therefore will have a debit balance in the trial balance. However, these two carriages will appear in different sections of the trading and profit and loss account.

18

Accounting Treatment of Carriage Inwards and Carriage Outwards

Journal Entry for Carriage Inwards: Debit Carriage Inwards Credit Bank Journal Entry for Carriage Outwards: Debit Carriage Outwards Treatment in Trading, Profit and Loss Accounts: Carriage inwards Trading account expense Carriage outwards Profit & loss account expense

19

Summary: Carriage inwards is connected with the cost of getting goods into the business and ready for sale. As a result, it will be added on in the calculation for the cost of goods sold. Carriage outwards does not have anything to do with the cost of getting goods into saleable condition. Therefore it will appear with all the other overhead expenses in the profit and loss account. Good to know: Nowadays, the price quoted for goods being purchased will usually be inclusive of any delivery charge, and so a separate charge for carriage inwards (or outwards) is not very common. In cases where separate carriage inwards charges are incurred, the cost should be added on to the cost of purchases in the trading account. Consequently, a proportion of carriage inwards charges should be added to the purchase cost when determining the cost of closing stock.

is not very common. In cases where separate carriage inwards charges are incurred, the cost should be added on to the cost of purchases in the trading account. Consequently, a proportion of carriage inwards charges should be added to the purchase cost when determining the cost of closing stock.")

20

Drawings Are the money or goods that the owner of the business is taking out of the company (draws) for his own personal use. The Drawings account is always debited and the account affected is credited. At the end of the year the drawings account goes to Capital Account and reduces it. If the owners takes cash out of the business: Journal Entry: Debit Drawings a/c Credit Cash/Bank If the owners takes goods out of the business: Debit Drawings a/c Credit Purchases a/c

for his own personal use. The Drawings account is always debited and the account affected is credited. At the end of the year the drawings account goes to Capital Account and reduces it. If the owners takes cash out of the business: Journal Entry: Debit Drawings a/c. Credit Cash/Bank. If the owners takes goods out of the business: Debit Drawings a/c. Credit Purchases a/c.")

21

Capital Account Loss for the year x B/ce b/d x Drawings x Net Profit x

B/ce c/d x Cash injections x x x B/ce b/d x

22

Some Basic Ratios

23

1. Gross Margin ratio (%) =Gross Profit to Sales

Or = Sales – Cost of Sales = ……..% It means that ….% of sales is gross profit. Is the percentage that a company keeps from its sales, after deducting the direct costs of producing the goods and services sold by the company. The higher is that ratio the better!!! Gross Margin Ratio is also called Gross Profit Margin Margin is profit expressed as a percentage of the sales.

24

2.Mark up ratio Mark up Ratio = Sales – Cost of Sales = ……..%

Or Gross Profit =……..% Cost of Sales Mark-up is profit expressed as a percentage of the cost of goods sold.

25

3. Stock Turnover = Cost of Sales / Stock= ……times

Indicates how rapidly inventory is being sold. Usually, the faster inventory is sold, the more profitable the firm will be. Firms with rapid turnover might include grocery stores, donut shops, etc. A larger inventory turnover number is usually preferred over a smaller number.

26

4. Net Profit to Sales Ratio

Net Profit to Sales Ratio = Net Profit = …..% Sales It means that ….% of sales is Net profit. Is the percentage that a company keeps from its sales, after deducting the direct costs of producing the goods and services sold by the company and all other expenses: selling, administrative, general expenses and interest. So after deducting all costs and expenses.

Similar presentations

>")