Download presentation

Presentation is loading. Please wait.

1

FURTHER CONSIDERATIONS (By Frank Wood and Alan Sangster, 2005)

")

2

Purchase If we buy GOODS we need to record as Purchase. If we buy anything other than goods, we need to enter its name. e.g: We bought goods on credit: Dr Purchase Cr Accounts Payable e.g: We bought machinery on credit: Dr Machinery Cr Accounts Payable

3

Sale If we sell GOODS we need to record as Sales. If we sell anything other than goods, we need to enter its name. e.g: We sold goods by check: Dr Bank Cr Sales e.g: We sold machinery on account: Dr Account Receivable Cr Machinery

4

We must distinguish between transactions that cause stock to increase and those that cause stock to decrease. Let’s deal with each of these in turn.

5

1 Increase in stock This can be due to one of two causes: (a) The purchase of additional goods. (b) The return in to the business of goods previously sold. The reasons for this are numerous. The goods may have been the wrong type; they may, for example, have been surplus to requirements or faulty.

The return in to the business of goods previously sold. The reasons for this are numerous. The goods may have been the wrong type; they may, for example, have been surplus to requirements or faulty..")

6

To distinguish the two aspects of the increase of stocks of goods, two accounts are opened: (i) a Purchases Account – in which purchases of goods are entered; and (ii) a Returns Inwards Account – in which goods being returned in to the business are entered. (This is also known as the Sales Returns Account.) So, for increases in stock, we need to choose which of these two accounts to use to record the debit side of the transaction.

So, for increases in stock, we need to choose which of these two accounts to use to record the debit side of the transaction..")

7

2 Decrease in stock. Ignoring things like wastage and theft, this can be due to one of two causes: (a) The sale of goods. (b) Goods previously bought by the business now being returned to the supplier. Once again, in order to distinguish the two aspects of the decrease of stocks of goods, two accounts are opened: (i) a Sales Account – in which sales of goods are entered; and (ii) a Returns Outwards Account – in which goods being returned out to a supplier are entered. (This is also known as the Purchases Returns Account.)

The sale of goods. (b) Goods previously bought by the business now being returned to the supplier. Once again, in order to distinguish the two aspects of the decrease of stocks of goods, two accounts are opened: (i) a Sales Account – in which sales of goods are entered; and (ii) a Returns Outwards Account – in which goods being returned out to a supplier are entered. (This is also known as the Purchases Returns Account.).")

8

So, for decreases in stock, we need to choose which of these two accounts to use to record the credit side of the transaction. As stock is an asset, and these four accounts are all connected with this asset, the double entry rules are those used for assets.

9

Returns inwards On 5 August 20X8, goods which had been previously sold to F Lowe for £29 are now returned to the business. This could be for various reasons such as: we sent goods of the wrong size, the wrong colour or the wrong model; the goods may have been damaged in transit; the goods are of poor quality.

10

1 The asset of stock is increased by the goods returned. Thus, a debit representing an increase ofan asset is needed. This time, the movement of stock is that of ‘returns inwards’. The entry required is a debit in the Returns Inwards Account 2 There is a decrease in an asset. The debt of F Lowe to the business is now reduced. A credit is needed in F Lowe’s account to record this.

12

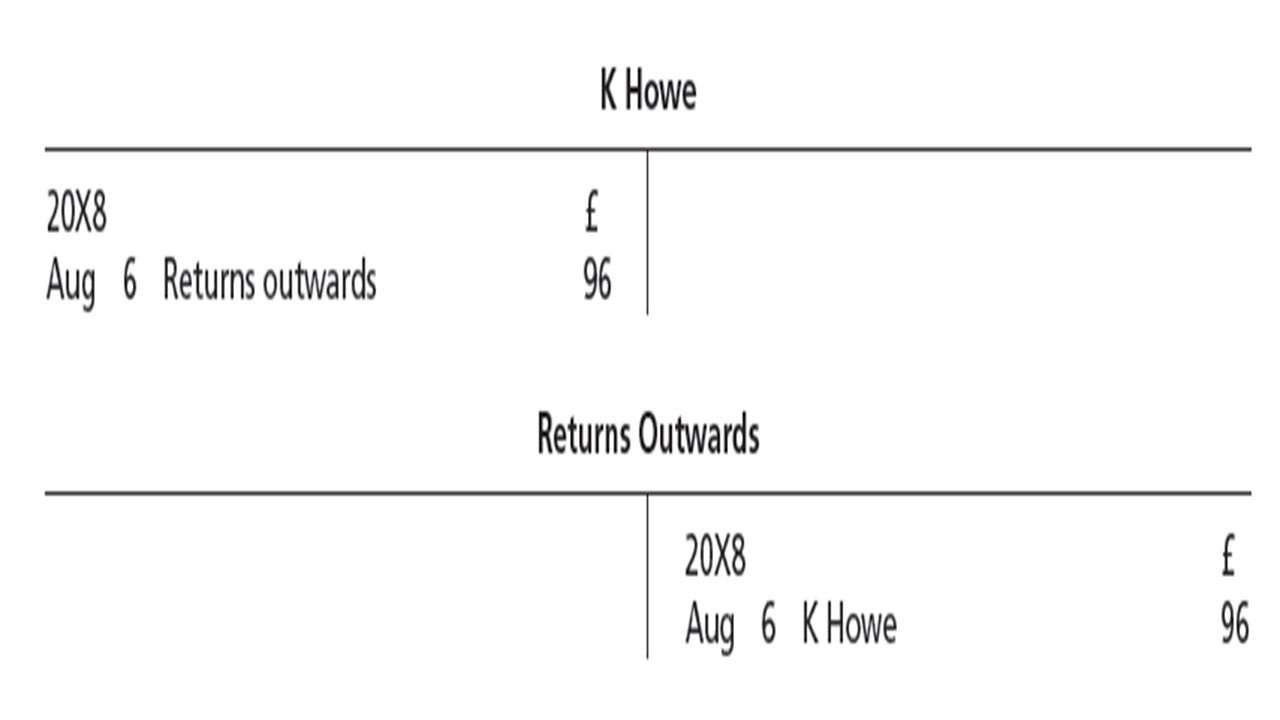

Returns outwards On 6 August 20X8, goods previously bought for £96 are returned by the business to K Howe. 1 The liability of the business to K Howe is decreased by the value of the goods returned. The decrease in a liability needs a debit, this time in K Howe’s account. 2 The asset of stock is decreased by the goods sent out. Thus, a credit representing a reduction in an asset is needed. The movement of stock is that of ‘returns outwards’ so the entry will be a credit in the Returns Outwards Account.

14

For example: Enter the following transactions in the journal of L Linda: MAY 8 Sold goods on credit to H Rise £1,374.MAY 12 H Rise (Debtor) returned goods to us £65.MAY 14 Sold goods on credit to G Pate £535 and R Sim £262.MAY 15 Bought goods on credit from B Brown £1,530MAY 17 We returned goods to B Brown £94

returned goods to us £65.MAY 14 Sold goods on credit to G Pate £535 and R Sim £262.MAY 15 Bought goods on credit from B Brown £1,530MAY 17 We returned goods to B Brown £94")

15

MAY 8 Sold goods on credit to H Rise £1,374. 8 May: Dr. H Rise (Acc Receivable) 1374 Cr. Sale 1374

1374 Cr. Sale 1374")

16

MAY 12 H Rise (Debtor) returned goods to us £65. 12 May Dr. Return Inwards 65 H Rise (Acc Receivable) 65

65.")

17

MAY 14 Sold goods on credit to G Pate £535 and R Sim £262. 14 May: Dr. G Pate (Acc Receivable) 535 Dr. R Sim (Acc Receivable) 262 Cr. Sale 797

535 Dr. R Sim (Acc Receivable) 262 Cr. Sale 797.")

18

MAY 15 Bought goods on credit from B Brown £1,530 15 May Dr. Purchase 1530 Cr. B Brown (Acc Payable) 1530

")

19

MAY 17 We returned goods to B Brown £94 17 May Dr. B Brown (Acc Payable) 94 Cr. Return Outwards 94

94 Cr. Return Outwards 94")

20

Carriage If you have ever purchased anything by mail order or over the Internet, you have probably been charged for ‘postage and packing’. When goods are delivered by suppliers or sent to customers, the cost of transporting the goods is often an additional charge. In accounting, this charge is called ‘carriage’. When it is charged for delivery of goods purchased, it is called carriage inwards. Carriage charged on goods sent out by a business to its customers is called carriage outwards.

21

When goods are purchased, the cost of carriage inwards may either be included as a hidden part of the purchase price, or it may be charged separately. For example, suppose your business was buying exactly the same goods from two suppliers. One supplier might sell them for £100 and not charge anything for carriage. Another supplier might sell the goods for £95, but you would have to pay £5 to a courier for carriage inwards, i.e. a total cost of £100. In both cases, the same goods cost you the same total amount. It would not be appropriate to leave out the cost of carriage inwards from the ‘cheaper’ supplier in the calculation of gross profit, as the real cost to you having the goods available for resale is £100. As a result, in order to ensure that the true cost of buying goods for resale is always included in the calculation of gross profit, carriage inwards is always added to the cost of purchases in the trading account.

22

Carriage outwards is not part of the selling price of our goods. Customers could come and collect the goods themselves, in which case there would be no carriage out expense for us to pay or to recharge to our customers. Carriage outwards is always entered in the profit and loss account.It is never included in the calculation of gross profit. Suppose that in the illustration shown in this chapter, the goods had been bought for the same total figure of £31,200 but, in fact, £29,200 was the figure for purchases and £2,000 for carriage inwards.

23

Drawings Sometimes the owners will want to take cash out of the business for their private use. This is known as drawings. The following example illustrates the entries for drawings: On 25 August, the owner takes £50 cash out of the business for his own use. Effect Action 1 Capital is decreased by £50 Debit the drawings account £50 2 Cash is decreased by £50 Credit the cash account £50

24

COST OF GOODS SOLD Net profit, found in the Profit and Loss Account, consists of the gross profit plus any revenue other than that from sales, such as rents received or commissions earned, less the total costs used up during the period other than those already included in the ‘cost of goods sold’. Where the costs used up exceed the gross profit plus other revenue, the result is said to be a net loss. Thus: Net profit is what is left of the gross profit after all other expenses have been deducted.

25

We have already seen that gross profit is calculated as follows: It would be easier if all purchases in a period were always sold by the end of the same period. In that case, cost of goods sold would always equal purchases. However, this is not normally the case and so we have to calculate the cost of goods sold as follows:

26

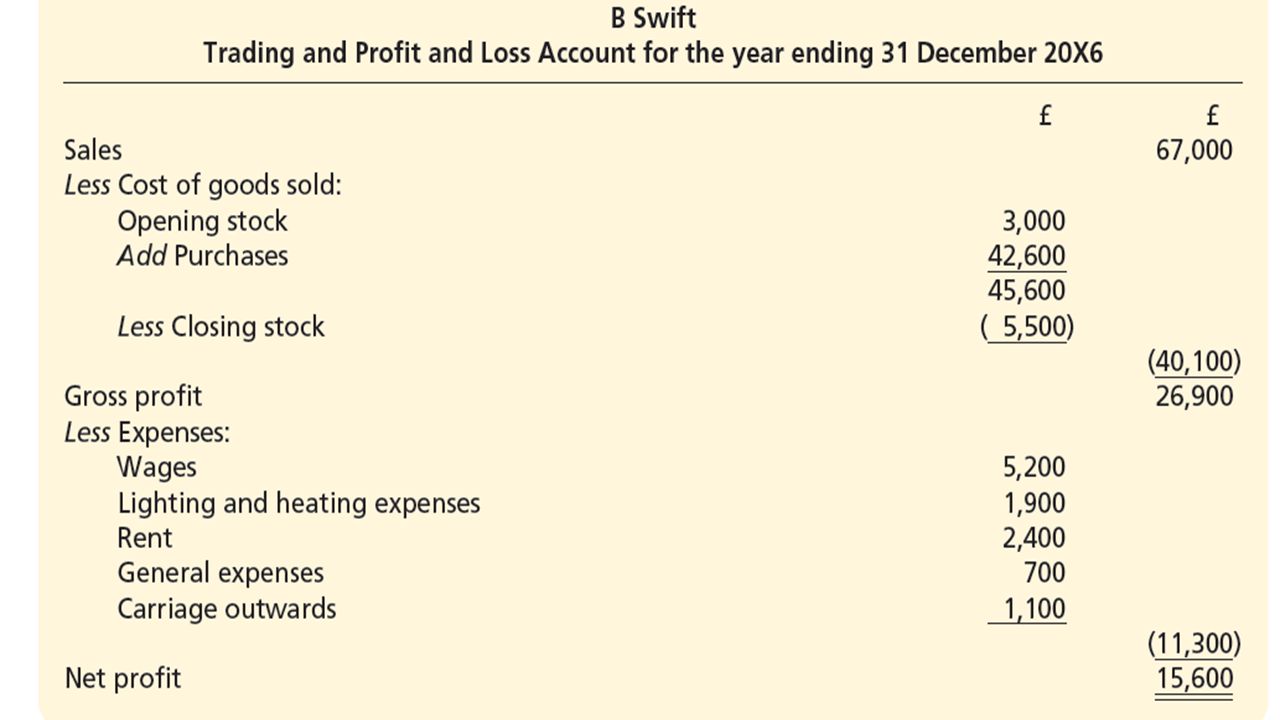

What we bought in the period: Less Goods bought but not sold in the period: Purchases- (Closing stock)= Cost of goods sold In Swift’s case, there are goods unsold at the end of the period. However, there is no record in the accounting books of the value of this unsold stock. The only way that Swift can find this figure is by stocktaking at the close of business on 31 December 20X5. To do this he would have to make a list of all the unsold goods and then find out their value. The value he would normally place on them would be the cost price of the goods, i.e. what he paid for them. Let’s assume that this is £3,000.

27

The cost of goods sold figure will be: £ Purchases 29,000 Less Closing stock ( 3,000) Cost of goods sold 26,000 Based on the sales revenue of £38,500 the gross profit can be calculated: Sales − Cost of Goods Sold = Gross Profit £38,500 − £26,000 = £12,500

Cost of goods sold 26,000 Based on the sales revenue of £38,500 the gross profit can be calculated: Sales − Cost of Goods Sold = Gross Profit £38,500 − £26,000 = £12,500")

31

WORKING CAPITAL Net liquid assetsNet liquid assets computed by deducting current liabilities from current assets. The amount of available working capital is a measure of a firm's ability to meet its short-term obligations.current liabilitiescurrent assetsamountmeasureabilityshort-term Working Capital = Current Asset – Current Liabilities Current Assets are the assets that are available within 12 months. Current Liabilities are the liabilities that are due within 12 months.

32

Here is some balance sheet information about HMB Companybalance sheet Balance Sheet for Company HMB Cash$10,000Accounts Payable$30,000 Bank$60,000Bank loan due within 12 months$20,000 Accounts Receivable$40,000Notes Payable$ 5,000 Equipments$50,000Long Term Debt$10,000 Total Current Asset$160,000Total Current Liabilities$65,000

33

Calculate the company’s working capital. Working Capital = Current Asset – Current Liabilities Working Capital = 110,000 – 55,000 Working Capital = $55,000

34

Working capital is a common measure of a company's liquidity, efficiency, and overall health. Because it includes cash, inventory, accounts receivable, accounts payable, the portion of debt due within one year, and other short-term accounts, a company's working capital reflects the results of a host of company activities, including inventory management, debt management, revenue collection, and payments to suppliers.

35

Positive working capital generally indicates that a company is able to pay off its short-term liabilities almost immediately. Negative working capital generally indicates a company is unable to do so. This is why analysts are sensitive to decreases in working capital; they suggest a company is becoming overleveraged, is struggling to maintain or grow sales, is paying bills too quickly, or is collecting receivables too slowly. Increases in working capital, on the other hand, suggest the opposite.

Similar presentations

There are 10 accounts in the ledger. How do you calculate.>")