Download presentation

Presentation is loading. Please wait.

1

Khon Kaen University International College Business in the Greater Mekong Sub-region Course number 050 451 - Second semester 2013 Wednesdays at 9:00 in room 823 Lecturer: Michael Cooke office room 817 E-mail: Michco@kku.ac.th Web: KKU.AC.TH/Michco

2

Field Trip with GMS Tourism Class To Southern Laos (Pakse) by bus Leave 10 January (Friday) Return January 13 th (Monday) Ten seats available Cost 8,900 baht per person plus visa Includes transportation, hotel, some meals Cross border into Laos near Ubon Contact Aj. Chonlada or Aj. Michael

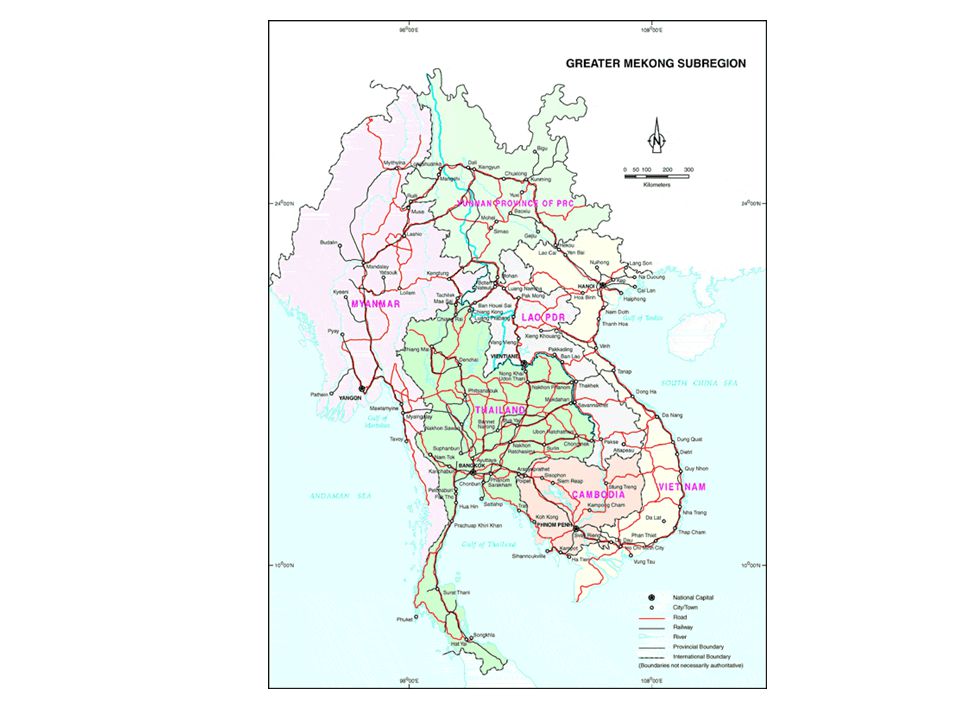

3

Pakse Laos

4

ICRG Country risk information (oldest source) https://www.prsgroup.com/ICRG_TableDef.as px https://www.prsgroup.com/ICRG_TableDef.as px If the link does not work: www.prsgroup.comwww.prsgroup.com ◦ Ask for free samples Give e-mail address and name, purpose = education Decline contact if you wish ◦ On free samples page, click *To see a list of ICRG Tables ◦ Download the sample 4

px px If the link does not work: ◦ Ask for free samples Give address and name, purpose = education Decline contact if you wish ◦ On free samples page, click *To see a list of ICRG Tables ◦ Download the sample 4")

5

Find a successful industry in GMS, or one which shows potential to be successful (13 Nov) Explore reasons the industry located in GMS What is the nature of the business (capital or labor intensive, etc) Any spillover effects? What was the mode of entry for the businesses? Study a GMS country in which the industry is successful (4 Dec) What are the strengths of that country from a business perspective? What are the weaknesses? Look for barriers to further business success in the country How do you see the business evolving (5 Feb) Effect of ASEAN or other alliances (trade, labor mobility, etc) Relevant demographic, economic, trade projections Infrastructure, education, and other changes as a result of government or business initiatives Advice you would give to government units to encourage industry growth

What are the strengths of that country from a business perspective. What are the weaknesses. Look for barriers to further business success in the country How do you see the business evolving (5 Feb) Effect of ASEAN or other alliances (trade, labor mobility, etc) Relevant demographic, economic, trade projections Infrastructure, education, and other changes as a result of government or business initiatives Advice you would give to government units to encourage industry growth.")

7

Mekong Watershed 36% of the River’s Volume is from Laos

8

Mekong River Commission Secretariat

9

Resources JETRO (Japan External Trade Organization) established 1958 helps small to medium size Japanese firms maximize their global export potential JETRO-Institute of Developing Economies (IDE) Bangkok Research Center links – http://www.ide.go.jp/English/Links/southeast_asia.html http://www.ide.go.jp/English/Links/southeast_asia.html – Good for links to government and university sites for the GMS countries Institute of Developing Economies (IDE) Bangkok Research Center publications – http://www.ide.go.jp/English/Publish/Download/Brc/ http://www.ide.go.jp/English/Publish/Download/Brc/ – Relevant and relatively recent research reports – Examples: "Five Triangle Areas in the Greater Mekong Subregion" Edited by ISHIDA Masami / Published in 2013 "Economic Reforms in Myanmar: Pathways and Prospects" Edited by HANK LIM and YASUHIRO YAMADA / Published 2013 "Cause and Consequence of FIRMS' FTA Utilization in Asia" Edited by HAYAKAWA Kazunobu / Published in 2012 "Emerging Economic Corridors in the Mekong Region" Edited by ISHIDA Masami / Published in 2012 "Industrial Readjustment in the Mekong River Basin Countries: Toward the AEC" Edited by Yasushi UEKI AND TEERANA BHONGMAKAPAT / Published in 2012 "Investment Climate of Major Cities in CLMV Countries" Edited by ISHIDA Masami / Published in 2010 "Economic Relations of China, Japan and Korea with the Mekong River Basin Countries (MRBCs)" Edited by KAGAMI Mitsuhiro / Published in 2010 "Major Industries and Business Chance in CLMV Countries" Edited by UCHIKAWA Shuji / Published in 2009 "A China-Japan Comparison of Economic Relationships with the Mekong River Basin Countries" Edited by KAGAMI MItsuhiro / Published in 2009 Mekong Institute (on the KKU Campus) http://www.mekonginstitute.org/http://www.mekonginstitute.org/

established 1958 helps small to medium size Japanese firms maximize their global export potential JETRO-Institute of Developing Economies (IDE) Bangkok Research Center links – – Good for links to government and university sites for the GMS countries Institute of Developing Economies (IDE) Bangkok Research Center publications – – Relevant and relatively recent research reports – Examples: Five Triangle Areas in the Greater Mekong Subregion Edited by ISHIDA Masami / Published in 2013 Economic Reforms in Myanmar: Pathways and Prospects Edited by HANK LIM and YASUHIRO YAMADA / Published 2013 Cause and Consequence of FIRMS FTA Utilization in Asia Edited by HAYAKAWA Kazunobu / Published in 2012 Emerging Economic Corridors in the Mekong Region Edited by ISHIDA Masami / Published in 2012 Industrial Readjustment in the Mekong River Basin Countries: Toward the AEC Edited by Yasushi UEKI AND TEERANA BHONGMAKAPAT / Published in 2012 Investment Climate of Major Cities in CLMV Countries Edited by ISHIDA Masami / Published in 2010 Economic Relations of China, Japan and Korea with the Mekong River Basin Countries (MRBCs) Edited by KAGAMI Mitsuhiro / Published in 2010 Major Industries and Business Chance in CLMV Countries Edited by UCHIKAWA Shuji / Published in 2009 A China-Japan Comparison of Economic Relationships with the Mekong River Basin Countries Edited by KAGAMI MItsuhiro / Published in 2009 Mekong Institute (on the KKU Campus)")

10

Mekong Institute Focus on Labor http://www.mekonginstitute.org/images/abook_file/policy_bri ef_labour_supply.pdf http://www.mekonginstitute.org/images/abook_file/policy_bri ef_labour_supply.pdf From a study of a Laos SEZ : “ The breakdown in occupational skills indicate mismatches in supply and demand for specific skills areas such as IT/computer operators, maintenance mechanics, welders, sewers/dressmakers, gem lapicides, and others. On the other hand, majority of students at TVET schools enroll in accountancy and Business management courses.” From a study of a Cambodian SEZ: “ The new SEZs that have been set up in the border areas with Thailand and Vietnam have reduced the pull factor to migrate to Phnom Penh for work. The preference of students for enrolling in academic courses such as management and accounting due to the perception that vocational training will lead to a career of hard labor and low wages in factories. In Laos, many prefer to migrate to Thailand where they can earn more even without the necessary educational credentials.”

11

Projections In 1989 Vietnam’s population was expected to reach 105MM by 2010 – Government made efforts to reduce population growth – Vietnam reached 90MM in 2013 – Declining birthrates have affected many countries Vietnam experiences a ‘demographic bonus’ – Few non-working age young – Relatively small number of elderly dependents – Same story as Thailand, a few years later

12

Effect of declining birth-rates in the 1990s Vietnam 1990 – 67MM 2015 – 92MM (added 25MM) Thailand 1990 – 57MM 2015 – 71MM (added 14MM) http://www.indexmundi.com/vietnam/age_structure.html

Thailand 1990 – 57MM 2015 – 71MM (added 14MM)")

13

Effect of declining birth-rates in the 1990s Cambodia 1990 – 9.5MM 2015 – 15.0MM Laos 1990 – 4.1MM 2015- 6.6MM http://www.indexmundi.com/

14

Effect of declining birth-rates in the 1990s Myanmar 1990 – 39.0 2015 – 50.0MM (added 11MM Thailand 1990 – 57MM 2015 – 71MM (added 14MM) http://www.indexmundi.com/

")

15

Effect of declining birth-rates in the 1990s China 1990 – 1,145MM 2015 – 1,370MM (added 225MM) Thailand 1990 – 57MM 2015 – 71MM (added 14MM) http://www.indexmundi.com/

Thailand 1990 – 57MM 2015 – 71MM (added 14MM)")

16

City Singles (Excerpts from the Bangkok Post 30 September, 2013) Urban women tend to prefer single status to those in rural areas. About 30% of Bangkok woman are single. Thai women are tending to marry later, or not at all Even those in a marriage may postpone having a child because of the high cost of raising a child The total fertility rate (TFR), a direct measure referring to births per woman, is now the lowest in Thai history, according to Pramote Prasartkul, of Mahidol University's Institution for Population and Social Research (IPSR). The TFR dropped from more than six births per woman before 1970 to 1.6 at present. In the Southeast Asian region, only Singapore has a lower TFR rate than Thailand at 1.2. Vietnam is at 1.8, Malaysia is at 2.6, and Cambodia, Laos and Myanmar are more than three. Due to the low TFR, the IPSR estimates people in the workforce aged between 15 and 59 years will decrease from 67% of the Thai population in 2010 to 55.1% in 2040 The 11th National Economic and Social Development Plan (2012-2016), approved by the cabinet last year, expresses concern about the change in demographic structure. The plan focuses on improving the workforce's skills and expertise to meet emerging challenges as well as technology development. Besides the low birth rate, longer life expectancy is also a factor in Thailand's rapidly ageing society. Thailand was classified as an ageing society in 2005 when the number of people aged over 60 reached 10% of the population. This number is expected to reach 20% by 2027, by which time the country will be an "aged" society. People aged over 65 will reach 20% in 2031, which is classified as a "super aged" society. As the government of China relaxes the one child policy, the government of Singapore provides financial incentives to have children and academics encourage the Thai government focuses on improving workforce skills and expertise to meet emerging demographic challenges.

, a direct measure referring to births per woman, is now the lowest in Thai history, according to Pramote Prasartkul, of Mahidol University s Institution for Population and Social Research (IPSR). The TFR dropped from more than six births per woman before 1970 to 1.6 at present. In the Southeast Asian region, only Singapore has a lower TFR rate than Thailand at 1.2. Vietnam is at 1.8, Malaysia is at 2.6, and Cambodia, Laos and Myanmar are more than three. Due to the low TFR, the IPSR estimates people in the workforce aged between 15 and 59 years will decrease from 67% of the Thai population in 2010 to 55.1% in 2040 The 11th National Economic and Social Development Plan ( ), approved by the cabinet last year, expresses concern about the change in demographic structure. The plan focuses on improving the workforce s skills and expertise to meet emerging challenges as well as technology development. Besides the low birth rate, longer life expectancy is also a factor in Thailand s rapidly ageing society. Thailand was classified as an ageing society in 2005 when the number of people aged over 60 reached 10% of the population. This number is expected to reach 20% by 2027, by which time the country will be an aged society. People aged over 65 will reach 20% in 2031, which is classified as a super aged society. As the government of China relaxes the one child policy, the government of Singapore provides financial incentives to have children and academics encourage the Thai government focuses on improving workforce skills and expertise to meet emerging demographic challenges..")

17

Implications of the Demographic Shift Smaller households require different housing Families with fewer children spend more/child With fewer people of working age – Cost of labor will rise – Low skill jobs will go to countries with younger populations – Need to move to higher value added (skills) More retirees and elderly – a unique market Japanese model – Higher value added industries – Investment abroad Pressures for immigration from labor surplus countries

More retirees and elderly – a unique market Japanese model – Higher value added industries – Investment abroad Pressures for immigration from labor surplus countries")

18

Hurdles to GMS development Nation June 14 th, 2013 Participants at a seminar in Bangkok June 13 th, 2013 raised concerns over labor shortages and how to share resources in the growing economy of the GMS. The labor market in the GMS was one of the topics at "GMS and the ASEAN Economic Community: Convergence, Opportunity and Challenges", a seminar arranged by Euromoney Conferences Labor shortages might become a barrier to business competitiveness, said a senior executive vice president of Bangkok Bank The executive said GMS is the place for businesses that want low costs, citing Cambodia as an example The shortage of labor, however, is a more serious issue for Thailand than other countries in the GMS because it is no longer considered a low-wage market, so many labor-intensive businesses have shifted to Cambodia Thai businesses should seriously think about mechanizing their production because they cannot rely on workers from neighboring countries, he said "Laos is not a source of labor because of the low population, while workers in Cambodia often strike. Therefore, Myanmar is the choice for Thai business, but Myanmar is developing, and once it has become a developed country, Thailand might be unable to rely on workers from Myanmar." He said the bank had attempted to encourage small and medium-sized enterprises to use more machines in the production process, and this encourages loan growth The deputy governor of the National Bank of Cambodia, noted that the free movement of labor might be a barrier for businesses' competitiveness Companies in Cambodia might not be able to secure workers The slow growth of the younger population in some countries in the GMS is a challenge to the growth of the sub-region

19

http://link.springer.com/article/10.1007%2FBF03031794?LI=true#page-4

20

Comparative Statistics GMS-China Urban %Rate urbanization FertilityLiteracyMedian age Labor forceGDP/cap PPP Thailand34%1.6%1.6693%35.139MM$10,300 Myanmar33%2.5%2.2193%27.633MM$1,400 Vietnam31%3.0%1.8793%28.749MM$3,600 Cambodia20%2.1%2.7274%23.78MM$2,400 Laos34%4.4%3.0073%21.64MM$3,100 China51%2.91.5595%36.3799MM$9,300 https://www.cia.gov/library/publications/the-world-factbook/geos/

21

Late 1990s global carmakers made decision to form regional production networks in SE Asia (Thailand a net exporter) ◦ Thailand came to serve as regional hub for car production and parts manufacture, both for local markets and exports ◦ CLM countries have instability, small markets, lack of skilled labor, or underdeveloped support industries ◦ Vietnam produces motorcycles and parts (sufficiently large market for motorcycles) while auto parts needed for JIT are made in Thailand Thailand may shift labor intensive operations to Vietnam ◦ In 2007 a large Thai vehicle parts manufacturer established operations in VN to supply motorcycle parts to local makers Engineering is done in Thailand Assembly is done in VN ◦ A Japanese parts maker established operations in Thailand in 1960s. The company now makes parts in VN for export to Japan These are labor intensive operations, where VN has an advantage using materials from Japan and Thailand Cambodia may be a next step because of location and labor costs With elimination of tariffs within ASEAN in 2018, VN may become specialized in labor intensive and mature technology Techakanont, Kriengkrai ‘New Division of Labor between Thailand and CLMV Countries’ 2012

22

Thailand’s Thai Beverage in a joint venture with UMEHL (Union of Myanmar Economic Holdings Limited) ◦ Myanmar Brewery Ltd – largest taxpayer in Myanmar ◦ Dispute with JV partner over control ◦ Heavy international attention to the arbitration PTT – largest market cap on SET ◦ Invests $3BB in power and resources projects- views Myanmar as growth center (July 2012) In addition to a refinery near Rangoon, PTT has been looking at investing in petrochemical and refining possibilities at Dawei on Burma’s southeast coast as part of a proposed special economic zone PTT considers developing a chain of roadside vehicle fuel stations across the country ◦ Now rumored to consider $30BB refinery project in VN Vietnam suffers from similar problems to Burma: plenty of crude oil and natural gas resources but inadequate oil refining and petrochemical production. Vietnam has only one refinery and must import two-thirds of its domestic fuel oils such as diesel. PTT plans to sell at least 50 percent of products from this Vietnam refinery into the regional market, which needs diesel, gasoline and other fuels as the Association of Southeast Asian Nations moves toward a single market. PTT might be eyeing Vietnam for such a major investment project as the mega refinery because of the export-potential “Some of the fuel would be shipped back to Thailand, where the environmentalist lobby is hampering further expansion of refining and petrochemicals.”* Although Burma is opening up economically, lack of infrastructure such as roads and ports and poor electricity supplies pose a serious problem for export-driven investments. *http://www.irrawaddy.org/business/thai-oil-firm-ptt-sees-vietnam-as-better-investment-bet-than-burma.html http://www.ft.com/cms/s/0/14074a42-d013-11e1-bcaa-00144feabdc0.html#axzz2kU1LkQqa

Similar presentations

The 8th Asia Economic Forum on “ASEAN in the Evolving Regional Architecture: Opportunities,>")

, all in Support of GMS Program on TTF Kazi Matin & Baher El-Hifnawi Workshop on World Bank’s Regional.>")