Download presentation

Presentation is loading. Please wait.

1

The Economic Outlook Mark Schniepp Director February 24, 2012 The Nation, State and the Antelope Valley

2

Economic Outlook Mark Schniepp, Director February 24, 2012 Not Quite through the tunnel yet When is the recession over ?

3

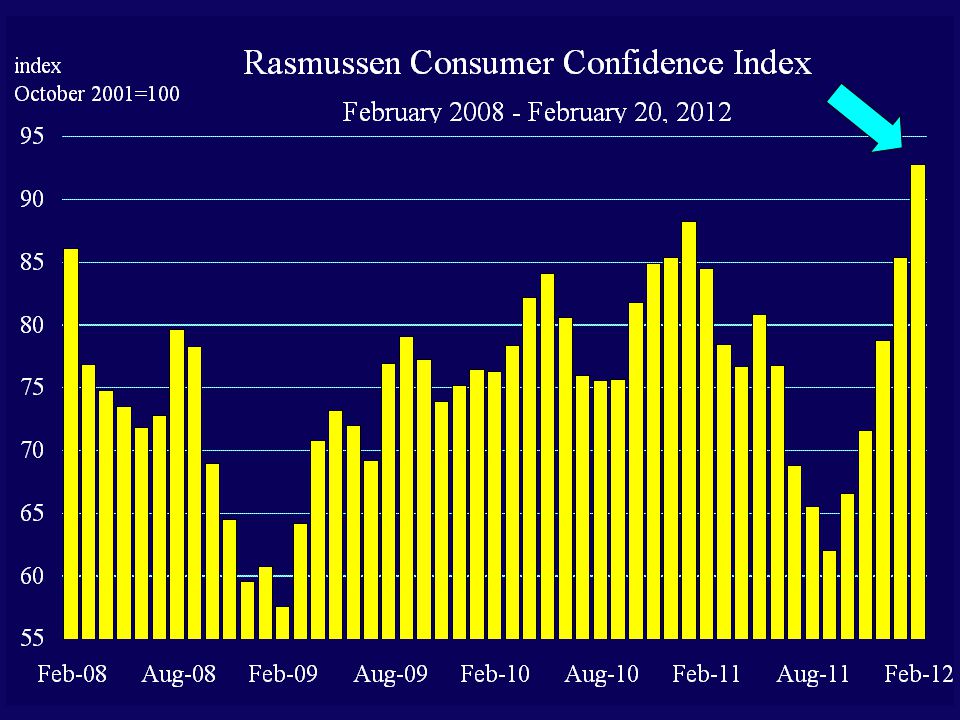

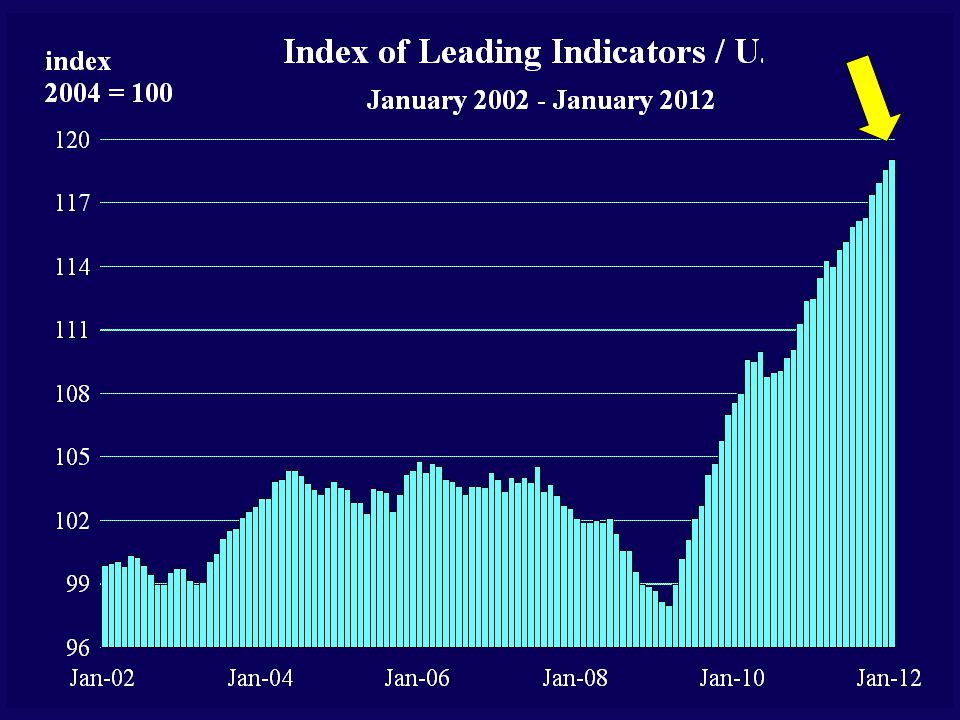

Recent Economic Evidence Significant improvement - last 10 weeks - most indicators now rising steadily

12

Los Angeles Times, February 8, 2012, Page B2

14

Recent Economic Evidence Significant improvement - last 3 months - most indicators now rising steadily Despite modestly growing GDP, the labor market unimpressed in 2011 Though the nation created 1.6 million jobs, unemployment remains high 25 million Americans seek full time work How is the momentum going into 2012 ?

15

Los Angeles times, January 7, 2012, front page 8.3%

17

23 months = 3.5 million jobs 8.8 million jobs

18

U.S. Economic Summary Consumers are feeling better and spending more Factories are producing more goods Autos are selling again; U.S. automakers reported their three best months of sales (post recession) in November, December, January The stock market has rallied sharply Business is hiring more / the u-rate is....

in November, December, January The stock market has rallied sharply Business is hiring more / the u-rate is.....")

19

2.7 %

20

What about California ?

21

327,000 jobs

22

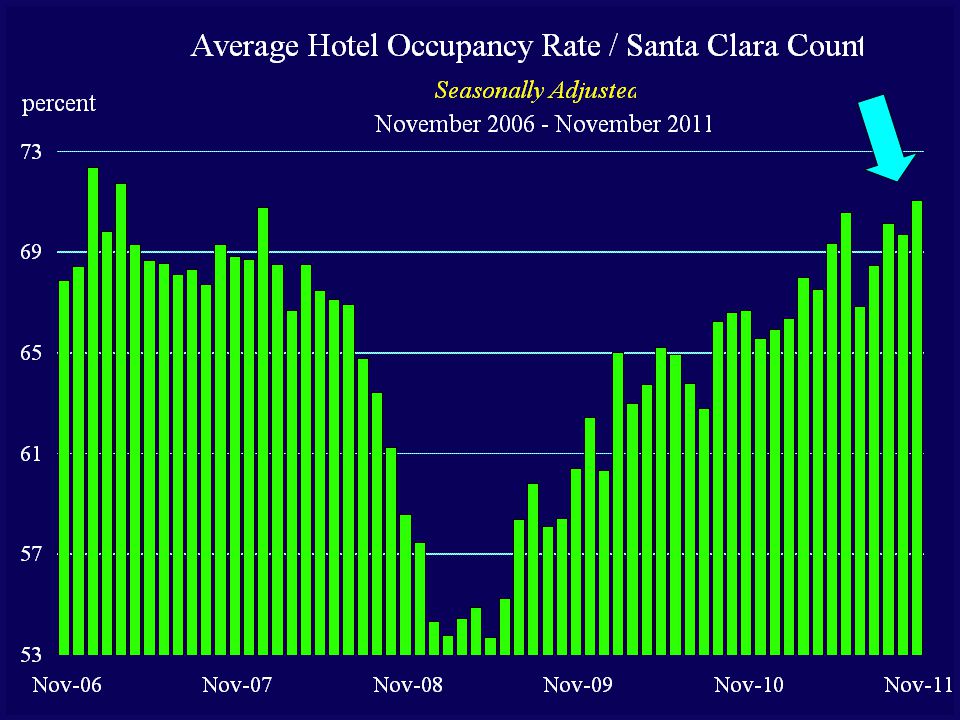

Recent Evidence / California Technology sector leading the charge Exports were explosive in 2011 Tourism also rising in all major markets Manufacturing growing again, but slowly Hiring is picking up, mostly in coastal markets but recently, inland areas are creating jobs Demographics are largely responsible for the abnormally high unemployment rates... and will also be responsible for the inevitable breakout of the housing market

31

Los Angels Times, December 17, 2011, B1Los Angels Times, January 21, 2012, front page

36

Question? If the state is still growing, and housing inventories are low, then why is there no new construction? Household formation has dried up - unemployed move in with Mom/Dad - or they never moved out ! This is an employment induced temporary problem … with growing likelihood that a dramatic breakout in housing demand could occur

37

Summary / California Technology, Exports, and Tourism are the current engines of growth Construction and Manufacturing show little recovery to date Public sector employment in decline Hotel occupancy now at pre-recession levels Commercial real estate slowly rebounding Inland counties have lagged the recovery in California but have recently joined with sharp increases in employment since the summer

39

Antelope Valley

40

Growth In California

41

Fastest Growing Counties / California 2008 - 2011 CountyPopulation Growth Placer Riverside Imperial Antelope Valley Tulare Kern Fresno San Joaquin Contra Costa Merced 5.3 4.9 4.7 4.5 4.1 3.5 3.1 2.7

43

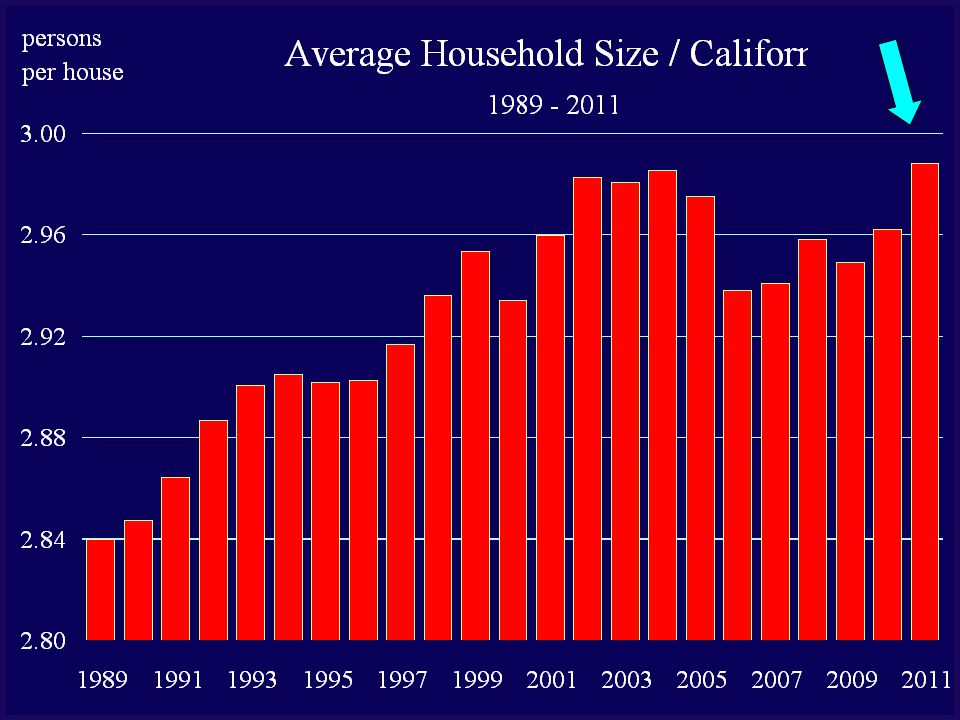

(a) 34.3 million (b) 37.3 million (c) 40.5 million (d) Just tell us the answer and get on with it.... ! Quiz part I: What is the Population of California? (census estimate)

.")

44

Quiz part II: What will be the Population of California in 2020 ? (a) 38 million (b) 40 million (c) 42.8 million (d) Who cares?

38 million (b) 40 million (c) 42.8 million (d) Who cares. .")

45

Where are these 5.4 million people going to live? (a) Orange County (b) Santa Clara County (c) Coachella Valley (d) Victor Valley (e) Antelope Valley (f) San Joaquin Valley (g) Sacramento Valley Quiz part III:

Orange County (b) Santa Clara County (c) Coachella Valley (d) Victor Valley (e) Antelope Valley (f) San Joaquin Valley (g) Sacramento Valley Quiz part III: .")

47

150,000 - 250,000 people per year

49

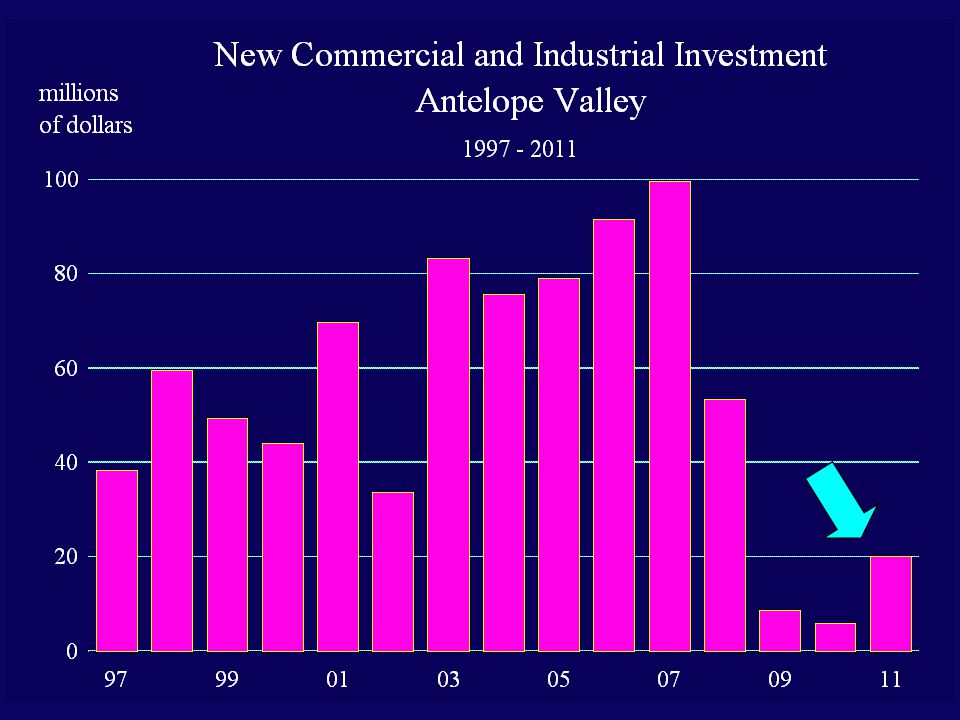

Recent job loss was deep and broad based Construction, manufacturing, and the retail sector experienced the greatest loss of jobs Unemployment leaped to an estimated 16 % Commercial markets weakened in tandem with the labor markets The retail fallout has been sharp Home production... well, negligible There is good news on the homeowner distress front... but conventional sales remain slow 2011 Economic Smmary Antelope Valley

50

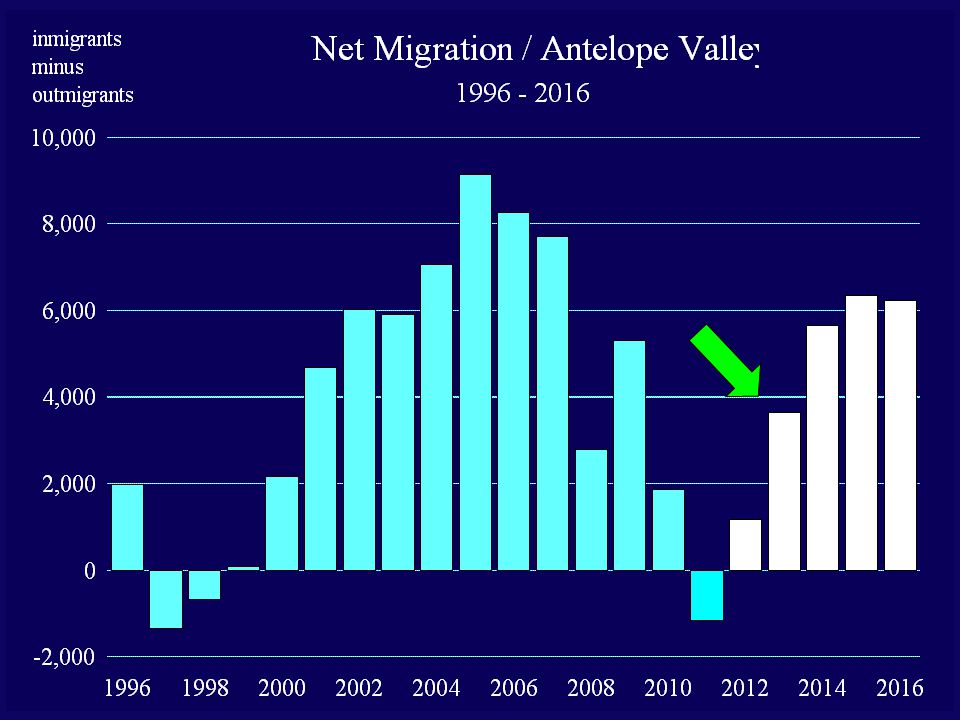

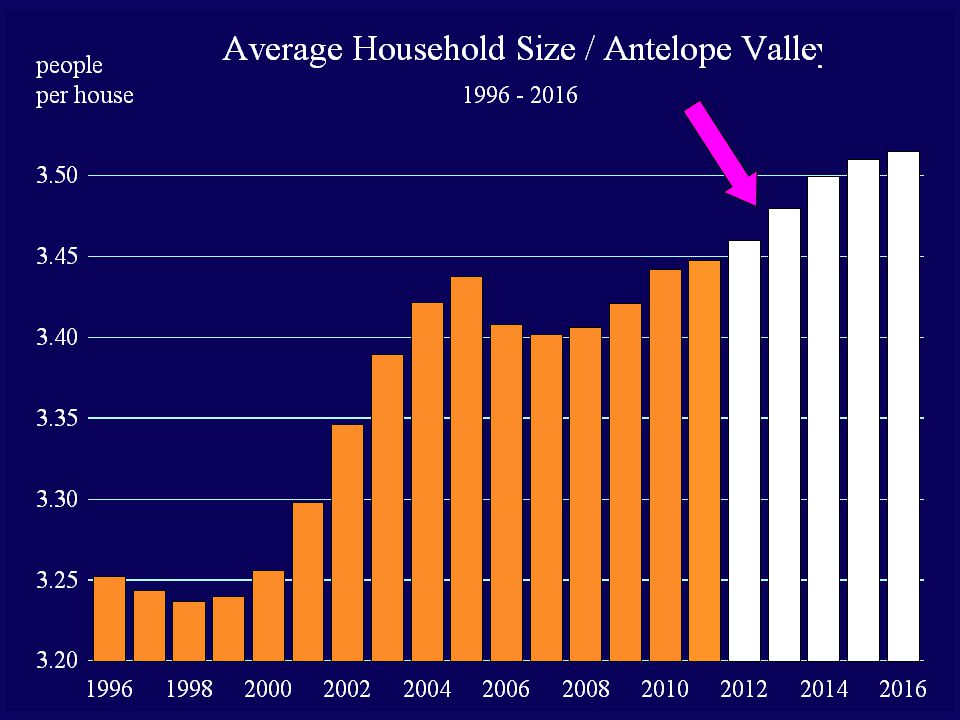

Recent Evidence / Antelope Valley The regional economy is slowly recovering – like other inland areas of California Population growth remains positive Job creation has been intermittent Residential entitlements are prolific Home prices have finally stabilized Affordability is extremely high relative to surrounding communities Retail spending is rising again

52

Labor Markets

53

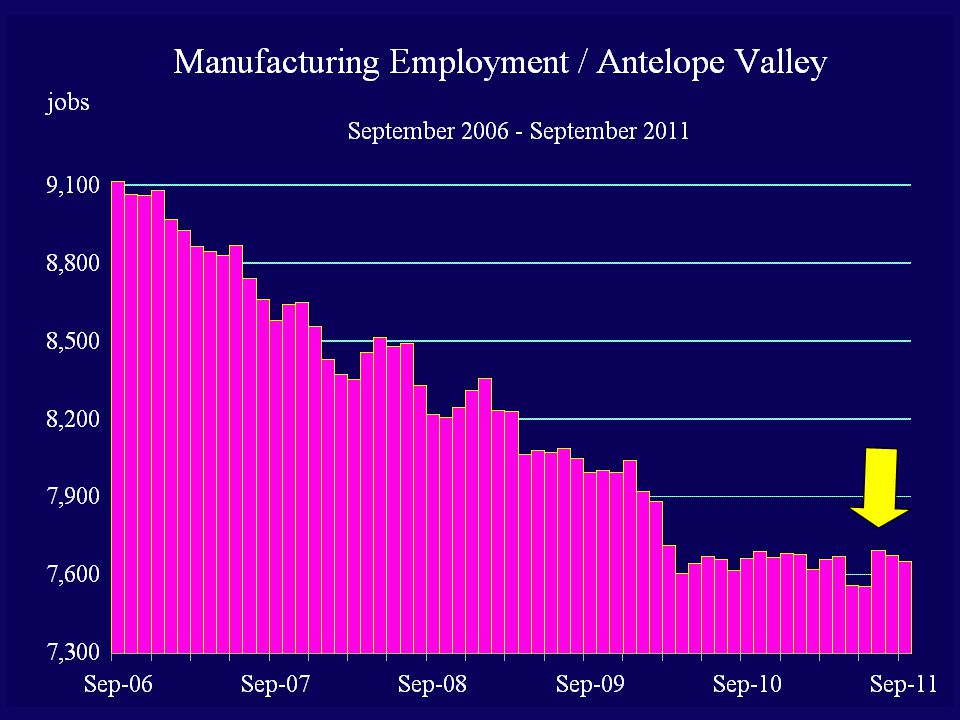

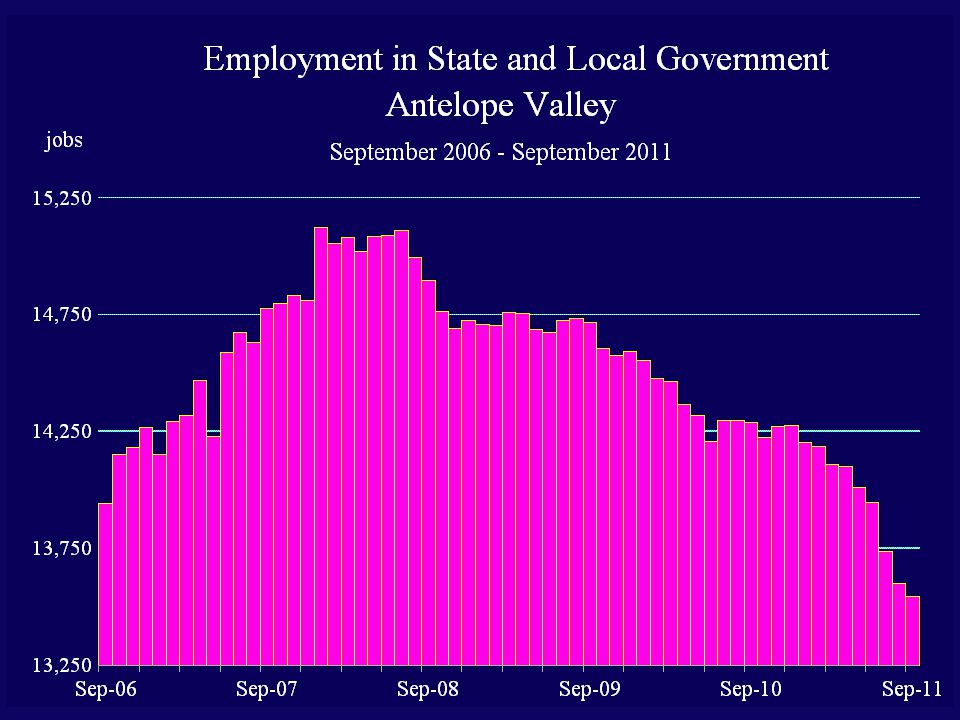

10 of 24 months = net loss of 100 jobs

64

Residential Real Estate The most frustrating sector of the economy

67

Median Home Selling Prices California Counties December 2011 San Diego Orange Los Angeles Inland Empire Ventura Antelope Valley San Fernando Valley California CountyPrice $359,930 $484,630 $306,950 $172,430 $391,060 $151,700 $322,000 $285,920 % Change From Peak -42.2 -37.5 -51.0 -55.7 -45.0 -61.4 -45.6 -51.9 -4.2 -3.7 -7.3 -3.3 -11.4 -5.8 -10.1 -6.2 % change

70

Los Angeles Times, February 18, 2011, page B2

71

Los Angeles Times, April 20, 2011, page B1

75

Los Angeles Times, January 12, 2012, page B3

76

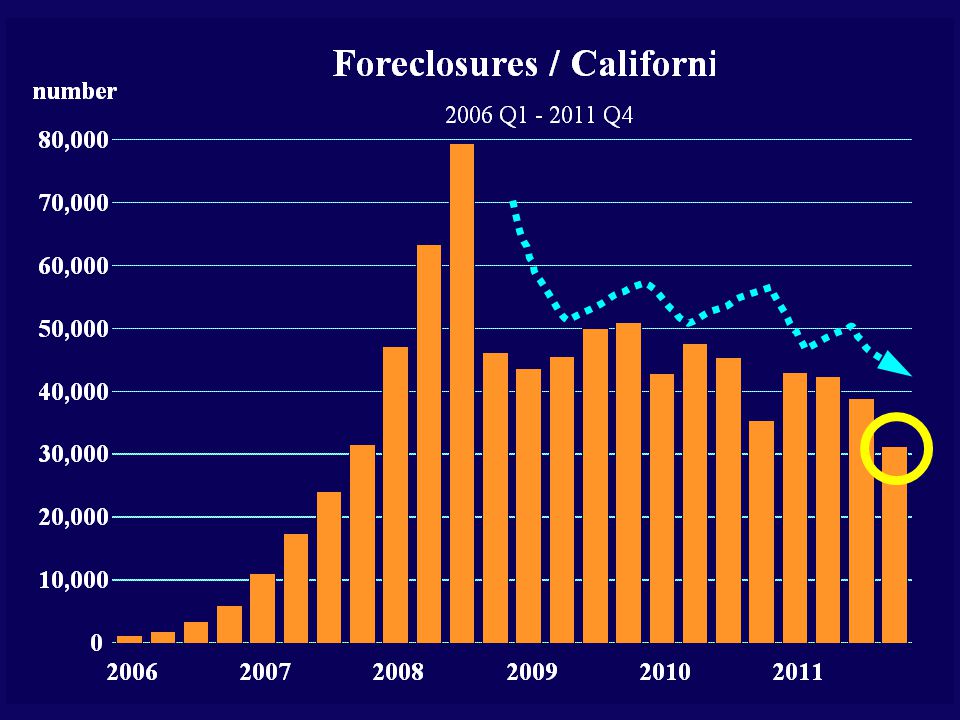

Housing Summary / California Values have stabilized ? Purchase market held back by credit conditions and labor markets Lack of demand along with distressed inventory keeps housing values from rising Credit conditions are tight because values have yet to rebound Catch 22: prices won’t rise until credit markets loosen; credit markets won’t loosen until values start rising again Distressed inventory will begin to subside in 2013

77

5 year Outlook The Forecast

78

2012 Antelope Valley Forecast Summary 2011 was a transition year: the economic recovery will be more convincing in 2012throughout Southern California Though labor markets are already adding jobs, the pace of expansion will accelerate and broaden Home sales finally improve in 2012 due to high affordability, and more new jobs Job creation, home sales, and consumer spending return to more normal levels in 2013 Homeowner distress is the wild card

79

- 6,700 jobs

83

40,000

85

10,50 0

90

Southern California Forecast Summary The recovery will lag in the inland areas, but over the long run growth will be stronger A much stronger expansion of labor markets will occur by 2013, reaching a peak in 2014 The unemployment rate will remain high for years to come as more new workers enter the labor force Population grows slightly faster, inland areas grow much faster than the coast Home prices rise in 2012 ? …… or beyond ? Prices rise when distressed properties account for a smaller share of total transactions Housing production ultimately increases throughout the forecast to meet the needs of a growing population

91

The Economic Timeline U.S. economic expansion underway now Regional expansion more evident by Q3 or Q4 Solid job creation sustainable: 2012 Q4 Unemployment rate falling throughout year Foreclosures subsiding by 2012 Q4 More new housing underway this year, with breakout in 2013 Fed raises rates: late 2014 / early 2015 Expansionary conditions sustainable: 2012 Q4

92

Antelope Valley 2012 Economic Outlook

Similar presentations

Robert Carrillo September2013.>")