Download presentation

Presentation is loading. Please wait.

1

WELCOME: BEEF ECONOMICS WEBINAR Audio Announcement: all lines are currently muted and we will begin promptly at 1:30pm CST Please select your audio now. To dial the conference, select “Use Telephone” in your audio pane and enter your unique audio pin. Select “Use Mic & Speakers” to use VoIP audio. Submit questions and comments via the Chat panel Note: Today’s presentation is being recorded and will be provided within 48 hours. Audio Announcement: all lines are currently muted and we will begin promptly at 1:30pm CST Please select your audio now. To dial the conference, select “Use Telephone” in your audio pane and enter your unique audio pin. Select “Use Mic & Speakers” to use VoIP audio. Submit questions and comments via the Chat panel Note: Today’s presentation is being recorded and will be provided within 48 hours.

2

May 14, 2013 Sponsored by: Presenter: Dr. Glynn Tonsor, Kansas State University

3

WEBINAR OVERVIEW Broad Economic Outlook Overview for Industry Note take-home points of “big picture” reports: – 2012 Cow-Calf Cost and Returns Estimates – 10-year breeding herd projections

4

Overarching Current Economic Outlook Supplies – “Certain” Cattle Supplies (hd) – Less Certain Beef Supplies (lbs) Demand – Uncertain and Confused Weather Persistence or Recovery? – Corn planting growing concern – Drought management varies regionally Additional Excess Capacity Resolution?

5

Economic Outlook Overview: Cow-Calf Expansion? Feeders Available per Feeder in Feedlot: 3.41 in 1973; 2.43 in 2012 Source: USDA NASS Jan. 1 data; Tonsor tabulations

6

Economic Outlook Overview: Cow-Calf Expansion? Source: USDA NASS Jan. 1 data; Tonsor tabulations

7

Economic Outlook Overview: Cow-Calf Expansion? Feeders Available per Feeder in Feedlot: 3.41 in 1973;2.43 in 2012 No July Cattle Inventory Report Pasture conditions worst in areas of attempted heifer retention

8

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC

9

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC CO, KS, MT, NE, ND, SD, & WY 29.6% of Cows 34.3% of Retained Heifers (Jan. 2013)

.")

10

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC AZ, CA, ID, NV, NM, OR, UT, & WA 10.4% of Cows 11.3% of Retained Heifers (Jan. 2013)

.")

11

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC OK & TX 19.7% of Cows 16.4% of Retained Heifers (Jan. 2013)

.")

12

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC IL, IN, IA, MI, MN, MO, OH, & WI 14.6% of Cows 14.5% of Retained Heifers (Jan. 2013)

.")

13

Livestock Marketing Information Center Data Source: USDA-NASS, Compiled & Analysis by LMIC AL, AR, FL, GA, KY, LA, MS, NC, SC, TN, VA, & WV 24.6% of Cows 21.3% of Retained Heifers (Jan. 2013)

.")

14

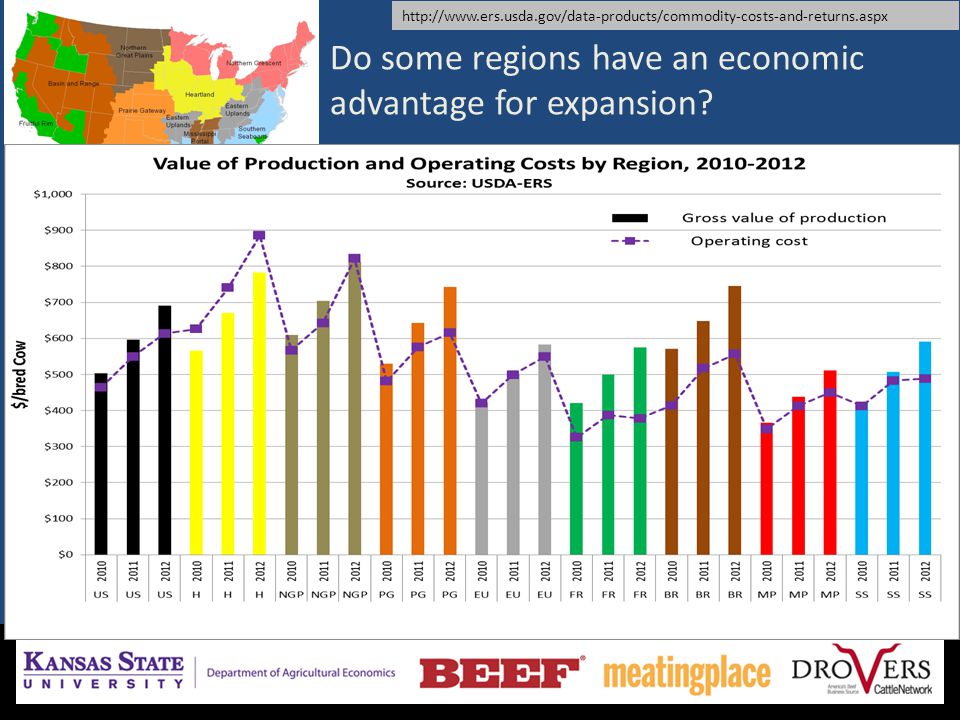

Do some regions have an economic advantage for expansion? http://www.ers.usda.gov/data-products/commodity-costs-and-returns.aspx

15

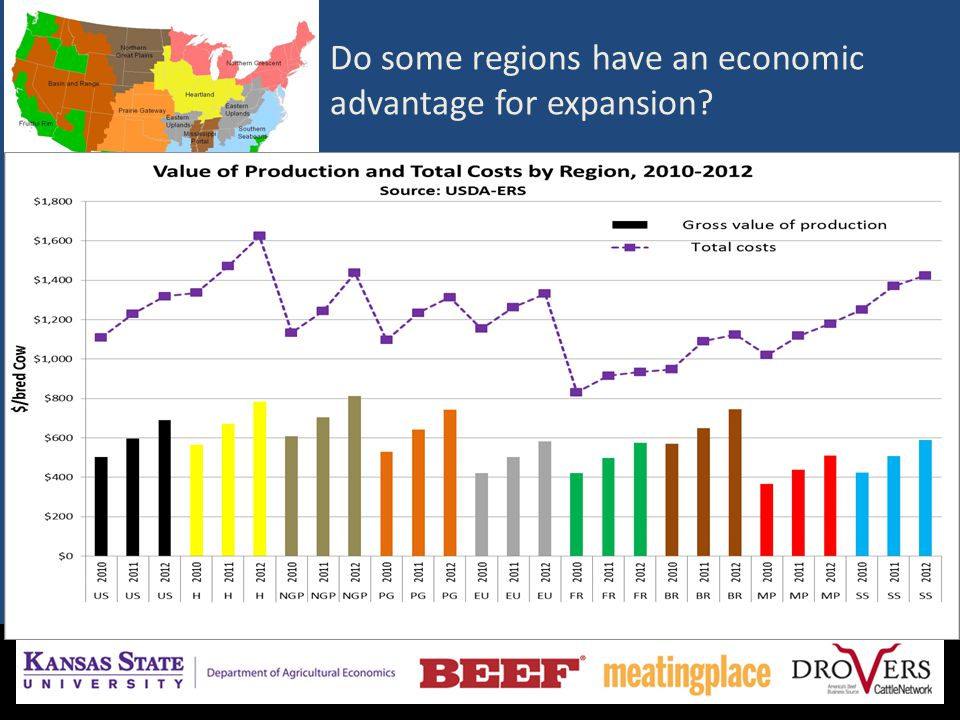

Do some regions have an economic advantage for expansion?

18

Allocated Costs: Opportunity costs of unpaid labor, capital recovery, etc.

19

Do some regions have an economic advantage for expansion? Operating Costs: Feed (purchased, homegrown, grazed), vet/medicine, utilities, etc.

, vet/medicine, utilities, etc..")

20

20 As of: 5/13/13’ http://www.agmanager.info/livestock/marketing/graphs/cattle/prices/default.asp May FC: 5/13: $136 4/12: $141 3/13: $144

21

Economic Outlook Overview : Stockers Historically high Values of Gain (VOG) – But also historically high Costs of Gain (COG)… Salina, KS 5/13/13 situation: – Buy 550 lb steer on 10/16/13 ($159) – Sell 750 lb steer on 1/15/14 ($148) {2.2 ADG} VOG: $117/cwt – http://www.beefbasis.com/ForecastingTools/ValueofGain/tabid/113 2/Default.aspx

– But also historically high Costs of Gain (COG)… Salina, KS 5/13/13 situation: – Buy 550 lb steer on 10/16/13 ($159) – Sell 750 lb steer on 1/15/14 ($148) {2.2 ADG} VOG: $117/cwt – 2/Default.aspx")

22

22 http://www.agmanager.info/livestock/marketing/graphs/cattle/prices/VOG.asp

23

Economic Outlook Overview : Feedlots Excess capacity concerns remain & are growing… Closeouts have been at historically high losses… – 12 month rolling avg. thru March 13’ -$173 Watch response to shrinking available supplies… – Is “feeding country moving north” ???

24

Historical and Projected Kansas Feedlot Net Returns (as of 5/9/13’) ( http://www.agmanager.info/livestock/marketing/outlook/newsletters/FinishingReturns/default.asp ) Representative Barometer for Trends in Profitability March 13’: -$182/steer June LC: 5/13: $121 4/12: $121 3/12: $124 1/14: $130

( ) Representative Barometer for Trends in Profitability March 13’: -$182/steer June LC: 5/13: $121 4/12: $121 3/12: $124 1/14: $130")

25

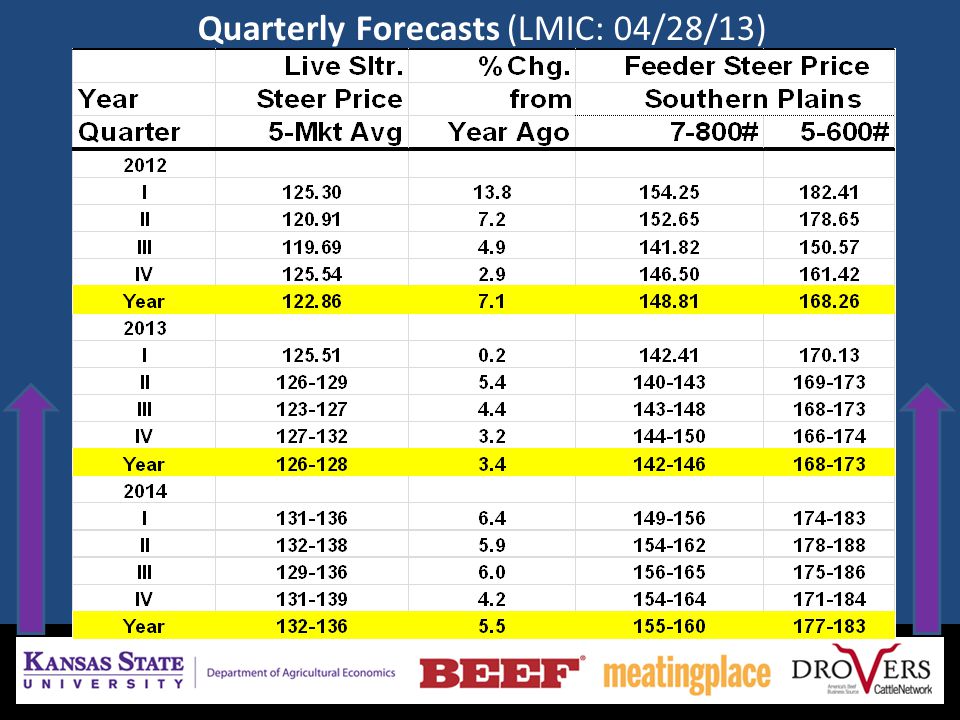

Quarterly Forecasts (LMIC: 04/28/13)

")

27

Economic Outlook Overview : Beef Demand Demand less certain than supply currently heightened need to monitor… Meat prices rising w/i basket of purchases… – as prices increase, public will require more quality… quality and value are in the eye of the beholder... debates on various technologies likely will intensify within industries, with customers, and with consumers… – “Vote vs. buy” behavior differences important

28

28 Yr-over-Yr increases in 10 of last 11 quarters (since Q3 of ’10); Q1.2013 = +1.57% Actual Quantity & Price Changes: 1990: 67.8 lbs (per capita cons.);$2.00 (real All Fresh price) 2012: 57.3 lbs (per capita cons.);$2.04 (real All Fresh price) Q1.2013: Per Capita Consumption = -1.71% (Year-over-Year) Real All Fresh Beef Prices = +3.78% ($4.91/lb nominal price) IF Real All Fresh Beef Prices +2.18% = 0% Demand Change http://www.agmanager.info/livestock/market ing/Beef%20Demand/default.asp

; Q = +1.57% Actual Quantity & Price Changes: 1990: 67.8 lbs (per capita cons.);$2.00 (real All Fresh price) 2012: 57.3 lbs (per capita cons.);$2.04 (real All Fresh price) Q1.2013: Per Capita Consumption = -1.71% (Year-over-Year) Real All Fresh Beef Prices = +3.78% ($4.91/lb nominal price) IF Real All Fresh Beef Prices +2.18% = 0% Demand Change ing/Beef%20Demand/default.asp")

29

Livestock Marketing Information Center Data Source: Bureau of Economic Analysis & USDA-ERS, Compiled & Analysis by LMIC 2013, 54.8 lbs/capita, 0% Demand Change Case = $4.89/lb (+4.28% vs. 12’)

.")

30

Longer-term projections (as of Feb. 2013) http://www.usda.gov/oce/commodity/projections/index.htm IF 2013 per capita consumption falls from 56.8 lbs to 54.8 lbs (-3.52%) AND IF 2013 All Fresh Beef price increases by +4.28% ($4.89/lb) = 0% Demand Change… 2021 Projection 1.1 million less than Feb. 12’… 2022 herd +12% (vs. 2012)

IF 2013 per capita consumption falls from 56.8 lbs to 54.8 lbs (-3.52%) AND IF 2013 All Fresh Beef price increases by +4.28% ($4.89/lb) = 0% Demand Change… 2021 Projection 1.1 million less than Feb. 12’… 2022 herd +12% (vs. 2012).")

31

U.S. beef cow inventory: 29.9 million in 2012 (was 37.9 million in 1983) 29.8 million in 2013 29.5 million in 2014; net expansion starts in 2015 (29.6) 33.5 million in 2022 34.5 million in 1997; Beef Production (billion lbs): 25.4 (1997), 25.7 (2012) More beef/cow will continue = less # head throughput … If/when herd expands, likely NOT going back to 1980s levels … Longer-term projections (as of Feb. 2013) http://www.usda.gov/oce/commodity/projections/index.htm

29.8 million in million in 2014; net expansion starts in 2015 (29.6) 33.5 million in million in 1997; Beef Production (billion lbs): 25.4 (1997), 25.7 (2012) More beef/cow will continue = less # head throughput … If/when herd expands, likely NOT going back to 1980s levels … Longer-term projections (as of Feb. 2013)")

32

“Developing World” Changes (2012-2022) Increasing global $, pop., & per capita meat cons. Africa & Middle East (3.8 - 4.9% GDP/yr) Region accounts for >40% of meat import growth. Yet arguably the least understood growth market… Latin America (4.0% GDP/yr) Growing producer & consumer… China (7.8% GDP/yr) Canada has access but US does not … South Korea (3.5% GDP/yr – but 10x per capita inc. of China) US has access but Canada does not… Longer-term projections (as of Feb. 2013) http://www.usda.gov/oce/commodity/projections/index.htm

Region accounts for >40% of meat import growth. Yet arguably the least understood growth market… Latin America (4.0% GDP/yr) Growing producer & consumer… China (7.8% GDP/yr) Canada has access but US does not … South Korea (3.5% GDP/yr – but 10x per capita inc. of China) US has access but Canada does not… Longer-term projections (as of Feb. 2013)")

33

“Developed World” Changes (2012-2022) Declining global economic prevalence, populations, & per capita meat consumption US/Canada (2.4 – 2.6% GDP/yr) Different dependence on domestic consumption… Japan (1.1% GDP/yr): Major meat importer currently (changes in age restriction a +) but will exporters care less going forward? Europe (1.7% GDP/yr): Will influential role as “food thought leader” persist? Longer-term projections (as of Feb. 2013) http://www.usda.gov/oce/commodity/projections/index.htm

: Will influential role as food thought leader persist. Longer-term projections (as of Feb. 2013)")

36

Sponsored by: Mark your calendars for remaining 2013 webinars (all begin at 1:30 pm CST): August 13 November 5

: August 13 November 5")

37

What will U.S. beef cow herd size be in 10 years?

38

How much “excess capacity” currently exist in U.S. feedlot industry? 1. None 2. 1-10% 3. 11-20% 4. 21-30% 5. Over 30%

39

Questions typed by participants during the webinar presentation which were not directly responded to are addressed in the remaining subsequent slides.

40

Sponsored by:

Similar presentations

Future of U.S. Cattle Industry>")