Download presentation

Presentation is loading. Please wait.

1

A GENT B ASED M ODEL OF T AX E VASION B EHAVIOR Abhishek Malik (Y6020) Guide: Prof Amitabha Mukerjee

Guide: Prof Amitabha Mukerjee")

2

AIM To develop a realistic model using the agents, to get some idea of human tax evasion behavior in the given specified conditions. APPLICATION: After sufficient development Suitable for Tax Agencies to determine the effects of their decisions. Help understand the complex human behavior.

3

I NTRODUCTION Developed a multi-agent model showing tax paying behavior of agents under certain parameters. Coding done in NetLogo simulation language. An agent posses 20 different traits. Two class of taxpayers. Model determines Social Effect on behavior. Varying tax rates and income levels. Varying honesty and lifespan.

4

I NCOME D ISTRIBUTION We assign income of agents as addition of an exponential distribution with mean 4 lakhs and a normal distribution with mean 3.5 lakhs and variance 1.5 lakhs. I=E(4lakh) + N(3.5lakh, 1.5 lakh). For Business agents the income varies every cycle.

+ N(3.5lakh, 1.5 lakh). For Business agents the income varies every cycle..")

5

I NCOME V ISIBILITY There are two types of agents: Service type agents They have all their income as visible. Income remains constant for the cycles. Business type agents They have fixed amount of income as visible (this percentage is set by the user). Income fluctuates with small variations in each cycle.

. Income fluctuates with small variations in each cycle..")

6

T AXPAYER E VASION D ECISION Bloomquist used: I have modified it a little to include the effect of varying tax rates:

7

E VASION O F S ERVICE T YPE A GENT For more than 70 percent of the agents in the neighborhood are evading then the agent would decide to evade irrespective of other things. Except when Audited recently or If under social effect.

8

T AX G IVEN If the agent has decided not to evade: Both type of agents give the fair amount of tax. On total income sum = visible + non-visible. But if the agent has decide to evade then: Service type agent gives tax on income based on honesty (but they will still give about 80 percent tax). The business type agents Give complete tax on the visible income Only fixed percentage of tax on non-visible income, which depends on their randomly assigned honesty ( which is low).

. The business type agents Give complete tax on the visible income Only fixed percentage of tax on non-visible income, which depends on their randomly assigned honesty ( which is low)..")

9

P ERCEIVED A UDIT R ATE It is independent for each agent. Assigned randomly from Normal distribution with mean as actual audit rate and variance as 0.03 It is also increased under the social effect as later explained.

10

S OCIAL E FFECT A ND S OCIAL N ETWORKS The social effect can be turned on or off in the model. Social effect means the effect on one’s own behaviour due to knowledge of neighbours. Social Network In the previous works this was mostly static and fixed. In this model the agents keep moving within fixed area The neighbouring agents within fixed range form the social network of the agent. Thus network is not fixed and keeps changing in every run.

11

S OCIAL E FFECT If the agent finds out that number of agents audited in the social network is larger than some fixed number: It will stop evading, if it was evading. Perceived audit rate will increase by random number from 0 to 20. The increased perceived audit rate will last for fixed time which is again different for each agent and determined randomly.

12

V ARYING L IFESPAN O F A GENTS In some of the previous models the lifespan of the agents were infinite. In the Bloomquist model the lifespan of the agent varied. In this model the lifespan of an agent is determined randomly from a normal distribution with mean 45 and variance 15. These figures are taken keeping in mind the active tax paying age of a person.

13

T HE M ODEL

14

A GENTS AND THEIR T RAITS

15

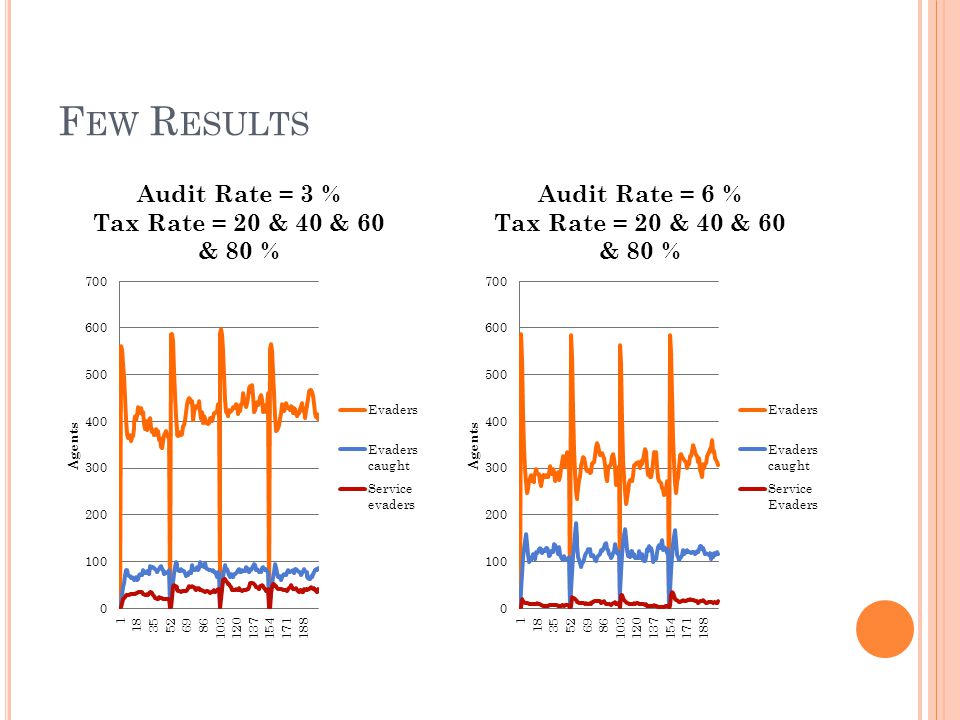

F EW R ESULTS

19

P REVIOUS R ESULT ON A UDIT R ATES AND V ISIBILITY

20

C URRENT R ESULTS (A LL B USINESS A GENTS )

")

21

A UDIT R ATES AND V ISIBILITY ( 70% S ERVICE A GENTS )

")

22

E ARLIER R ESULT FOR V ARIATION W ITH A UDIT R ATES A ND S OCIAL N ETWORK S IZE

23

C URRENT R ESULTS FOR V ARIATION WITH A UDIT R ATES A ND S OCIAL N ETWORK S IZE

24

S OCIAL E FFECT V ARIANCE

25

S IMILARITY W ITH O THER R ESULTS Theses non-compliance rates have somewhat similarity to those obtained by Bloomquist, but more realistic. The result when social effect is on and the audit rates are close to 0.04 - 0.05, the results are similar to those obtained by IRS. The noncompliance rate is from 15 percent to 16.6 percent of the true tax liability, according to the IRS.

26

C ONCLUSION The results with sufficient audit rates and 70% service agent population have some similarity to real situations. The agents of the model developed, have high level of dishonesty. Effect of tax rates on the evasion decision is not very well implemented as yet and more work could be done on it. The level of unpredictability is high. I wanted to introduce some irrationality into the system, but I think it is a bit overdone.

27

R EFERENCES Bloomquist, Kim M. “A Comparison of Agent-Based Models of Income Tax Evasion.” Social Science Computer Review 24 No. 4 Winter, 2006): 411-25. Bloomquist, Kim M. “Multi-Agent Based Simulation of the Deterrent Effects of Taxpayer Audits.” Paper presented at the 97th Annual Conference of the National Tax Association, Minneapolis, MN, November, 2004. Davis, Jon S., Gary Hecht, and Jon D. Perkins. “Social Behaviors, Enforcement and Tax Compliance Dynamics.” Accounting Review 78 No. 1 January, 2003): 39-69. Mittone, L., & Patelli, P. (2000). “Imitative behaviour in tax evasion.” In B. Stefansson & F. Luna (Eds.), Economic simulations in swarm: Agent-based modelling and object oriented programming (pp. 133-158) Amsterdam: Kluwer. Internal Revenue Service (IRS), United States Department of the Treasury.(FS(Fact Sheets)-2005-14, March 2005). (http://www.irs.gov/newsroom/article/0,,id=137246,00.html)

: Bloomquist, Kim M. Multi-Agent Based Simulation of the Deterrent Effects of Taxpayer Audits. Paper presented at the 97th Annual Conference of the National Tax Association, Minneapolis, MN, November, Davis, Jon S., Gary Hecht, and Jon D. Perkins. Social Behaviors, Enforcement and Tax Compliance Dynamics. Accounting Review 78 No. 1 January, 2003): Mittone, L., & Patelli, P. (2000). Imitative behaviour in tax evasion. In B. Stefansson & F. Luna (Eds.), Economic simulations in swarm: Agent-based modelling and object oriented programming (pp ) Amsterdam: Kluwer. Internal Revenue Service (IRS), United States Department of the Treasury.(FS(Fact Sheets) , March 2005). (")

Similar presentations