Download presentation

Presentation is loading. Please wait.

1

1 Succession The Roles of Specialized Assets and Transfer Costs Corporate Governance and Product Market Competition Yin-Hua Yeh (NCTU, Taiwan)

")

2

2 Succession: The Roles of Specialized Assets and Transfer Costs Joseph P.H. Fan (CUHK) Ming Jian (NTU, Singapore) Yin-Hua Yeh (NCTU, Taiwan) Rewrite and submit to the special issue of JCF (by including Morten Bennedsen as an additional co-author)

Ming Jian (NTU, Singapore) Yin-Hua Yeh (NCTU, Taiwan) Rewrite and submit to the special issue of JCF (by including Morten Bennedsen as an additional co-author).")

3

3 Succession as An Urgent Issue Many Asian entrepreneurial firms have experienced succession In our research, we identified numerous succession cases in the past decades There are more to come soon

4

4

5

5 Research Questions Family ownership of business is popular around the world. How successful are family firms? Recent economics research in developed economies report a mixed picture (Smith and Amoako-Adu, 1999; Morck, Strangeland, and Yeung, 2000; Anderson and Reeb, 2003; Perez-Gonzales, 2006; Villalonga and Amit, 2006) If heir succession is bad, why do some firms insist? A second-best solution in weak institutional environments Interest alignment with the family (Bhattacharya and Ravikumar, 2002) The threat of expropriation (Burkart, Panuzi, and Shleifer, 2003)

If heir succession is bad, why do some firms insist. A second-best solution in weak institutional environments Interest alignment with the family (Bhattacharya and Ravikumar, 2002) The threat of expropriation (Burkart, Panuzi, and Shleifer, 2003).")

6

6 Research Questions Family ownership and family succession To protect specialized assets that are difficult to partition, value, and transfer across organizational boundaries (Alchian, 1965; 1969). Research Questions How successful are successions? What determine the success (or failure) of succession ? What determine the choice between an heir and an unrelated successor?

of succession ? What determine the choice between an heir and an unrelated successor .")

7

7 The Specialized Assets The property right approach Asset specificity governance structures of business activities Asset specificity and transfer costs in entrepreneurial activities Surviving firms probably possess competitive advantages. Entrepreneurial activities often consume a large amount of entrepreneurs’ personal time, effort, and financial capital, dictating an ideology to take on these activities and associated risks. Entrepreneurial activities often involve strong team spirit.

8

The Specialized Assets The specialized assets are difficulties to partition and transfer across individuals and/or firm boundaries. A founder’s ideology, reputation in business, and political connections are specific to the founder, Intangible assets such as relationships with employees and banks, or Assets jointly controlled by family members and/or co-founders.

9

9 Hypothesis development Family or outside succession Because of the transfer difficulties of the specialized assets, we expect to observe persistent concentrated ownership and control of the assets. We expect that an heir or a close relative would be chosen as the successor if the extent of asset specificity is large. Conversely, an important condition for outside succession is that the firm’s assets are standardized and easy to transfer across generations.

10

10 Hypothesis development Firm value We expect an overall decline in firm capitalized value within the process of succession. Across different firms, the extent of value dissipation depends on the degree of asset specificity within their different activities. We expect that the asset specificity induces high transfer costs, and hence the likelihood of family succession, high family ownership concentration, and poor performance in the succession process.

11

11 Definition of Succession Succession as an event in which a controlling owner/manager steps down from the top executive (usually chairman in Asia) positions Our succession events provide a unique opportunity to test the theory, because, by the natural force of aging, the old leadership has to be terminated and ownership and control transferred to the new generation. Typically succession is a process that takes time to complete We track firms from 5 years before to 3 years after their chairman turnovers.

12

Sample Hong Kong, Singapore and Taiwan The prevalence of firms controlled by Chinese families. Keep track of turnovers of the top executive (typically chairman) for each of the firms starting from IPO year. We exclude firms that are controlled by non-Chinese or governments, are in financial distress around succession, and an entrepreneur steps down from chairmanship but remains a director on the board. If any two turnovers of the same firm occur within 5 years, we exclude the earlier turnover as it is likely a transitory arrangement.

for each of the firms starting from IPO year. We exclude firms that are controlled by non-Chinese or governments, are in financial distress around succession, and an entrepreneur steps down from chairmanship but remains a director on the board. If any two turnovers of the same firm occur within 5 years, we exclude the earlier turnover as it is likely a transitory arrangement..")

13

13 Table 1 Sample Distribution This table presents the sample by succession year and industry. Panel A By succession year YearHong KongSingaporeTaiwanTotal 1987 0022 1988 00 4 4 1989 00 6 6 1990 00 6 6 1991 0 05 5 1992 0 46 10 1993 0 54 9 1994 0 67 13 1995 0 46 10 19964511 20 1997726 15 1998338 14 19999412 25 200012413 29 20019112 22 2002830 11 2003640 10 200421 03 200521 03 Total6247108217

14

14 Panel B By industry IndustryHong KongSingaporeTaiwanTotal Agriculture, Forestry and Fishing 0101 Construction and Real Estate206834 Food and Kindred Products1157 Textile and Apparel311317 Lumber, Furniture, Paper and Printing 1247 Chemicals, Petroleum, Rubber, Plastic and Leather 501520 Minerals and Metals121316 Machinery, Equipment and Instrument 1172644 Transportation and Communication 241016 Utility1012 Commerce85619 Financial Company47314 Service511420

15

15 Table 2 Successor Types The defined types include ‘ Family member ’, ‘ Outsiders ’ and ‘ Sold-out ’. ‘ Unknown ’ is for firms whose successor type is unclear. We further differentiate the succession type of ‘ Family members ’ into heir succession ‘ Heir ’ and ‘ Relative ’, of which successors are close relatives such as brothers or nephews. Hong KongSingaporeTaiwanTotal Family member 4369%1736%8074%14065% Heir 1829%49%5753%7936% Relative 2540%1328%2321%6128% Outsiders 610%1736%2422%4722% Sold-out 1321%817%44%2512% Unknown 00%511%00%52% Total62 100% 47 100% 108 100% 217 100%

16

16 Measuring asset specificity and transfer costs Measurement cost of subjective value (Ideology) Founder Amenity : any business in entertainment, media, or sport business (amenity potential, Demsetz and Lehn, 1985) Conflicts due to indivisibility of property rights Co-founded Family managed: number of family members on board To capture intangible assets that pose high transfer costs Bank relation : long-term financing relation Labor intensity: Employees’ trust and relationships with an entrepreneur is likely a specialized asset.

Founder Amenity : any business in entertainment, media, or sport business (amenity potential, Demsetz and Lehn, 1985) Conflicts due to indivisibility of property rights Co-founded Family managed: number of family members on board To capture intangible assets that pose high transfer costs Bank relation : long-term financing relation Labor intensity: Employees’ trust and relationships with an entrepreneur is likely a specialized asset.")

17

Measuring asset specificity and transfer costs to proxy for successor’s capability Experience: has been a senior manager of the firm prior to succession Education : has a bachelor or higher degree In all regressions, we include Size, to control for any effects of firm size. All the above variables are constructed using data from 5 years before the succession year, to prevent any effects of succession per se.

18

18 Table 3 Summary Statistics of Independent Variables VariableObs.MeanMedianStd. Dev. Founder2170.55301.000.4983 Amenity2170.0553-0.2291 Co-founded2170.0461-0.2101 Family managed2102.44762.00001.5027 Labor intensity2130.00890.00480.0239 Bank relation2160.09390.04910.1434 Experience2170.4378-0.4973 Education2170.56681.00000.4967 Size21711.822011.83151.4940 Ultimate ownership2020.33550.31060.2180

19

19 Successor Choice and Ownership Structure

20

Firm Value Change Compounded abnormal return (CAR) The monthly compounded return of a security within a defined period and the corresponding monthly compounded return of a market index. The difference between the security and the market index compounded return Cumulative abnormal returns (CAR) The monthly abnormal return for a security Add up AR i,t across all t to obtain CAR. CAR (-60, -1), CAR (-36, -1), and CAR (-60,36) Month 0 of a given event is defined as Jan. of the succession year

The monthly abnormal return for a security Add up AR i,t across all t to obtain CAR. CAR (-60, -1), CAR (-36, -1), and CAR (-60,36) Month 0 of a given event is defined as Jan. of the succession year.")

21

21

22

22 Table 5 Statistics of Abnormal Stock Returns around Succession VariableObs.MeanMedianStd. Dev. Full sample CAR (-60, 0)144-0.5558-0.54121.1225 CAR (-36, 0)161-0.1560-0.27280.8471 CAR (0, +48)179-0.0288-0.07540.8302 Hong Kong CAR (-60, 0)54-1.2567-1.02240.8656 CAR (-36, 0)58-0.5400-0.76000.7163 CAR (0, +48)540.0233-0.09301.0643 Singapore CAR (-60, 0)300.22170.04840.7734 CAR (-36, 0)320.1884-0.09500.7176 CAR (0, +48)32-0.1849-0.37340.8080 Taiwan CAR (-60, 0)60-0.3139-0.41011.1270 CAR (-36, 0)710.0025-0.22440.8902 CAR (0, +48)93-0.0054-0.04090.6712

CAR (-36, 0) CAR (0, +48) Hong Kong CAR (-60, 0) CAR (-36, 0) CAR (0, +48) Singapore CAR (-60, 0) CAR (-36, 0) CAR (0, +48) Taiwan CAR (-60, 0) CAR (-36, 0) CAR (0, +48)")

23

23 Regression results of firm value changes around succession

24

24 Summary and Conclusion Specialized assets play a crucial role in the emergence of family ownership A tendency that entrepreneurial firms, through family successions, evolve into family owned and managed firms The slow (or lack of) diffusion of ownership and control can be explained by the desire to protect value associated with specialized assets A pronounced dissipation of firm value during succession, which is positively related to asset specificity

diffusion of ownership and control can be explained by the desire to protect value associated with specialized assets A pronounced dissipation of firm value during succession, which is positively related to asset specificity")

25

25 Succession: Corporate Governance and Product Market Competition Yin-Hua Yeh (NCTU, Taiwan)

")

26

Co-founded firms Asset specificity Family succession Firm value Family succession Firm value Corporate Governance Product Market Competition

27

NEW Sample Distribution and Successor Types Year Family member %Outsiders%Total 2000654.55%545.45%11 2001550.00%5 10 2002337.50%562.50%8 2003861.54%538.46%13 2004937.50%1562.50%24 2005787.50%112.50%8 2006853.33%746.67%15 2007753.85%646.15%13 2008430.77%969.23%13 Total 5749.57%5850.43%115

28

28 Original sample : Successor Types The defined types include ‘ Family member ’, ‘ Outsiders ’ and ‘ Sold-out ’. ‘ Unknown ’ is for firms whose successor type is unclear. We further differentiate the succession type of ‘ Family members ’ into heir succession ‘ Heir ’ and ‘ Relative ’, of which successors are close relatives such as brothers or nephews. Hong KongSingaporeTaiwanTotal Family member 4369%1736% 8074% 14065% Heir 1829%49%5753%7936% Relative 2540%1328%2321%6128% Outsiders 610%1736%2422%4722% Sold-out 1321%817%44%2512% Unknown 00%511%00%52% Total62 100% 47 100% 108 100% 217 100%

29

NEW Sample Distribution and Successor Types Industry Family member %Outsiders%Total Textile and Fiber666.67%333.33%9 Electronics1330.95%2969.05%42 Construction571.43%228.57%7 Rubber150.00%1 2 Plastic240.00%360.00%5 Oil, Utility1100.00%00.00%1 Electronic Machinery350.00%3 6 Paper150.00%1 2 Transportation375.00%125.00%4 Electric Appliance and Cable 150.00%1 2 Automobile1100.00%00.00%1 Cement2100.00%00.00%2 ……………………

30

NEW Sample Summary Statistics of Independent Variables VariablesMeanStd. Dev.Median Founder0.520.5021 Co-founded0.400.4990 Family managed2.672.2753 Bank relation (%)8.559.714.3 Size (million NT $)20,26252,191,4,863 Company Age33.7212.4935 Education2.190.7932 Experience0.530.511 Electronic industry0.370.490 Ultimate voting rights31.8819.4729.27 Ultimate cash flow rights23.1617.6619.93

Size (million NT $)20,26252,191,4,863 Company Age Education Experience Electronic industry Ultimate voting rights Ultimate cash flow rights")

31

31 Original sample Summary Statistics of Independent Variables VariableObs.MeanMedianStd. Dev. Founder2170.55301.000.4983 Amenity2170.0553-0.2291 Co-founded2170.0461-0.2101 Family managed2102.44762.00001.5027 Bank relation2160.09390.04910.1434 Experience2170.4378-0.4973 Education2170.56681.00000.4967 Size21711.822011.83151.4940 Ultimate ownership2020.33550.31060.2180

32

NEW Sample Comparisons with Successor Types Family memberOutsiders MeanStd. Dev.MeanStd. Dev.t value Founder0.480.5050.560.501-0.795 Co-founded0.330.4740.560.501-2.414** Family managed3.442.1091.862.1763.729*** Labor intensity (%)5.749.51.973.322.652*** Bank relation (%)9.19.77.979.790.589** Log (Size)15.61.4115.481.460.424 Company Age37.2911.6073012.3983.066*** Education2.290.8252.080.7521.333 Experience0.630.4860.420.4992.201*** Electronic industry0.270.4480.50.505-2.444*** Ultimate cash flow rights (%) 26.1317.7219.9517.21.766** Ultimate voting rights (%)32.7419.2530.9319.860.463

*** Bank relation (%) ** Log (Size) Company Age *** Education Experience *** Electronic industry *** Ultimate cash flow rights (%) ** Ultimate voting rights (%)")

33

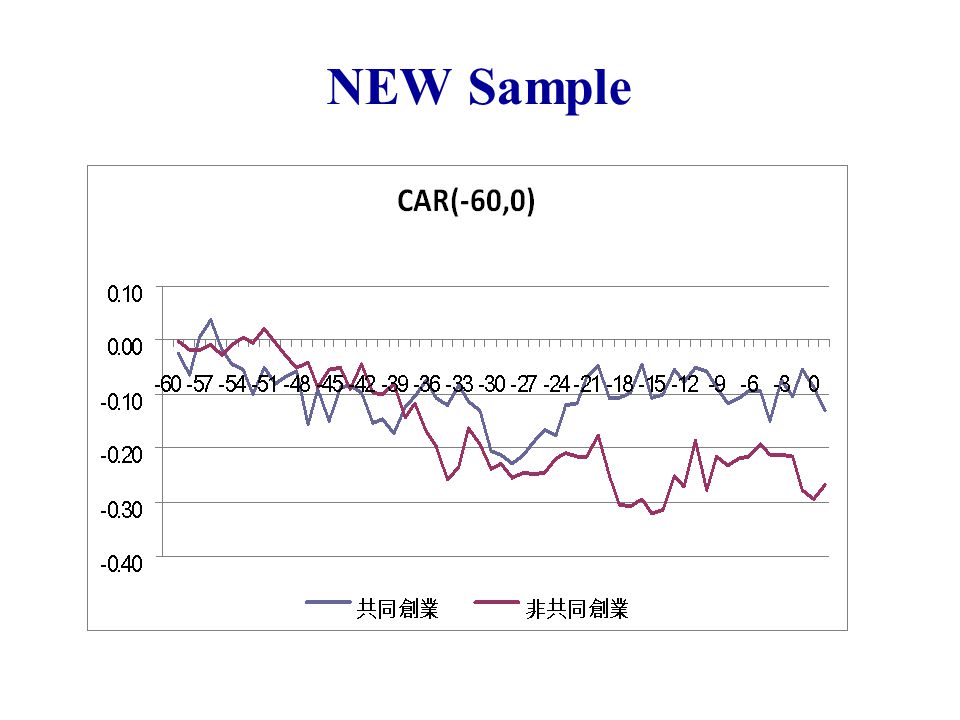

NEW Sample

34

34 Original sample Statistics of Abnormal Stock Returns around Succession VariableObs.MeanMedianStd. Dev. Full sample CAR (-60, 0)144-0.5558-0.54121.1225 CAR (-36, 0)161-0.1560-0.27280.8471 CAR (0, +48)179-0.0288-0.07540.8302 Hong Kong CAR (-60, 0)54-1.2567-1.02240.8656 CAR (-36, 0)58-0.5400-0.76000.7163 CAR (0, +48)540.0233-0.09301.0643 Singapore CAR (-60, 0)300.22170.04840.7734 CAR (-36, 0)320.1884-0.09500.7176 CAR (0, +48)32-0.1849-0.37340.8080 Taiwan CAR (-60, 0)60-0.3139-0.41011.1270 CAR (-36, 0)710.0025-0.22440.8902 CAR (0, +48)93-0.0054-0.04090.6712

CAR (-36, 0) CAR (0, +48) Hong Kong CAR (-60, 0) CAR (-36, 0) CAR (0, +48) Singapore CAR (-60, 0) CAR (-36, 0) CAR (0, +48) Taiwan CAR (-60, 0) CAR (-36, 0) CAR (0, +48)")

35

NEW Sample

37

The Role of Co-founded Firms Co-founded firms are subject to more serious infighting for property right re-distribution during succession. However, co-founded firms can mitigate the transfer costs in succession because they are mutually managed and monitored. the shareholdings of co-founders

38

Product market competition Can help entrepreneurial firms professionalize their business early on to mitigate the transfer costs in succession. More serious agency problems are in noncompetitive industries, and competitive forces can reduce the need for shareholders to bear the costs of monitoring agents and increase the frequency of CEO turnover (Giroud and Muller, 2011; Leventis, et al.,2011; de Bettignies and Baggs,2005; De Fond and Park, 1999)

.")

39

CG index Can help entrepreneurial firms systematize their business before succession. CGI is a composite corporate governance index (Yeh, Shu and Su, 2012) Controlling shareholders’ cash flow rights cash/control the proportion of the directory membership being controlled by the controlling shareholders the proportion of supervisory membership being controlled by the controlling shareholders the proportion of directors’ and supervisors’ shareholdings being pledged to bank loans the proportion of related-party sales the proportion of related-party loans and the proportion of related-party loan guarantees

Controlling shareholders’ cash flow rights cash/control the proportion of the directory membership being controlled by the controlling shareholders the proportion of supervisory membership being controlled by the controlling shareholders the proportion of directors’ and supervisors’ shareholdings being pledged to bank loans the proportion of related-party sales the proportion of related-party loans and the proportion of related-party loan guarantees.")

40

Preliminary Results Assets specificity also provide good explanation of successor choice The negative relation between Co-founded firms and CAR disappear and change to a positive relation when co-founders hold high shareholdings. We expect product market competition and governance quality will moderate the probability of family succession and the value loss during succession

Similar presentations

, Shaun Bond (University of Cincinnati), & Joseph Ooi (National University of Singapore)>")

: Public Pension Fund Activism n 1996: Public pension funds own over $300 billion; 30% of corporate equity. n Political pressure on Public.>")

Director, Centre of Economics & Finance Professor, School.>")