Download presentation

Presentation is loading. Please wait.

1

Investor Update AGM November 2008

2

AGENDA Depth and duration of global recession? How long will the bear market last? Portfolio strategy Investment process Performance

3

Economic Outlook Systemic risk of financial system failure may have past Deleveraging cycle has began ensuring sub- optimal growth for some time to come Leading indicators are suggesting the global economy is in for a protracted recession Australian economy unlikely to soften as much as G7. Outcome will depend on quantum of policy support and economic strength of trading partners

4

Credit markets are improving

5

US Retail Sales (Year on Year % Change) US Unemployment

US Unemployment")

7

Australian Economy Outcome less clear Supportive Strong financial system Monetary Stimulus Fiscal Support Drag Softer global growth Credit rationing Household deleveraging Resources Growth in Emerging Asia? Infrastructure Business Investment

8

Treasury Estimates Look Optimistic

9

Resources and Infrastructure have been a big support for the economy, if this were to reverse recession will be much deeper

10

Market Outlook While the downturn in activity might not be as bad as offshore, local shares will inevitably taking their lead from International markets Shares are already priced for a sharp correction in 2009 earnings. The unknown is the shape of the recovery, are we in for a long period of sub-optimal growth? If so it is difficult to envisage a strong recovery in the value of risk assets.

11

BUY SIGNAL Equities outstanding value in absolute sense Equities outstanding value versus other risk assets Valuation Speculative interests have been unwound Hedge fund cash positions at record levels Capitulation Outlook will improve as we move forward Hard to envisage any further deterioration Fundamentals “I am fearful when others are greedy and greedy when others are fearful” Warren Buffet VIX Index measure of volatility at record levels Risk

13

2 Years of negative returns are rare

14

Market Cheap on Balance Sheet measures

15

Market Cheap on prospective profits (forecasts are to high)

")

16

Earnings Bubble Vs Price Bubble in 2000

17

Same story in Australia

18

Hedge Fund Capitulation (US Equity Holdings- Sept qtr V June qtr) June 30-2008Sept 30-2008 Appaloosa$3.1bn$648m Atticus$8.1bn$510m Tudor$5.7bn$453m Vinik$11.8bn$1.8m Moore Capital$4.5bn$1.4bn Jana$5.9bn$2.1bn SAC$14.4bn$7.7bn

June Sept Appaloosa$3.1bn$648m Atticus$8.1bn$510m Tudor$5.7bn$453m Vinik$11.8bn$1.8m Moore Capital$4.5bn$1.4bn Jana$5.9bn$2.1bn SAC$14.4bn$7.7bn")

19

Defensive sectors have outperformed

20

Portfolio Strategy Investors have pushed the premium on earnings certainty and balance sheet strength to extremes Heavy supply of new equity continues as companies recapitalise balance sheets Earnings risk still to downside

21

Sector Strategy- no where to hide Banks are still at risk from emerging non performing loans and a slowing credit cycle Resources will struggle as growth expectations and commodity prices move lower Domestic Cyclicals will struggle as earnings disappoint with the economy slowing Property will see ongoing equity supply and downward revisions to valuations

22

Everything is on sale- a winning strategy is to: Stick to stronger companies, investors will be surprised at the contraction in weaker businesses. In this environment the strong get stronger and the weak fall by the wayside. Avoid leveraged balance sheets as these companies will inevitably have to recapitalise Cash is the only truly defensive asset, so called “defensive companies” are overvalued Buy cheap structural growth companies, the structurally impaired may not make it through this downturn

23

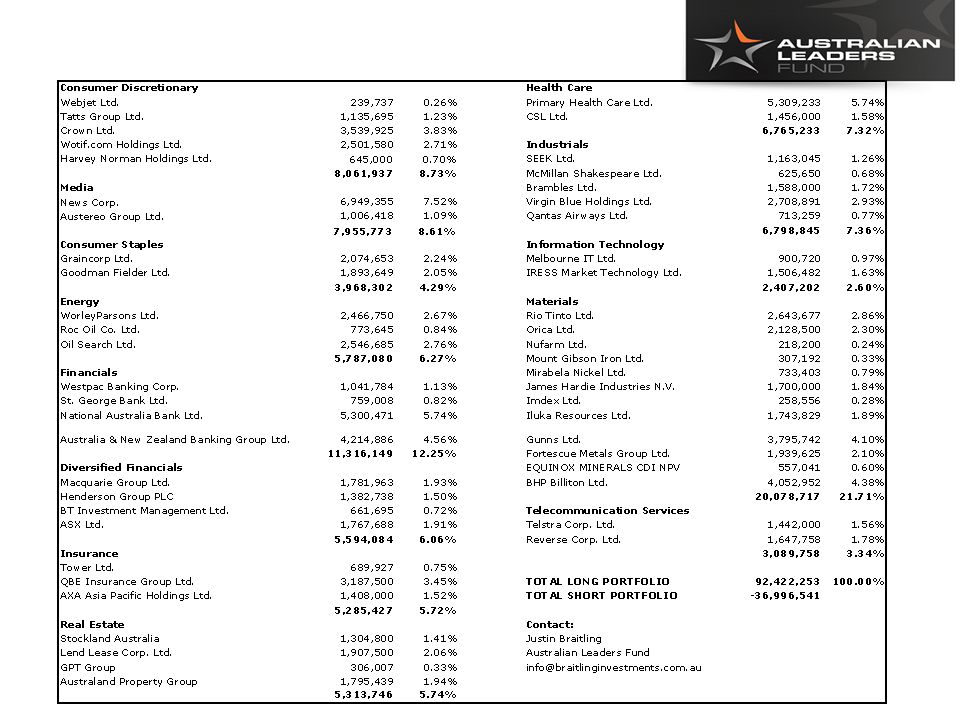

Investments Portfolio (Top 10) NEWS CORP PRIMARY HEALTHCARE OIL SEARCH ANZ Bank WESTPAC BANKING NATIONAL AUSTRALIA BANK ARISTOCRAT LEISURE BRAMBLES LIMITED WOOLWORTHS LIMITED HENDERSON GROUP PLC CompanyQualitative Score Management Score Target Upside NEWS CORP ## HARVEY NORMAN ## CROWN LTD ## PRIMARY HEALTHCARE ## WESTPAC BANKING CORP ## AXA ## SEEK LTD ## COCA-COLA AMATIL LTD ## WOOLWORTHS LIMITED ## TELSTRA ## SINGAPORE TELECOM ## WESFARMERS LTD. ## AMCOR ## COMMONWEALTH BANK ## MACMAHON HOLDINGS ## HEALTHSCOPE ## AUSTAR UNITED ## BANK OF QUEENSLAND ## BENDIGO BANK LIMITED ## ADELAIDE BRIGHTON ## INVESTMENT UNIVERSE RANKED (1-200) ASX200 TOP Quartile ASX 200 Bottom Quartile TARGET 3% OUTPERFORMANCE

ASX200 TOP Quartile ASX 200 Bottom Quartile TARGET 3% OUTPERFORMANCE.")

24

Investments Portfolio (Top 10) NEWS CORP PRIMARY HEALTHCARE OIL SEARCH ANZ Bank WESTPAC BANKING NATIONAL AUSTRALIA BANK ARISTOCRAT LEISURE BRAMBLES LIMITED WOOLWORTHS LIMITED HENDERSON GROUP PLC CompanyQualitative Score Management Score Target Upside NEWS CORP ## HARVEY NORMAN ## CROWN LTD ## PRIMARY HEALTHCARE ## WESTPAC BANKING CORP ## AXA ## SEEK LTD ## COCA-COLA AMATIL LTD ## WOOLWORTHS LIMITED ## TELSTRA ## SINGAPORE TELECOM ## WESFARMERS LTD. ## AMCOR ## COMMONWEALTH BANK ## MACMAHON HOLDINGS ## HEALTHSCOPE ## AUSTAR UNITED ## BANK OF QUEENSLAND ## BENDIGO BANK LIMITED ## ADELAIDE BRIGHTON ## INVESTMENT UNIVERSE RANKED (1-200) Funding Portfolio SINGAPORE TELECOM MACQUARIE INFRAST GRP AMCOR HEALTHSCOPE TRANSURBAN TOWER AUSTRALIA BANK OF QUEENSLAND BENDIGO BANK LIMITED ADELAIDE BRIGHTON LION NATHAN ASX200 TOP Quartile ASX 200 Bottom Quartile

Funding Portfolio SINGAPORE TELECOM MACQUARIE INFRAST GRP AMCOR HEALTHSCOPE TRANSURBAN TOWER AUSTRALIA BANK OF QUEENSLAND BENDIGO BANK LIMITED ADELAIDE BRIGHTON LION NATHAN ASX200 TOP Quartile ASX 200 Bottom Quartile.")

25

ALF L PORTFOLIO $78m $50m Assets $128m ALF Balance Sheet Funding $128m SHAREHOLDER’S FUNDS $78m SHORTS / DEBT $50m TARGET 3% OUTPERFORMANCE ALF L TARGET 3% UNDERPERFORMANCE ALFs ALF s + Market +3% Market - 3% Market +7%

26

SHORT FUNDING IS DIFFERENT TO FINANCIAL LEVERAGE FROM DEBT

27

1 MONTH3 MONTHS6 MONTHS1 YEAR PORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADD -15.9%-13.9%-2.0%-15.9%-20.0%4.1%-21.3%-28.0%6.7%-33.4%-38.7%5.3% 2 YEARS (ANNUALISED)3 YEARS (ANNUALISED)SINCE INCEPTION (ANNUALISED)SINCE INCEPTION (CUMULATIVE) PORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADD -8.0%-10.3%2.3%5.2%0.6%4.5%9.3%8.5%0.8%51.5%46.6%4.8% COMPARATIVE PERFORMANCE

3 YEARS (ANNUALISED)SINCE INCEPTION (ANNUALISED)SINCE INCEPTION (CUMULATIVE) PORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADDPORTFOLIOBENCHMARKVALUE ADD -8.0%-10.3%2.3%5.2%0.6%4.5%9.3%8.5%0.8%51.5%46.6%4.8% COMPARATIVE PERFORMANCE")

Similar presentations

, detail from “The Red Sun”, oil on board, Sanlam Art Collection. FIA Meeting 16 October 2012.>")